- Medical Devices

- Scoliosis Management Market

Scoliosis Management Market Size, Trends, Share, Growth, and Regional Forecast, 2026 to 2033

Scoliosis Management Market by Product (Orthosis System and Spinal System), Disease Type (Idiopathic Scoliosis, Neuromuscular Scoliosis, Degenerative Scoliosis, and Others), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies), and Regional Analysis from 2026 to 2033

Scoliosis Management Market Share and Trends Analysis

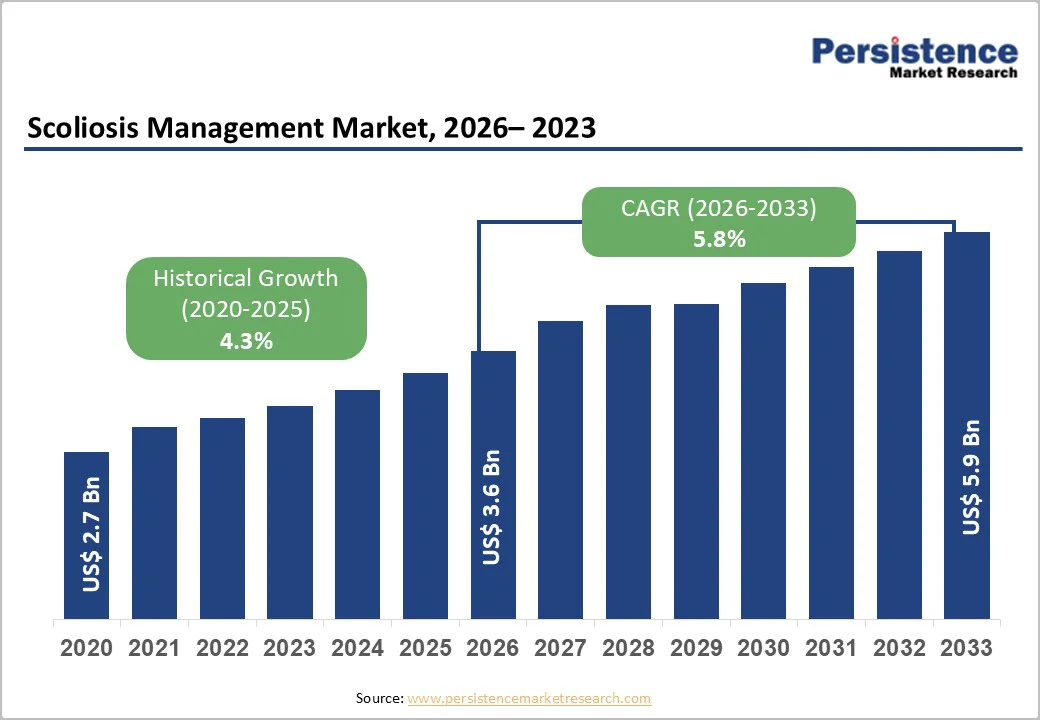

The global scoliosis management market size is likely to value at US$ 3.6 billion in 2026 and projected to reach US$ 5.9 billion by 2033, growing at a CAGR of 5.8% during the forecast period from 2026 to 2033.

Global demand for scoliosis management is rapidly increasing due to the rising prevalence of scoliosis across pediatric, adolescent, and adult populations, coupled with the growing preference for non-invasive and motion-preserving treatment options.

The expansion of outpatient orthotic care, increasing adoption of corrective bracing, and advancements in minimally invasive scoliosis surgery are key contributors. Technological innovations, including 3D-printed braces, digital scanning, AI-based curve monitoring, and sensor-integrated orthotic systems, are enhancing accuracy, comfort, and long-term clinical outcomes.

