- Industrial Machinery

- Thailand Water Pump Market

Thailand Water Pump Market Size, Share, and Growth Forecast 2026 - 2033

Thailand Water Pump Market by Pump Type (Centrifugal Pumps, Positive Displacement Pumps, Submersible Pumps, Booster Pumps), Power Source (Electric Pumps, Diesel Pumps, Solar Pumps, Hybrid Pumps), Application (Agriculture & Irrigation, Municipal & Water Utilities, Industrial, Commercial), End-user (Households, Farmers, Industrial Facilities, Municipal Authorities), 2026 - 2033

Thailand Water Pump Market Size and Trend Analysis

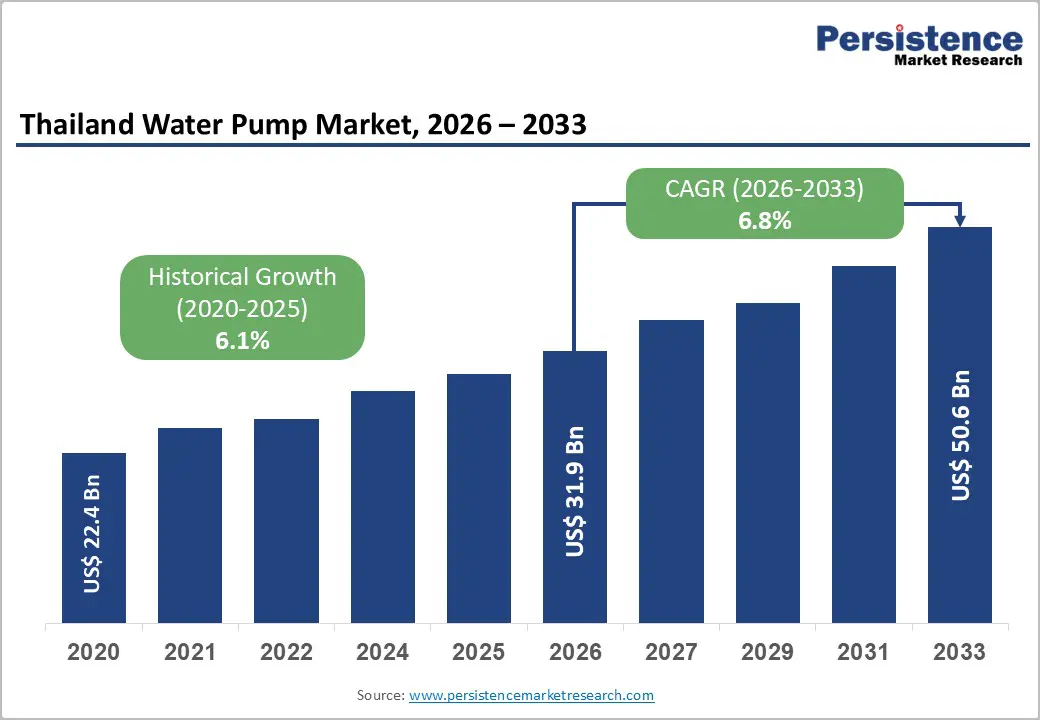

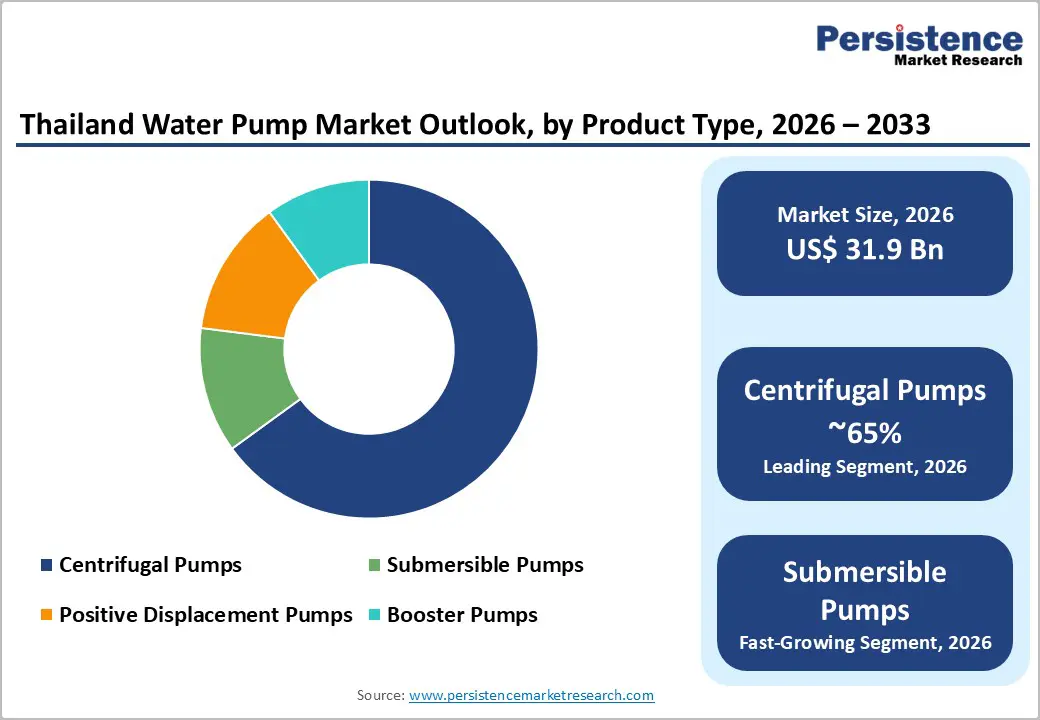

The Thailand water pump market size is likely to be valued at US$ 31.9 Billion in 2026 and is expected to reach US$ 50.6 Billion by 2033, growing at a CAGR of 6.8% during the forecast period from 2026 and 2033.

Market growth is driven primarily by the expansion of the Eastern Economic Corridor (EEC) and the urgent need for efficient water management systems amid fluctuating weather patterns. Thailand's agricultural sector, a cornerstone of the economy, is rapidly adopting modern irrigation technologies, such as solar-powered pumps, supported by government incentives, including the "Quick Big Win" policy.

Key Industry Highlights:

- Dominant Segment: Centrifugal Pumps remain the dominant product segment, favored for their versatility and cost-effectiveness across both the massive agricultural sector and industrial applications.

- Fastest Growing Segment: Solar Pumps are the fastest-growing category, supported by the "Quick Big Win" government policy and tax incentives aimed at reducing agricultural energy costs and carbon emissions.

