- Biotechnology

- Kinase Biology Tools and Services Market

Kinase Biology Tools and Services Market Size, Share, and Growth Forecast, 2026 - 2033

Kinase Biology Tools and Services Market by Component (Products, Services), Test Type (ELISA-Based Tests, Enzymatic Tests, Colorimetric Assay-Based Tests, Others), Application (Diagnosis, Research), End-User (Academic Research Institutes, Pharmaceutical & Biotechnology Companies, CROs), and Regional Forecast for 2026 - 2033

Kinase Biology Tools and Services Market Share and Trends Analysis

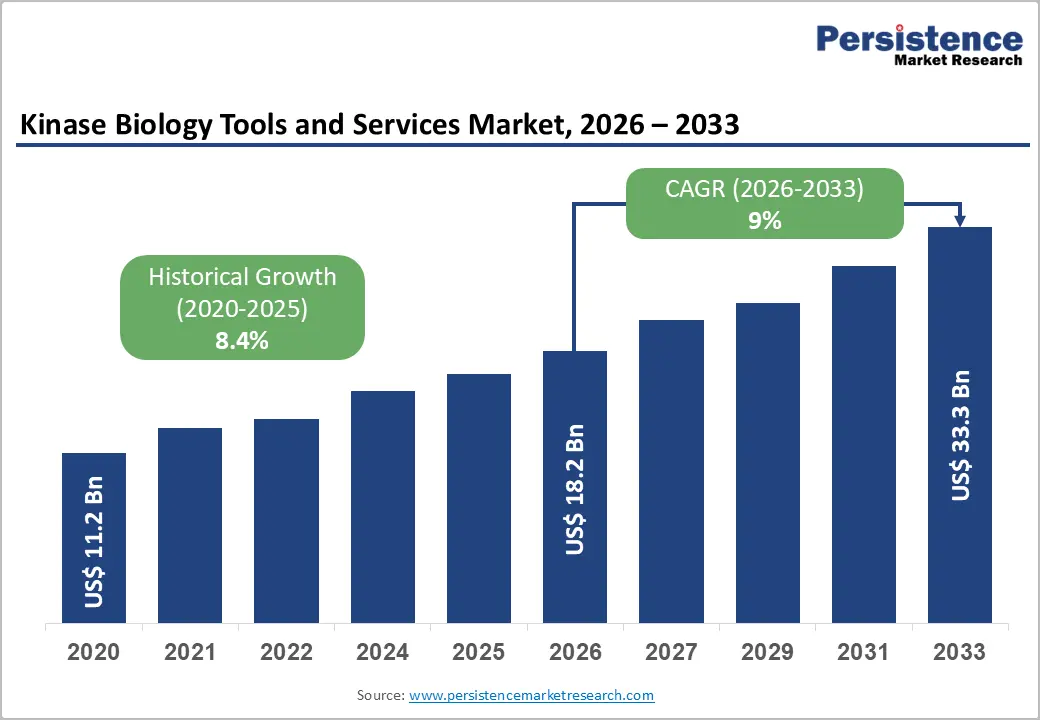

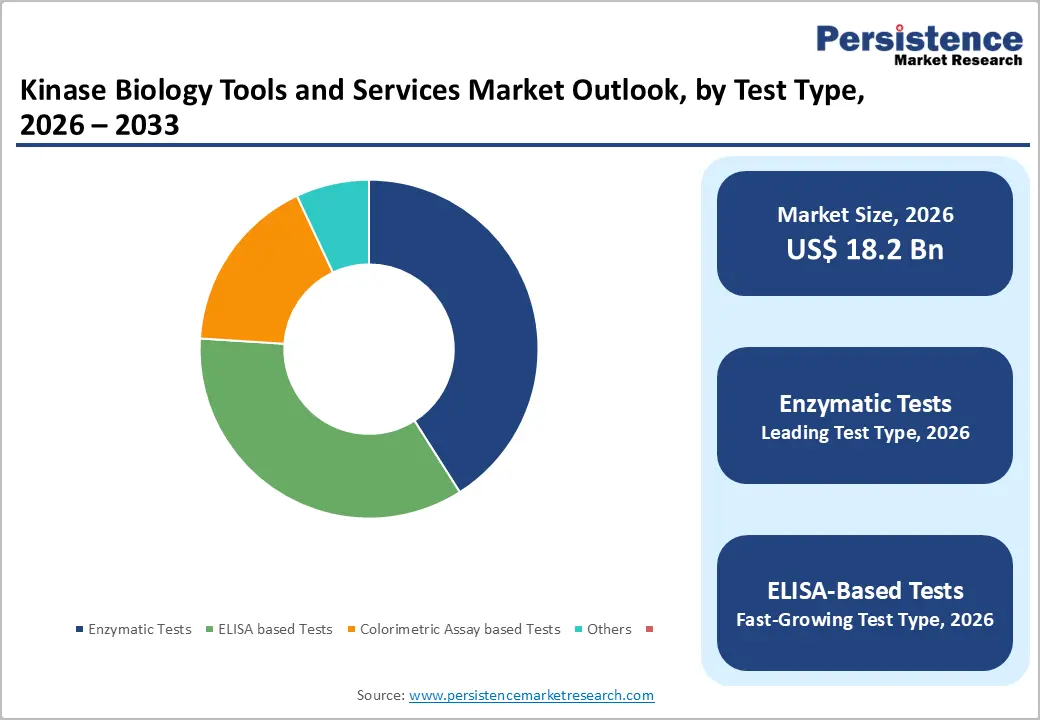

The global kinase biology tools and services market size is likely to be valued at US$ 18.2 billion in 2026, and is projected to reach US$ 33.3 billion by 2033, growing at a CAGR of 9% during the forecast period 2026 - 2033.

Pharmaceutical companies have integrated kinase-targeted drug discovery into their core research and development workflows. Investment priorities have been shifting toward oncology and immunology as organizations seek therapies with greater clinical relevance. High-throughput screening platforms have been gaining adoption across discovery pipelines as teams have been accelerating target validation and lead optimization. Regulatory authorities have been actively supporting precision medicine frameworks to improve treatment specificity and patient outcomes. At the same time, firms have been outsourcing specialized activities to contract research organizations (CROs) to improve operational flexibility. Together, these structural shifts have been creating a stable foundation for sustained expansion across this segment. Research pipelines have been aligning more closely with targeted therapeutic approaches to shorten translation timelines. Collaborative engagement with CRO partners has lowered execution risk while supporting faster innovation cycles. Precision-driven development models will have strengthened differentiation as competition intensifies, further aiding the market.

Key Industry Highlights

- Dominant Application: Research use is expected to dominate with 68% market share in 2026, while diagnosis use is projected to grow fastest at 10.1% CAGR, driven by expanding precision oncology.

- Leading Product Component: Reagents and kits are projected to dominate with about 48% share in 2026 due to high-volume consumption, while instruments are expected to be the fastest-growing at a 10.2% CAGR as automation penetration increases.

- Dominant Service Component: Data interpretation and analysis services are estimated to account for 36% of service revenues in 2026, reflecting assay complexity.

- Test Type Dynamics: Enzymatic tests are expected to lead with a 41% share in 2026, owing to their broad applicability in kinase profiling, while ELISA-based tests are forecast to grow fastest at a 9.9% CAGR due to their reproducibility and diagnostic relevance.

