- Pharmaceuticals

- Malignant Mesothelioma Market

Malignant Mesothelioma Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Malignant Mesothelioma Market by Drug Type (Pemetrexed, Cisplatin, Carboplatin, Gemcitabine, Vinorelbine, Others), Route of Administration (Oral, Parenteral), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Oncology Centers), and Regional Analysis from 2026 to 2033

Malignant Mesothelioma Market Size and Trends Analysis

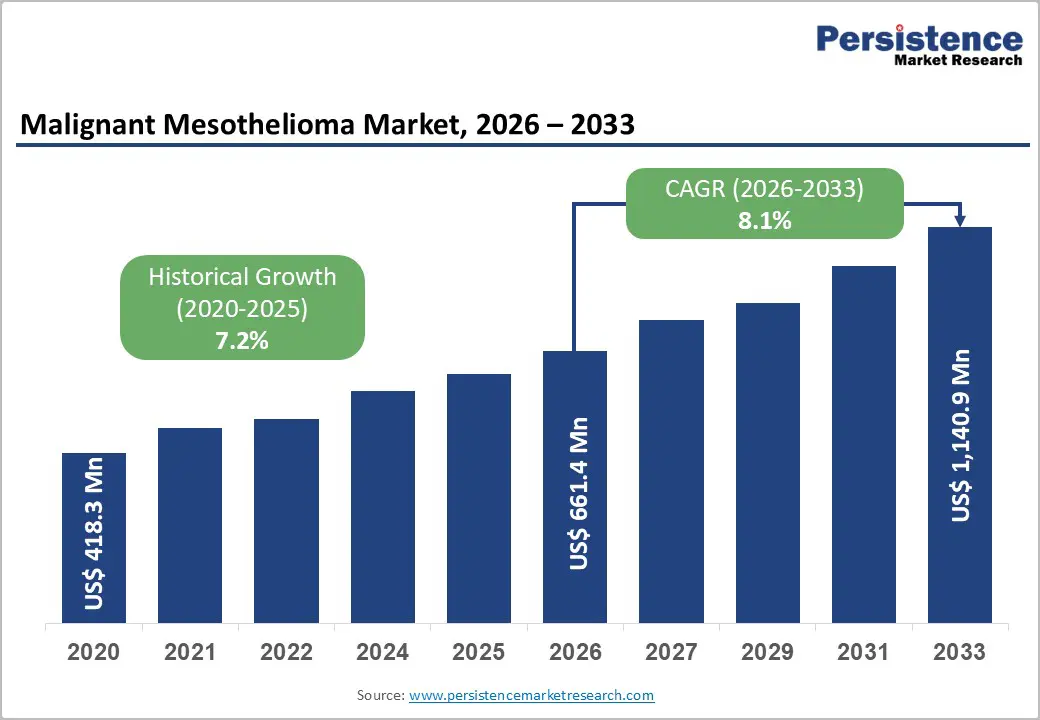

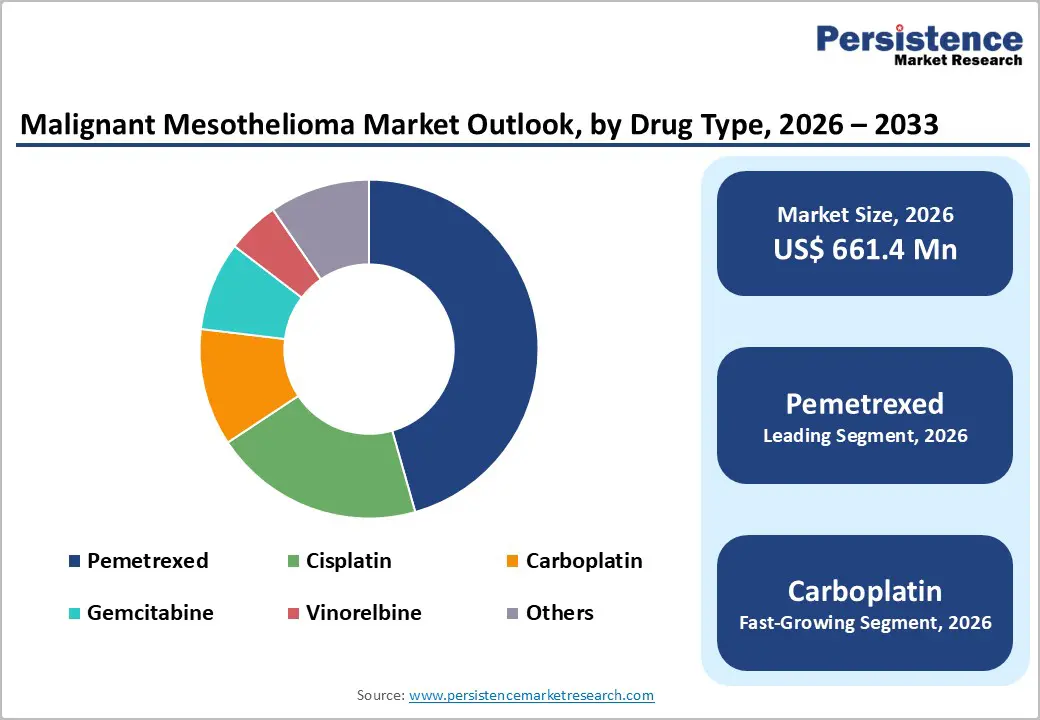

