- Pharmaceuticals

- Schizophrenia Treatment Market

Schizophrenia Treatment Market Size, Trends, Share, Growth, and Regional Forecast, 2026 to 2033

Schizophrenia Treatment Market by Product Type (Antipsychotic Drugs, Long-Acting Injectables, Psychosocial Therapies, Electroconvulsive Therapy (ECT), Digital Therapeutics), by Distribution Channel (Hospital Pharmacies, Drug Stores, Retail Pharmacies, E-Commerce, Others), and Regional Analysis from 2026 to 2033

Schizophrenia Treatment Market Share and Trends Analysis

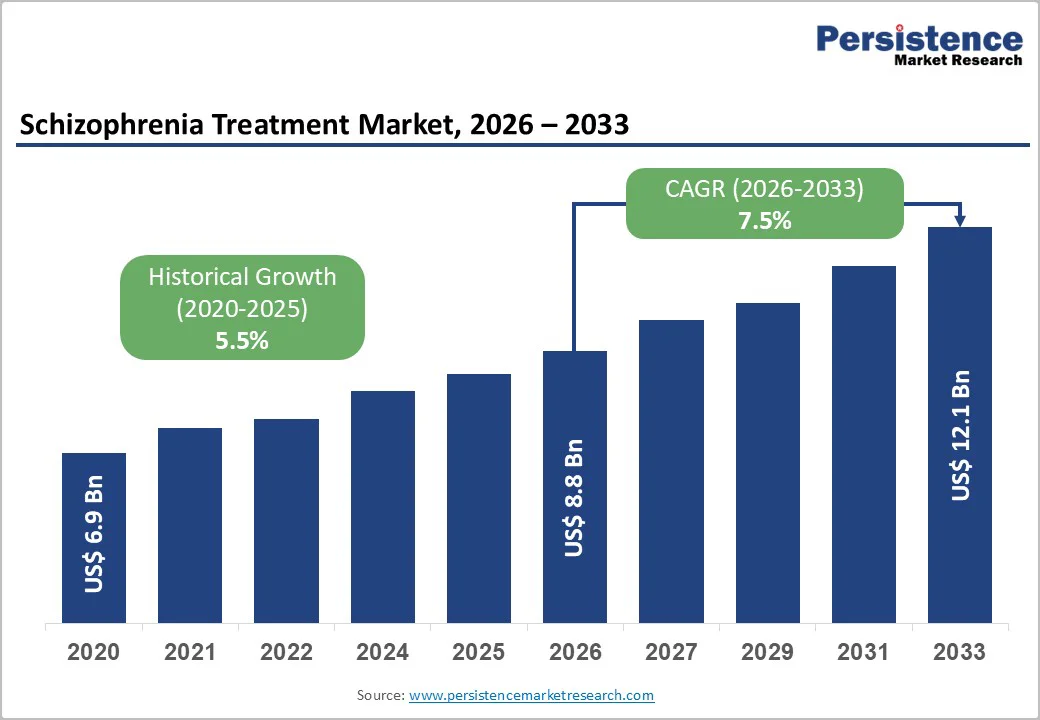

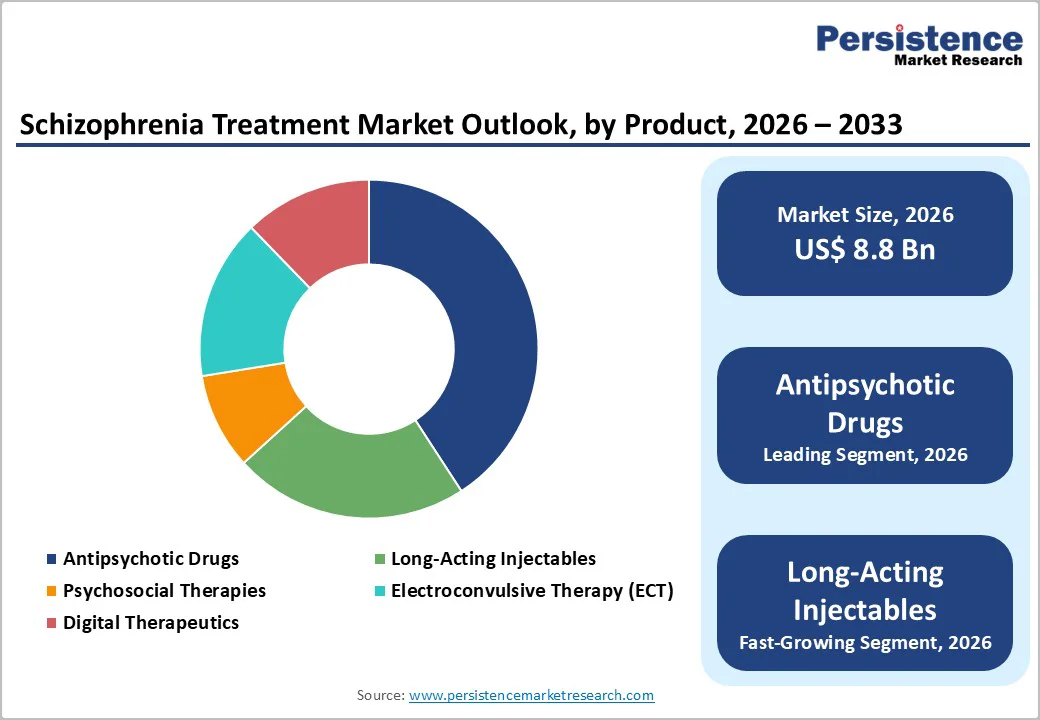

The global schizophrenia treatment market size is estimated to grow from US$8.8 billion in 2026 to US$12.1 billion by 2033. The market is projected to record a CAGR of 4.6% during the forecast period from 2026 to 2033.

Rise in disease prevalence, improved diagnostic access, and adoption of advanced long-acting antipsychotic formulations. Second-generation antipsychotics remain the standard of care due to better safety versus older drugs. Growing preference for long-acting injectables improves adherence and reduces relapse rates, boosting prescription volume.

