- Medical Devices

- Laparoscopic Clip Appliers Market

Laparoscopic Clip Appliers Market Size, Share, and Growth Forecast, 2026 – 2033

Laparoscopic Clip Appliers Market by Product Type (Single-use Clip Appliers, Reusable Clip Appliers), Application Type (General Surgery, Gynecological Surgery, Urological Surgery, Bariatric Surgery, Pediatric Surgery), and Regional Analysis for 2026 – 2033

Laparoscopic Clip Appliers Market Size and Trends Analysis

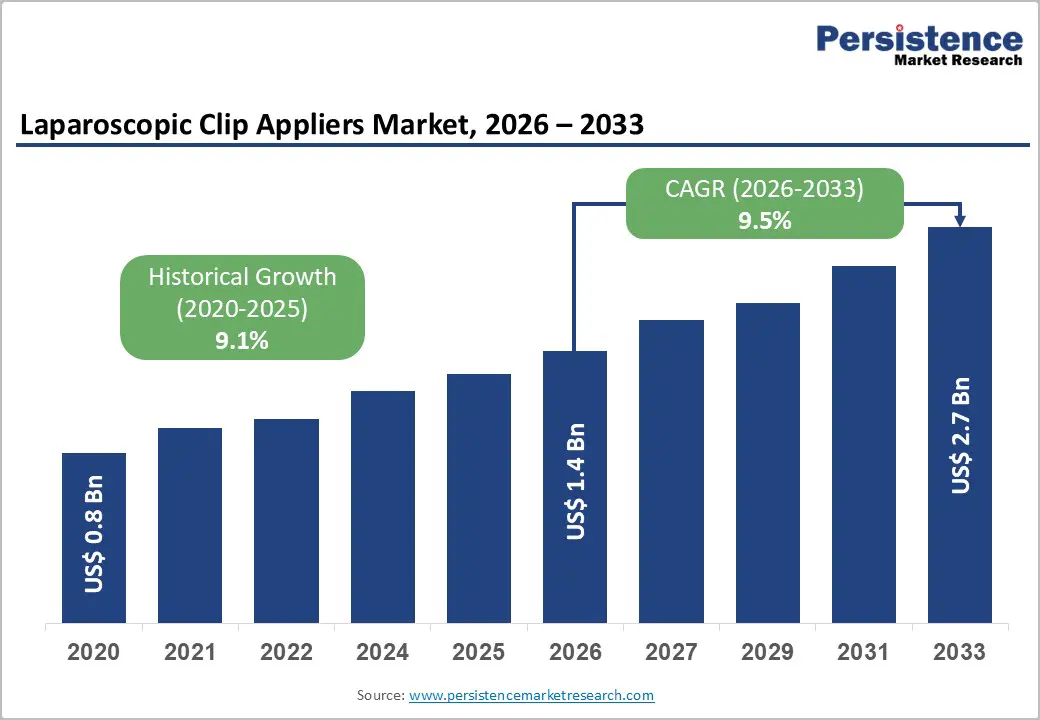

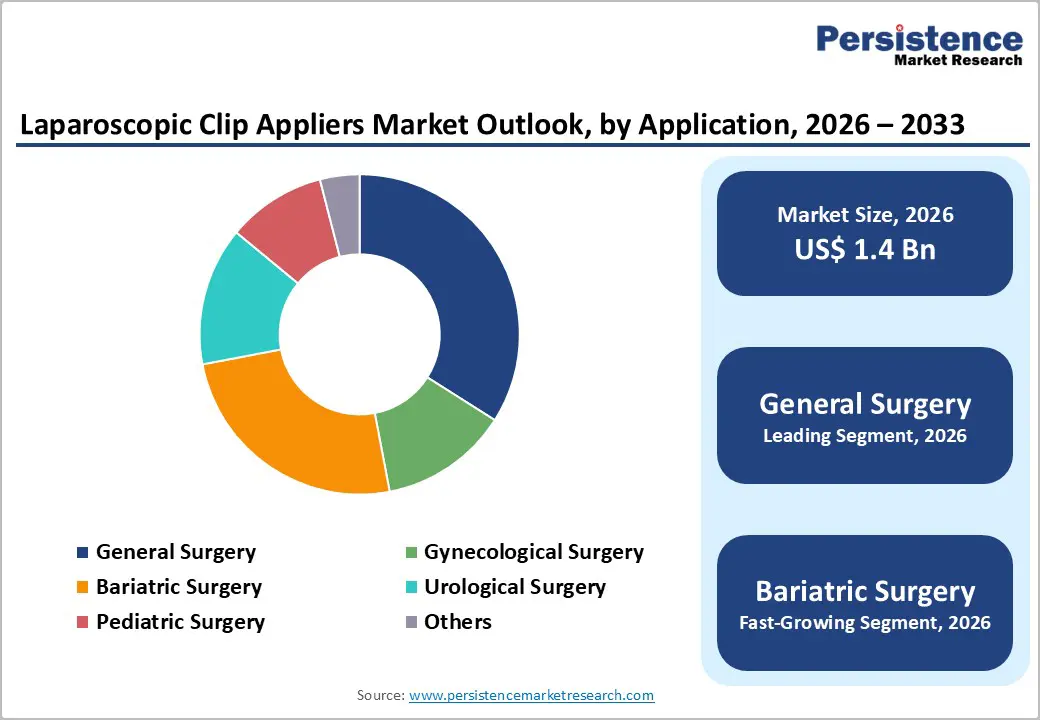

The global laparoscopic clip appliers market size is likely to be valued at US$1.4 billion in 2026 and is expected to reach US$2.7 billion by 2033, growing at a CAGR of 9.5% during the forecast period from 2026 to 2033, driven by the rising adoption of minimally invasive surgical procedures, which offer benefits such as reduced