- Agrochemicals

- Herbicide Safener Market

Herbicide Safener Market Size, Share, and Growth Forecast 2026 - 2033

Herbicide Safener Market by Product Type (Benoxacor, Furilazole, Dichlormid, Isoxadifen, Other Safeners), by Crop Type (Barley, Maize, Rice, Sorghum, Soybeans, Wheat, Others), by Application (Pre-Emergence, Post-Emergence), by Regional Analysis, 2026 - 2033

Herbicide Safener Market Size and Trend Analysis

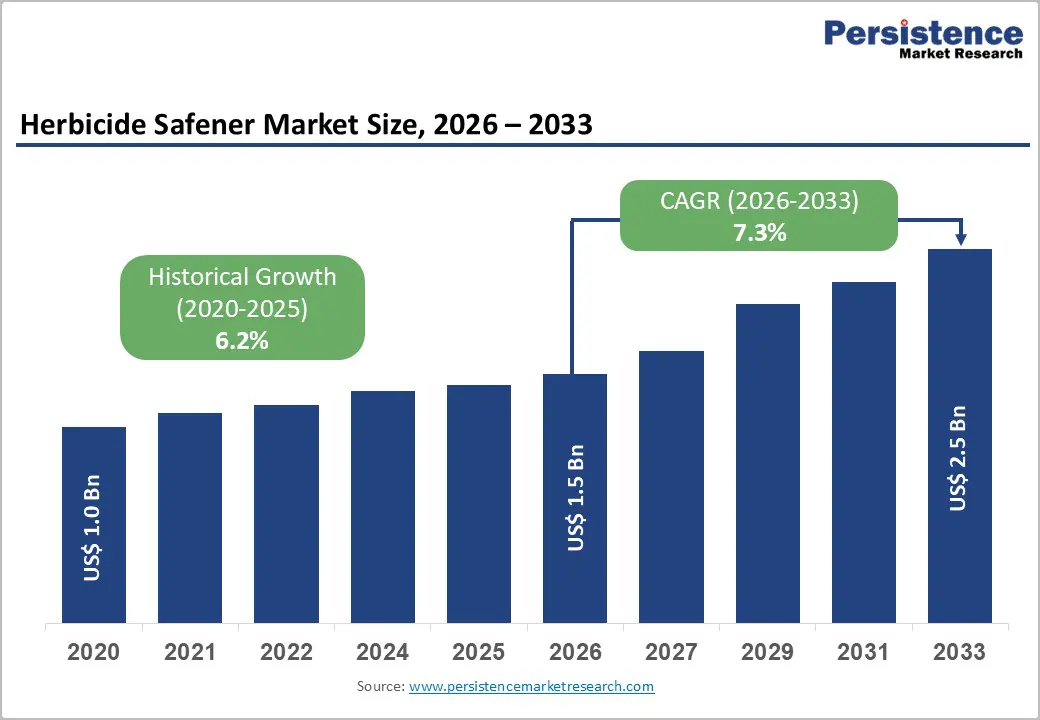

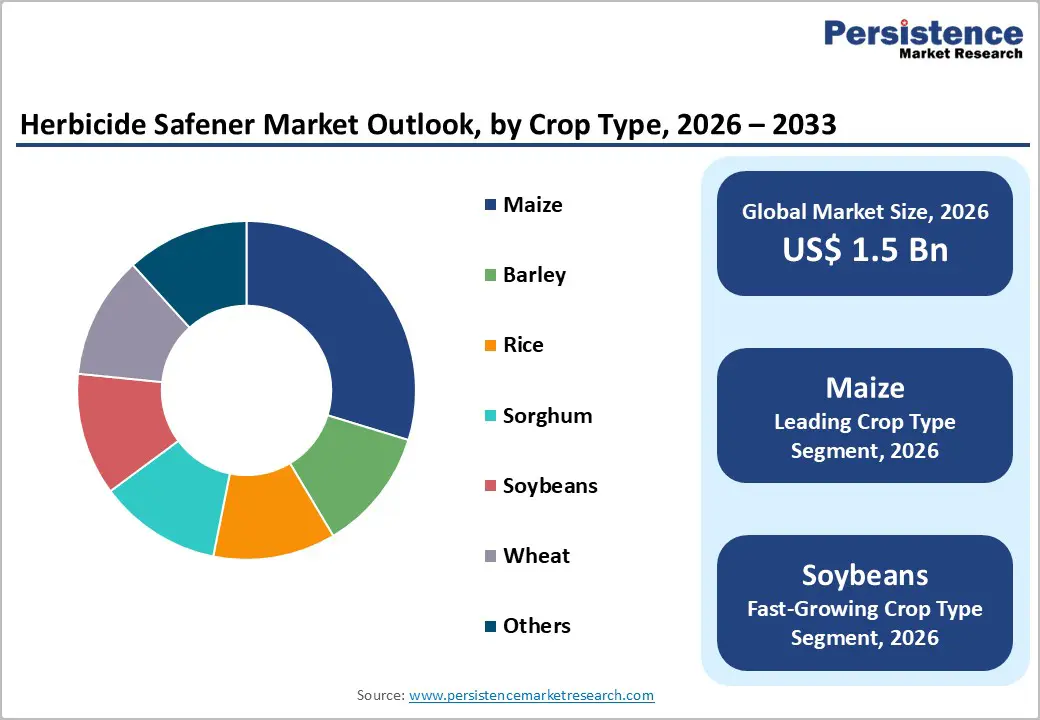

The global herbicide safener market size is expected to be valued at US$ 1.5 billion in 2026 and projected to reach US$ 2.5 billion by 2033, growing at a CAGR of 7.3% between 2026 and 2033.

The market expansion is fundamentally driven by escalating global food production requirements to support expanding populations, intensifying agriculture on limited arable land, and accelerating the adoption of sustainable crop protection strategies that minimize herbicide application rates and environmental impact.

