- Bulk Chemicals

- High-Performance Refinery Additives Market

High-Performance Refinery Additives Market Size, Share, and Growth Forecast, 2026 - 2033

High-Performance Refinery Additives Market by Product Type (Corrosion Inhibitors, Antifoulants, Antioxidants, Cetane Improvers, Octane Improvers, Stabilizers, Lubricity Improvers, Others), Fuel Type (Gasoline, Diesel, Jet Fuel, Heating Oil, Marine Fuel, Others), Application (Crude Oil Processing, Fluid Catalytic Cracking (FCC), Hydroprocessing, Others), and Regional Analysis for 2026 - 2033

High-Performance Refinery Additives Market Share and Trends Analysis

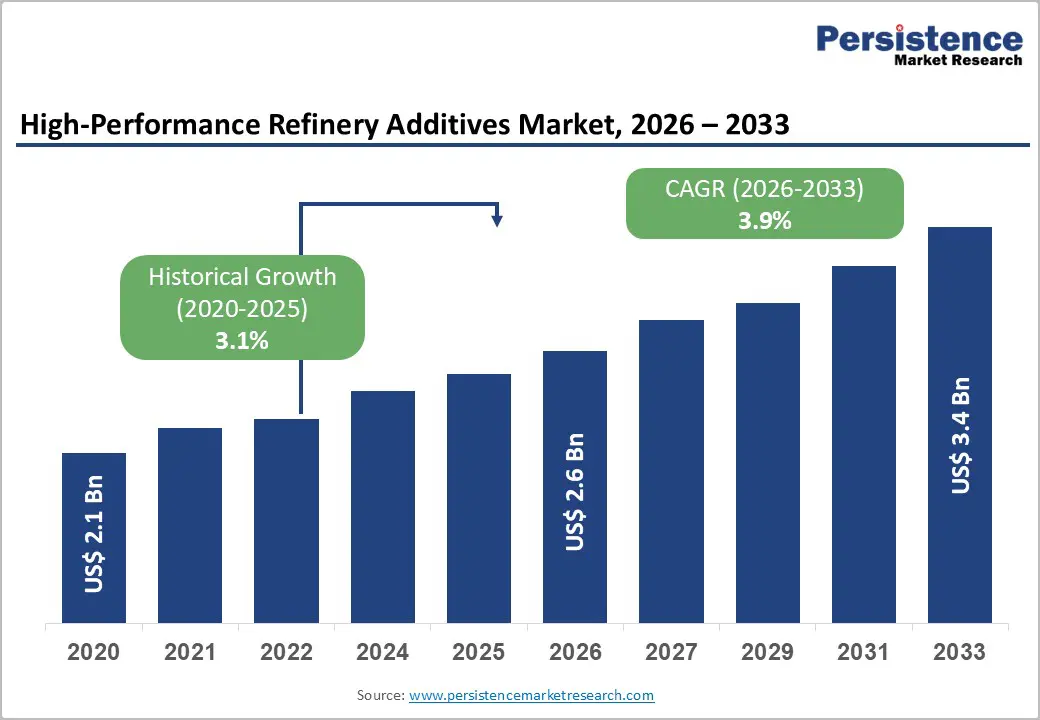

The global high-performance refinery additives market size is likely to be valued at US$ 2.6 billion in 2026, and is projected to reach US$ 3.4 billion by 2033, growing at a CAGR of 3.9% during the forecast period 2026−2033. Growth of refining complexity and the need for fuel quality optimization represent the central drivers of demand for high-performance refinery additives. Increasing processing of heavier and lower-quality crude oil streams requires chemical additives that stabilize fuel composition, prevent corrosion, and enhance refining efficiency.

Refinery operators deploy advanced additive solutions to maintain operational reliability, minimize fouling, and support catalytic performance in complex refining units. Energy transition policies and environmental standards further strengthen adoption of advanced refinery additives. Government agencies such as the International Energy Agency (IEA) and the United States Environmental Protection Agency (EPA) emphasize cleaner fuel production, which requires additives capable of reducing impurities and improving combustion characteristics.