post-operative recovery times, lower infection risks, and shorter hospital stays. The increasing volume of laparoscopic surgeries worldwide, estimated at over 15 million procedures annually, is fueling demand for advanced surgical instruments. Technological advancements in clip appliers, including ergonomic designs, enhanced precision, and integration with robotic-assisted systems, are expanding clinical applications and improving surgeon efficiency.

Key Industry Highlights:

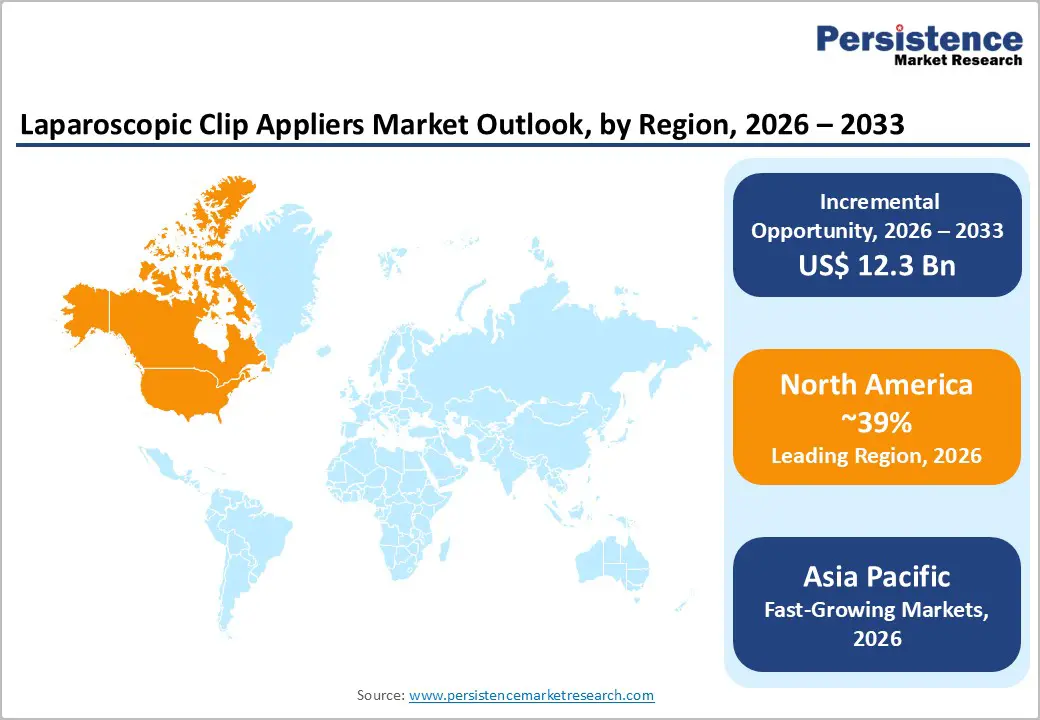

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 39% in 2026, driven by high procedural volumes, advanced healthcare infrastructure, and technological adoption.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in the laparoscopic clip appliers in 2026, driven by rising healthcare investments, medical tourism, and expanding surgical infrastructure.

