- Automotive Components & Materials

- KSA Tire Market

KSA Tire Market Size, Share, and Growth Forecast, 2025 - 2032

KSA Tire Market By Product Type (Pneumatic, Non-Pneumatic), Sales Channel (OEM, Aftermarket), Vehicle Type (Passenger Vehicles, Commercial Vehicles, Electric Vehicles, Off Highway Vehicles, Two & Three Wheelers), and Regional Analysis for 2025 - 2032

KSA Tire Market Size and Trends Analysis

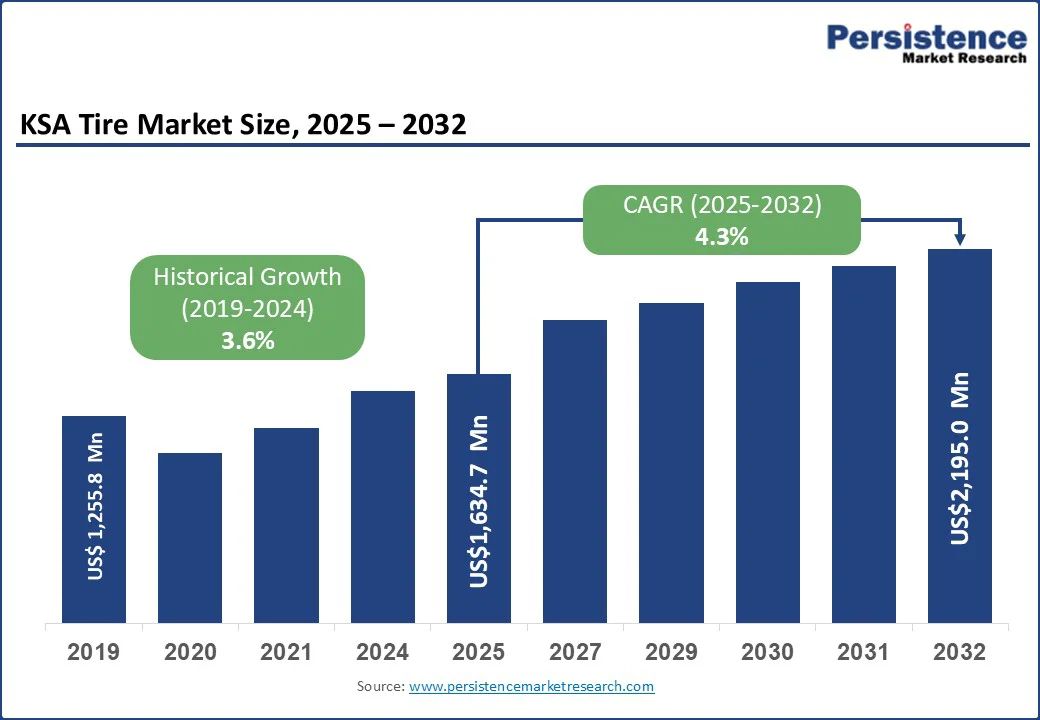

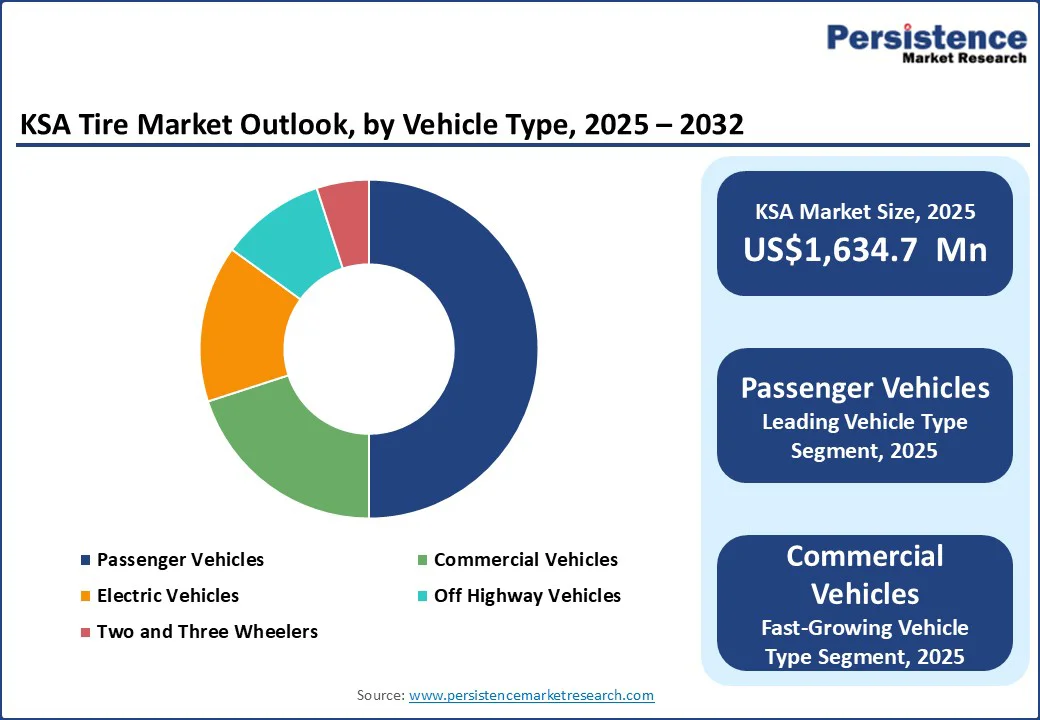

The ksa tire market size is likely to be valued at US$1,634.7 Mn in 2025 and is expected to reach US$2,195.0 Mn by 2032, growing at a CAGR of 4.3% during the forecast period from 2025 to 2032, driven by the rapid growth in vehicle ownership in Saudi Arabia. As vehicle ownership shifts from luxury to necessity, vehicle sales are rising rapidly, thereby increasing demand for a durable tire supply.

Key Industry Highlights:

- Leading Region: Northern & Central Region, accounting for over 35% of market revenue in 2025, supported by major cities such as Qassim and Hail. Rapid urbanization and industrialization in these areas have led to rising vehicle ownership across both personal and commercial segments, driving substantial demand for tires.

- Fastest-growing Region: The Eastern Region of Saudi Arabia holds a dominant position in the market, as it is the hub of the Kingdom’s oil and gas industry. This region, encompassing cities such as Dammam and Khobar, drives strong demand for commercial vehicle tires and off-the-road (OTR) tires used extensively in industrial, mining, and construction activities.