Digital tools, telepsychiatry, and personalized therapy enhance disease monitoring and patient management. Increasing R&D investment into non-dopaminergic mechanisms, such as glutamate-based therapies, supports innovation. However, high treatment costs, medication non-compliance, and limited awareness in emerging economies remain barriers. Expanding reimbursement coverage and psychiatric infrastructure continue to support market growth.

Key Industry Highlights:

- Second-generation antipsychotics continue dominating prescriptions due to improved tolerability, lower EPS risk, and better symptom control.

- Telepsychiatry, digital therapy platforms, medication-reminder apps, and remote counseling increase compliance.

- Pipeline drugs are exploring glutamatergic pathways, serotonergic modulation, TAAR agonists, and inflammation-linked mechanisms.

- Antipsychotic drugs account for the highest market share because they are the primary and first-line standard of care for almost all diagnosed schizophrenia patients.

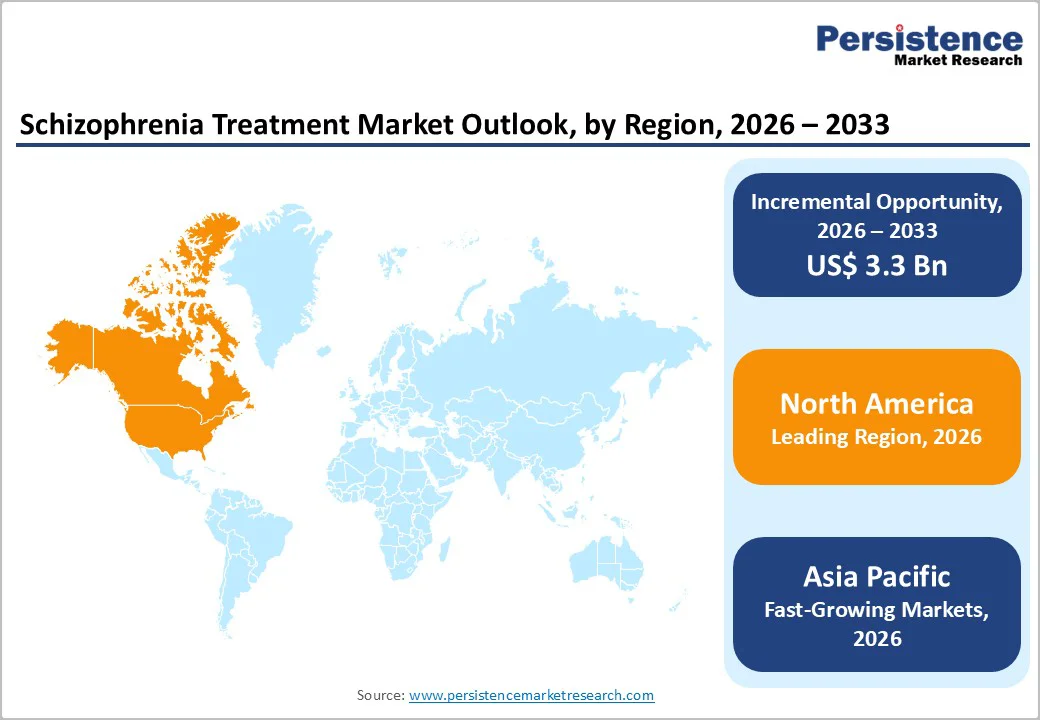

- North America accounts for the largest share of the global antipsychotic-drugs / schizophrenia treatments market.