Key Industry Highlights

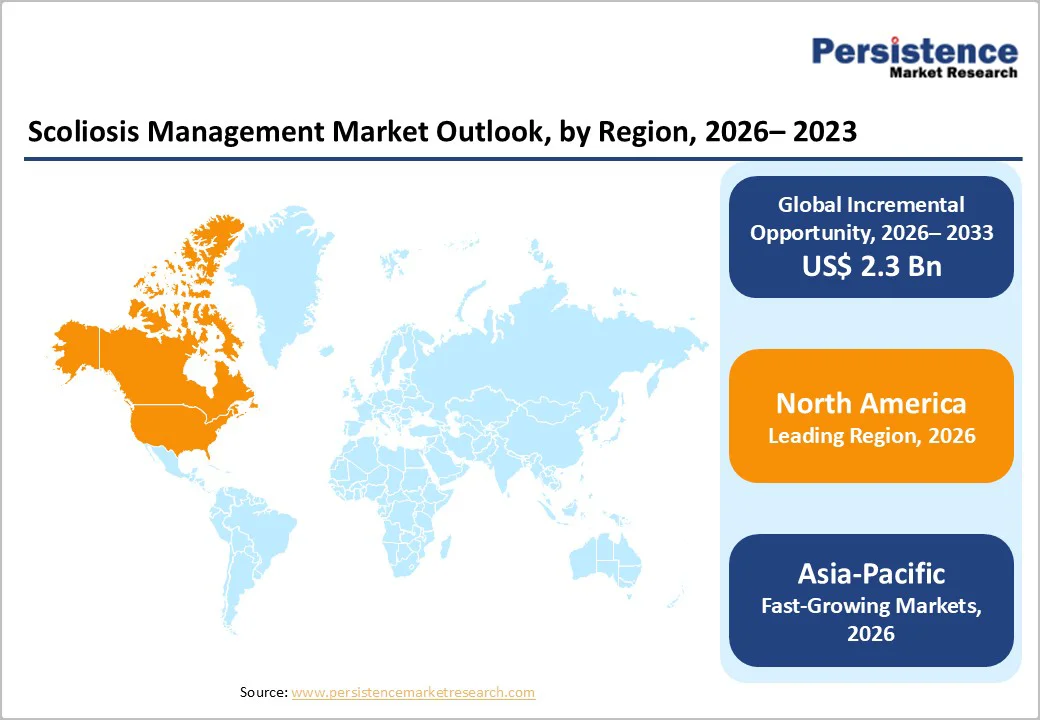

- Leading Region: North America dominates the global scoliosis management market with a 45.8% share, supported by high scoliosis screening rates, advanced orthotic fabrication facilities, strong adoption of 3D-printed braces, and favorable reimbursement for pediatric bracing and corrective procedures.

- Fastest-Growing Region: Asia Pacific is the fastest-growing market, driven by increasing scoliosis incidence among school-age children, expanding access to orthopedic care, rapid digitization of brace manufacturing, and growing adoption of cost-effective custom bracing solutions.

- Leading Product Segment: Thoracolumbosacral Orthosis (TLSO) braces lead the product category due to widespread use in adolescent idiopathic scoliosis (AIS), strong clinical efficacy, non-invasive application, and increasing adoption of lightweight, 3D-printed designs.

- Fastest-Growing Product Segment: Spinal system devices (growth modulation, fusion-less systems) are the fastest-growing segment, fueled by rising demand for minimally invasive correction, motion-preserving techniques, and expanding approvals for pediatric and early-onset scoliosis systems.

