- Inks, Coatings, Adhesives & Sealants (ICAS)

- Rosin Resin Market

Rosin Resin Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Rosin Resin Market by Product Type (Rosin Acids, Rosin Esters, Hydrogenated Rosin Resins, Dimerized Rosin Resins, Modified Rosin Resins), Source (Gum Rosin, Tall Oil Rosin, Wood Rosin), Application (Rubbers, Coatings, Inks, Adhesives, Food & Beverages, Cosmetics & Personal Care, Others), by Regional Analysis, 2025 - 2032

Rosin Resin Market Size and Trend Analysis

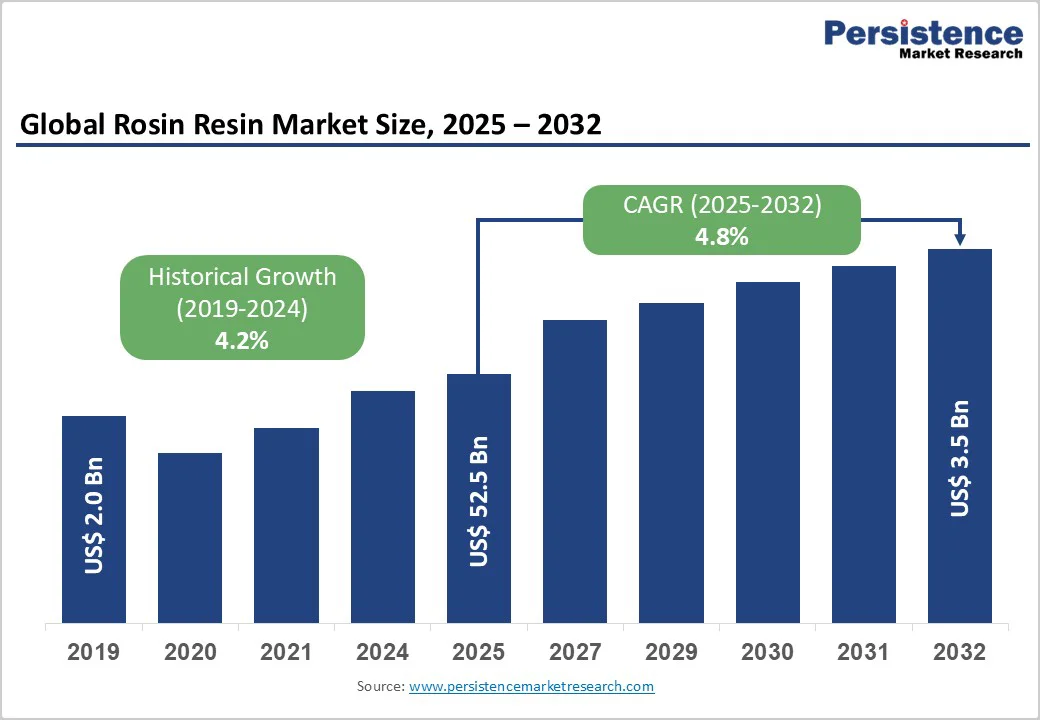

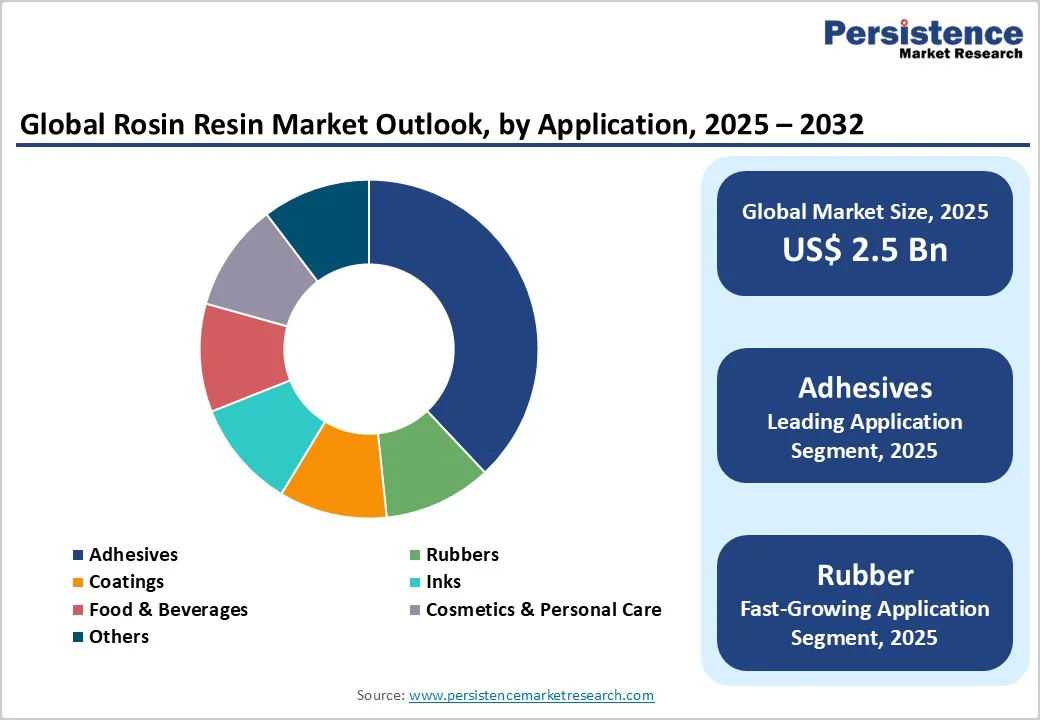

The global rosin resin market size is likely to value at US$ 2.5 billion in 2025 and is projected to reach US$ 3.5 billion, growing at a CAGR of 4.8% between 2025 and 2032. The market expansion is driven primarily by increasing demand from adhesives, coatings, and rubber industries where rosin resin serves as a critical bio-based tackifier and binding agent.

The shift toward sustainable and renewable chemical alternatives over petroleum-based materials is accelerating adoption across packaging, construction, and automotive sectors, as rosin resin offers superior environmental credentials while maintaining excellent adhesion, tack, and thermal stability properties that are essential for modern industrial applications.