- Key Market Opportunity: Smart/IoT Water Management presents a critical opportunity, with municipal and industrial sectors seeking intelligent pumping systems to reduce non-revenue water and comply with Thailand 4.0 efficiency goals.

| Key Insights | Details |

|---|---|

| Thailand Water Pump Market Size (2026E) | US$ 31.9 Billion |

| Market Value Forecast (2033F) | US$ 50.6 Billion |

| Projected Growth CAGR (2026 - 2033) | 6.8% |

| Historical Market Growth (2020 - 2025) | 6.1% |

Market Dynamics

Market Growth Drivers - Government Incentives and Renewable Energy Adoption Driving Solar Pump Demand Across Thailand’s Agricultural Sector

The growing shift toward renewable energy in Thailand’s agricultural sector is a major driver for the water pump market. As part of the national carbon-neutrality agenda, the government has introduced strong policy support through the Department of Alternative Energy Development and Efficiency (DEDE). Subsidies, tax rebates, and incentive programs have made solar-powered pumps more affordable for farmers. Recent tax policies allow households and agricultural users to claim deductions of up to 200,000 THB for installing solar systems, significantly lowering the financial burden.

These incentives directly address rising diesel fuel costs and unreliable electricity supply in rural regions. Solar pumps offer a dependable solution for farmers operating in remote, off-grid areas where grid access is limited. Their ability to function independently ensures uninterrupted irrigation, especially during dry seasons. This transition supports Thailand’s broader goal of modernizing agricultural infrastructure, improving water security, and promoting sustainable farming practices nationwide.