The global malignant mesothelioma market is estimated to grow from US$ 661.4 Mn in 2026 to US$ 1,140.9 Mn by 2033. The market is projected to record a CAGR of 8.1% during the forecast period from 2026 to 2033.

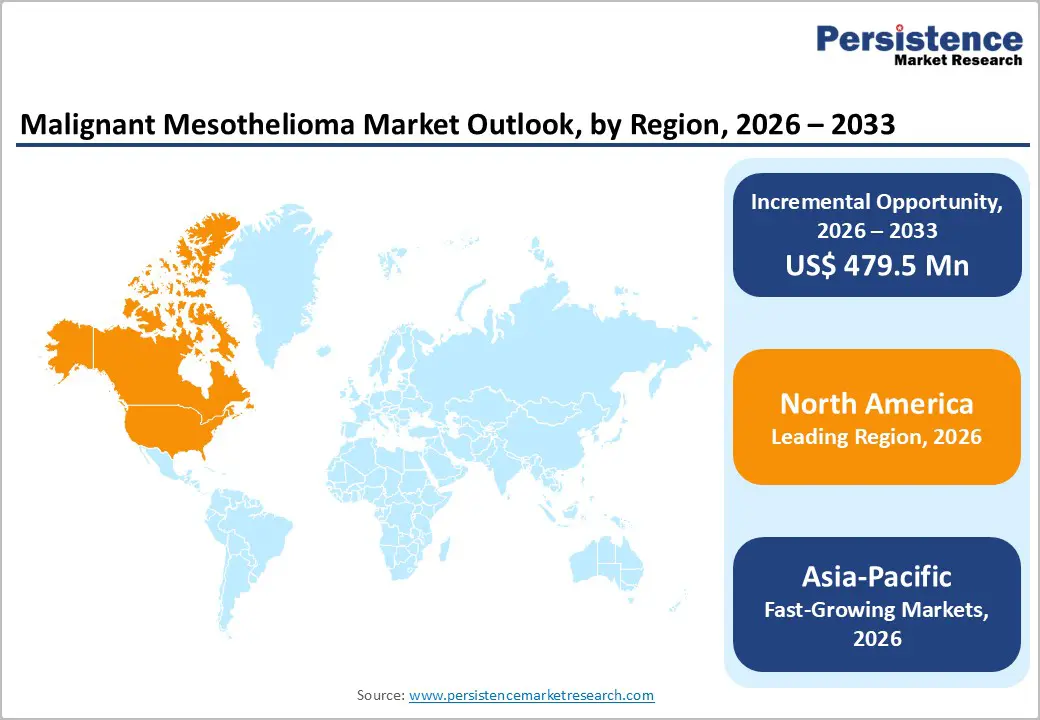

The global malignant mesothelioma market is witnessing steady growth, driven by rising asbestos exposure cases, advances in diagnostics, and improving treatment options such as immunotherapy and targeted therapies. North America is dominated due to early diagnosis and strong healthcare systems, while Asia-Pacific is the fastest-growing region owing to increasing awareness, improving healthcare infrastructure, and expanding treatment access.