Key Market Highlights

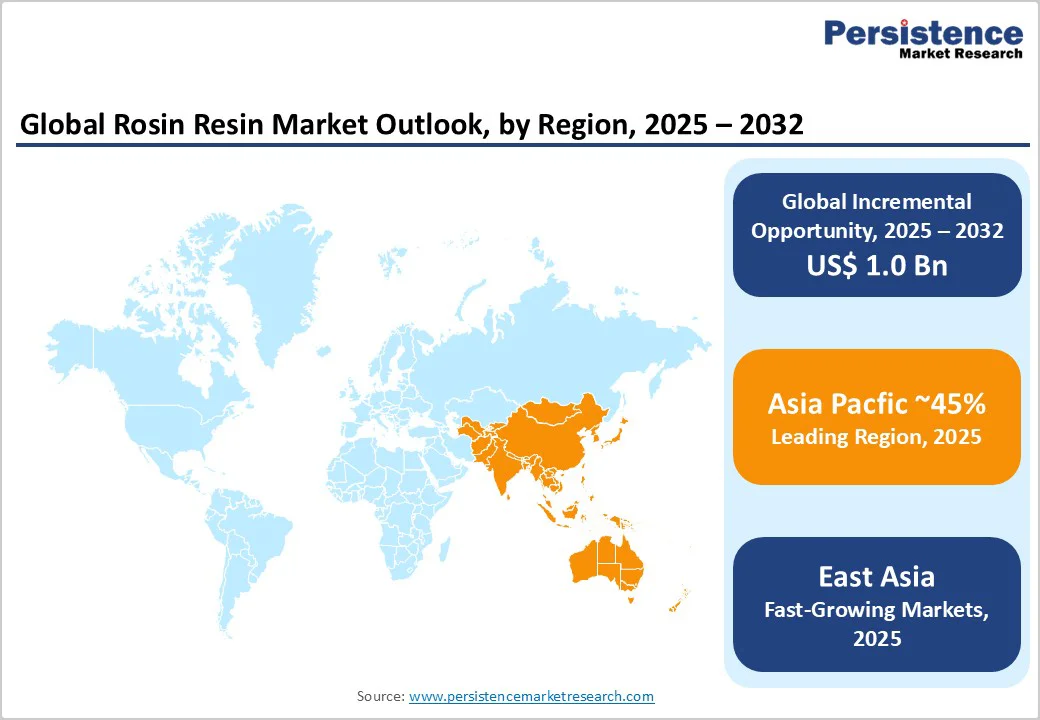

- Leading Region: Asia Pacific dominates the rosin resin market with approximately 45% revenue share, driven by substantial consumption across adhesives, rubber, coatings, and printing applications supported by rapid industrialization and expanding manufacturing sectors.

- Fastest Growing Region: East Asia demonstrates the highest growth trajectory at over 5% CAGR, propelled by robust industrial expansion in China, Japan, and South Korea.

- Dominant Segment: Rosin Esters command approximately 42% of the product type segment driven by superior stability, compatibility, and performance characteristics in hot-melt adhesives.

- Fastest Growing Segment: Adhesives application segment represents the most dynamic growth area at over 5% CAGR, driven by expanding packaging industry demand, growing construction adhesive requirements, and automotive assembly applications.

- Key Market Opportunity: Expanding applications in food packaging and pharmaceutical industries present substantial growth potential, with FDA-approved glycerol rosin esters serving antimicrobial food contact materials.

| Key Insights | Details |

|---|---|

|

Rosin Resin Market Size (2025E) |

US$ 2.5 Bn |

|

Market Value Forecast (2032F) |

US$ 3.5 Bn |

|

Projected Growth CAGR (2025-2032) |

4.8% |

|

Historical Market Growth (2019-2024) |

4.2% |

Market Dynamics

Drivers - Rise in Demand for Bio-Based and Sustainable Materials Across Industrial Applications

The global transition toward sustainable and renewable resources is fundamentally reshaping the chemical industry landscape, with rosin resin emerging as a preferred bio-based alternative to petroleum-derived synthetic resins. Extracted from pine trees through environmentally responsible tapping processes, rosin resin offers biodegradability and renewable sourcing advantages that align with increasingly stringent environmental regulations and corporate sustainability commitments.

According to the U.S. Environmental Protection Agency (EPA), demand for renewable chemical inputs has grown by over 12% annually since 2019. The palm oil market, valued at US$ 76.8 billion in 2025, demonstrates parallel growth in bio-based materials, while the pine-derived chemicals market is projected to reach US$ 9.6 billion by 2035 with a CAGR of 4.4%, creating a supportive ecosystem for rosin resin adoption across complementary applications in adhesives, paints, and surfactants where sustainability credentials are increasingly non-negotiable.

Robust Growth in Adhesives and Rubber Industries Driven by Construction and Automotive Sectors

The adhesives industry represents a critical growth driver for rosin resin consumption, with applications spanning hot-melt adhesives, pressure-sensitive adhesives, and industrial bonding solutions across packaging, construction, and automotive manufacturing. Rosin resin functions as an essential tackifier that enhances initial stickiness and bonding performance, typically accounting for 30-50% of adhesive formulations while delivering cost-effective performance enhancement.

Research published in the Journal of Applied Polymer Science in 2024 demonstrates that rosin resin-based composites enhance cut growth resistance and tear strength in tire tread compounds by approximately 35% compared to conventional formulations. Additionally, the construction sector's expansion, particularly in the Asia Pacific, where infrastructure investment exceeded US$ 1.5 trillion in 2024, is generating substantial demand for rosin-based adhesives used in flooring, lamination, and wood panel applications, while automotive production growth in emerging markets further amplifies consumption across sealing, bonding, and interior component manufacturing applications.