Key Industry Highlights

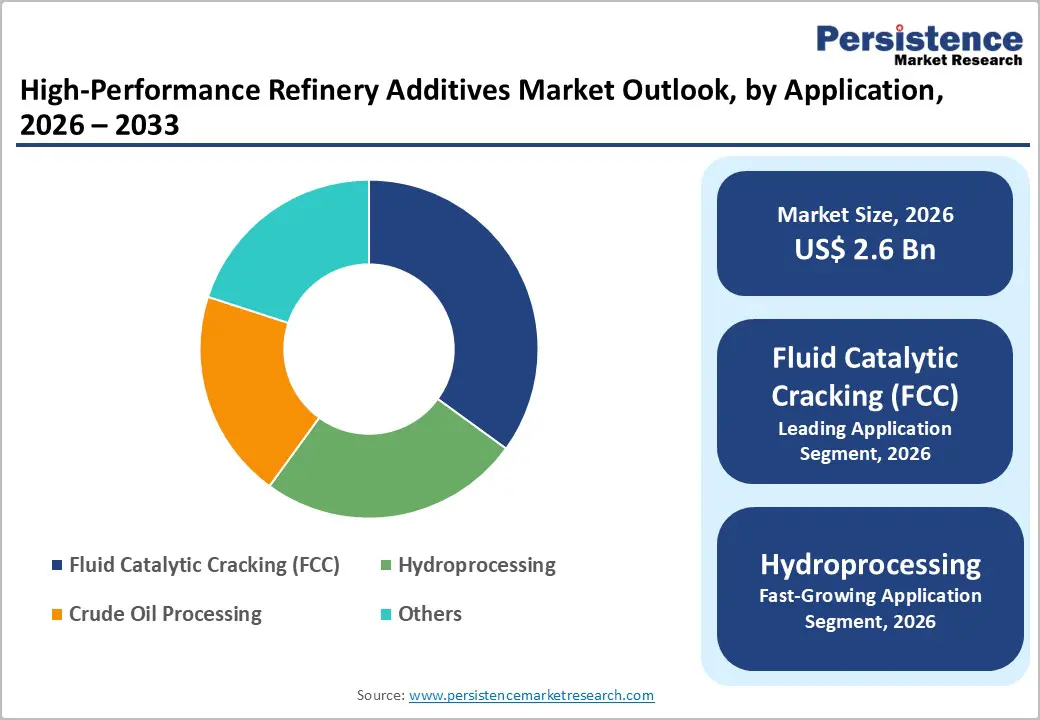

- Leading Application: Fluid catalytic cracking (FCC) is expected to hold a revenue share of about 35% in 2026, owing to additives that maintain catalyst performance.

- Fastest-growing Application: Hydroprocessing is forecasted to be the fastest-growing segment between 2026 and 2033, aided by additives that enhance catalyst stability and fuel purification.