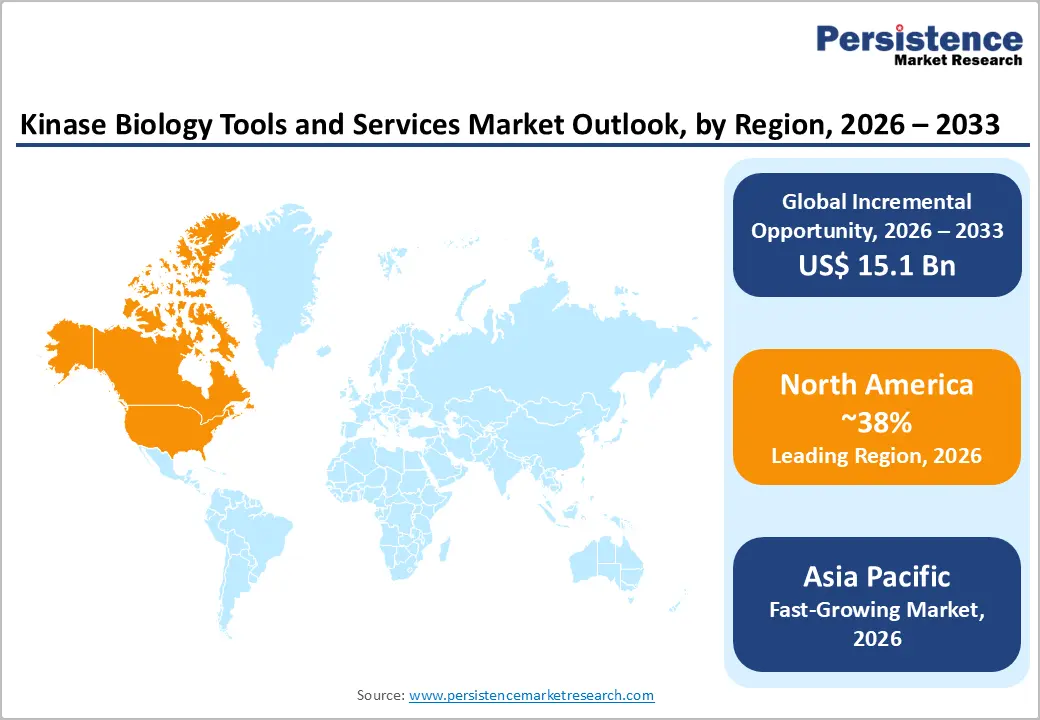

- Regional Leadership: North America is set to dominate with around 38% market share in 2026, while the Asia Pacific market is projected to expand fastest at a 10.6% CAGR through 2033, led by China and India.

- Competitive Differentiation: Competitive advantage increasingly hinges on AI-driven kinase analytics and cloud integration, which improve screening efficiency and drive higher client retention across the pharma and CRO segments.

| Key Insights | Details |

|---|---|

| Kinase Biology Tools and Services Market Size (2026E) | US$ 18.2 Bn |

| Market Value Forecast (2033F) | US$ 33.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Sustained R&D Funding and Technological Progress Accelerating Kinase Research Adoption

Global pharmaceutical R&D expenditure exceeded US$ 245 billion in 2023, with oncology accounting for over 40% of late-stage development pipelines, underscoring the central role of kinase biology in targeted therapeutics. Kinases represent more than 30% of validated drug targets across oncology and inflammatory disorders, reinforcing their clinical and commercial relevance. This sustained focus drives continuous demand for kinase assay kits, enzymatic tests, and analytical services across discovery and translational research. The impact remains strongest in early-stage development, where screening accuracy directly affects downstream success rates. As precision medicine adoption expands, kinase-focused research continues to gain structural importance. This trend supports long-term utilization of both tools and services.

Public research funding further strengthens this demand environment, with the National Institutes of Health (NIH) budget reaching approximately US$ 47.35 billion in FY 2024, reflecting an increase of more than US$ 17 billion since FY 2015 in nominal terms. Despite inflationary adjustments, sustained funding levels ensure continuity in kinase signaling research across cancer, neurological, and metabolic disease programs. In parallel, advances in automation enhance research productivity, as automated kinase assays reduce screening time by up to 45% compared to conventional methods. These efficiency gains improve throughput and reproducibility across laboratory settings. Thus, the funding stability and workflow optimization accelerate adoption across pharmaceutical and outsourced research environments.

High Capital Intensity and Regulatory Complexity Constraining Market Accessibility

Sophisticated kinase profiling instruments and integrated data analytics platforms require capital investments exceeding US$ 250,000 per installation, creating a significant entry barrier for small and mid-sized laboratories. Cost sensitivity remains particularly acute in emerging economies, where institutional research budgets are limited and procurement cycles are prolonged. These financial constraints restrict adoption primarily to Tier-1 academic centers, large pharmaceutical companies, and well-funded CROs. As a result, broader market penetration of advanced kinase tools remains uneven across regions. Limited access also slows the diffusion of technology into early-stage and exploratory research environments. This cost structure narrows the immediate addressable customer base.

Regulatory requirements further intensify these constraints, as stringent assay-validation standards lengthen development timelines and increase compliance costs for new kinase platforms. Reproducibility challenges inherent to biological assays elevate operational risk, especially for outsourced and multi-site research workflows. Inconsistent results can necessitate repeated validation, increasing time and resource consumption. These factors collectively reduce development efficiency and delay the commercialization of innovative tools. For service providers and CROs, compliance obligations add complexity to client delivery models. Together, high capital demands and regulatory rigor act as structural restraints on market scalability.