The increasing prevalence of herbicide-resistant weed populations demands more sophisticated herbicide formulations paired with safeners to protect valuable crops, including corn, soybean, wheat, and rice. According to the Food and Policy Research Institute, meeting global grain demand requires an additional 6 million hectares of corn and 4 million hectares of wheat, combined with 12% yield increases, directly amplifying demand for herbicide safener solutions that enable efficient weed management without crop injury.

Key Industry Highlights:

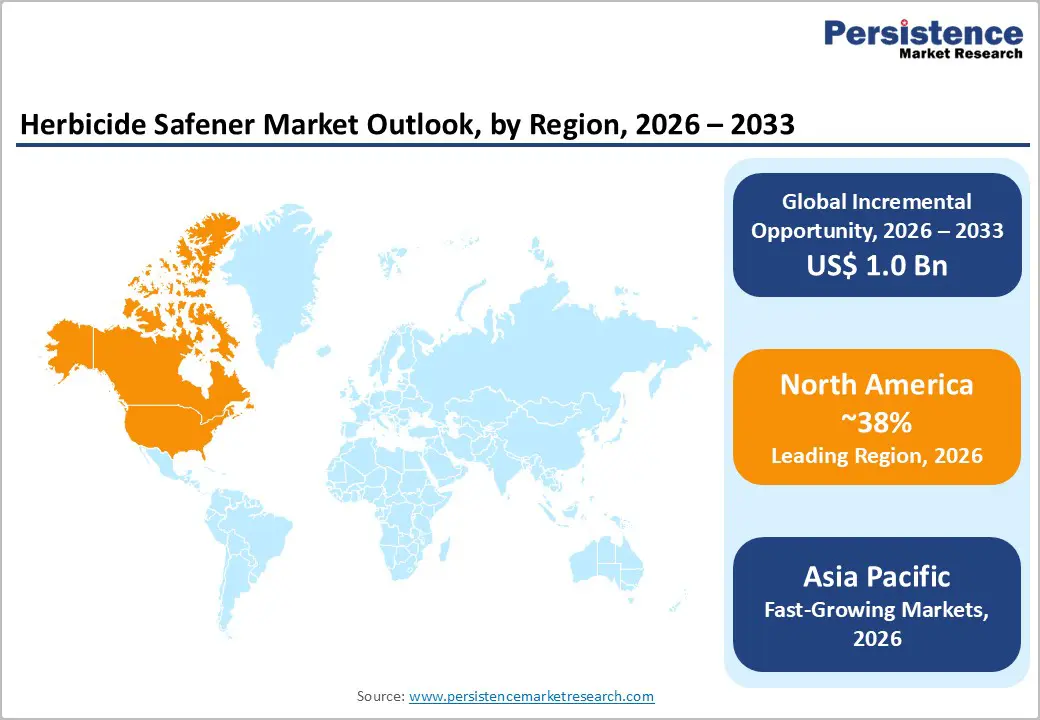

- Leading Region: North America dominates the global Herbicide Safener Market with approximately 38% share in 2025, supported by extensive corn and soybean cultivation, established herbicide safener infrastructure, and strong farmer awareness regarding crop protection benefits.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, expected to post approximately 8.3% CAGR through 2033, driven by agricultural intensification in China and India, expanding herbicide usage, and government support for advanced crop protection technologies.

- Dominant Segment from Product Type: Benoxacor leads with roughly 36% share in 2025, driven by proven effectiveness protecting corn and cereal crops from herbicide injury and compatibility with multiple herbicide formulations.