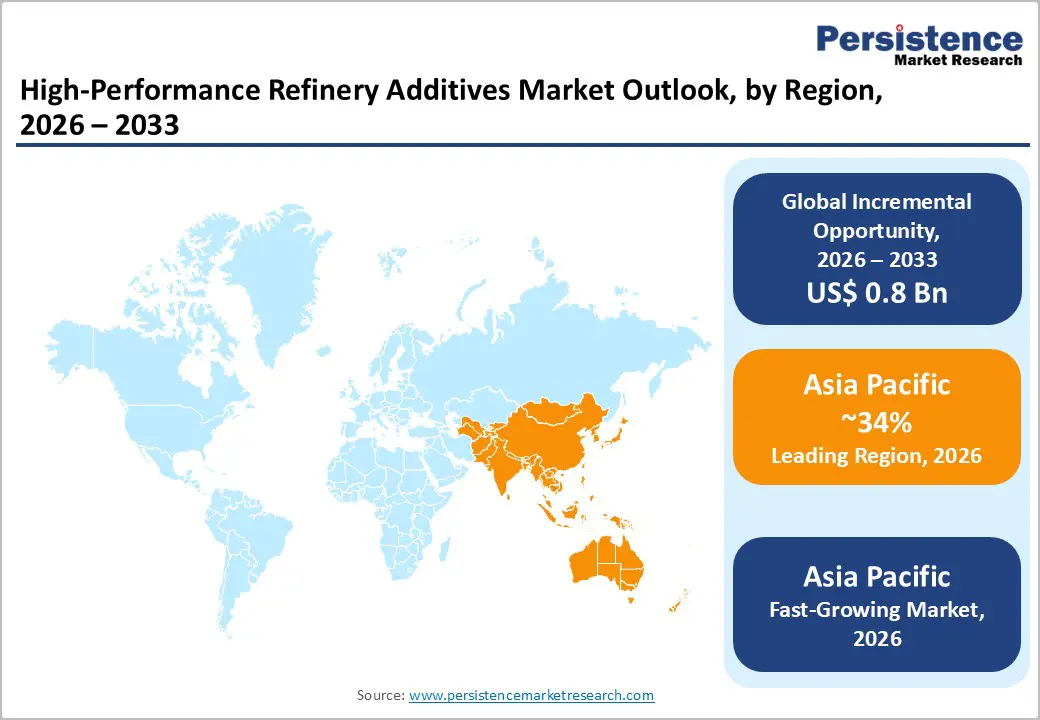

- Dominant Region: Asia Pacific is expected to dominate with approximately 34% market share in 2026, driven by expanding refineries and adoption of multifunctional additives.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, fueled by refinery expansions and multifunctional additives.

| Key Insights | Details |

|---|---|

|

High-Performance Refinery Additives Market Size (2026E) |

US$ 2.6 Bn |

|

Market Value Forecast (2033F) |

US$ 3.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

3.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Refinery Complexity and Processing of Heavy Crude Streams

Processing heavier and lower-quality crude streams increases operational severity across modern refining units. Heavy crude contains higher concentrations of sulfur, metals, asphaltenes, and complex hydrocarbons, which create challenges in distillation columns, hydrocrackers, cokers, and catalytic units. Elevated impurity levels accelerate corrosion, catalyst poisoning, and equipment fouling, reducing operational efficiency and increasing maintenance intervals. Advanced chemical additives address these operational constraints by stabilizing reaction conditions, neutralizing corrosive compounds, and preventing deposition in high-temperature equipment.

Rising processing intensity across global refining systems reinforces this requirement for specialized additives. Government energy statistics highlight the scale of refinery activity requiring advanced operational support. The U.S. Energy Information Administration (EIA) reported that refining capacity in the United States is expected to reach about 17.9 million barrels per day by the end of 2025, reflecting extensive utilization of complex refining units that process diverse crude grades. Complex conversion units such as delayed cokers, hydrocrackers, and hydrotreaters operate under high pressure and temperature conditions when handling heavy crude streams, intensifying risks related to fouling, catalyst degradation, and corrosion.

Expansion of Global Transportation Fuel Demand

Growing mobility across road freight networks, commercial aviation, and maritime logistics increases refining activity and intensifies operating conditions within distillation, catalytic cracking, and hydroprocessing units. Large volumes of crude processing expose refining systems to elevated temperatures, sulfur compounds, and unstable hydrocarbon intermediates that accelerate corrosion, fouling, and catalyst degradation. High-performance refinery additives support operational reliability through corrosion protection, deposit control, and stabilization of hydrocarbon streams during refining operations. Expanding vehicle fleets, aviation traffic, and global shipping activity stimulate continuous refinery utilization, creating strong demand for chemical treatment solutions that protect equipment and maintain production efficiency across complex refining environments.

Strict fuel quality expectations within the transportation sector reinforce the role of specialized additives during refining and fuel formulation processes. Gasoline, diesel, and aviation fuels require optimized combustion characteristics, storage stability, and compliance with environmental emission standards. Additive technologies such as cetane improvers, octane enhancers, antioxidants, and antifoulants enable refiners to achieve precise chemical balance in finished fuels while maintaining operational stability within processing units. Intensive refinery throughput linked with transportation fuel demand increases risks associated with fouling deposits, catalyst poisoning, and thermal degradation in refining systems.

Operational Integration Complexity within Refinery Systems

Operational compatibility challenges across complex refining units create significant barriers for chemical additive deployment. Modern refining infrastructure integrates multiple conversion processes such as hydrocracking, catalytic reforming, and alkylation that operate under distinct temperature, pressure, and feedstock conditions. Each process unit requires precise chemical dosing and compatibility with catalysts, metals, and crude compositions. Any mismatch between additive chemistry and process configuration may disrupt reaction efficiency, accelerate fouling, or alter catalyst activity. Refining systems therefore, demand customized formulations and extensive testing before operational implementation, which increases integration time and cost.

Operational scale and structural complexity intensify the integration barrier. Large refining networks operate through interconnected processing units, where a single operational adjustment can influence upstream and downstream chemical reactions. This interdependence limits the flexibility for introducing new additive technologies without redesigning monitoring protocols, injection systems, and safety procedures. According to the U.S. EIA, refinery infrastructure processed about 18.4 million barrels of crude oil per calendar day in the United States as of January 1, 2025, indicating the magnitude and operational intensity of modern refining facilities. In such high-throughput environments, even minor chemical incompatibility may trigger process instability, unplanned maintenance, or equipment integrity risks.