Expanding Outsourcing Models and Advanced Analytics: Unlocking New Growth Avenues

The market is likely to continue its upward trajectory as pharmaceutical companies increasingly outsource kinase screening and data analytics to control costs and accelerate research timelines. This trend is particularly strong in Asia Pacific and Eastern Europe, where skilled talent and infrastructure support rapid service expansion. Outsourcing allows access to specialized kinase expertise without heavy capital investment, enabling faster project execution and improved resource efficiency. Strategic collaborations and service extensions further reinforce market scalability and long-term adoption of service-based kinase solutions.

Advanced analytics and AI integration are reshaping the value proposition of outsourced research. For example, Eli Lilly launched its AI-enabled TuneLab platform, allowing biotech partners to leverage proprietary AI models to accelerate high-throughput drug discovery workflows, including kinase-targeted assays. Cloud-based platforms and AI-driven data interpretation improve screening accuracy, throughput, and predictive modeling, enhancing decision-making across distributed research teams. This outsourcing momentum and digital convergence create durable, high-margin growth opportunities across tools and services, positioning providers to capture incremental value beyond consumables.

Category-wise Analysis

Component Insights

Products are expected to dominate the component segment, accounting for an estimated 58% of the kinase biology tools and services market revenue in 2026, led by reagents and kits. Reagents and kits enable reproducible kinase assays, while instruments and consumables support high-throughput profiling in drug discovery. Government initiatives like India’s DBT-BIRAC grants and Singapore’s Biopolis infrastructure provide funding for platform adoption. Platforms are crucial for maintaining data control and reproducibility in pharmaceutical pipelines. Academic research centers also benefit from these programs, supporting early-stage discovery. Sustained platform demand reflects their central role across preclinical and translational research.

Services are projected to be the fastest-growing segment, likely to expand at around 10.2% CAGR through 2033, driven by outsourcing and demand for specialized expertise. Service types include data management & storage, cloud-based computing, and data interpretation & analysis, enabling scalable research without a heavy upfront investment. Cloud platforms enable secure, collaborative analytics across global teams. National bioinformatics initiatives in Japan and Singapore reinforce adoption. The other categories, including workflow consulting, support complex research projects. Services offer flexibility, rapid deployment, and cost efficiency, making them increasingly attractive to mid-tier biotech and academic labs.

Test Type Insights

Enzymatic tests are projected to lead, capturing around 41% of the kinase biology tools and services market share in 2026, driven by their role in kinase profiling, inhibitor screening, and target validation. They provide reproducible quantitative data and integrate well with high-throughput platforms. Government programs such as Japan’s AMED grants subsidize assay kits and instrument access. Academic and translational research centers benefit from these programs, thereby supporting widespread adoption of enzymatic tests. Enzymatic assays are essential for early-stage discovery pipelines. Their reliability ensures they remain the preferred test type globally.

ELISA-based tests are anticipated to be the fastest-growing, projected at 9.9% CAGR through 2033, driven by clinical and research demand for high-specificity assays. ELISA is increasingly used in biomarker validation and patient stratification, aligning with precision medicine. Funding from China’s NSFC, Japan’s AMED, and Korea’s NRF supports the adoption of immunoassays. Hospitals and clinical labs upgrading diagnostic infrastructure accelerate growth. Colorimetric and multiplex assays grow more slowly, while ELISA continues expanding rapidly. Government-backed programs and rising clinical utility reinforce adoption across regions.

Application Insights

Research use is likely to dominate, accounting for roughly 68% of revenue in 2026, as kinase tools are primarily used in discovery, preclinical studies, and mechanistic research. Tools and assays support oncology, metabolic disease, and immunology pipelines. Funding programs such as the NIH Common Fund and the European Union (EU)’s Horizon initiatives enhance research infrastructure and access. Academic labs and translational centers leverage these grants to adopt high-throughput and multiplex platforms. Research use continues to drive overall market demand, ensuring stable consumption of tools and services.

Diagnosis use is slated to be the fastest-growing segment, with a 10.1% CAGR through 2033, fueled by kinase-based biomarkers for precision medicine and patient stratification. Companion diagnostics, clinical biomarker assays, and molecular testing are driving uptake. National healthcare policies in Singapore and South Korea incentivize the adoption of diagnostic assays. Clinical laboratories upgrading infrastructure benefit from funding programs that improve assay throughput. Technological advances in automation enhance reproducibility and efficiency. Diagnosis use adoption is expanding, complementing research-driven growth.