Key Industry Highlights

- Dominant Segment: Pemetrexed represents the leading drug type in the Malignant Mesothelioma Market, accounting for 45.6% share in 2025. Its dominance is driven by its long-established role as the standard first-line chemotherapy, widespread clinical adoption in combination with platinum-based agents, proven efficacy in improving survival outcomes, and strong inclusion in international treatment guidelines.

- Dominant Region: North America leads the market with 45.3% share in 2025, due to early diagnosis, strong oncology infrastructure, high treatment adoption, and favorable reimbursement frameworks. Asia-Pacific is the fastest-growing region, supported by rising asbestos exposure cases, improving healthcare access, growing awareness, and expanding oncology treatment capabilities.

- Market Drivers: Key growth drivers include increasing incidence of asbestos-related diseases, advances in immunotherapy and targeted treatments, improved diagnostic techniques, and rising investments in oncology research and clinical trials.

- Market Opportunity: Emerging opportunities include novel immunotherapies, combination treatment regimens, biomarker-based personalized therapy, expansion of treatment access in developing regions, and ongoing clinical development of next-generation targeted agents.

| Global Market Attributes | Key Insights |

|---|---|

| Global Malignant Mesothelioma Market Size (2026E) | US$ 661.4 Mn |

| Market Value Forecast (2033F) | US$ 1,140.9 Mn |

| Projected Growth (CAGR 2026 to 2033) | 8.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.2% |

Market Dynamics

Driver: Rising incidence of asbestos-related diseases

The rising incidence of asbestos-related diseases significantly drives the malignant mesothelioma market by increasing demand for effective diagnosis and treatment solutions. Asbestos exposure remains a major global health issue, with World Health Organization estimates indicating that occupational and environmental exposure leads to more than 200,000 deaths annually from asbestos-related diseases including mesothelioma, lung cancer, and asbestosis. Mesothelioma itself accounts for a substantial proportion of these mortality figures, with global incident cases reported near 30,000–35,000 per year and age-standardized incidence around 0.30 per 100,000 persons, especially higher in regions historically using asbestos.

Historical and ongoing exposure contribute to persistent case numbers despite bans in many countries. The long latency period, often 20–60 years between first exposure and disease onset means that cases continue to occur even after asbestos use is restricted, sustaining clinical demand. In the United States, for example, 2,669 new mesothelioma cases were reported in 2022, reflecting continued asbestos-associated disease burden. This sustained incidence directly supports market growth through greater need for diagnostics, oncology therapies, and healthcare services targeted at mesothelioma management.

Restraints: High treatment costs and limited reimbursement in developing regions

High treatment costs present a significant constraint on the malignant mesothelioma market, particularly in low- and middle-income countries where healthcare financing is limited. Mesothelioma treatment often involves multimodal care, surgery, chemotherapy, immunotherapy, and radiation with total expenses frequently exceeding USD 400,000 per patient in advanced care settings, even in well-insured systems. Immunotherapy alone can cost USD 150,000–292,000 per year, placing a heavy financial burden on patients and families. Such high prices translate into affordability barriers where out-of-pocket payments dominate, and insurance coverage is incomplete or absent for expensive therapies.

In many developing regions, reimbursement systems are underdeveloped or non-existent for costly oncology drugs and procedures. A study in Morocco found that the cost of a course of pembrolizumab, a widely used immunotherapy, can amount to about eight times the average monthly income, underscoring profound affordability challenges outside high-income markets. Limited public funding, lack of comprehensive insurance coverage for novel therapies, and high ancillary costs (travel, diagnostics, follow-up) compound access disparities. These financial constraints reduce treatment uptake and restrict market growth, as patients defer or forego effective therapies due to cost pressures.

