- Pharmaceuticals

- Sickle Cell Disease Treatment Market

Sickle Cell Disease Treatment Market Size, Share, Growth, and Regional Forecast, 2025 - 2033

Sickle Cell Disease Treatment Market by Drug Type (Hydroxyurea, Antibiotics, Pain-relieving Medications, Others), by Disease Type (Sickle Cell Anemia, Sickle Hemoglobin C Disease, Sickle beta Thalassemia, Others), by Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), by Regional Analysis, from 2026 - 2033

Sickle Cell Disease Treatment Market Share and Trends Analysis

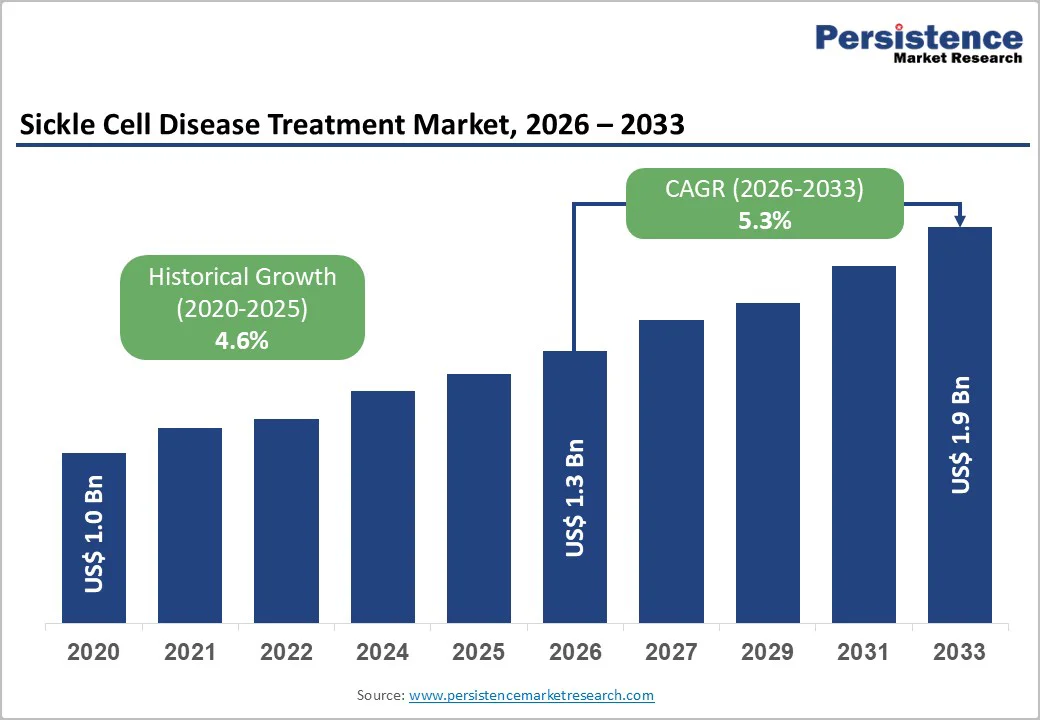

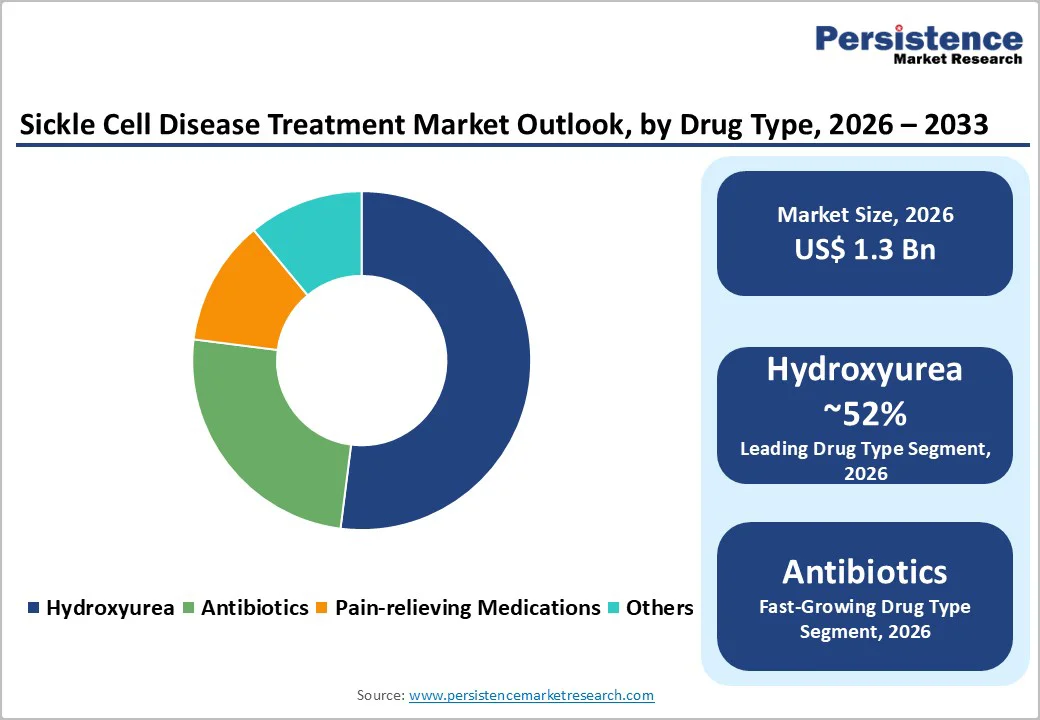

The global sickle cell disease treatment market size is estimated to grow from US$ 1.3 billion in 2026 to US$ 1.9 billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033. The global market is growing steadily, with early accessibility to first-hand diagnosis, and new therapies are enlarging care options. Rising awareness, wider newborn screening, and better management protocols are strengthening long-term treatment demand across high-burden regions.