Eastern Economic Corridor Development Accelerating Demand for Industrial Water Pumps and Advanced Water Management Systems

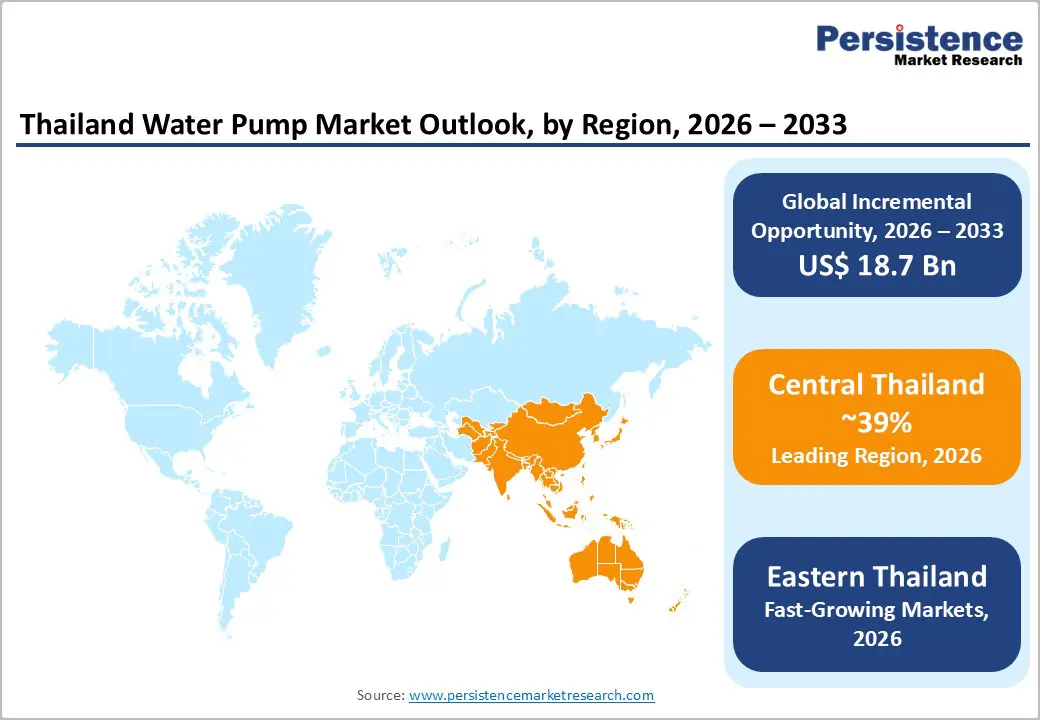

The rapid development of the Eastern Economic Corridor (EEC) is creating strong demand for industrial water pumping systems. Covering key provinces such as Rayong, Chonburi, and Chachoengsao, the EEC has become a major hub for manufacturing, petrochemicals, electronics, and automotive industries. The Industrial Estate Authority of Thailand (IEAT) enforces strict water management regulations, requiring factories to install advanced pre-treatment, wastewater recycling, and desalination systems.

As new industrial estates and production clusters continue to expand, demand for high-capacity centrifugal and positive displacement pumps has increased sharply. These pumps are essential for cooling systems, wastewater treatment, and process water circulation. According to estimates from the Office of National Water Resources, industrial water demand in the EEC will rise substantially over the next decade. This growth will require an additional watershed capacity of more than 350 million cubic meters, directly driving long-term pump procurement.

Restraints - Rising Import Dependence and Price Competition Challenging Domestic Water Pump Manufacturers and Distributors in Thailand

One of the key challenges facing Thailand’s domestic water pump market is intense competition from low-cost imports, mainly from China and Vietnam. Trade statistics indicate that Thailand imported more than 872 water pump shipments in the last fiscal year, reflecting strong year-on-year growth. While imports provide affordable options for buyers, they place significant pricing pressure on local manufacturers and distributors.

Domestic players often struggle to compete on cost rather than quality or innovation. In addition, local assemblers rely heavily on imported raw materials and advanced components, particularly for high-performance and industrial pumps. This dependence exposes the market to global supply chain disruptions, currency volatility, and rising logistics costs. As a result, profit margins are increasingly squeezed for local companies that lack the scale and cost advantages enjoyed by multinational manufacturers. These factors collectively limit the competitiveness of domestic suppliers in the long term.