Volatility in Refining Margins and Energy Market Cycles

Fluctuating refinery profit spreads create a challenging investment climate for specialty chemical inputs used in fuel processing. Refining margins shift in response to crude price swings, product demand variability, and geopolitical supply disruptions. During periods of compressed margins, refinery management prioritizes cost control, maintenance deferral, and operational efficiency programs rather than procurement of premium chemical formulations. Energy market cycles therefore introduce irregular purchasing patterns across refinery operations, leading to inconsistent consumption volumes for specialty chemical suppliers. Data from the U.S. Energy Information Administration indicate that average refinery capacity utilization in the United States remained near 90% during 2025, reflecting operating pressure tied to margin management and feedstock cost volatility.

Energy market cyclicality further amplifies operational uncertainty across refining networks, especially during periods of crude price spikes or declining fuel demand. Refinery operators frequently adjust throughput rates, delay process optimization upgrades, and suspend non-essential chemical programs when profit spreads weaken. Procurement planning therefore becomes short-term and reactive rather than strategic, limiting long-term supply agreements for advanced refinery chemistry solutions. Financial risk exposure across the refining sector encourages cautious inventory management, reduced chemical storage volumes, and tighter procurement schedules.

Emergence of Advanced Refinery Digitalization and Process Optimization

Digital refinery transformation is creating strong demand for high-efficiency chemical solutions that support optimized processing environments. Integration of Industrial Internet of Things (IIoT), artificial intelligence (AI), and advanced process control systems allows continuous monitoring of parameters such as temperature, pressure, and hydrocarbon composition across refining units. Real-time operational data enables engineers to fine-tune catalyst performance, reaction conditions, and feedstock blending strategies. In such digitally controlled environments, chemical additives play a strategic role in stabilizing reactions, controlling fouling, and maintaining fuel quality under highly optimized operating conditions. Predictive maintenance systems supported by AI identify early signals of corrosion, deposition, or instability in refining units, prompting targeted use of inhibitors, antifoulants, and stabilizing agents.

Operational efficiency targets and sustainability policies further strengthen this opportunity. Digital optimization systems allow refineries to reduce energy consumption, emissions, and operating costs through automated control of process units. Data-driven decision platforms evaluate equipment performance, energy consumption, and production throughput simultaneously, creating demand for chemical formulations that enhance equipment reliability and energy efficiency. Smart sensors and predictive analytics improve equipment health monitoring and detect anomalies before operational disruption occurs, supporting timely additive intervention in heat exchangers, distillation columns, and catalytic units.

Technological Convergence with Multifunctional Additives

Integrated formulations that combine multiple functional properties into a single additive package create significant value for refiners by reducing the number of discrete chemical treatments required to achieve fuel quality and compliance objectives. These multifunctional additives can simultaneously enhance combustion characteristics, mitigate corrosion, prevent deposit formation, and improve fuel stability, resulting in streamlined inventory management and lower operational complexity for refinery process engineers. Simplified dosing regimens paired with broad-spectrum performance mitigate the need for frequent adjustments across different processing units while supporting the production of fuels that align with stringent regulatory standards for emissions and engine performance.

Government regulations such as the U.S. EPA’s requirements for additive registration under 40 CFR Part 79 demonstrate that fuel additives must meet defined performance and emissions criteria to be approved for use, encouraging innovation in fuel treatment technologies that address multiple refinery challenges within compliant formulations. This framework supports broader adoption of multifunctional solutions by providing a clear regulatory pathway for additives that can deliver performance, emissions control, and stability benefits in a single product, increasing operational efficiency while maintaining compliance with national fuel and air quality standards.

Category-wise Analysis

Product Type Insights

Corrosion inhibitors are poised to lead with a forecasted 22% of the high-performance refinery additives market revenue share in 2026, owing to the widespread requirement for equipment protection within refinery processing systems. Refinery infrastructure contains extensive networks of pipelines, reactors, and heat exchangers exposed to corrosive substances including sulfur compounds, acids, and water contaminants. Corrosion inhibitors provide chemical protection by forming protective films on metal surfaces, reducing chemical degradation within process units. Refinery operators prioritize corrosion prevention to maintain operational safety and equipment longevity. Corrosion damage can disrupt refining operations and increase maintenance requirements, which elevates operational costs. Additive solutions therefore represent essential components within refinery chemical treatment programs.