- Leading Product Type: Single-use clip appliers are projected to represent the leading product type in 2026, accounting for 62% of the revenue share, driven by infection control and convenience in high-volume surgical settings.

- Leading Application: General surgery is anticipated to be the leading application type, accounting for over 45% of the revenue share in 2026, reflecting wide applicability in procedures such as cholecystectomy and appendectomy.

| Key Insights | Details |

|---|---|

| Laparoscopic Clip Appliers Market Size (2026E) | US$1.4 Bn |

| Market Value Forecast (2033F) | US$2.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Preference for Minimally Invasive Surgery (MIS)

Minimally invasive surgery (MIS) techniques, including laparoscopic and robotic-assisted procedures, have become widely adopted across various surgical specialties due to their clear advantages over traditional open surgery. These benefits include smaller incisions, less post-operative pain, reduced infection risk, minimal blood loss, faster patient recovery, and shorter hospital stays. As hospitals and surgical centers increasingly implement MIS protocols, the demand for essential instruments, such as laparoscopic clip appliers used for vessel ligation and tissue closure, has grown. Single-use clip appliers are particularly favored for their convenience, guaranteed sterility, and ease of use in high-volume operating environments.

MIS is increasingly adopted across general, gynecological, urological, bariatric, and pediatric surgeries. Rising rates of chronic diseases, obesity, and elective procedures have driven faster adoption of MIS, with bariatric and urological surgeries emerging as the fastest-growing segments. Advanced healthcare infrastructure in regions such as North America and Europe has further supported the integration of robotic-assisted MIS systems, improving surgical precision and reducing operating times.

Regulatory Hurdles and Reimbursement Challenges

Regulatory approval for medical devices, including clip appliers, requires extensive clinical testing, thorough documentation, and adherence to standards set by authorities such as the U.S. FDA, European CE marking, and national agencies across the Asia Pacific. These procedures are often lengthy and expensive, delaying the introduction of new or innovative products to the market. Variations in regulatory requirements across countries further complicate product launches, as manufacturers must ensure compliance with different safety, performance, and labeling standards.

The high cost of laparoscopic clip appliers, especially single-use and advanced robotic-compatible models, also limits adoption in price-sensitive markets. In many regions, reimbursement policies may not fully cover minimally invasive procedures or disposable instruments, reducing hospitals’ incentive to invest in these devices. Smaller healthcare facilities and emerging economies are particularly affected, restricting market penetration. The combination of regulatory delays, high device costs, and reimbursement constraints slows adoption and revenue growth, highlighting the importance for manufacturers to develop cost-effective solutions and work with policymakers to secure favorable coverage and accelerate market access.

Integration with Robotic-Assisted Surgery

Robotic surgical platforms, such as the da Vinci Surgical System, provide surgeons with greater precision, enhanced dexterity, and improved visualization during minimally invasive procedures. These benefits have driven demand for compatible surgical instruments, including laparoscopic clip appliers, which are crucial for vessel ligation and tissue closure. To meet the needs of these advanced systems, manufacturers are increasingly designing ergonomic, multi-fire, and robot-compatible clip appliers. Integration with robotic surgery not only boosts procedural efficiency but also enables more complex procedures across general, urological, gynecological, and bariatric surgeries, broadening the clinical applications of clip appliers.

The adoption of robotic-assisted surgery is growing rapidly, particularly in North America, Europe, and the Asia Pacific region, fueled by technological advancements and increased healthcare investments. Hospitals and surgical centers are willing to invest in robotic-compatible disposable instruments, creating significant opportunities for manufacturers of single-use clip appliers that offer enhanced sterility and precision. Robotic platforms are seeing increased use in bariatric and urological surgeries, which are among the fastest-growing applications requiring precise vessel ligation. By aligning product development with the trends in robotic surgery, companies can differentiate their offerings, capture emerging market opportunities, and drive long-term revenue growth in both mature and developing regions.

