- Healthcare Services

- Sperm Bank Market

Sperm Bank Market Size, Share, and Growth Forecast, 2026-2033

Sperm Bank Market by Service Type (Sperm Freezing, Semen Analysis, Genetic Screening, Others), Donor Type (Anonymous, ID-Disclosure, Known, Others), End-User (Fertility Clinics, IVF Centers, Single Parents, Others), and Regional Analysis for 2026-2033

Sperm Bank Market Share and Trends Analysis

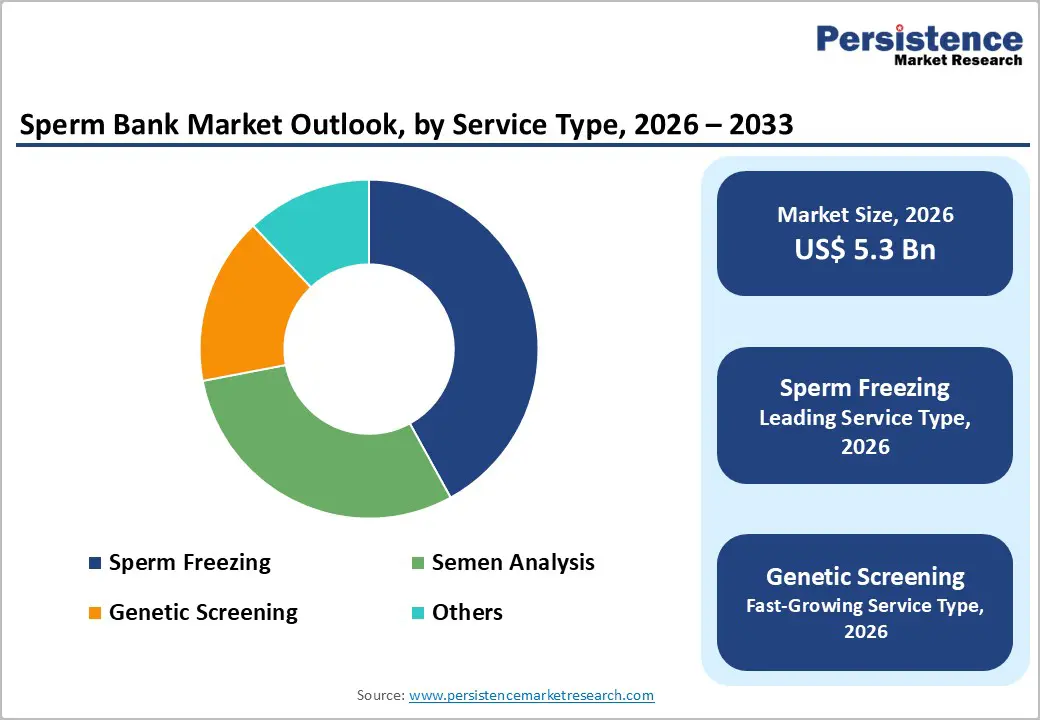

The global sperm bank market size is likely to be valued at US$ 5.3 billion in 2026, and is projected to reach US$ 6.9 billion by 2033, growing at a CAGR of 3.8% during the forecast period 2026–2033. Market expansion is being driven by increasing infertility prevalence among both men and women, alongside growing awareness of fertility preservation options. Assisted reproductive technology (ART) services are becoming more accessible across developed and emerging economies, which is strengthening demand for donor sperm programs and long-term cryogenic storage. Social and demographic trends are also influencing utilization patterns.

Delayed parenthood due to career priorities and financial planning is increasing reliance on fertility services. In addition, broader societal acceptance of diverse family structures is expanding demand within single-parent households and the lesbian, gay, bisexual, transgender, and queer (LGBTQ+) community. Technological progress is enhancing service quality and clinical confidence. Advances in cryopreservation techniques are improving post-thaw sperm viability and increasing the probability of successful fertilization outcomes. Expanded genetic screening protocols are enabling more comprehensive donor evaluation, which is reducing inherited disease risk and improving recipient assurance. Fertility clinics are integrating digital platforms for donor matching and long-term storage management, which is streamlining service delivery. As healthcare systems continue recognizing reproductive health as a core medical service, sperm banks are strengthening operational standards and compliance frameworks.

