- Pharmaceuticals

- Immuno-Oncology Market

Immuno-Oncology Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Immuno-Oncology Market by Treatment Type (Immune Checkpoint Inhibitors, CAR-T Cell Therapy, Cancer Vaccines, Others), End-user (Hospitals, Others), Disease Type (Lung Cancer, Breast Cancer, Others), Assay (PCR, Others), and Regional Analysis for 2025 - 2032

Immuno-Oncology Market Share and Trends Analysis

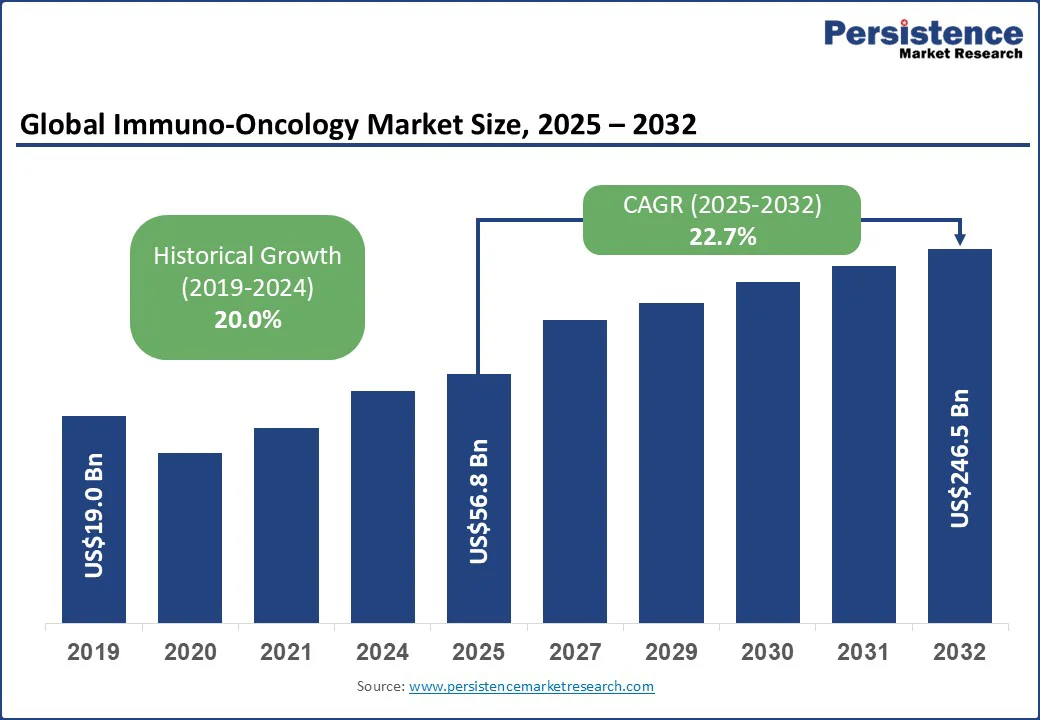

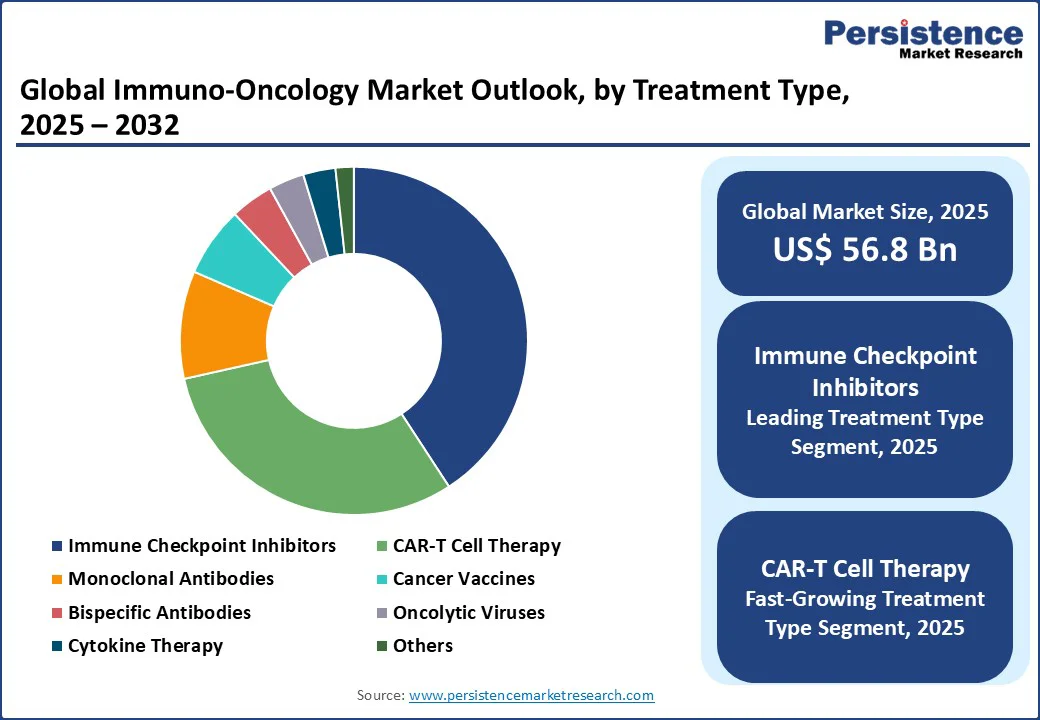

The global immuno-oncology market size is likely to be valued at US$56.8 Bn in 2025 and is expected to reach US$246.5 Bn by 2032, growing at a CAGR of 22.7% during the forecast period from 2025 to 2032. The approval of novel drugs targeting PD-1/PD-L1 pathways and the expanding usage of combination therapies for treating cancer are fueling the market.

Immuno-oncology, a groundbreaking subset of cancer treatment, harnesses the body's immune system to identify, target, and eliminate cancer cells with precision. Unlike traditional therapies such as chemotherapy and radiation, which harm healthy cells, immuno-oncology empowers the immune system to selectively attack tumors, thereby reducing collateral damage to other healthy cells and improving patient outcomes.

Stimulated by advancements in immune checkpoint inhibitors, CAR-T cell therapies, and personalized cancer vaccines, the immune-oncology market growth is poised to gather unprecedented momentum. The central factor brightening the market outlook is the rising incidence of cancer worldwide, complemented by the increasing adoption of immunotherapies in standard treatment protocols. The integration of biomarker-driven precision medicine and the surge in clinical trials are unlocking the immense growth potential of the market.

Key Industry Highlights

- Leading Disease Type: The lung cancer segment is slated to dominate in 2025, with a revenue share of approximately 20.7%, fueled by a high prevalence of the disease and early diagnoses via screening programs.

- Fastest-growing Disease Type: Prostate cancer is expected to display a high CAGR of approximately 22.6% in 2025, on account of an increasing number of elderly individuals worldwide.

- Dominant Treatment: Immune checkpoint inhibitors are set to lead here with around 40.8% market share in 2025, reflecting their revolutionary role in cancer therapy by activating the immune system to target tumors.