Category-wise Analysis

Product Type Insights

The single-use segment is expected to dominate the laparoscopic clip appliers market, accounting for around 62% of total revenue in 2026. This growth is driven by priorities such as infection control, guaranteed sterility, and operational efficiency in high-volume operating rooms. Disposable clip appliers eliminate the need for complex sterilization, reducing cross-contamination risks and streamlining workflow. For instance, Ethicon’s Endo-Surgery™ disposable clip appliers are commonly used in laparoscopic cholecystectomy and appendectomy procedures, offering surgeons reliable performance and safety. Hospitals and outpatient surgical centers favor these instruments for their ready-to-use design, consistent functionality, and compliance with strict regulatory standards.

The single-use segment is also projected to be the fastest-growing in 2026, fueled by regulatory support for disposable instruments and the increasing number of outpatient laparoscopic procedures. For example, Medtronic’s Endo Clip™ disposable appliers are gaining adoption in minimally invasive bariatric and urological surgeries, providing consistent ligation while reducing procedural downtime. The trend toward single-use devices is reinforced by the focus on patient safety, improved procedural efficiency, and lower sterilization costs. Emerging markets, particularly in the Asia Pacific region, are experiencing higher uptake as hospitals upgrade surgical infrastructure and strengthen hygiene standards.

Application Insights

In 2026, general surgery is expected to dominate the market, accounting for approximately 45% of revenue, due to its widespread use in high-volume procedures such as cholecystectomy, appendectomy, and hernia repair. The frequent need for general surgical interventions sustains strong demand for clip appliers, which are essential for reliable vessel ligation and tissue closure. For instance, B. Braun’s Aesculap Clip Appliers are commonly utilized in laparoscopic general surgeries, offering precise and secure ligation during minimally invasive procedures. Hospitals and outpatient centers prioritize these instruments for their efficiency and safety, supporting rapid adoption across both developed and emerging markets.

Bariatric surgery is projected to be the fastest-growing application in 2026, fueled by the rising prevalence of obesity and the increasing preference for laparoscopic techniques that reduce post-operative recovery times. Expansion of healthcare infrastructure in Asia Pacific, along with investments in minimally invasive bariatric programs in North America and Europe, is driving growth. Patient demand for less invasive procedures and quicker recovery is boosting surgical volumes, thereby increasing clip applier usage in this segment. For example, Medtronic’s Endo Clip™ disposable clip appliers are widely employed in laparoscopic bariatric procedures such as sleeve gastrectomy and gastric bypass, enabling precise vessel ligation and enhancing procedural safety.

Regional Insights

North America Laparoscopic Clip Appliers Market Trends

North America is expected to lead the market, capturing approximately 39% of the share in 2026, driven by the widespread adoption of minimally invasive and robotic-assisted surgeries, advanced healthcare infrastructure, and high procedural volumes in hospitals and outpatient centers. The increasing prevalence of chronic conditions such as gallbladder disease, gastrointestinal disorders, and obesity has boosted demand for laparoscopic interventions, which in turn drives higher usage of clip appliers. Healthcare providers in the region prioritize patient safety, operational efficiency, and infection control, contributing to the growing preference for single-use disposable clip appliers.

Technological innovation is a major trend shaping the North American market. Surgical instruments are increasingly integrated with robotic platforms to improve precision, ergonomics, and multi-fire capabilities. For instance, Ethicon’s Endo-Surgery™ disposable clip appliers are widely employed in laparoscopic general and bariatric procedures, offering reliable performance and sterility. Hospitals are also expanding infrastructure to support high-volume minimally invasive surgeries, particularly in bariatric and urological fields, creating opportunities for new product introductions. There is a rising emphasis on single-use, polymer-based clips, which minimize imaging interference and enhance patient safety.

Europe Laparoscopic Clip Appliers Market Trends

Europe is expected to be a key market for laparoscopic clip appliers in 2026, driven by the growing volume of minimally invasive surgeries, particularly in general, gynecological, and bariatric procedures. The focus on shorter hospital stays, reduced post-operative complications, and faster patient recovery has accelerated the adoption of laparoscopic clip appliers. Hospitals are increasingly investing in advanced surgical infrastructure and high-volume operating rooms, while surgeons prefer instruments that deliver precision, sterility, and efficiency during complex procedures. Compliance with the European CE marking system ensures device safety and builds clinical confidence, though it can affect approval timelines and market entry.