| Key Insights | Details |

|---|---|

| Schizophrenia Treatment Market Size (2026E) | US$8.8 Bn |

| Market Value Forecast (2033F) | US$12.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.5% |

Market Dynamics

Driver - Rising Awareness of Equine Health and Expansion of Equestrian Sports

The shift toward Long-Acting Injectables (LAIs) is one of the most significant trends in the schizophrenia treatment market. LAIs are gaining preference among physicians and psychiatrists because they address one of the biggest challenges in schizophrenia care: medication non-adherence. Many patients struggle with daily oral regimens due to forgetfulness, side effects, or lack of insight into their condition, which often leads to relapse and hospitalization. LAIs, administered once monthly, quarterly, or at other extended intervals, provide consistent therapeutic levels of medication, significantly reducing relapse rates and improving long-term outcomes. Moreover, LAIs support better monitoring by caregivers and healthcare providers, enhancing patient engagement and continuity of care. The convenience of fewer injections and reduced need for daily compliance encourages both physician recommendation and patient acceptance. Consequently, pharmaceutical companies are investing heavily in developing and marketing LAIs, which is driving rapid growth in the injectable antipsychotic segment and reshaping the overall schizophrenia treatment landscape.

Restraints - Limited Access to Psychiatric Care

Limited Access to Psychiatric Care is one of the most critical restraints in the schizophrenia treatment market. Across many regions, particularly in rural and semi-urban areas, there is a significant shortage of trained psychiatrists, clinical psychologists, and mental health specialists. This shortage leads to delayed diagnosis, misdiagnosis, or under-treatment of schizophrenia, as general practitioners often lack the expertise to manage complex psychiatric cases. Early-stage intervention is crucial for improving long-term outcomes, but the absence of specialized care means that many patients only receive treatment during acute episodes, increasing relapse rates and hospitalization. Additionally, rural healthcare facilities often lack the necessary infrastructure for administering long-acting injectables, monitoring side effects, or providing psychosocial therapy, further limiting comprehensive treatment. The scarcity of mental health professionals also increases patient load on urban centers, creating overburdened systems and longer waiting times. Collectively, these gaps reduce treatment adherence, worsen disease progression, and restrict market growth by limiting patient access to essential schizophrenia therapies.

Opportunity - Digital Therapeutics & Telepsychiatry

Digital therapeutics and telepsychiatry are transforming schizophrenia care by bridging gaps in access, adherence, and continuous monitoring. Mobile applications now enable patients to track symptoms, medication schedules, and mood changes in real time, generating actionable data for clinicians. AI-driven platforms analyze these inputs to identify early signs of relapse, allowing timely interventions before acute episodes occur. Telepsychiatry expands mental-health services to rural and underserved areas, where psychiatric specialists are scarce, providing virtual consultations, therapy sessions, and caregiver guidance. These tools also facilitate personalized care plans, tailored reminders, and digital cognitive-behavioral programs that complement pharmacological treatment. Importantly, digital solutions reduce stigma by offering private, home-based care, improving patient engagement and long-term adherence. With integration into electronic health records and predictive analytics, digital therapeutics not only enhance clinical outcomes but also lower hospitalization rates, cut healthcare costs, and create a scalable, data-driven approach to managing schizophrenia globally.

Category-wise Analysis

By Product Type Insights

Antipsychotic drugs account for the highest market share in schizophrenia treatment because they are the foundation of care for all stages of the disease, from acute episodes to long-term maintenance. Globally, treatment guidelines recommend immediate initiation of antipsychotic therapy upon diagnosis, making these drugs universally prescribed for both first-episode and chronic patients. Second-generation antipsychotics dominate this segment due to their superior efficacy in controlling positive and negative symptoms, along with a lower risk of extrapyramidal side effects compared to first-generation drugs. Oral formulations are widely accessible, and generic availability further enhances affordability, expanding patient reach across both developed and emerging markets. Additionally, long-acting injectable antipsychotics are increasingly adopted to improve adherence and reduce relapse rates, reinforcing market demand. The combination of high prescription frequency, long-term use, and broad clinical applicability ensures that antipsychotic drugs remain the largest and most consistently used segment in the schizophrenia treatment market.