Key Industry Highlights

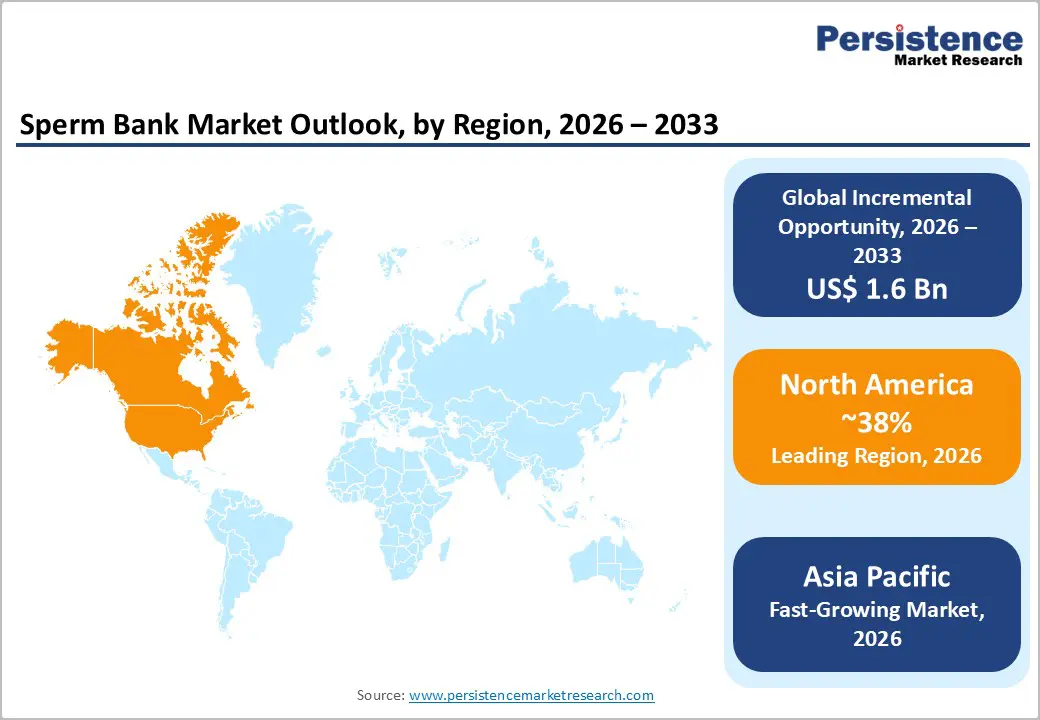

- Regional Leadership: North America is poised to dominate with an estimated 38% share in 2026, while Asia Pacific is anticipated to be the fastest-growing 2026-2033 market at roughly 7.9% CAGR, driven by fertility awareness campaigns in China, India, and Southeast Asia.

- Dominant Service Type: Sperm freezing is projected to command around 42% revenue share in 2026, while genetic screening services are likely to grow the fastest at nearly 6.1% CAGR through 2033, driven by the strong preference for personalized donor selection.

- Leading Donor Type: Anonymous donors are expected to lead with an estimated 55% share in 2026, while ID?disclosure donors are likely to be the fastest-growing segment at about 7.4% CAGR during 2026–2033, reflecting increasing consumer preference for transparency in donor identity.

- Dominant End-User Segment: Fertility clinics are projected to retain the largest share at 48% in 2026, while in-vitro fertilization (IVF) centers and single parents are expected to expand the fastest through 2033, supported by growing ART adoption.

- Technological Trends: Cryopreservation and genetic screening innovations are expected to improve service efficacy and success rates, with advanced donor matching platforms contributing to enhanced clinical outcomes and patient adoption.