- Fastest Growing Segment from Crop Type: Soybeans is the fastest-growing segment, with estimated 8.2% CAGR through 2033, fueled by expanding global cultivation, herbicide-resistant weed challenges, and increasing safener adoption in soybean protection programs.

- Key Market Opportunity: Seed-applied herbicide safener solutions and precision agriculture integration present significant opportunity for developing proactive crop protection systems reducing overall herbicide application requirements while improving sustainability alignment.

| Key Insights | Details |

|---|---|

|

Herbicide Safener Market Size (2026E) |

US$ 1.5 billion |

|

Market Value Forecast (2033F) |

US$ 2.5 billion |

|

Projected Growth CAGR (2026-2033) |

7.3% |

|

Historical Market Growth (2020-2025) |

6.2% |

Market Dynamics

Drivers - Expanding Global Crop Production and Intensified Agricultural Demand

Global agricultural intensification presents a powerful growth catalyst for herbicide safener adoption, as farmers worldwide confront mounting pressure to maximize yields from finite arable resources while managing escalating weed pressure. The United States Department of Agriculture reports that global corn production is expanding significantly, with approximately 91 million acres planted annually in the United States alone, creating substantial demand for integrated herbicide management solutions incorporating safeners. Safeners enable farmers to utilize more effective herbicides while minimizing crop damage risks, thereby optimizing weed control efficacy and protecting crop yields.

The Indian agrochemical industry reported herbicide segment revenues exceeding INR8,200 crore in 2024, demonstrating robust growth driven by intensive crop production requirements, limited cultivatable land, and rising farmer awareness regarding herbicide safener benefits. Developing nations in Asia, Latin America, and Africa are rapidly adopting safener-herbicide combinations as agricultural productivity pressures intensify, supported by increasing government investments in agricultural infrastructure and farmer education initiatives promoting advanced crop protection practices.

Rising Prevalence of Herbicide-Resistant Weeds and Crop Protection Needs

The emergence of herbicide-resistant weed populations represents a critical growth driver for safener adoption, as traditional herbicide applications become less effective, necessitating alternative weed management strategies and enhanced crop protection formulations. Herbicide-resistant weeds have become a major agricultural challenge, with resistant biotypes identified in most major crop-producing regions globally, forcing farmers to adopt more sophisticated herbicide programs combining multiple active ingredients with advanced safeners.

Safeners enhance crop tolerance to herbicides by inducing protective enzyme expression, particularly glutathione transferases (GSTs), which metabolize herbicides into harmless compounds while leaving herbicide efficacy on target weeds unchanged. The United States Environmental Protection Agency expanded regulatory tolerance for safeners including cloquintocet-mexyl in March 2024, permitting broader herbicide formulation applications and facilitating adoption across diverse crop types. This regulatory action acknowledges safener value in sustainable agriculture, enabling farmers to deploy stronger herbicide active ingredients paired with enhanced crop safeguards, directly supporting expanded safener market penetration across North American and international agricultural markets.

Restraints - High Product Development and Regulatory Compliance Costs

Developing new herbicide safener formulations requires substantial research and development investments, regulatory testing, and environmental impact assessments, creating barriers to entry for smaller manufacturers and limiting market competition. Each new safener candidate must undergo extensive toxicological evaluation, environmental fate studies, and field efficacy trials across diverse crop types and geographic regions before regulatory approval, incurring development costs often exceeding US$ 10-15 million per product.

Ongoing regulatory scrutiny of safener residues in surface waters, with dichloroacetamide safeners detected in 43% of Midwestern United States water samples, is intensifying environmental compliance requirements and potential future restrictions limiting safener applications. These regulatory complexities and compliance costs favor large multinational agrochemical companies with established regulatory expertise and substantial financial resources, constraining market entry opportunities for emerging competitors and regional players with limited development budgets.

Potential Environmental Concerns and Regulatory Uncertainty

Environmental detection of dichloroacetamide safeners including benoxacor (maximum 190 ng/L), furilazole (150 ng/L), and dichlormid (42 ng/L) in surface waters raises long-term regulatory uncertainty regarding potential use restrictions or enhanced application limitations. Scientific research has documented safener presence in groundwater and surface environments following agricultural application, prompting regulatory agencies to evaluate potential long-term ecological and human health impacts.

This environmental scrutiny could result in future use restrictions, reduced application rates, or regulatory designation changes that would constrain market growth and necessitate reformulation of established products. Regulatory uncertainty regarding safener classification and potential reclassification as active ingredients rather than adjuvants could substantially increase compliance burdens, development costs, and potential liability risks for manufacturers, particularly affecting smaller companies lacking sophisticated regulatory risk management capabilities.