Restraints - Raw Material Price Volatility and Supply Chain Vulnerabilities

The rosin resin market faces significant challenges related to raw material availability and price fluctuations, as production depends entirely on pine resin extraction from live trees or processing of pine stumps and tall oil byproducts from kraft paper manufacturing. Global pine resin supply is concentrated in specific geographical region creating supply concentration risks. Climate variations, forest fires, regulatory restrictions on pine tapping practices, and competing land uses for pine forests contribute to supply uncertainty and periodic price spikes that impact manufacturing cost structures. The 2023-2024 period witnessed pine resin prices fluctuate by 15-20% due to reduced tapping activities in key producing regions of Guangxi and Yunnan provinces in China, affecting downstream rosin resin production economics and forcing manufacturers to absorb margin pressure or pass costs to end users in highly price-sensitive applications.

Competition from Synthetic Alternatives and Performance Limitations

Despite its sustainability advantages, rosin resin faces competitive pressure from petroleum-based synthetic resins including hydrocarbon resins, phenolic resins, and polyurethane systems that offer superior thermal stability, color retention, and performance consistency in demanding applications. Unmodified rosin exhibits inherent limitations including oxidative instability, tendency toward color degradation, and brittleness that restrict usage in high-performance coatings and adhesives without chemical modification through hydrogenation, esterification, or disproportionation processes. These modification steps add processing costs and complexity, narrowing the cost advantage versus synthetic alternatives. Synthetic resin alternatives captured shows strong penetration in specialty adhesive segments where performance requirements exceed rosin's technical capabilities even with modification, representing a structural competitive challenge for market expansion.

Opportunity - Expanding Applications in Food Packaging and Pharmaceutical Industries

The food packaging sector presents substantial growth opportunities as manufacturers seek biodegradable, food-safe alternatives to conventional plastic-based materials. Recent research published in the International Journal of Biological Macromolecules in 2024 demonstrates that rosin-based antimicrobial coatings significantly enhance food packaging performance by providing hydrophobic barriers while maintaining breathability and incorporating natural antibacterial properties against gram-positive and gram-negative bacteria. The pharmaceutical industry is increasingly utilizing hydrogenated rosin esters in controlled drug release systems, transdermal patches, and taste-masking applications, capitalizing on rosin's film-forming ability, biocompatibility, and ease of chemical modification.

Technological Advancements in Modification Processes and Green Chemistry Innovation

Continuous innovation in rosin modification technologies is opening new opportunities to overcome performance limitations and expand market applications. Advanced processes such as hydrogenation, esterification, and polymerization are producing next-generation rosin resins with improved thermal stability, lighter color, reduced odor, and enhanced compatibility with modern polymers. Kraton Corporation’s REvolution™ Rosin Ester technology, launched in 2024, enables adhesive formulators to reduce scope 3 greenhouse gas emissions while maintaining adhesion and color stability, demonstrating that sustainability and performance can advance together. Emerging applications in UV-curable systems, high-performance coatings, and electronics benefit from tailored rosin derivatives. Water-dispersible formulations meet demand for low-VOC, environmentally compliant products, while integrated bio-refinery approaches improve economics and sustainability, offering vertically integrated producers opportunities to differentiate across the pine chemicals value chain.

Category-wise Insights

Product Type Analysis

Rosin Esters dominate the rosin resin market with an estimated 42% market share, driven by their superior stability, compatibility, and performance characteristics compared to unmodified rosin acids. Pentaerythritol rosin esters demonstrate particularly strong performance in high-temperature adhesive applications and food-contact materials due to their molecular structure providing four esterification sites that enhance thermal stability. Glycerol rosin esters hold FDA approval for food applications and serve critical roles in chewing gum formulations and food packaging materials, representing a specialized high-value segment. The dominance of rosin esters reflects the industrial preference for modified materials that balance natural origin with performance characteristics approaching synthetic alternatives while maintaining significant cost advantages in adhesive and coating formulations.