- Dominant Vehicle Type: Passenger vehicles are expected to gain significant traction in the market, driven by rising disposable incomes and economic growth. More people are purchasing personal vehicles, supported by government initiatives and affordable financing options, boosting the demand for passenger car tires.

- Sales Channel Insights: The OEM segment is expected to dominate, accounting for approximately 62% of the market share in 2025, driven by the consistent replacement cycle associated with new vehicles purchased from manufacturers or dealerships, where tires are included as part of the original vehicle setup.

- Import-Export Scenario: The market is predominantly import-driven due to limited domestic production, with Asian and European manufacturers meeting most of the demand to support the expanding vehicle fleet and replacement needs.

| Key Insights | Details |

|---|---|

| KSA Tire Market Size (2025E) | US$1,634.7 Mn |

| Market Value Forecast (2032F) | US$2,195.0 Mn |

| Projected Growth (CAGR 2025 to 2032) | 4.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Vehicle Ownership

The rapid growth in vehicle ownership is a major driver for the KSA tire market. In 2024, Saudi Arabia recorded over 1 million newly registered vehicles, a historic peak driven by rising disposable incomes, population growth, and the lifting of restrictions on driving, such as the repeal of the ban on women’s driving.

The surge includes passenger cars, SUVs, trucks, and commercial vehicles, all generating strong demand for original equipment tires and their eventual replacements. As vehicle use increases, tires experience more wear and need to be replaced regularly, sustaining the aftermarket demand.