- August 2025: Researchers at Harvard University’s George Church laboratory announced advancement toward growing human eggs in a dish, and the fertility biotech startup Gameto plans to complete this work that could one day expand options for IVF-related therapies.

| Key Insights | Details |

|---|---|

| Sperm Bank Market Size (2026E) | US$ 5.3 Bn |

| Market Value Forecast (2033F) | US$ 6.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Infertility Burden and Global Healthcare Recognition

Infertility continues to emerge as a major global public health concern, with an estimated one in six people of reproductive age affected worldwide. The World Health Organization (WHO) released its first ever global guideline on infertility prevention, diagnosis, and treatment, urging countries to make fertility care safer, fairer, and more affordable within national health systems. This milestone guideline includes 40 evidence based recommendations, reinforcing the need for diagnostic services and fertility preservation interventions such as sperm banking.

By highlighting infertility as a major equity and public health issue, WHO supports increased policy focus and resource allocation toward reproductive health challenges that have historically been under?prioritized. Given rising infertility prevalence, demand for clinical diagnostic services, fertility preservation programs, and donor sperm banking has sharply increased, further establishing these services as core components of comprehensive reproductive care. The WHO call for access and affordability pressures health systems to recognize infertility treatment as a necessary element of broader healthcare offerings, which expands market opportunity for sperm banks and fertility service providers.

Technology Innovation and Supportive Policy Actions

Technological advancements continue to elevate the quality, reliability, and adoption of fertility care practices. Enhanced cryopreservation techniques, optimized storage media, and digital lab systems significantly improve the viability and post?thaw performance of stored sperm, leading to better clinical outcomes in ART procedures such as IVF and intrauterine insemination (IUI). These innovations support more robust donor?recipient matching and enrich patient experiences, further legitimizing fertility services as dependable healthcare solutions. Combined with genetic screening and advanced diagnostics, these tools promote precision medicine approaches, improving treatment personalization and patient confidence.

On the governmental front, in February 2025, the U.S. White House issued an executive action aimed at expanding access to in IVF and reducing regulatory barriers, signaling increased public policy support for reproductive services. Although this action focuses on policy review and cost reduction recommendations rather than direct legislative change, it represents a notable shift toward recognizing fertility treatments as essential healthcare components. Taken together, technological advancements and evolving health policy frameworks are elevating the entire fertility solutions landscape, driving uptake of donor sperm services, genetic screening, and reproductive healthcare innovations.

Regulatory Complexities and Ethical Considerations

Regulatory frameworks governing sperm donation, handling standards, donor consent, and patient protections vary widely across countries, creating significant compliance challenges for fertility service providers. In the U.K., the Human Fertilisation and Embryology Authority (HFEA) continues to enforce rigorous requirements, including limits on the number of families per donor and strict clinic licensure standards, to protect patients and donors alike. These evolving legal parameters demand ongoing operational adjustments and can delay new service offerings.

In addition to legal complexity, ethical debates persist around donor identity disclosure, long?term data privacy, and consent frameworks. These concerns shape public policy and clinic practices, requiring providers to invest heavily in governance and legal counsel. Even established fertility markets are seeing heightened scrutiny; the UK regulator’s annual report noted a year?on?year increase in incident reporting, underscoring the delicate balance between access and regulatory oversight. Smaller and emerging providers often lack the compliance infrastructure of larger clinics, slowing expansion into new regions. This fragmented regulatory ecosystem ultimately increases operational risk, contributes to higher service costs, and can dampen investor confidence.

High Service Costs and Economic Barriers

Fertility services, including sperm banking, advanced genetic screening, and donor matching, often involve premium pricing that may not be covered by standard insurance plans or public healthcare systems. Even as some state mandates expand coverage, implementation remains uneven; California’s infertility and IVF coverage mandates under SB 729 were delayed to 2026, creating uncertainty over when patients will experience tangible insurance benefits. This ambiguity prolongs out?of?pocket barriers, particularly for middle?income families who lack comprehensive benefits.