By Distribution Channel Insights

Hospital pharmacies hold the highest share in the schizophrenia treatment market because hospitals are the primary point of care for diagnosis, treatment initiation, and ongoing management of patients. Most antipsychotic medications, including oral and long-acting injectable formulations, are prescribed and dispensed within hospital settings to ensure correct dosing, monitor side effects, and manage acute episodes. Long-acting injectables, in particular, require administration under medical supervision, further concentrating demand in hospitals. Additionally, hospitals provide integrated psychiatric care, including follow-up consultations, therapy sessions, and adherence monitoring, making hospital pharmacies the most reliable channel for consistent prescription fulfillment. While retail pharmacies, drug stores, and e-commerce platforms support outpatient access, they handle smaller volumes because schizophrenia treatment often requires professional oversight, controlled administration, and continuous monitoring, solidifying hospital pharmacies’ dominant role in the market.

Region-wise Insights

North America Schizophrenia Treatment Market Trends

North America leads the global schizophrenia treatment market due to advanced healthcare infrastructure, high diagnosis rates, and strong insurance coverage. In the U.S., the majority of patients have access to second-generation antipsychotics, which dominate prescriptions because of their efficacy and improved safety profiles. Long-acting injectables are gaining traction, particularly for treatment-resistant patients, as they improve adherence and reduce hospitalizations.

Telepsychiatry and digital therapeutics are increasingly integrated into care, enabling remote monitoring and early intervention, especially in rural or underserved areas. Government initiatives and mental health awareness campaigns are reducing stigma, encouraging timely treatment initiation. Hospitals and hospital pharmacies remain the primary distribution channel, while retail pharmacies and e-commerce channels are expanding outpatient access. Combined, these factors reinforce North America’s leading position, driving both treatment uptake and innovation in schizophrenia care.

Asia Pacific Schizophrenia Treatment Market Trends

The Asia Pacific region is emerging rapidly in the schizophrenia treatment market, driven by increasing awareness, improving healthcare infrastructure, and rising diagnosis rates. Countries like China, India, and Japan are witnessing growing adoption of second-generation antipsychotics, supported by expanding hospital networks and mental health programs. Long-acting injectables are gradually gaining acceptance, particularly in urban centers, to improve patient adherence and reduce relapse. Telepsychiatry and digital health solutions are playing a key role in bridging the gap between urban and rural care, providing remote consultations and adherence monitoring. Government initiatives, mental health policies, and NGO-led awareness campaigns are enhancing treatment access and reducing stigma. The combination of growing patient population, expanding hospital and pharmacy networks, and increasing insurance coverage positions Asia Pacific as a high-growth, emerging market for schizophrenia therapies.

Competitive Landscape

The schizophrenia treatment market report provides valuable insight with an emphasis on the dynamic The schizophrenia treatment market is highly competitive, driven by innovation, product differentiation, and expanding access to care. Companies focus on launching new antipsychotic drugs, long-acting injectable formulations, and generic alternatives to capture market share. Advances in digital therapeutics, telepsychiatry, and non-dopaminergic therapies are intensifying competition by addressing treatment-resistant cases and improving patient adherence. Strategic collaborations, mergers, and regional expansions further enhance competitive positioning.

Key Industry Developments:

- In September 2025, the FDA approved an injectable extended-release suspension of risperidone by Amneal Pharmaceuticals, referencing Risperdal Consta (Janssen Biotech), for treating patients with schizophrenia. Following this approval, the extended-release formulation was made available in 12.5-, 25-, 37.5-, and 50-mg vials.

Companies Covered in Schizophrenia Treatment Market

- Johnson & Johnson (Janssen)

- Eli Lilly and Company

- AstraZeneca

- Otsuka Pharmaceutical

- Alkermes plc

- Bristol-Myers Squibb

- H. Lundbeck A/S

- Pfizer Inc.

- AbbVie Inc.

- Teva Pharmaceutical Industries Ltd.

- Sumitomo Pharma

- Vanda Pharmaceuticals

- GlaxoSmithKline (GSK)

- Novartis AG

- Sanofi S.A.

- Other

Frequently Asked Questions

The global schizophrenia treatment market is projected to be valued at US$8.8 Bn in 2026.

The increasing number of cases worldwide, especially in urban populations, expands the patient pool requiring treatment.

The global market is poised to witness a CAGR of 4.6% between 2026 and 2033.

Remote monitoring, mobile apps, and virtual consultations for rural and underserved populations.

Johnson & Johnson (Janssen), Eli Lilly and Company, AstraZeneca, Otsuka Pharmaceutical, and others.