Opportunity: Development of novel immunotherapies and combination regimens

The development of novel immunotherapies and combination regimens presents a significant growth opportunity for the malignant mesothelioma market by improving treatment outcomes and expanding therapeutic options. Regulatory advancements highlight this trend: the U.S. Food and Drug Administration approved the combination of nivolumab and ipilimumab as a first-line treatment for unresectable malignant pleural mesothelioma, demonstrating a median overall survival of 18.1 months compared with 14.1 months for chemotherapy alone in the CheckMate-743 trial. This approval reflects validation of immune checkpoint blockade in clinical practice. Additionally, pembrolizumab combined with pemetrexed and platinum chemotherapy has also been approved, showing higher objective response rates (52% versus 29%) and median survival benefits (17.3 versus 16.1 months) compared with chemotherapy alone. These regulatory outcomes underscore the clinical and commercial promise of immunotherapy combinations.

More than fifty active clinical trials in the U.S. alone are exploring immunotherapy strategies, including combinations with chemotherapy, novel agents, and immune modulators, indicating robust research momentum. Immune checkpoint inhibitors like PD-1/PD-L1 and CTLA-4 blockers, as well as emerging modalities such as perioperative immunotherapy and adoptive cell therapy, are under investigation to improve survival beyond current standards. Combination approaches have shown higher efficacy in meta-analyses, with dual checkpoint blockade and chemo-immunotherapy demonstrating improved survival outcomes over monotherapy. This expanding pipeline not only increases treatment options for patients but also supports long-term market growth as newer, more effective regimens gain regulatory and clinical traction.

Category-wise Analysis

By Drug Type, Pemetrexed Dominates the Malignant Mesothelioma Market

Pemetrexed occupies 45.6% share of the global market in 2025, because it is the established standard chemotherapy backbone that has consistently demonstrated superior clinical outcomes compared to older regimens. In the pivotal randomized trial that supported its regulatory approval, pemetrexed combined with cisplatin significantly improved median overall survival to 12.1 months versus 9.3 months with cisplatin alone and boosted tumor response rates to 41.3% compared with 16.7% for cisplatin, while also extending time to progression. These meaningful survival and response benefits underpin its global clinical adoption as first line therapy for malignant pleural mesothelioma. Additionally, recent approvals of pemetrexed in combination with immunotherapy (e.g., pembrolizumab) further reinforce its central role in evolving treatment protocols.

By Route of Administration, Parenteral administration dominates mesothelioma treatment as IV delivery ensures effective, controlled, and monitored chemotherapy and immunotherapy

Parenteral administration dominates the malignant mesothelioma market by route of administration because the primary and most effective treatments, systemic chemotherapy and immunotherapy are given intravenously, ensuring the drugs enter the bloodstream directly to reach cancer cells throughout the body. For example, standard agents such as pemetrexed, cisplatin, carboplatin, nivolumab, and ipilimumab are routinely delivered via IV infusion in clinical practice, as documented by the U.S. National Cancer Institute and American Cancer Society. IV infusion allows precise dose control, predictable pharmacokinetics, and direct monitoring by healthcare professionals, which is essential given the potency and toxicity of these agents. Oral chemotherapy is less common in mesothelioma due to issues with absorption and effectiveness, making parenteral routes the established norm in treatment protocols.

Regional Insights

North America Malignant Mesothelioma Market Trends

North America dominates the malignant mesothelioma market with 45.3% share in 2025, due to its historically high asbestos exposure and advanced healthcare ecosystem. In the United States alone, approximately 2,669 new mesothelioma cases were reported in 2022, reflecting a continuing disease burden despite reduced asbestos use over time, and driving demand for effective treatments and care infrastructure. The region’s comprehensive oncological infrastructure, including highly developed cancer centers, widespread access to diagnostic technologies, and robust insurance coverage enables early diagnosis and adoption of advanced therapies such as immunotherapy and multimodal regimens. Additionally, strong clinical research activity and regulatory support through agencies like the U.S. FDA facilitate rapid approval and uptake of innovative treatments, further reinforcing North America’s leadership in the mesothelioma market.