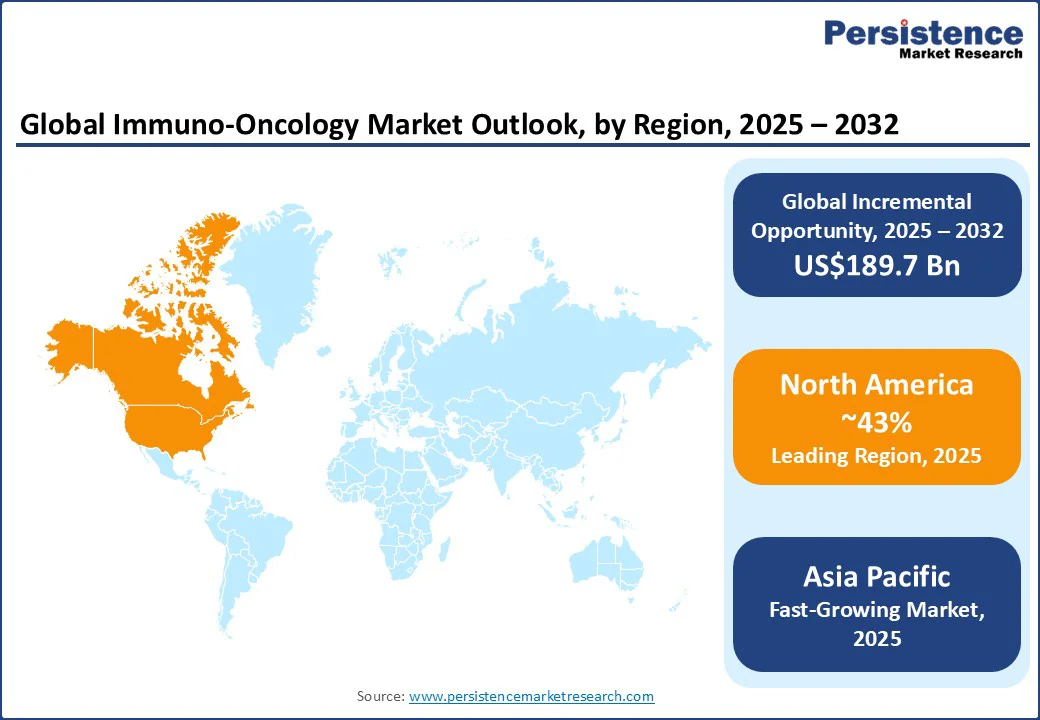

- Dominant Region: North America is expected to hold a commanding immune-oncology market share of about 43.2%, due to its widespread cancer burden and a strong biotech and pharmaceutical R&D ecosystem.

- The fastest-growing regional market is likely to be Asia Pacific, forecasted to exhibit a CAGR exceeding 12.0% through 2032, driven by rising cancer incidence, expanding healthcare access, and regulatory facilitation.

|

Global Market Attribute |

Key Insights |

|

Immuno-Oncology Market Size (2025E) |

US$56.8 Bn |

|

Market Value Forecast (2032F) |

US$246.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

22.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

20.0% |

Market Dynamics

Driver - Growing Global Cancer Burden to Accelerate Immuno-Oncology Market Expansion

The persistent and alarming rise in cancer incidence worldwide, which is intensifying the demand for more effective, personalized cancer therapies, is the primary growth stimulant for the immune-oncology market. Latest data from the International Agency for Research on Cancer (IARC) reveals that in 2022, there were an estimated 20 million new cancer cases globally, and cancer deaths amounted to nearly 9.7 million.

According to recent data from the American Cancer Society, the U.S. alone is expected to witness nearly 1.9 million new cancer diagnoses annually. The World Health Organization (WHO) also states that about 30% of people in low- and middle-income countries suffer from cancer-causing infections such as hepatitis. These dramatic figures are compelling healthcare systems to adopt cutting-edge immuno-oncology solutions such as CAR-T cell therapies and novel cancer vaccines. This escalating cancer prevalence acts as a powerful catalyst, attracting investments in pharmaceutical R&D aimed at innovating next-generation immunotherapies with enhanced efficacy and safety profiles. The integration of predictive biomarkers and companion diagnostics has enabled precision medicine approaches that optimize treatment response and reduce adverse effects, benefiting the market.

Restraint - Escalating Treatment Costs to Impede Larger Adoption of Immuno-Oncology Therapies

The principal impediment stifling the full potential of the immuno-oncology market is the prohibitively high costs associated with immunotherapy treatments, which will severely limit their access and uptake, especially in emerging economies. Leading immuno-oncology agents such as pembrolizumab and nivolumab frequently carry price tags exceeding US$12,500 to US$15,000 per month, resulting in multi-year treatment costs that surpass typical cancer drug regimens manifold, as documented by the American Society of Clinical Oncology in 2021. This economic burden constrains payer reimbursement capabilities and compels healthcare systems to grapple with cost-effectiveness assessments amid growing oncology care demand.

Moreover, the complexity and elevated costs of personalized therapies, such as CAR-T cell treatments, which involve sophisticated manufacturing and specialized administration, further exacerbate affordability challenges. Coupled with limited infrastructure for precision diagnostics and biomarker testing in low- and middle-income countries, these factors are collectively restricting the widespread clinical adoption of immuno-oncology therapeutics and may even deter investments toward the development of innovative therapies.

Opportunity - Breakthrough Advances in Precision Medicine to Unleash Market Potential

As the immuno-oncology market rapidly evolves, key players can capitalize on emerging opportunities by integrating precision medicine technologies, enabling highly personalized cancer treatments that enhance therapeutic efficacy and patient outcomes. This opportunity is magnified by breakthroughs in biomarker detection assays, next-generation sequencing, and AI-driven analytics, which collectively facilitate more accurate patient selection and adaptive immunotherapy regimens. These advances are also garnering support from regulatory authorities. For instance, in December 2024, the FDA granted accelerated approval to BIZENGRI® (zenocutuzumab-zbco) for treating NRG1 fusion-positive pancreatic adenocarcinoma, marking the first targeted systemic therapy for this mutation in both pancreatic and non-small cell lung cancers.