Across multiple regions, patients continue to report high costs for fertility procedures and ancillary services, with pricing fluctuations influenced by clinic reputation, technology use, and geographical location. Recent reports highlight increasing IVF and egg?freezing fees in Australia jumping hundreds of dollars per cycle, reinforcing the financial strain on patients. Though some policy efforts aim to broaden access and promote coverage innovation, overall adoption remains limited, with many employers and insurers still excluding fertility treatments from basic plans. These economic barriers restrict accessibility for price?sensitive segments and make it difficult for smaller providers to compete without significant capital investment, ultimately slowing broader market expansion despite growing demand.

Rising Infertility Burden and Policy Recognition

Infertility continues to be recognized as a significant public health concern worldwide, prompting direct action from global and national authorities. In late 2025, the WHO released its first global guideline on infertility care, urging countries to make fertility prevention, diagnosis, and treatment safer, more equitable, and more affordable for all individuals experiencing reproductive challenges. The guideline outlines 40 evidence?based recommendations to support health systems in integrating infertility care into broader reproductive health services.

This official acknowledgment by WHO underscores growing global demand for reproductive care access and demonstrates a shift toward viewing fertility care, including cryopreservation, sperm analysis, and third?party reproduction services, as essential components of health systems. By calling for increased affordability and broader insurance integration, the WHO position supports long?term expansion of fertility support services while strengthening patient confidence in evidence?based fertility interventions. Countries adapting these guidelines are likely to see accelerated health policy alignment with clinical service provision, further amplifying demand for sperm bank services and associated reproductive technologies.

Government Initiatives and Clinical Access Expansion

Policymakers in multiple jurisdictions have taken measures to expand access to reproductive care, which directly supports the fertility services ecosystem, including sperm bank demand. In the U.S., state legislatures are advancing reproductive health protections, with the New York State Senate passing legislation in early 2026 to expand access to in-vitro fertilization and strengthen patient privacy rights as part of broader reproductive healthcare reforms. This legislative action reflects sustained governmental interest in reproductive service access expansion, which includes insurance reform and privacy safeguards for fertility patients.

Similarly, in Malaysia in late 2025, the government announced plans to provide subsidized fertility treatment support to approximately 30,000 couples nationwide, aiming to address declining birth rates through expanded access to medically assisted reproduction, including IUI and advocacy support. This large?scale public program underscores the strategic importance governments are placing on reproductive health interventions as part of national demographic and population policies. These parallel policy developments, from reproductive rights legislation to direct government?supported treatment programs, reinforce a broader trend toward institutional support for fertility services, which drives adoption of fertility preservation technologies, clinical diagnostics, and donor sperm services throughout key markets.

Category-wise Analysis

Service Type

The sperm freezing segment is expected to capture an estimated 42% sperm bank market revenue share in 2026, as clinics increasingly bundle long?term cryopreservation with donor sperm provision, semen analysis, and genetic risk assessment. Cryopreservation remains foundational to fertility preservation for patients undergoing medical treatments or planning delayed parenthood, reinforcing stable recurring service demand. Global investments in publicly funded fertility care are increasing access to these foundational services; for example, the Ontario government committed US$?250?million to expand publicly funded IVF and fertility clinics, supporting wider availability of reproductive and cryopreservation services across Canadian populations.

This foundational segment is further strengthened by specialized screening enhancements that provide added clinical insights and personalized care pathways. The widening demand for differentiated donor profiles and risk assessments is prompting clinics to integrate more comprehensive diagnostics as part of fertility service bundles, lifting average revenue per client and deepening patient engagement. As fertility care continues to evolve toward a more integrated and patient?centric model, sperm freezing and ancillary assessments are projected to remain core revenue drivers, sustaining the segment’s leading position and reinforcing adoption across diverse demographic and geographic markets.