Europe Malignant Mesothelioma Market Trends

Europe is an important region in the malignant mesothelioma market due to its substantial disease burden and historical asbestos exposure. According to WHO’s GLOBOCAN 2022 data, Europe accounted for approximately 48.1% of global mesothelioma cases and 48.4% of deaths, making it the region with the highest share worldwide. In the European Union alone, Eurostat reported mesothelioma as the second most common occupational cancer, with 1,409 new cases in 2021 and 13,530 cases between 2013 and 2021.

These figures reflect the long term impact of extensive historical asbestos use across European industries, particularly in construction, shipbuilding, and manufacturing, which continues to drive incidence despite bans. The ongoing healthcare response and surveillance systems across Europe contribute to sustained diagnosis, treatment adoption, and clinical research efforts, reinforcing the region’s significance in global mesothelioma care and market demand.

Asia-Pacific Malignant Mesothelioma Market Trends

Asia Pacific is the fastest growing region in the malignant mesothelioma market largely because continued or historical asbestos use and emerging healthcare investment are driving a rising disease burden and improving care access. Although age standardized incidence rates in parts of Asia remain lower than in Europe or North America, the region accounted for 28.1 % of global mesothelioma cases in 2022, second only to Europe, reflecting a substantial share of the disease burden. Many Asian countries have historically increased asbestos consumption, with per capita use rising markedly since the 1970s, suggesting future case increases as long latency periods unfold. Concurrently, expanding healthcare infrastructure and diagnostics in China, India, and Southeast Asia are facilitating higher detection rates and treatment uptake, accelerating market growth.

Market Competitive Landscape

Leading companies in the malignant mesothelioma market focus on advanced therapies, including chemotherapy and immunotherapy, and regulatory compliance. Investments in clinical research, combination regimens, and biomarker-driven approaches enhance treatment efficacy. Collaborations with oncology centers, standardized protocols, and quality monitoring drive innovation, support widespread adoption, and improve patient outcomes in diagnosis, therapy, and personalized mesothelioma care.

Key Industry Developments:

- In June 2025, Ono Pharmaceutical Co., Ltd. and Bristol Myers Squibb K.K. received supplemental regulatory approval in Japan for the combination of Opdivo® (nivolumab) and Yervoy® (ipilimumab) to expand its use for the treatment of unresectable hepatocellular carcinoma (HCC).

- In September 2024, The U.S. Food and Drug Administration approved Merck’s KEYTRUDA® (pembrolizumab) in combination with pemetrexed and platinum based chemotherapy as a first line treatment for adult patients with unresectable advanced or metastatic malignant pleural mesothelioma (MPM).

Companies Covered in Malignant Mesothelioma Market

- AstraZeneca Plc.

- Bristol-Myers Squibb Company

- F. Hoffmann-La Roche Ltd.

- Merck & Co., Inc.

- Novartis AG

- Pfizer Inc.

- Sanofi

- Eli Lilly and Company

- Teva Pharmaceuticals

- Boehringer Ingelheim GmbH

- Mylan N.V.

- Fresenius Kabi AG

- Sun Pharmaceuticals Industries Ltd

- Corden Pharma International GmbH

- Concordia International Corp

- Kyowa Hakko Kirin Co Ltd.

- Polaris Pharmaceuticals, Inc.

- MolMed SpA

- Ono Pharmaceutical Co. Ltd

- Nichi-Iko Pharmaceutical Co., Ltd

- Others

Frequently Asked Questions

The global malignant mesothelioma market is projected to be valued at US$ 661.4 Mn in 2026.

Rising asbestos exposure, advanced therapies, early diagnosis, immunotherapy adoption, and increasing oncology research drive growth.

The global malignant mesothelioma market is poised to witness a CAGR of 8.1% between 2026 and 2033.

Novel immunotherapies, combination regimens, biomarker-driven personalized treatments, emerging markets, and minimally invasive diagnostics present key opportunities.

AstraZeneca Plc, Bristol-Myers Squibb Company, F. Hoffmann-La Roche Ltd., Merck & Co., Inc., Novartis AG, Pfizer Inc.