Source Analysis

Gum Rosin commands the largest market share at approximately 60% of global rosin supply, derived from tapping live pine trees. China dominates gum rosin production, accounting for 60% of global output, with Indonesia, Brazil, Mexico, and India serving as secondary producers. Gum rosin offers superior quality characteristics including lighter color, lower impurity content, and more consistent chemical composition compared to wood rosin or tall oil rosin alternatives, making it preferred for high-grade applications in adhesives, coatings, and pharmaceutical formulations. The segment’s growth is supported by increasing demand for premium-grade rosin in electronics solder flux, specialty adhesives, and food-grade applications.

Application Analysis

Adhesives represent the largest and fastest-growing application segment, accounting for approximately 38% of global rosin resin consumption, driven by versatile applications across hot-melt adhesives for packaging and bookbinding, pressure-sensitive adhesives for labels and tapes, construction adhesives for flooring and panels, and automotive assembly applications. Rosin derivatives function as essential tackifiers that enhance initial grab, peel adhesion, and bonding strength across diverse polymer systems including styrene-butadiene rubber (SBR), ethylene-vinyl acetate (EVA), and acrylic emulsions. The rubber segment, primarily tire manufacturing, accounts for 24% of rosin resin demand, utilizing rosin as a plasticizer, processing aid, and compound ingredient that improves green tack, dispersion of fillers like carbon black and silica, and final performance characteristics including wet grip and rolling resistance.

Regional Insights

North America Rosin Resin Market Trends

North America maintains a significant market position with the United States driving approximately 85% of regional rosin resin demand, supported by established adhesives, coatings, and rubber industries alongside strong regulatory frameworks promoting bio-based materials. The region benefits from domestic tall oil rosin production as a kraft paper manufacturing byproduct, with major pulp mills in the Southeastern United States providing integrated supply chains for rosin derivatives.

Regulatory trends favor rosin adoption, with the U.S. Environmental Protection Agency promoting bio-based alternatives through the BioPreferred Program that certifies and promotes rosin-containing products. The packaging industry's growth, particularly e-commerce-driven corrugated box demand, supports hot-melt adhesive consumption where rosin esters serve critical tackifying roles. The region's mature market characteristics emphasize quality, regulatory compliance, and sustainability credentials over pure cost considerations, positioning rosin derivatives favorably in premium application segments such as food packaging, pharmaceutical excipients, and electronics materials.

Europe Rosin Resin Market Trends

Europe represents a mature market characterized by stringent environmental regulations, strong sustainability commitments, and advanced technical requirements driving demand for high-performance modified rosin derivatives. Germany commands approximately 28% of European market share with 4.5% projected growth through 2032, driven by automotive, construction adhesives, and specialty coatings sectors where rosin esters provide bio-based alternatives meeting REACH compliance requirements.

The United Kingdom, France, Spain, and Italy collectively represent substantial demand centers supported by rubber, construction and automotive applications. European manufacturers emphasize product innovation, with companies like DRT (France) leading in bio-based tackifier development and sustainable sourcing practices.

The European pharmaceutical and food packaging industries demonstrate growing interest in food-grade glycerol rosin esters for applications requiring biocompatibility and regulatory approval, positioning the region as a key market for high-purity specialty rosin derivatives where technical performance and sustainability documentation justify premium pricing compared to commodity-grade alternatives.

Asia Pacific Rosin Resin Market Trends

Asia Pacific dominates global rosin resin markets with approximately 45% revenue share, driven by China's position as the world's largest producer and consumer accounting for 60% of gum rosin output and substantial downstream processing capacity for modified derivatives. The region demonstrates the fastest growth trajectory at over 5% CAGR, supported by rapid industrialization, expanding manufacturing sectors, and growing consumption across adhesives, rubber, coatings, and printing applications.