In clinical studies, 40% of treated patients saw tumor shrinkage, and many responders experienced effects lasting at least six months. Pharmaceutical companies are also deeply engaged in innovating next-generation checkpoint inhibitors and combination therapies tailored to tumor molecular profiles, fueling a transition from one-size-fits-all to precision oncology.

Category-wise Analysis

Treatment Type Insights

In the treatment category, the leading segment in 2025 is likely to be immune checkpoint inhibitors, expected to command approximately 41% of the market revenue share. This dominance is driven by the unrivalled ability of checkpoint inhibitors to reactivate T-cells by blocking proteins such as PD-1, PD-L1, and CTLA-4, which cancer cells use to evade immune detection. Drugs such as pembrolizumab (Keytruda) and nivolumab (Opdivo) have transformed treatment paradigms, showing durable clinical responses in cancers such as melanoma, lung cancer, and kidney cancer. Breakthrough regulatory approvals, expanded biomarker testing, and growing adoption in frontline therapies are key drivers expanding the scope of this segment.

Meanwhile, the fastest-growing segment through 2025-2032 within treatment types is anticipated to be CAR-T cell therapy, with a notably high CAGR of around 21.5%. CAR-T therapies involve engineering patient-derived T-cells to identify and eradicate cancer cells, offering personalized, precision-driven treatment options for hematologic malignancies.

In August 2025, for example, a case study published in The New England Journal of Medicine showed that a 51-year-old patient who developed CAR-positive T-cell lymphoma after CAR T-cell therapy for multiple myeloma achieved complete remission through a targeted regimen including mogamulizumab, marking the first reported successful use of this approach. The prospects of this segment are also being elevated by timely FDA approvals and steady investment inflows for immune-oncology therapies, and persistent research addressing scalability, cost reduction, and enhanced safety profiles.

Disease Type Insights

Lung cancer is anticipated to dominate with a market revenue share of around 20.7% in 2025. Not only is cancer of the lungs the most common type in the world, but it is also the most fatal type. According to the World Cancer Research Fund, in 2022, lung cancer killed over 2 million people worldwide. High incidence of smoking and increasing air pollution in urban centers have been contributing to the proliferation of lung cancer across the globe. As a result, there is an increased need for innovative treatments, particularly immuno-oncology therapies.

Drugs such as pembrolizumab and nivolumab have transformed the treatment of advanced non-small cell lung cancer (NSCLC), demonstrating superior survival benefits compared to conventional chemotherapy. Early diagnosis improvements via screening programs have expanded patient eligibility coverage for immunotherapy, creating a fertile market. Furthermore, the growing focus on biomarker-driven treatments, such as PD-L1 expression testing, deepens personalized treatment adoption in lung cancer, contributing to sustained market progress.

The prostate cancer segment is projected to exhibit a high CAGR through 2032, propelled by demographic shifts, including aging populations and better detection methodologies that have improved diagnostic accuracy. The market for prostate cancer is set to gain from the introduction of novel immunotherapies such as sipuleucel-T (Provenge), an FDA-approved therapeutic cancer vaccine that stimulates the immune system to attack prostate cancer cells. The unmet clinical need for effective treatments in metastatic castration-resistant prostate cancer (mCRPC) and the relentlessly elongating research pipeline aiming to combine immunotherapies with hormone therapies or checkpoint inhibitors are the other two major drivers for this segment.

Regional Insights

North America Immuno-Oncology Market Trends

At around 43.2%, North America is set to dominate the immuno-oncology market share in 2025, primarily due to a high prevalence of cancer in the region and substantial R&D investments for cancer research from leading biopharmaceutical companies and academic institutions. The National Cancer Institute (NCI) predicts that over 2 million new cancer cases will be diagnosed in the U.S. in 2025, and more than 600,000 people will die from the disease. These stark, data-based predictions are likely to propel the demand for cutting-edge immunotherapies such as checkpoint inhibitors in the region to prevent deaths.

Well-established regulatory frameworks facilitating expedited approvals, robust reimbursement policies supporting patient accessibility to advanced cancer therapies, and concentrated networks of comprehensive cancer centers adopting innovative treatments swiftly are some of the prime factors aiding the market here. Additionally, the increasing use of companion diagnostics for patient stratification and growth in combination immunotherapy regimens to overcome resistance are emerging as major regional market trends.