End-User Insights

Fertility clinics are expected to hold the leading end?user sperm bank market share of about 45% in 2026, serving as the primary execution points for donor sperm use, sperm storage, and ART procedures such as IVF and IUI. Clinics leverage deep partnerships with sperm bank services to streamline patient care journeys, from initial fertility testing to long?term storage and embryo creation workflows. Expansion of public sector offerings are proving to be a major growth determinant for fertility clinics. For example, Cama Hospital in Mumbai received government permission to offer both sperm bank and egg?freezing facilities, demonstrates rising institutional support for integrated reproductive care, strengthening clinic-based adoption and improving patient access to fertility services.

IVF centers are anticipated as fastest?growing end users, projected to register a 2026-2033 CAGR of 8.7%, reflecting broader social acceptance of diverse family structures and rising use of advanced reproductive options. IVF centers increasingly require specialized sperm donor matching, genetic consultation, and premium storage services to meet complex clinical needs. Social trends toward delayed family building, along with expanded access to IVF and related interventions, further fuel this demand. Single parents, supported by evolving policy landscapes and increased coverage for fertility treatments, are seeking tailored fertility solutions, strengthening demand for targeted end?user offerings that support individualized care pathways.

Regional Insights

North America Sperm Bank Market Trends

North America is estimated to remain the dominant region, with an estimated 38% of the sperm bank market share and fertility services market in 2026. The United States leads this position through widespread adoption of fertility preservation offerings, ART procedures, and advanced reproductive clinics. Robust regulatory frameworks that ensure quality of care and compliance also support innovation and patient safety. Partial insurance coverage expansions, such as emerging state?level IVF mandates, are reducing out?of?pocket costs for patients and enhancing treatment accessibility, boosting service utilization. Growth in delayed parenthood trends and broader acceptance of diverse family structures continue to sustain demand across end?user groups.

A notable 2025 development that underscores this trend is Progyny Global’s expansion of employer?sponsored fertility and family?building benefits worldwide, enabling multinational access to inclusive reproductive care across North America and beyond. This initiative reflects increasing recognition of fertility services as a core employee health benefit and demonstrates how policy and private sector actions are elevating fertility care infrastructure and utilization. These dynamics ensure North America’s leadership is supported by clinical demand, insurance evolution, and an expanding ecosystem of fertility service providers.

Europe Sperm Bank Market Trends

Europe holds a strong position in the global market for sperm banks and fertility services, supported by high procedural volumes in ART hubs such as Spain, Germany, and the U.K., where IVF and other reproductive procedures are widely adopted. Harmonized European Union (EU) regulations ensure standardized donor screening, data protection, and clinical quality, building patient confidence. Cross-border fertility treatment and medical tourism continue to drive demand as patients seek specialized services. The region benefits from mature healthcare infrastructure, well-established clinics, and advanced research capabilities, supporting operational efficiency and innovative service delivery.

Recent developments emphasized Europe’s focus on expanding fertility care capacity. Memphasys Limited secured a long-term European supply agreement with a major Italian IVF group, highlighting strong clinical demand and adoption of advanced reproductive technologies. Integration of diagnostic innovations and next-generation genetic screening enhances patient outcomes and clinic capabilities. These initiatives reinforce Europe’s reputation as a high-quality, innovative fertility market, attracting both domestic and international patients, and positioning the region for steady, sustainable growth.The combination of regulatory support, medical expertise, and technology adoption positions Europe for sustained growth in the coming years.

Asia Pacific Sperm Bank Market Trends

Asia Pacific is expected to be the fastest-growing regional market for sperm banks and fertility services market, projected to expand at a CAGR of approximately 9.1% from 2026 to 2033. Rapid urbanization, rising healthcare investment, growing reproductive health awareness, and expanding fertility clinic infrastructure are driving adoption across China, Japan, India, and ASEAN countries. Government and regulatory efforts are improving ART accessibility and addressing disparities in access and reimbursement. Large populations, increasing infertility prevalence, and delayed parenthood trends further boost market potential. Public-private partnerships and investments in specialized fertility centers support local demand and international medical tourism.