Japan represents a sophisticated market emphasizing quality and technical innovation, driven by automotive coatings, electronics applications, and specialty adhesives where performance requirements demand premium-grade hydrogenated and esterified rosin derivatives. India demonstrates strong growth potential with expanding rubber, adhesives, and coatings industries consuming increasing quantities of imported gum rosin and domestically produced tall oil rosin.

Southeast Asian countries including Indonesia, Thailand, Vietnam, and Malaysia demonstrate growing consumption driven by expanding manufacturing sectors, packaging industry growth, and automotive production expansion, positioning Asia Pacific as the dominant force shaping global rosin resin market.

Competitive Landscape

The rosin resin market demonstrates a moderately fragmented competitive landscape with a mix of large multinational chemical companies and regional specialty producers. Key market differentiators include vertical integration capabilities from pine resin sourcing through modified derivatives production, technological expertise in advanced modification processes like selective hydrogenation and esterification, product quality consistency and color stability, regulatory approvals for food-contact and pharmaceutical applications, and sustainability certifications including RSPO recognition for responsible forest management.

Leading global players including Eastman Chemical Company, Arakawa Chemical Industries, Ltd., and Ingevity Corporation emphasize R&D investment to develop next-generation rosin derivatives with enhanced performance, while regional producers compete through cost advantages and proximity to raw material sources. Strategic initiatives focus on capacity expansion in high-growth Asian markets, development of bio-based product portfolios aligned with sustainability trends, partnerships with end-use manufacturers in adhesives and coatings sectors, and vertical integration to secure pine resin supply chains amid growing demand and potential supply constraints.

Key Market Developments:

- March 2024: Henkel and Kraton Corporation signed a multi-year supply agreement for REvolution™ rosin ester technology to develop sustainable adhesive solutions with reduced environmental impact across global markets.

- April 2024: Dow Inc., Henkel and Kraton stated that two of Henkel’s Technomelt® adhesives achieved a ~25 % cradle-to-gate carbon footprint reduction through use of Kraton’s SYLVALITE™ 2200 biobased tackifiers developed with REvolution™ rosin ester technology.

Companies Covered in Rosin Resin Market

- Eastman Chemical Company

- Arakawa Chemical Industries, Ltd.

- Lawter Inc.

- Forestarchem Chemical Co., Ltd.

- Indonesia Pinus

- Jinggu Forest Chemical Co. Ltd.

- G.C. RUTTEMAN & Co.

- Promax Industries

- Resin Chemicals Co., Ltd.

- Foreverest Resources Ltd.

- Guilin Songquan Forest Chemical Industry Co., Ltd.

- CV. Indonesia Pinus

- Hindustan Resins & Terpenes

- Harima Chemicals Group

- Ingevity Corporation

- Kraton Corporation

- DRT (Dérivés Résiniques et Terpéniques)

- Florachem Corporation

- United Resins SA

- Wuzhou Sun Shine Forestry and Chemicals

Frequently Asked Questions

The global rosin resin market is projected to reach US$ 3.5 billion by 2032, growing at a CAGR of 4.8% from 2025 to 2032.

The primary demand drivers include the global transition toward sustainable bio-based materials over petroleum-derived alternatives, robust growth in adhesives and rubber industries driven by packaging and automotive sectors.

Rosin Esters dominate the market with approximately 42% share, driven by their superior stability, compatibility, and performance characteristics compared to unmodified rosin acids.

Asia Pacific dominates with approximately 45% revenue share, led by China which accounts for 60% of global gum rosin production at 400,000-450,000 metric tons annually.

Technological advancements in modification processes enabling enhanced performance, development of water-dispersible low-VOC formulations, and growing demand for bio-based materials in specialty applications present substantial growth potential.

Key market players include Eastman Chemical Company, Arakawa Chemical Industries, Ltd., Lawter Inc., Forestarchem Chemical Co., Ltd., Ingevity Corporation, Kraton Corporation, among others.