Additionally, consumers are increasingly opting for premium and custom tires that offer better safety and performance, further fueling market expansion. This growth in vehicle ownership ensures a continuous, steady demand for a wide range of tires across different vehicle categories, supporting manufacturers and suppliers in expanding their product lines and market reach.

Economic Volatility and Oil Price Fluctuations

Economic volatility and oil price fluctuations act as significant restraints on the KSA tire market, as the country’s economy is heavily dependent on oil exports. As a large portion of government revenue and economic activity is tied to global oil prices, any sharp decline or instability in these prices can lead to economic downturns.

During such periods, consumer confidence and disposable incomes tend to decrease, leading to reduced spending on non-essential goods, including tires. This directly impacts tire sales, as vehicle owners may postpone tire replacements or new purchases due to financial uncertainty.

Moreover, economic volatility can affect industrial investment and infrastructure projects that drive demand for commercial and off-the-road tires. The cyclical nature of oil prices means the tire market must adapt to periods of both growth and contraction. Tire companies need robust strategies to manage this volatility, such as diversifying product lines or focusing on more cost-effective solutions that appeal during downturns. These economic sensitivities make the tire market susceptible to fluctuations tied to oil price dynamics.

Expanding Transportation and Logistics Sectors

Saudi Arabia’s substantial investments in infrastructure development and logistics expansion under Vision 2030 create a robust demand for commercial vehicle tires. The logistics market was valued at US$52.7 Bn in 2024, driven by e-commerce growth and industrial activities requiring efficient freight transport. The daily use of trucks, vans, and heavy-duty vehicles in long-distance and heavy-load operations escalates tire wear, prompting frequent replacements.

Infrastructure mega-projects such as NEOM and the Red Sea Project necessitate commercial and off-the-road (OTR) tires that are durable and high-performance. Fleet operators prioritize tire maintenance for safety and operational efficiency, fueling aftermarket demand.

Moreover, expanding construction activities, along with the increasing use of commercial vehicles, bolster tire sales. This sector’s growth ensures continuous demand for specialized tires, presenting lucrative opportunities for manufacturers and suppliers to cater to logistics and construction vehicle fleets in Saudi Arabia.

Category-wise Analysis

Vehicle Type Insights

Passenger vehicles are expected to gain significant traction in the market during the forecast period due to several factors. The increasing vehicle fleet size, driven by rising disposable incomes and economic growth, is a key driver.

More people are purchasing personal vehicles, supported by government initiatives and affordable financing options, which boosts demand for passenger car tires. Additionally, consumers are increasingly opting for premium and customized tires that offer better performance, safety, and aesthetics.

Moreover, as Saudi Arabia lacks a luxury tax or VAT on vehicles, it is among the most affordable markets, offering lucrative opportunities for automakers and tire manufacturers to introduce new models and variants. Accordingly, the country represents a large market for passenger cars and tires, offering profitable growth prospects through 2032.

Sales Channel Insights

The OEM segment is expected to dominate, accounting for approximately 62% of the market share in 2025. This dominance is driven by the consistent replacement cycle associated with new vehicles purchased from manufacturers or dealerships, where tires are included as part of the original vehicle setup. OEM tire sales benefit from bulk procurement by car manufacturers, ensuring steady demand and competitive pricing advantages.

In contrast, the aftermarket segment, which includes tire replacements when existing tires wear out, exhibits more intermittent demand as replacements are not synchronized across vehicles. Consumers replace tires based on wear and usage, leading to irregular purchase patterns. Despite this, the aftermarket remains important for replacement tires but is currently less dominant compared to OEM in terms of market share.

Regional Insights

Northern and Central KSA Tire Market Trends

The Northern and Central regions of Saudi Arabia, particularly Riyadh, serve as the country’s economic hub, supported by major cities such as Qassim and Hail. Rapid urbanization and industrialization in these areas have led to rising vehicle ownership across both personal and commercial segments, driving substantial demand for tires. Higher disposable incomes and thriving business activity further stimulate vehicle purchases, directly supporting tire market growth.