Cetane improvers are anticipated to be the fastest-growing segment between 2026 and 2033, fueled by increasing demand for high-quality diesel fuels in freight transportation and industrial mobility. Cetane improvers enhance ignition quality within diesel fuels, allowing more efficient combustion within diesel engines. Improved ignition performance reduces engine emissions, enhances fuel efficiency, and supports engine reliability in heavy-duty transport systems. Freight transportation networks depend heavily on diesel fuel for long-distance logistics and industrial distribution activities. Governments and regulatory agencies promote fuel quality improvements to reduce emissions from diesel engines. Cetane improvers enable refiners to achieve these performance objectives while maintaining fuel stability.

Application Insights

Fluid catalytic cracking is expected to hold a dominant position, accounting for an anticipated 35% of the high-performance refinery additives market share in 2026, driven by extensive use of catalytic conversion processes within modern refineries. FCC units convert heavy hydrocarbon fractions into lighter fuels such as gasoline and diesel. This process involves high-temperature catalytic reactions that require precise chemical stability and catalyst protection. Additives play a crucial role in maintaining catalyst efficiency and preventing fouling within FCC reactors. Antifoulants, metal deactivators, and catalyst stabilizers enhance catalytic performance and extend operational cycles.

The hydroprocessing is forecasted to be the fastest-growing application segment between 2026 and 2033, boosted by increasing demand for low-sulfur fuels and cleaner fuel production technologies. Hydroprocessing technologies remove sulfur, nitrogen, and other impurities from crude oil fractions through catalytic hydrogen treatment. These processes enable production of cleaner fuels that comply with environmental standards. Additives enhance hydroprocessing efficiency by preventing catalyst poisoning and reducing deposit formation. Catalyst stabilizers and corrosion inhibitors support reliable reactor performance under high-pressure hydrogen conditions. Environmental policies promoting low-sulfur fuels increase adoption of hydroprocessing technologies across global refineries.

Regional Insights

North America High-Performance Refinery Additives Market Trends

North America represents a mature refining landscape characterized by extensive processing capacity and advanced regulatory frameworks that drive adoption of high-performance additive solutions. Complex refinery operations in the United States and Canada prioritize production of low-sulfur diesel, gasoline, and jet fuels, increasing demand for chemistries that enhance thermal stability, prevent corrosion, and minimize deposit formation. Integration of renewable fuel blending, including biodiesel and ethanol, amplifies the need for multifunctional additives capable of maintaining compatibility and stability across diverse fuel streams. Operational efficiency initiatives, such as real-time process monitoring and predictive maintenance, incentivize use of solutions that optimize combustion performance, reduce downtime, and extend equipment lifespan.

Investments in refinery modernization and upgrading catalytic processes create opportunities for innovative additive formulations that support throughput enhancement and emission compliance simultaneously. Stringent environmental standards enforced by authorities, including the U.S. Environmental Protection Agency, stimulate adoption of high-performance chemistries that enable compliance with fuel quality and air emission requirements. Texas and Louisiana serve as key hubs for refining expansions focused on heavier and sour crude feedstock, generating demand for specialized solutions that maintain operational reliability and fuel performance.

Europe High-Performance Refinery Additives Market Trends

Europe represents a technologically advanced refining environment characterized by stringent environmental regulations and fuel quality standards. Established refining complexes in Germany, Italy, and the Netherlands focus on high-value middle distillates and low-sulfur fuels, increasing reliance on multifunctional additives that reduce fouling, enhance thermal stability, and protect equipment from corrosion. Integration of petrochemical production within refinery units elevates demand for solutions capable of maintaining consistent product quality across multiple process streams. Automation and real-time monitoring adoption encourages the deployment of chemistries that optimize combustion efficiency, extend equipment lifespan, and minimize operational disruptions.

Biofuel blending initiatives in France and Spain further drive the need for specialized additives that ensure stability and compatibility in blended fuels while maintaining throughput and compliance with emission mandates. Germany and Italy lead efforts to process heavier, higher-sulfur feedstock, generating demand for additives that sustain throughput while controlling emissions. Ports in the Netherlands and Belgium emphasize low-sulfur marine fuels, driving use of chemistries that prevent deposit formation and maintain fuel lubricity under variable operating conditions. Operational optimization and emission compliance pressures shape consumption patterns for high-performance chemistries, supporting innovation and strategic deployment across refining and fuel production networks.