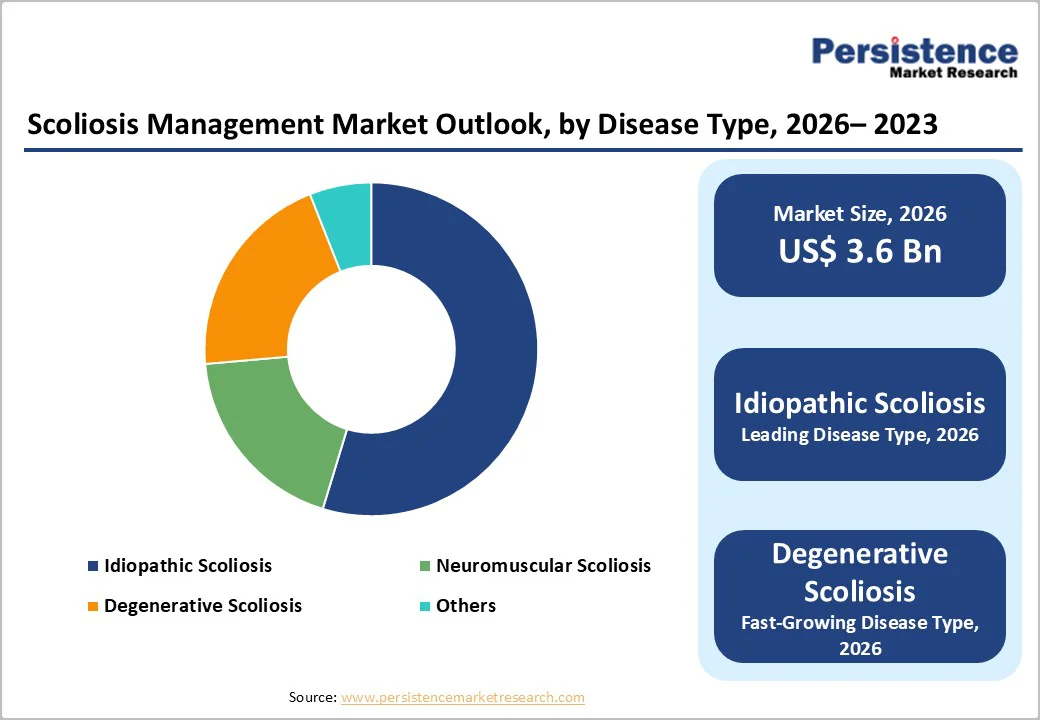

- Leading Disease Type Segment: Idiopathic scoliosis dominates the disease segment, attributed to high global prevalence, strong focus on early screening, and increasing adoption of bracing as a first-line, cost-effective alternative to surgery.

- Fastest-Growing Disease Type Segment: Degenerative scoliosis is the fastest-growing category, due to aging populations, increasing adult spinal deformity cases, higher demand for pain-relief bracing, and improved surgical technologies supporting minimally invasive adult scoliosis correction.

| Key Insights | Details |

|---|---|

| Scoliosis Management Market Size (2026E) | US$ 3.6 Bn |

| Market Value Forecast (2033F) | US$ 5.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Dynamics

Driver - Increasing Prevalence and Technological Advancements Driving Adoption

The growing incidence of adolescent idiopathic scoliosis, along with a rapidly expanding adult degenerative-scoliosis population, is significantly increasing the demand for braces, imaging, and surgical interventions, which is driving market growth. Additionally, improved school-based screening, broader clinical awareness, and better diagnostic tools are enabling earlier detection, expanding the pool of patients eligible for conservative management as well as corrective procedures.

Furthermore, innovations such as 3D-printed custom braces, digital scanning workflows, and sensor-embedded smart orthoses are enhancing comfort, fit, and compliance monitoring. These advancements improve patient experience and clinical outcomes, boosting acceptance of conservative therapy and strengthening overall market growth for scoliosis management solutions.

Restraints - High Treatment Costs and Reimbursement Limitations Restrict Adoption

The adoption of robotics, surgical navigation platforms, and premium spinal implants remains challenging due to their substantial capital and operational costs. These technologies require significant upfront investment, specialized training, and ongoing maintenance, all of which raise the per-procedure expense.

As a result, many hospitals especially mid-tier and resource-constrained centers delay or avoid upgrading to advanced scoliosis treatment systems, slowing technological penetration in several markets.

Moreover, conservative treatment tools such as custom braces, 3D-printed orthoses, and sensor-enabled devices often receive limited or inconsistent reimbursement. In many countries, insurers cover only a fraction of the brace cost or exclude newer devices entirely, placing a heavy financial burden on patients.

This gap reduces the adoption of higher-quality orthotic solutions, widens treatment disparities, and restricts overall market growth in regions where out-of-pocket spending drives purchasing decisions.

Opportunity - Advances in Bracing & Remote Monitoring and Premium Surgical and Robotics Platforms

Rapid adoption of 3D-printed, lightweight custom braces is transforming conservative scoliosis care by improving comfort, aesthetics, and patient compliance while reducing production time. At the same time, smart-brace ecosystems integrating sensors, wear-time tracking, posture monitoring, and cloud-based dashboards enable continuous remote supervision and data-driven adjustments.

These technologies create new recurring-revenue models for manufacturers and clinics, while offering payers better outcome visibility.

Furthermore, emerging fusionless systems including tethering and growth-friendly implants are opening high-value niches that appeal to surgeons seeking motion-preserving, less invasive solutions.