Technological innovation is a major trend in Europe. Robot-compatible and single-use clip appliers are gaining popularity to support minimally invasive and robotic-assisted surgeries. For example, B. Braun’s Aesculap™ disposable clip appliers are commonly used in laparoscopic cholecystectomy and bariatric procedures, offering reliable ligation and user-friendly handling. Manufacturers are also focusing on ergonomic designs, multi-fire functionality, and polymer-based clips to enhance both precision and patient safety. Combined with ongoing investments in healthcare infrastructure and rising patient awareness of minimally invasive options, these factors continue to drive growth, particularly in high-demand surgical areas such as bariatric and urological procedures.

Asia Pacific Laparoscopic Clip Appliers Market Trends

The Asia Pacific region is expected to be the fastest-growing market for laparoscopic clip appliers in 2026, driven by expanding healthcare infrastructure, rising surgical procedure volumes, and growing patient demand for minimally invasive surgeries. Countries such as China, Japan, India, and ASEAN nations are making significant investments in modern hospital facilities and surgical suites, supporting the adoption of advanced laparoscopic instruments. The increasing prevalence of conditions requiring laparoscopic intervention, including gallbladder disease, obesity-related disorders, and gynecological issues, is boosting demand for clip appliers across general, bariatric, and gynecological procedures.

Technological innovation is a key trend in the region. Manufacturers are introducing more precise, ergonomically designed, and single-use laparoscopic clip appliers tailored to local needs. For example, TEC?OLI’s automatic disposable clip applier, compatible with polymer and titanium ligating clips, is gaining popularity for its ease of use and secure deployment in minimally invasive surgeries. Companies are also focusing on features such as articulating jaws and multi-clip firing mechanisms to improve surgical precision, efficiency, and overall procedural safety.

Competitive Landscape

The global laparoscopic clip appliers market is moderately fragmented, characterized by the presence of several multinational medical device manufacturers alongside a growing number of specialized regional players. Market leadership is dominated by companies with comprehensive portfolios in minimally invasive surgical devices, extensive distribution networks, and robust clinical support systems. These established players benefit from long-standing relationships with hospitals, surgeon training programs, and integrated surgical ecosystems that combine clip appliers with complementary instruments such as staplers, energy devices, and visualization systems.

Key market leaders include Medtronic plc, Johnson & Johnson (Ethicon), B. Braun Melsungen AG, CONMED Corporation, and Teleflex Incorporated. Competition is driven by both the scale and depth of product offerings, with players focusing on continuous research and development, strategic partnerships, geographic expansion, and customized solutions for general, bariatric, urological, and gynecological surgeries. Companies also invest in regulatory approvals and localized manufacturing to improve market access and ensure compliance across different regions.

Key Industry Developments:

- In October 2024, LivsMed Launches the First 5mm Wristed Articulating Laparoscopic Instrument Line. LivsMed, a leader in minimally invasive surgical devices, has announced the release of ArtiSential 5, the first 5mm wristed articulating laparoscopic instrument line on the market. The new line builds on the company’s acclaimed ArtiSential™ series, offering enhanced flexibility, ergonomic handling, and precision comparable to robotic surgical platforms at a lower cost.

Companies Covered in Laparoscopic Clip Appliers Market

- Johnson & Johnson (Ethicon)

- Medtronic

- B. Braun Melsungen

- Conmed

- Teleflex

- Cooper Medical

- Genicon

- HOYA Corporation (Microline Surgical)

- Ackermann Instrumente

- Applied Medical

- Ovesco Endoscopy

- Surgical Innovations

- Unimax Medical Systems

- Mediflex Surgical Products

- Utah Medical Products (Femcare-Nikomed)

- Maxer Endoscopy

- Rudolf Medical

- Taiwan Surgical Corporation (TWSC)

- Zhejiang GeYi Medical

Frequently Asked Questions

The global laparoscopic clip appliers market is projected to reach US$1.4 billion in 2026.

The increasing adoption of minimally invasive surgeries is due to benefits such as reduced recovery time, lower complication rates, and rising surgical procedure volumes worldwide.

The laparoscopic clip appliers market is expected to grow at a CAGR of 9.5% from 2026 to 2033.

The growing integration of clip appliers with robotic-assisted surgery, the rising demand for single-use disposable instruments, and the expanding adoption of minimally invasive procedures in emerging healthcare markets.

Johnson & Johnson (Ethicon), Medtronic, B. Braun Melsungen, Conmed, and Teleflex are the leading players.