Recent approvals of disease-modifying drugs and the emergence of gene therapies have shifted the market toward more targeted and potentially curative solutions. Partnerships between governments, global organizations, and pharmaceutical companies are improving access, while ongoing research, real-world evidence, and value-based pricing discussions continue to shape future market trends.

Key Industry Highlights

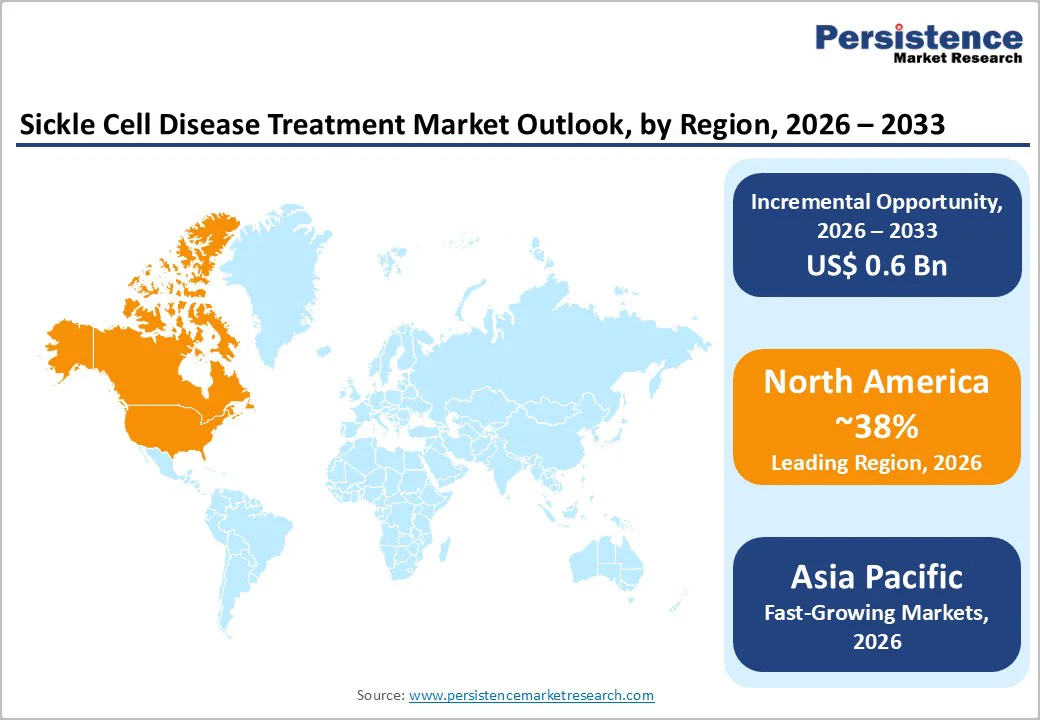

- Leading Region: North America leads the global market with approximately 39% share in 2025, supported by strong newborn screening programs, advanced hematology centers, and broad reimbursement for innovative therapies.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by large undiagnosed populations in India and parts of ASEAN, increasing government initiatives for screening, and gradual expansion of access to hydroxyurea and comprehensive SCD care.

- Dominant Segment: Hydroxyurea remain the dominant segment due to its guideline-endorsed role as first-line disease-modifying therapy and widespread use across pediatric and adult patients.