When combined with navigation systems and minimally invasive robotics, these approaches enhance surgical precision and reduce complications, boosting demand for premium implants, advanced instrument sets, and integrated robotic platforms, creating significant opportunities for scoliosis management market.

Category-wise Analysis

By Product Insights - Thoracolumbosacral Orthosis (TLSO) Dominates Globally Due to Advanced Programmable Drug Delivery and Enhanced Safety Features

The thoracolumbosacral orthosis (TLSO) segment is projected to dominate the global scoliosis management market in 2026, accounting for a revenue share of 34.6%. The segment’s strong performance is primarily driven by its role in non-surgical intervention for adolescent idiopathic scoliosis, which represents the largest and most clinically active patient population worldwide.

TLSO devices provide effective three-point corrective pressure, better spinal stabilization, and strong evidence-based outcomes, making them the most widely prescribed brace type across hospitals, orthopedic clinics, and specialized spine centers.

The growing preference for custom-molded and digitally designed TLSO braces, including 3D-printed variants, is further accelerating their uptake. Advances in CAD/CAM scanning, lightweight composite materials, and smart sensor integration have significantly improved comfort, wear-time compliance, and aesthetics, addressing the historical limitations of bracing therapy.

By Disease Type Insights - Idiopathic Scoliosis Leads the Market Globally Due to Cost-Efficiency and Reduced Long-Term Treatment Expenses

The idiopathic scoliosis segment is projected to dominate the global Scoliosis Management market in 2026, accounting for a revenue share of 54.7%. This is driven by the high prevalence of adolescent idiopathic scoliosis (AIS), which represents the most commonly diagnosed form of the condition worldwide.

Large-scale school screening programs, improved pediatric surveillance, and growing clinical awareness among parents and caregivers are enabling earlier detection, increasing the number of patients entering conservative management pathways such as bracing and physiotherapy.

Additionally, idiopathic scoliosis patients respond well to established treatment protocols, making this category the most actively managed and clinically standardized segment. The availability of evidence-based bracing options like TLSO, combined with advancements in custom-fit 3D-printed orthoses and posture-monitoring technologies, continues to strengthen treatment adoption.

By Distribution Channel Insights - Hospital Pharmacies are Leading Due to High Patient Volumes, Advanced Infusion Care Infrastructure, and Strong Reimbursement Support

The hospital pharmacies segment is projected to dominate the global Scoliosis Management market in 2026, accounting for a revenue share of 54.5%. This is driven by their central role in dispensing prescribed braces, pain-management medications, and post-operative rehabilitation supplies for both pediatric and adult scoliosis patients.

Hospitals typically serve as the primary point of diagnosis and treatment initiation, enabling pharmacy units within these facilities to capture the highest prescription volume and ensure timely access to orthotic products and supportive therapies.

Moreover, the strong presence of multidisciplinary spine centers, pediatric orthopedic departments, and surgical units within hospitals contributes to steady patient inflow and repeat visits for brace adjustments, follow-ups, and medication refills.

Region-wise Insights

North America Scoliosis Management Market Trends

North America is expected to dominate globally with a value share of 45.8% in 2026, with the U.S. leading the region due to its highly advanced healthcare infrastructure, strong presence of specialized spine centers, and widespread adoption of evidence-based scoliosis treatment protocols.

Higher diagnostic rates, greater awareness among pediatric and adult populations, and a well-established reimbursement framework further support early intervention and sustained treatment uptake.

Additionally, the region benefits from rapid integration of innovative technologies, including 3D-printed braces, sensor-enabled orthoses, and minimally invasive surgical systems which are more widely accessible through U.S. hospitals and orthopedic clinics. Strong industry presence, continuous product launches, and substantial R&D investments also contribute to maintaining North America’s leadership position in the global scoliosis management market.

Europe Scoliosis Management Market Trends

The Europe market is expected to grow steadily, driven by increasing early diagnosis rates, stronger pediatric monitoring frameworks, and the expansion of school-based musculoskeletal screening programs across several countries.

These initiatives are enabling earlier identification of adolescent idiopathic scoliosis, boosting demand for conservative interventions such as bracing and physiotherapy. Europe’s well-established network of orthopedic specialists, spine care centers, and rehabilitation facilities further supports consistent patient inflow and long-term management.