End-User Insights

Pharmaceutical and biotechnology companies are expected to dominate end-user demand, with an estimated 47% share in 2026, driven by extensive use of kinase tools for drug discovery, preclinical profiling, and candidate optimization. Companies such as AbbVie and Novartis partner with specialized CROs, including Parexel and Syneos Health, to enhance R&D efficiency and expand assay capabilities. Outsourcing kinase studies allows access to advanced analytics while reducing internal infrastructure needs. This demand is sustained by growing pipelines for biologics and targeted therapies. Government programs in Europe and North America support translational research infrastructure. Strategic collaborations enable integrated workflows across complex kinase targets. These factors ensure that pharma/biotech remains the primary revenue contributor.

Contract research organizations are likely to be the fastest-growing end users, projected at 11.3% CAGR through 2033, as outsourcing continues to expand globally. CROs offer high-throughput kinase profiling, cloud-based analytics, and data interpretation services that complement internal R&D. Around 45% of pharma R&D is outsourced to CROs, reflecting growing reliance on external expertise for complex biological studies. National initiatives such as Singapore’s RIE Biomedical Sciences strategy fund digital infrastructure and advanced analytics, supporting CRO expansion. CROs also provide flexible services for emerging biotech firms. Their growth is fueled by demand for scalable, cost-efficient solutions across discovery and translational workflows. Partnerships with biotech clients enable rapid adoption of novel assay platforms.

Regional Insights

North America Kinase Biology Tools and Services Market Trends

North America is expected to hold the largest share of the kinase biology market at about 38% in 2026, led by the United States. Leading biotech companies in the Boston/Cambridge area, including Schrödinger, Inc., Benchling, Alterome Therapeutics, and Kymera Therapeutics, drive the demand for high-throughput kinase assays, reagents, and analytical platforms. AI-enabled discovery tools and cloud-based data management support kinase target identification and profiling.

Federal initiatives such as the Cancer Moonshot program fund molecular research infrastructure and translational projects. Advanced biotechnology hubs in San Francisco and the Research Triangle enhance the adoption of instruments and reagents. These companies and programs ensure North America remains the dominant global market. Strategic collaborations reinforce integrated research and innovation.

The region also sees rapid growth in cloud-based and outsourced services through 2033, driven by pharma reliance on CROs and data analytics providers. Platforms such as Benchling support collaborative data interpretation, while high-performance computing tools accelerate kinase research. Venture capital continues to fund digital biology startups and precision oncology initiatives in 2025-2026. Outsourced analytics and AI-driven data integration improve efficiency in clinical and preclinical workflows. Government-backed research grants further support infrastructure expansion. These developments position North America as both the market leader and innovation hub in kinase biology globally.

Europe Kinase Biology Tools and Services Market Trends

Europe remains a key player in the market for kinase biology tools and services, supported by major research hubs in Germany, the U.K., and France. The European Medicines Agency (EMA) ensures harmonized regulatory standards and mutual recognition of assay validation. Funding programs such as Germany’s High-Tech Strategy 2025 and the U.K.’s Biomedical Catalyst Fund support both fundamental research and applied biotech. Academia-industry collaborations, including partnerships between Evotec SE and MedImmune (AstraZeneca), enhance discovery workflows. These initiatives promote procurement of kinase profiling tools, high-throughput platforms, and CRO services. European research centers continue to expand translational capacity. Collectively, these factors strengthen Europe’s influence in global kinase research.

Central and Eastern Europe is emerging as a growth hub, with expanding biotech clusters and cost-efficient CRO services attracting international projects. Poland and Czechia are implementing digital research programs that enable cloud-based analytics and the integration of high-throughput assays. Horizon Europe funding prioritizes translational research, increasing uptake of kinase assays and multi-omics platforms. Local biotech manufacturing is modernizing to meet sustainability standards, supporting instruments and consumables production.

Partnerships between CROs and pharmaceutical firms accelerate advanced tool adoption. Government-backed grants further enhance research infrastructure. These developments position Europe as both a stable market and an emerging innovation center in kinase biology.

Asia Pacific Kinase Biology Tools and Services Market Trends

Asia Pacific is the fastest-growing regional market for kinase biology tools and services, forecasted to expand at approximately 10.6% CAGR through 2033, led by China, Japan, and India. China’s biotechnology development plans for 2025-2030 emphasize domestic capability building in molecular assay platforms and diagnostics, significantly boosting demand for kinase biology tools. Policy support through programs such as the National Major Science and Technology Projects enhances funding for research infrastructure and translational platforms.