Asia Pacific Immuno-Oncology Market Trends

Accounting for around 27%, Asia Pacific is poised to be the fastest-growing regional market with an approximate CAGR of 13.0% during 2025-2032. The immuno-oncology market is poised for significant growth, driven by rising cancer incidence and increasing awareness of advanced therapies in the region. China and India are making profound strides with their national cancer screening programs, such as India’s Cancer Patient Fund under the Ministry of Health, and improvements in healthcare infrastructure, providing fertile ground for market expansion.

Government incentives for biotech and pharmaceutical innovation, along with streamlined regulatory pathways, are accelerating the market entry of novel immunotherapies. Growth opportunities are further fueled by a surge in clinical trials and expanding oncology research hubs in nations such as South Korea and Singapore.

Europe Immuno-Oncology Market Trends

The market in Europe is powered by an unshakable support for cancer research by the European Union (EU), log-running and well-established healthcare systems, and increasing adoption of immunotherapies across major economies such as Germany, France, and the U.K. Progressive approvals by the European Medical Agency (EMA) for new immune-oncological therapies and other emerging cancer treatments underscore the EU’s commitment to biopharmaceutical innovation, thus boosting the market.

Collaborative ecosystems involving academia, government, and industry are fostering research and enabling the co-development of novel agents. Reimbursement frameworks and EU-wide regulatory compliance are expected to further accelerate the adoption of immunotherapies in cancer treatment.

Competitive Landscape

The global immuno-oncology market landscape is highly competitive with a mix of participants deeply engaged in technological innovation, strategic collaborations, and an unwavering focus on developing personalized cancer therapeutics. A critical driver for the leading players is the continuous evolution of immune checkpoint inhibitors and CAR-T therapies, which have outpaced conventional treatments through durable efficacy and improved safety profiles, as illustrated by the accelerated FDA approval of AbbVie’s EMRELIST in 2025 for non-squamous NSCLC.

Competitiveness among market players is intensifying with the integration of AI and machine learning in drug discovery, enabling faster development and cost efficiencies, as well as the rise of combination immunotherapy regimens designed to overcome resistance to monotherapies. Mergers, acquisitions, and partnerships, such as the 2025 collaboration between BioNTech and Bristol Myers Squibb to co-develop novel immuno-oncology agents for solid tumors, are also being leveraged by companies to strengthen their market position.

Key Industry Developments

- In August 2025, Pfizer and Astellas’ Padcev, combined with Merck’s Keytruda, became the first systemic regimen to significantly improve survival in cisplatin-ineligible muscle-invasive bladder cancer patients when used before and after surgery, potentially redefining the standard of care.

- In July 2025, AbbVie signed a global licensing deal with Ichnos Glenmark Innovation (IGI) for ISB 2001, a first-in-class trispecific T-cell engager for relapsed/refractory multiple myeloma. The agreement includes US$700 Mn upfront, up to US$1.225 Bn in milestones, and tiered royalties. Early Phase 1 data showed a 79% overall and 30% complete response rate, highlighting its potential as a next-gen immuno-oncology therapy.

- In June 2025, Sanofi announced a US$9.1 Bn cash acquisition of Blueprint Medicines, potentially rising to US$9.5 Bn with milestone-based CVRs tied to BLU-808. The deal adds Ayvakit, the only FDA-approved treatment for systemic mastocytosis, and strengthens Sanofi’s rare disease and immunology pipeline.

Companies Covered in Immuno-Oncology Market

- Bristol-Myers Squibb Company

- Merck & Co., Inc.

- Pfizer Inc.

- Roche Holding AG

- Novartis AG

- Johnson & Johnson Services, Inc.

- AstraZeneca PLC

- AbbVie Inc.

- BioNTech SE

- Gilead Sciences, Inc.

Frequently Asked Questions

The immuno-oncology market is projected to reach US$56.8 Bn in 2025.

The alarming rise in cancer incidence worldwide is intensifying the demand for more effective, personalized cancer therapies, driving the market.

The market is poised to witness a CAGR of 22.7% from 2025 to 2032.

Key market opportunities include breakthroughs in biomarker detection assays, next-generation sequencing, and AI-driven analytics, which collectively facilitate more accurate patient selection and adaptive immunotherapy regimens.

Key players include Bristol-Myers Squibb Company, Merck & Co., Inc., and Pfizer Inc.