Strategic initiatives by individual countries are also contributing to cross-border fertility care expansion. For example, the United Arab Emirates has announced plans to become a global fertility and medical tourism hub, investing in IVF clinics, satellite consultation centers, and advanced technologies such as AI-assisted embryo selection and robotic cryobanking to attract regional and international patients. In addition, countries such as Thailand and Singapore are strengthening infrastructure for fertility tourism by offering integrated diagnostic and reproductive services. These investments, combined with rising awareness and adoption of digital fertility platforms, are enhancing patient access, improving treatment outcomes, and reinforcing Asia Pacific’s trajectory as a high-growth market within the sperm bank landscape

Competitive Landscape

The global sperm bank market structure is moderately consolidated, with leading players such as Cryos International, Fairfax Cryobank, California Cryobank, European Sperm Bank, and Seattle Sperm Bank collectively accounting for a significant portion of market revenue. These established providers leverage extensive clinic partnerships, strong regulatory compliance expertise, and integrated service offerings that include sperm freezing, genetic screening, and donor matching. They also invest heavily in R&D to enhance cryopreservation technologies, genetic testing capabilities, and digital donor management platforms, maintaining a competitive edge in clinical quality and patient experience.

Regional and niche providers, including smaller national banks and fertility clinic-affiliated sperm banks, focus on specialized donor services, local market penetration, and personalized fertility solutions. Regulatory compliance, ethical considerations, and high infrastructure costs create barriers for new entrants, but digital telefertility platforms and AI-assisted donor selection tools are enabling innovative startups to participate in select segments. Market consolidation is expected to continue gradually as leading global players expand geographically through acquisitions, partnerships, and technology integration, while smaller providers differentiate through service specialization and personalized care.

Key Industry Developments

- In February 2026, Legacy introduced a comprehensive motility testing solution for at-home semen analysis that aims to set a new clinical standard through enhanced diagnostic accuracy and user convenience. The offering is designed to support earlier detection of male fertility issues and improve patient engagement by combining laboratory-quality insights with home testing accessibility.

- In November 2025, Bessemer Venture Partners led a US$ 14 million Series A funding round in Pluro Fertility to expand IVF care and fertility services across India. The investment is aimed at enhancing clinical infrastructure, improving patient access, and scaling technology-enabled fertility solutions in a rapidly growing reproductive healthcare market.

- In July 2025, IVI RMA Global moved to acquire ART Fertility Clinics, a deal valued at approximately US$ 420 million, marking a major expansion into India’s growing IVF market. The acquisition added 11 clinics in India and additional operations in the UAE and Saudi Arabia, significantly strengthening IVI RMA’s regional footprint. The transaction reflects broader sector trends of clinic network consolidation and cross-border expansion.

- In February 2025, NewGenIVF Group Limited finalized the acquisition of MicroSort Reproductive Technology for US $5 million, via a combination of cash and ordinary shares. MicroSort’s proprietary sperm-sorting technology, which separates X and Y chromosome-bearing sperm for IVF, strengthens NewGenIVF’s technological capabilities.

Companies Covered in Sperm Bank Market

- California Cryobank

- Cryos International

- European Sperm Bank

- Fairfax Cryobank Inc.

- Indian Spermtech

- Seattle Sperm Bank

- New England Cryogenic Center

- Androcryos

- ReproTech

- The London Sperm Bank

- Xytex Corporation

- Cryobank America

- Global Fertility Services

- Asian Reproductive Solutions

Frequently Asked Questions

The global sperm bank market is projected to reach US$ 5.3 billion in 2026.

Increase in infertility prevalence, technological advancements in cryopreservation and genetic screening, and growing societal acceptance of diverse family structures are key growth drivers.

The market is poised to grow at a CAGR of 3.8% from 2026 to 2033.

Expansion in emerging markets, integration with precision medicine, and digital fertility and telehealth platforms present major growth opportunities.

Key players in the market include Cryos International, Fairfax Cryobank, California Cryobank, European Sperm Bank, and Seattle Sperm Bank.