High Upfront Costs and Income Volatility Limiting Modern Pump Adoption Among Small-Scale Farmers

Despite government incentives, the high upfront cost of modern pumping systems remains a significant barrier for small-scale farmers. These farmers represent a large share of the overall end-user base, especially in rural Thailand. While solar-powered and energy-efficient pumps offer clear long-term savings, their initial purchase and installation costs are considerably higher than traditional diesel or basic electric pumps.

Economic uncertainty, fluctuating crop prices, and unpredictable weather conditions often reduce farmers’ willingness or ability to invest in new equipment. Limited access to affordable financing further slows adoption. As a result, many farmers continue to rely on outdated and inefficient pumping systems that consume more fuel and require frequent maintenance. This financial sensitivity delays equipment upgrades and restricts mass adoption of advanced pumping technologies, particularly outside large-scale government irrigation schemes and subsidy-supported pilot projects.

Opportunity - Thailand 4.0 Strategy Creating Strong Opportunities for Smart, IoT-Enabled Pumping and Water Management Solutions

Thailand’s push toward digital transformation under the Thailand 4.0 strategy creates strong opportunities for smart, IoT-enabled water pumping solutions. Industrial estates, municipalities, and utility providers are increasingly looking for intelligent systems that support real-time monitoring, predictive maintenance, and remote operation. These features help reduce downtime, improve efficiency, and lower operating costs.

The Metropolitan Waterworks Authority (MWA) has set a clear objective to reduce non-revenue water (NRW) losses to below 20%, creating demand for smart booster pumps, pressure-controlled systems, and metering pumps integrated with centralized control platforms. IoT-based solutions also enable early leak detection and data-driven decision-making. Companies offering digital twin technology, cloud-based dashboards, and remote diagnostics alongside hardware products are well-positioned to gain market share. These solutions align strongly with Thailand’s smart city initiatives and the modernization of industrial infrastructure.

Aging Infrastructure and Energy Efficiency Mandates Driving Pump Replacement and Retrofitting Demand Nationwide

Thailand’s aging water infrastructure presents a significant opportunity for pump manufacturers and service providers. Many municipal systems, industrial facilities, and irrigation networks still operate with old, energy-inefficient pumps that increase electricity consumption and maintenance costs. Rising power tariffs and stricter environmental regulations are pushing facility operators to upgrade their equipment.

Replacing outdated pumps with high-efficiency IE3 or IE4 motor systems can deliver substantial energy savings and lower carbon emissions. In response, Energy Service Company (ESCO) business models are gaining popularity, allowing upgrades to be financed through future energy savings. This approach reduces upfront capital risk for end-users. As asset replacement cycles accelerate, demand is expected to remain stable and recurring. Suppliers that can clearly demonstrate return on investment through efficiency improvements, reduced downtime, and lower lifecycle costs will benefit the most from this modernization trend.

Category-wise Analysis

Pump Type Insights

Centrifugal pumps dominate the pump type, accounting for approximately 65% of the total market share. Their leadership is driven by versatility, ease of operation, and wide application across agriculture and industry. In Thailand’s agricultural regions, centrifugal pumps are commonly used for irrigation, particularly for rice paddies that require large volumes of water at low to medium pressure levels. Their simple design and lower maintenance requirements make them ideal for cost-sensitive users. In industrial applications, these pumps are essential for cooling towers, water circulation, and process water systems, especially within the EEC. Their ability to handle continuous operation with reliable performance further supports widespread adoption. Compared with more complex pump types, centrifugal pumps offer greater affordability and a higher availability of spare parts. These advantages ensure their continued dominance across multiple end-use sectors in Thailand.

Power Source Insights

Electric pumps lead the power source, holding an estimated market share of around 72%. Thailand’s extensive rural and urban electrification has firmly established electric pumps as the preferred option for water transfer applications. Compared to diesel pumps, electric models offer cleaner operation, lower noise levels, and reduced maintenance requirements. They are also not affected by fuel price fluctuations, making operating costs more predictable.

Government efforts by the Provincial Electricity Authority (PEA) to improve grid reliability have further strengthened adoption, even in semi-remote farming areas. Electric submersible pumps are widely used for groundwater extraction due to their efficiency and consistent power supply. As environmental regulations tighten and users seek more sustainable solutions, electric pumps remain well aligned with national energy and emissions reduction goals, reinforcing their strong market position.