In addition, the region is witnessing rising adoption of advanced orthotic solutions, including 3D-printed custom TLSO and LSO braces, which offer improved comfort, aesthetics, and clinical precision. Growing interest in digital health integration such as posture-monitoring apps, tele-rehabilitation, and remote brace compliance tracking is also contributing to treatment modernization.

Supportive reimbursement structures in countries such as Germany, France, and the Nordics, combined with expanding access to minimally invasive corrective procedures, drive market growth in the region.

Asia Pacific Scoliosis Management Market Trends

The Asia Pacific market is expected to register a relatively higher CAGR of around 7.8% between 2026 and 2033, fueled by a rapidly expanding patient pool, rising awareness of spinal deformities, and significant improvements in pediatric and orthopedic healthcare infrastructure across major economies such as China, India, Japan, and South Korea.

Increasing early diagnosis of adolescent idiopathic scoliosis, combined with growing acceptance of non-invasive bracing solutions, is driving higher treatment uptake across both urban and semi-urban settings.

The region is also benefiting from rising healthcare expenditure, expanding private hospital networks, and the growing availability of advanced orthotic technologies, including 3D-printed braces and digital scanning systems. Local manufacturing capacity for cost-effective orthoses continues to strengthen, improving accessibility for price-sensitive populations.

Additionally, increasing adoption of minimally invasive spine procedures, government-led healthcare modernization initiatives, and a surge in physiotherapy and rehabilitation services further support the strong growth in the region.

Competitive Landscape

The global scoliosis management market is highly competitive, with major players such as Boston Orthotics & Prosthetics, Globus Medical, Spinal Technology, LLC, Chaneco, and Charleston Bending Brace leveraging broad product portfolios, advanced bracing technologies, and strong international distribution networks.

Companies are increasingly focusing on innovation in 3D-printed orthoses, lightweight custom TLSO/LSO designs, and sensor-enabled smart braces aimed at improving patient comfort, enhancing compliance, and enabling real-time monitoring across hospital, clinic, and home-care settings.

Market participants are actively investing in next-generation platforms that incorporate digital scanning, CAD/CAM modeling, posture-tracking sensors, remote monitoring dashboards, and AI-driven customization algorithms to optimize brace fit and treatment outcomes.

Strategic initiatives include mergers and acquisitions to strengthen orthotic manufacturing capabilities, collaborations with orthopedic and pediatric spine centers for clinical validation, and expansion into high-growth markets such as Asia Pacific, Latin America, and the Middle East.

Key Industry Developments:

- In April 2025, OrthoPediatrics Corp. launched its new VerteGlide Spinal Growth Guidance System in the U.S., designed for the treatment of Early Onset Scoliosis (EOS). This marks the company’s 80th pediatric-focused system, reinforcing its expanding portfolio of musculoskeletal solutions for children.

- In May 2023, Globus Medical, Inc. received FDA approval for its REFLECT™ Scoliosis Correction System, marking the company’s first humanitarian device. The system is designed to treat progressive scoliosis in young patients by correcting curvature while preserving spinal motion, maintaining stability, and supporting continued modulated growth.

Companies Covered in Scoliosis Management Market

- Boston Orthotics & Prosthetics.

- Globus Medical

- Spinal Technology, LLC.

- Chaneco

- Charleston Bending Brace

- ORTHOTECH INDIA PRIVATE LIMITED

- Wilmington Orthotics & Prosthetics Inc.

- Lawall

- Horton's Orthotics & Prosthetics

- Aspen Medical Products

- UNYQ

- C H Martin Company

- Biomotion. Prosthetics & Orthotics.

- Others

Frequently Asked Questions

The global scoliosis management market is projected to be valued at US$ 3.6 Bn in 2026.

The growing prevalence of scoliosis, rising adoption of minimally invasive correction systems, and continuous advancements in spinal implants and bracing technologies are driving the global scoliosis management market.

The global scoliosis management market is poised to witness a CAGR of 5.8% between 2026 and 2033.

Expanding adoption of motion-preserving scoliosis correction systems and growing demand for advanced pediatric scoliosis solutions are creating opportunities in the market.

Boston Orthotics & Prosthetics, Globus Medical, Spinal Technology, LLC., Chaneco, and Charleston Bending Brace are some of the key players in the scoliosis management market.