Asia Pacific High-Performance Refinery Additives Market Trends

Asia Pacific is expected to dominate with an estimated 34% of the high-performance refinery additives market value in 2026, reflecting rapid expansion of complex refining units designed to process heavier, sulfur-rich feedstock while producing higher volumes of middle distillates and petrochemical intermediates. Increasing adoption of advanced additive technologies enables integrated management of corrosion, fouling, and fuel stability, reducing operational disruptions and enhancing overall throughput efficiency. Rising industrial activity and transportation fuel consumption elevate demand for multi-functional chemistries capable of maintaining compliance with evolving emission standards. Investment in refinery modernization and catalytic optimization drives preference for additives that improve thermal stability, combustion performance, and equipment lifespan.

Asia Pacific is forecasted to be the fastest-growing market for high-performance refinery additives between 2026 and 2033, stimulated by ongoing capacity expansions that surpass global growth averages, coupled with rising requirements for cleaner fuels and strict air quality regulations. Integration of petrochemical operations within refining complexes intensifies demand for multifunctional solutions that support higher product yields with lower energy input. Operational optimization strategies, including automation and real-time process monitoring, increase reliance on additives that provide multi-dimensional performance benefits. Government-mandated fuel quality and emission standards further accelerate adoption of high-efficiency chemistries, driving both market penetration and incremental innovation.

Competitive Landscape

The global high-performance refinery additives market structure demonstrates moderate concentration, with several multinational specialty chemical companies controlling substantial portions of the market. Key players such as ExxonMobil, Chevron, Total Energies, BASF, Evonik, Clariant, and Lubrizol leverage extensive global networks and integrated refining partnerships to deliver advanced additive solutions that optimize fuel stability, combustion performance, and equipment reliability. Large-scale chemical manufacturers capitalize on research and development capabilities to introduce multifunctional formulations that address multiple refinery challenges within a single product, enhancing operational efficiency and minimizing downtime.

Competitive positioning in this market depends on continuous product innovation, robust technical service offerings, and long-term relationships with refinery operators. ExxonMobil Corporation and Chevron Corporation focus on leveraging proprietary chemistries and field support to strengthen refinery process efficiency, while BASF SE and Evonik Industries prioritize performance-driven solutions for high-value fuels and petrochemicals. Clariant AG and Lubrizol Corporation differentiate through customized additive programs and engineering services that enhance compatibility with complex feedstock and emerging emission standards. Total Energies integrates additive solutions with sustainability objectives, aligning fuel performance improvements with regulatory compliance.

Key Industry Developments

- In February 2026, Baker Hughes signed a multiyear agreement with Marathon Petroleum to become its preferred provider of hydrocarbon treatment products and downstream chemical technologies across U.S. refineries.

- In September 2025, BASF SE unveiled its next-generation Keropur® Gasoline Performance Additive Series, certified to meet the revised U.S. TOP TIER+™ standard and designed to protect engines, improve fuel economy, and support cleaner combustion ahead of the January 2027 implementation deadline.

- In August 2025, Afton Chemical launched the HiTEC® 65522 gasoline performance additive series approved for the new TOP TIER+™ gasoline standard to support modern direct injection engine requirements.

Companies Covered in High-Performance Refinery Additives Market

- ExxonMobil Corporation

- Chevron Corporation

- Total Energies

- BASF SE

- Evonik Industries

- Clariant AG

- Lubrizol Corporation

- Afton Chemicals

- Baker Hughes

- GE Power & Water

- Dorf Ketal Chemicals

- Cristol

- Innospec

- Albermarle Corporation

- Amspec LLC

- Hindustan Petroleum

- Bharat Petroleum

Frequently Asked Questions

The global high-performance refinery additives market is projected to reach US$ 2.6 billion in 2026.

Rising demand for cleaner fuels, stricter emission regulations, and the need for enhanced refinery efficiency are driving the market.

The market is poised to witness a CAGR of 3.9% from 2026 to 2033.

Development of multifunctional additives and technological integration in refining processes represent key market opportunities.

Some of the key market players include ExxonMobil Corporation, Chevron Corporation, Total Energies, BASF SE, Evonik Industries, Clariant AG, and Lubrizol Corporation.