Application Analysis

The agriculture & irrigation segment dominates the application category with an estimated share of 45%. Agriculture remains a critical pillar of Thailand’s economy, with the country ranking among the world’s leading exporters of rice and other crops. A reliable water supply is essential to maintain productivity during dry seasons and manage flooding during monsoons. Large-scale irrigation projects commissioned by the Royal Irrigation Department drive demand for high-capacity pumps, while individual farmers contribute to steady sales of smaller units.

The shift toward high-value crops such as durian, vegetables, and ornamental plants has increased demand for more precise and efficient irrigation systems. This trend supports the adoption of specialized agricultural pumps rather than generic models. Growing awareness of water conservation and productivity optimization continues to strengthen demand in this segment.

End-user Insights

Municipal & water utilities represent a fast-growing end-user segment, accounting for approximately 25% of the total market. Rapid urbanization and population growth are increasing the need for reliable water supply and wastewater management systems across Thailand. The Metropolitan Waterworks Authority (MWA) and Provincial Waterworks Authority (PWA) are actively investing in new pumping stations, pipeline expansion, and treatment facilities.

Government initiatives aim to provide clean and safe drinking water to 100% of villages nationwide, driving sustained demand for booster pumps, sewage pumps, and treatment plant systems. Additionally, reducing non-revenue water losses remains a top priority, encouraging the adoption of advanced pressure-controlled and smart pumping technologies. These investments ensure consistent long-term demand from municipal bodies and utilities.

Competitive Landscape

The Thailand water pump market is moderately fragmented, with participation from global manufacturers and strong local distributors. International companies such as Grundfos, Ebara, and KSB dominate premium industrial and municipal segments by offering advanced technology, energy-efficient products, and robust after-sales service networks. These players differentiate themselves through smart monitoring solutions and compliance with international efficiency standards.

In contrast, the agricultural and residential segments face strong competition from local manufacturers and Chinese brands, which compete primarily on price. Localized manufacturing strategies adopted by companies like Ebara and Torishima help reduce costs and improve delivery timelines. Turnkey engineering solutions and long-term service contracts are key competitive advantages in large infrastructure projects. Overall, technology leadership, service quality, and cost optimization define competitive success in this evolving market.

Key Market Developments

- In September 2024, Thailand’s Department of Customs reported a 76% year-on-year increase in water pump imports, reflecting strong demand recovery across industrial and agricultural sectors.

- The surge also indicates rising competitive pressure from low-cost suppliers, particularly manufacturers based in China and Vietnam.

- In May, 2023: The Integrated Water Resources Management (IWRM) authority announced a 150 million THB investment to interconnect three water treatment plants in the EEC. This project immediately increased demand for high-capacity industrial transfer pumps supporting regional water distribution reliability.

Companies Covered in Thailand Water Pump Market

- Grundfos Holdings A/S

- Zoeller Company

- Xylem Inc.

- Tsurumi Manufacturing Co., Ltd.

- Wilo SE

- Weir Group PLC

- KSB SE & Co. KGaA

- FLYGT

- Torishima Pump Mfg. Co., Ltd.

- Franklin Electric Co., Inc.

- Honda Power Equipment

- Pentair plc

- Ebara Corporation

- ITT Goulds Pumps

- Cat Pumps, Inc.

Frequently Asked Questions

The Thailand Water Pump Market is projected to reach a value of US$ 50.6 Billion by the year 2033, expanding at a steady growth rate during the forecast period.

Key demand drivers include the expansion of the Eastern Economic Corridor (EEC) industrial zone, government incentives for solar-powered irrigation, and strict regulations on water reuse and recycling in the manufacturing sector.

Centrifugal pumps currently hold the largest market share, owing to their widespread usage in agricultural irrigation, flood control, and standard industrial water transfer applications.

A significant opportunity lies in the development of smart, IoT-integrated pumping systems that align with the Thailand 4.0 initiative, offering enhanced efficiency and remote monitoring for municipal and industrial users.

Key players include Grundfos Holdings A/S, Ebara Corporation, KSB SE & Co. KGaA, Wilo SE, and Torishima Pump Mfg. Co., Ltd., along with strong local distributors like C.M.P. Group.