Additionally, the Saudi Government’s Vision 2030 strategy is a key enabler, focusing on economic diversification and extensive infrastructure development. Major initiatives such as the Riyadh Metro, King Salman Energy Park, and large-scale road expansion projects are creating strong demand for commercial vehicles, including trucks, buses, and construction machinery. These activities, alongside continuous construction and industrial projects, significantly increase the need for heavy-duty tires, reinforcing the region’s pivotal role in the market.

Eastern KSA Tire Market Trends

The Eastern region of Saudi Arabia holds a dominant position in the market, as it is the hub of the Kingdom’s oil and gas industry. This region, encompassing cities such as Dammam and Khobar, drives strong demand for commercial vehicle tires and off-the-road (OTR) tires used extensively in industrial, mining, and construction activities. The presence of major oil refineries, petrochemical plants, and logistics ports fuels the need for durable tires capable of withstanding harsh and demanding environments.

Additionally, the Eastern province benefits from significant port activities, serving as a critical logistics and transportation gateway, which further boosts demand for tires required in freight and commercial vehicles. The high volume of heavy-duty vehicle usage results in frequent tire replacements. Government investments in infrastructure and expanding industrial projects in this region continue to stimulate market growth.

Competitive Landscape

The KSA tire market features a wide range of products catering to passenger cars, commercial vehicles, and off-the-road applications, addressing both performance and durability. With the rapidly growing vehicle fleet, fueled by rising incomes and urbanization, demand for high-quality tires is increasing steadily. The market includes radial, bias, and specialty tires that meet the diverse needs of private owners and fleet operators.

Innovation, distribution networks, and after-sales services are key competitive factors, as consumers prioritize safety, longevity, and cost-efficiency. Companies must remain agile and responsive to evolving trends such as fuel efficiency and sustainable tire technologies to capture market share.

Global players such as Bridgestone, Michelin, and Goodyear, alongside regional brands such as Al Dobowi and Al-Qahtani, dominate the landscape by offering a wide portfolio, strong distribution, and localized strategies to serve the dynamic KSA market.

Key Industry Developments

- In April 2025, Hankook Tire & Technology, a prominent tire manufacturer, introduced the ultra-high-performance tire, 'Ventus evo', in Saudi Arabia. The 'Ventus evo' represented the fourth generation of tires, created as the next iteration of the 'Ventus S1 evo 3,' providing notably better braking and cornering performance, along with superior fuel efficiency and mileage in comparison to the earlier model.

- In February 2025, The Goodyear Tire & Rubber Company introduced its advanced ‘Tire Pressure Monitoring System (TPMS)’ in Saudi Arabia. This innovative solution combined digital technology with Goodyear's tire knowledge to provide enhanced fleet management features for logistics and mass transit providers in one of the globe’s toughest environments.

Companies Covered in KSA Tire Market

- The Bridgestone Group

- Michelin Group

- Goodyear Tire and Rubber Company

- Pirelli & C S.p.A.

- Continental AG

- Hankook Tire Company

- Cooper Tire & Rubber Company

- Yokohama Rubber Company Ltd.

- Toyo Tire & Rubber Company Ltd.

- Apollo Tyres Ltd.

Frequently Asked Questions

The KSA tire market is estimated to be valued at US$1,634.7 Mn in 2025.

The key demand driver for the KSA tire market is the growing automotive fleet, supported by rising vehicle ownership, rapid urbanization, and expanding infrastructure projects.

In 2025, the Northern & Central region will dominate the market with an exceeding 35% revenue share in the KSA tire market.

Among the vehicle types, the smart helmets segment is expected to hold the largest share, capturing more than 60% of the market revenue share by 2025.

The key players in the KSA tire market are The Bridgestone Group, Michelin Group, Goodyear Tire and Rubber Company, Pirelli & C S.p.A., and Continental AG.