- Fastest Growing Segment: Antibiotics grow fastest, driven by increasing infection prevention and treatment needs in SCD patients.

| Key Insights | Details |

|---|---|

|

Sickle Cell Disease Treatment Market Size (2026E) |

US$ 1.3 Bn |

|

Market Value Forecast (2033F) |

US$ 1.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.6% |

Market Dynamics

Driver - Strong Epidemiological Burden and Rising Diagnosis Rates

The foremost growth driver for the sickle cell disease treatment market is the substantial and growing global disease burden, especially in Sub-Saharan Africa, India, the Middle East, and parts of the Caribbean. Global Burden of Disease estimates show that births of babies with SCD increased by about 13–14% between 2000 and 2021, reaching roughly 515,000 affected newborns annually, primarily due to population growth in high-prevalence regions. Expanded newborn screening initiatives in countries such as the U.S., Brazil, and several African nations are improving early detection, which in turn boosts demand for chronic therapies such as hydroxyurea, prophylactic antibiotics, and pain-relief medications across pediatric and adult populations. As health systems increasingly recognize SCD as a priority non-communicable condition, policy initiatives and donor-supported programs are broadening treatment access and reinforcing long-term prescription volumes.

Restraints - Lack of Proper Healthcare Infrastructure

The lack of proper healthcare infrastructure remains a major restraint on the growth of the sickle cell disease treatment market. Many regions with the highest disease burden, especially Sub-Saharan Africa and rural South Asia, lack specialized hematology centers, trained professionals, and reliable supply chains. Limited access to diagnostic services, newborn screening, and routine monitoring means many patients remain undiagnosed or are identified only after severe complications occur. This contributes to high early mortality and significantly reduces long-term demand for chronic therapies. Even when patients are diagnosed, essential treatments such as hydroxyurea, pain-relief support, transfusion services, and advanced options like stem cell or emerging gene therapies are often unavailable or inconsistently provided. Supply-chain gaps further disrupt access to essential medicines, making continuous management difficult. Emergency care for vaso-occlusive crises is also inadequate in many rural and low-resource settings, leading to preventable complications and treatment delays. Long travel distances, out-of-pocket expenses, and low awareness among communities add to these barriers. As a result, market growth remains constrained because the need for treatment is high, but the proper infrastructure to deliver it is lacking.

Opportunity - Scaling Access Programs and Optimized Standard-of-Care Regimens

There is a strong opportunity to improve access to sickle cell treatments by making care a regular part of public health and primary healthcare systems, especially in countries with the highest number of patients. Expanding newborn screening, vaccination, infection prevention programs, and early use of hydroxyurea can greatly reduce complications and increase long-term use of oral therapies, pain-relief medicines, and supportive drugs available in hospitals and retail pharmacies. Partnerships between pharmaceutical companies, NGOs, and governments such as drug donation programs, tiered pricing, and agreements for local manufacturing, can make medicines more affordable and improve supply reliability. As clinical guidelines increasingly recommend disease-modifying therapies and digital tools help track adherence and follow-up, more patients can receive consistent care. Companies that offer strong treatment portfolios along with patient-support services, education, and monitoring tools will be better positioned to meet the growing demand and benefit from expanding treatment coverage in underserved regions.

Category-wise Analysis

By Drug Type Insights

Within drug type, hydroxyurea is expected to dominate the market, accounting for about 52% share in 2025, reflecting its status as the foundational disease-modifying therapy for SCD. Since its approval for SCD in 1998, hydroxyurea has consistently demonstrated reductions in vaso-occlusive crises, acute chest syndrome, and transfusion requirements, while improving hemoglobin levels and overall survival, particularly in pediatric and young adult populations. Clinical guidelines in the U.S., Europe, and several African and Asian countries now recommend hydroxyurea as first-line therapy for many patients, which supports large-volume prescribing through hospital and retail pharmacies. Although newer agents such as L-glutamine, crizanlizumab, and voxelotor are gaining traction, their higher costs and access constraints mean they are often used in combination with or after hydroxyurea, reinforcing the latter’s leading revenue contribution.

By Distribution Channel Insights

By distribution channel, hospital pharmacies are anticipated to dominate the sickle cell disease treatment market, with around 60% share in 2025, due to the complex and acute nature of SCD management. Patients with SCD frequently require hospital-based care for vaso-occlusive crises, acute chest syndrome, and transfusion support, which concentrates prescribing and dispensing of key therapies within tertiary and secondary care centers. Hospital pharmacies are typically responsible for supplying injectable medications, advanced disease-modifying agents, and peri-procedural therapies associated with bone marrow transplantation and gene therapy. In addition, multidisciplinary SCD clinics often operate within hospital settings, where integrated care teams manage chronic prescriptions, monitor laboratory parameters, and coordinate access to clinical trials, further reinforcing the central role of hospital pharmacies compared with retail and online channels.