India’s rapidly expanding CRO ecosystem benefits from government-backed initiatives that build life sciences parks and strengthen biotech education pipelines. Japan continues to innovate in high-precision instruments and automation technologies for kinase profiling. These dynamics contribute to the Asia Pacific’s fast-growing status within the global landscape.

Strategic industry movements further reinforce regional expansion, with Asia Pacific stakeholders focusing on both local production and global partnerships. In 2025 and 2026, several major Asian research consortia received government backing to establish large-scale bioinformatics platforms that support cloud computing and big data analytics for kinase research. National digital transformation strategies, such as China’s Bioindustry Innovation Plan, elevate computing infrastructure to support data-intensive biology workflows.

Southeast Asian nations are also enhancing regulatory frameworks to attract foreign biotech investment and CRO engagements. These developments, combined with cost advantages and a strong talent base, make Asia Pacific an increasingly influential player in the global market.

Competitive Landscape

The global kinase biology tools and services market structure is moderately consolidated, with top players such as Thermo Fisher Scientific, Merck KGaA, PerkinElmer, and Agilent Technologies collectively controlling a significant portion of revenue. These established companies leverage extensive pharmaceutical and academic relationships, advanced assay platforms, and integrated instrument-reagent solutions. They also invest heavily in R&D to maintain leadership in high-throughput screening, multiplex kinase profiling, AI-driven data analytics, and cloud-enabled research services.

Regional and niche competitors, including Sartorius, Tecan Group, and Bio-Rad Laboratories, focus on specialized assay platforms, enzymatic and ELISA-based tests, and localized markets. Barriers such as stringent regulatory requirements, reproducibility challenges, and high capital costs limit new entrants. However, digitalization and cloud-based analytics platforms are enabling software-centric and service-focused companies to participate. Market consolidation is expected to gradually increase through strategic acquisitions, while collaboration between platform providers and service firms continues to drive innovation and expand global reach.

Key Industry Developments

- In January 2026, Seattle-based biotech Variant Bio launched ‘Inference’, described as the world’s first agentic genomic drug discovery platform, using autonomous AI agents to perform complex biological analyses and integrate genomic, transcriptomic, proteomic, and metabolomic data. The platform’s launch coincided with a multi-year collaboration with Boehringer Ingelheim worth over US$ 120 million to discover novel targets for kidney and cardiorenal diseases.

- In November 2025, researchers at Cornell University developed ProKAS (Proteomic Kinase Activity Sensors), a mass spectrometry-based technology that uses peptide “barcodes” to map kinase activity with high spatial and temporal resolution within living cells. ProKAS enables simultaneous multiplex monitoring of key kinase activities such as ATR, ATM, and CHK1 and is scalable for high-throughput applications, offering a powerful new tool for drug discovery and kinase signaling research.

- In June 2025, Caris Life Sciences completed its IPO, raising approximately $494.1 million to expand its AI-driven molecular profiling platforms that analyze genomic data to guide cancer treatment. The funding supports commercial growth of its precision oncology diagnostic products and reinforces the value placed on AI and data analytics within molecular profiling capabilities that intersect with kinase signaling assays and diagnostic workflows.

Companies Covered in Kinase Biology Tools and Services Market

- Thermo Fisher Scientific

- Merck KGaA

- Danaher Corporation

- Agilent Technologies

- PerkinElmer

- Bio-Rad Laboratories

- Abcam

- Promega Corporation

- Cell Signaling Technology

- Eurofins Scientific

- Charles River Laboratories

- Becton, Dickinson and Company

- Enzo Life Sciences

Frequently Asked Questions

The global kinase biology tools and services market is projected to reach US$ 18.2 billion in 2026.

Rising investments in kinase-targeted drug discovery, the expansion of government-funded life sciences research, and technological advancements in high-throughput and automated kinase assay platforms are the primary drivers.

The market is poised to witness a CAGR of 9% from 2026 to 2033.

Emerging outsourcing models, increased utilization of CRO services, AI integration, cloud-based analytics, and growing precision medicine initiatives offer substantial growth potential.

Thermo Fisher Scientific, Merck KGaA, PerkinElmer, Agilent Technologies, and Bio-Rad Laboratories are some of the leading players shaping the market.