Region-wise Insights

North America Sickle Cell Disease Treatment Market Trends

North America continues to lead the global sickle cell disease treatment market, accounting for an estimated 39% share in 2026. The region benefits from strong clinical infrastructure, well-established hematology centers, and universal newborn screening programs that allow early identification and timely management of affected children. Broad insurance coverage and reimbursement support the adoption of branded disease-modifying therapies, curative interventions, and advanced diagnostics. Over the past decade, the U.S. FDA has approved several important therapies for SCD, including L-glutamine, crizanlizumab, and voxelotor, along with the first gene therapies, reflecting an active research environment and extensive clinical trial activity.

Regulatory agencies are placing greater focus on real-world evidence and long-term safety monitoring, highlighted by re-evaluations of existing products and ongoing post-approval studies. Discussions around value-based pricing and performance-linked reimbursement models are expanding, particularly for high-cost gene therapies. At the same time, patient advocacy groups, nonprofit organizations, and community health programs continue to work on reducing disparities in access, especially among minority populations most affected by SCD. These combined efforts strengthen early intervention, expand treatment uptake, and reinforce long-term demand for comprehensive care solutions across North America.

Asia Pacific Sickle Cell Disease Treatment Market Trends

Asia Pacific is emerging as one of the fastest-growing markets for sickle cell disease treatment, supported by large, affected populations in India and selected Southeast Asian countries. In India, SCD prevalence is notably higher in tribal, rural, and socio-economically disadvantaged communities, where sickle trait rates can reach 10–30%. Historically, many patients remained undiagnosed or received minimal treatment, but recent government initiatives are changing this landscape. National and state-level programs are expanding population screening, genetic counseling, and hydroxyurea-based treatment pathways, gradually increasing the number of diagnosed and treated patients.

Countries such as China and Japan have lower disease prevalence but significantly contribute to regional progress through strong biotechnology ecosystems, high-quality research facilities, and participation in global clinical trials for advanced therapies. Several Asia Pacific governments are investing in rare-disease frameworks, strengthening hematology services, and integrating chronic disease management into universal health coverage schemes. This supports the adoption of cost-effective generics such as hydroxyurea today and creates pathways for future uptake of innovative treatments in specialized hospitals. Growing capabilities in local generic and biosimilar manufacturing, along with cross-border research collaborations, are expected to drive above-average market growth in the coming years.

Competitive Landscape

The global sickle cell disease treatment market shows moderate consolidation in advanced therapies, with major biopharma companies such as Novartis, Pfizer, AstraZeneca, and Bristol-Myers Squibb leading innovation in disease-modifying and gene-based treatments. In contrast, the hydroxyurea segment remains fragmented with multiple generic producers. Competition is driven by differentiated mechanisms of action, long-term outcomes, safety profiles, and supportive care programs. Companies are actively pursuing strategic partnerships, regulatory approvals, and pipeline expansion to strengthen their position. Emerging models integrating therapy with digital adherence tools and comprehensive care support further enhance competitiveness and create opportunities for sustained market leadership.

Key Industry Developments:

- In March 2024, Bluebird Bio officially launched Lyfgenia, its lentiviral gene therapy for sickle cell disease, following FDA approval in late 2023.

- In December 2023, following FDA approval, Vertex Pharmaceuticals and CRISPR Therapeutics introduced Casgevy, a CRISPR/Cas9-based gene therapy for sickle cell disease.

Companies Covered in Sickle Cell Disease Treatment Market

- AstraZeneca Plc.

- Eli Lilly and Company

- Bristol-Myers Squibb Company

- Novartis AG

- Pfizer Inc.

- Baxter International Inc.

- Emmaus Life Sciences, Inc.

- Bluebird bio, Inc.

- Global Blood Therapeutics Inc.

- Sangamo Therapeutics, Inc.

- Acceleron Pharma, Inc.

- Arena Pharmaceuticals, Inc.

- Alnylam Pharmaceuticals, Inc.

- Others

Frequently Asked Questions

The global sickle cell disease treatment market is projected to be valued at US$ 1.3 Bn in 2026.

Rising disease prevalence, improved screening, novel disease-modifying therapies, and increasing access to advanced care strongly drive market growth.

The global market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Expansion of gene therapies, biologics, newborn screening programs, and treatment availability across underserved regions creates substantial upcoming opportunities.

Key companies include AstraZeneca Plc., Eli Lilly and Company,Bristol-Myers Squibb Company, Novartis AG, and Pfizer Inc.