Opportunities - Development of Integrated Pest Management and Sustainable Agriculture Solutions

Significant opportunities exist for manufacturers developing integrated herbicide safener solutions aligned with global sustainability initiatives, precision agriculture adoption, and organic farming expansion where selective herbicide applications with safeners provide environmentally preferred weed management alternatives. The European Union’s ambitious Farm to Fork Strategy emphasizes reducing chemical pesticide use by 50% by 2030, creating substantial opportunities for herbicide safener suppliers to demonstrate how safener-enabled herbicide formulations reduce overall chemical input requirements while maintaining crop safety and yield protection.

Seed-applied herbicide safeners represent an emerging high-growth opportunity, enabling proactive crop protection from crop emergence while reducing herbicide application complexity and labor requirements. Research institutions including IACR-Long Ashton Research Station have documented that seed-dressing applications of safeners including naphthalic anhydride substantially reduce crop damage compared to untreated seeds, supporting adoption of seed treatment technologies among seed companies and major agricultural retailers.

Expansion into Emerging Agricultural Markets and Developing Economies

Asia-Pacific and Latin American agricultural markets present significant growth opportunities as crop intensification accelerates, farmer awareness regarding herbicide safeners increases, and government support for advanced agricultural technologies expands. China and India are experiencing rapid agricultural modernization with expanding herbicide usage across major crops including rice, wheat, and corn, creating substantial demand for safener-enhanced formulations optimized for regional cropping systems and weed populations.

Emerging market entry strategies focusing on developing simplified, cost-effective safener formulations tailored to regional crop types and farmer affordability constraints could unlock significant market expansion among smallholder farmers and agricultural communities currently utilizing older, less sophisticated crop protection technologies. Partnerships with local agricultural distributors, regional agrochemical manufacturers, and government agricultural extension services facilitate market penetration in developing economies with limited access to multinational agrochemical company sales networks.

Category-wise Analysis

Product Type Insights

Benoxacor is the leading product type in the herbicide safener market, accounting for approximately 36% of market share in 2025, driven by its proven effectiveness in protecting corn and other cereal crops from chloroacetamide herbicide injury. Its strong compatibility with widely used pre- and post-emergence herbicides makes it a preferred choice for integrated weed management programs, particularly in large-scale row crop farming. Benoxacor delivers consistent crop safety across varying soil conditions and climates, supporting stable yields under intensive herbicide use. Broad regulatory acceptance in major agricultural regions further reinforces its adoption. As herbicide-resistant weed pressure increases, benoxacor continues to serve as a cornerstone safener in high-value cropping systems, sustaining its dominant market position.

Crop Type Insights

Maize represents the largest crop segment, holding approximately 28% of herbicide safener demand in 2025 due to its extensive cultivation and high dependence on chemical weed control. Corn is particularly sensitive to herbicide phytotoxicity, making safener use essential for protecting early-stage crop development. Large maize acreages, especially in North America, consistently apply safener-enhanced herbicide programs to maintain yield stability and weed control efficiency. The widespread adoption of pre-emergence herbicides in maize production further strengthens safener demand. As maize remains a staple crop with intensive input requirements, its dominance continues to anchor overall herbicide safener consumption.

Application Insights

Pre-emergence application dominates the herbicide safener market, accounting for nearly 59% of total usage in 2025. Applying safeners before or at planting provides early protection to emerging seedlings, allowing effective weed suppression without crop damage. This timing integrates seamlessly with standard herbicide application schedules, minimizing operational complexity for farmers. Pre-emergence safeners enable the use of stronger herbicide chemistries by enhancing crop detoxification mechanisms, improving weed control reliability. Their role in supporting efficient, large-scale farming operations and consistent yield protection continues to make pre-emergence applications the preferred choice in modern crop management systems.

Regional Insights

North America Herbicide Safener Market Trends and Insights

North America maintains the dominant position in the global herbicide safener market, commanding approximately 38% market share in 2025, supported by extensive corn and soybean cultivation, established herbicide safener infrastructure, strong regulatory framework supporting safener adoption, and dominant presence of major agrochemical manufacturers. The United States accounts for the substantial majority of North American consumption, with approximately 91 million acres of corn and extensive soybean acreage requiring integrated herbicide management incorporating safeners. Farmer awareness regarding herbicide-resistant weed management and crop protection benefits drives consistent demand for established safener products, supported by long-standing regulatory acceptance and demonstrated field performance across diverse environmental conditions.

Research and development investments by major manufacturers, including Bayer AG, BASF SE, Syngenta AG, and DuPont in North American facilities support continuous product innovation and market expansion strategies. Regulatory agencies, including the United States Environmental Protection Agency, actively support safener adoption through expanded regulatory tolerances, as demonstrated by the March 2024 amendment broadening cloquintocet-mexyl usage across multiple herbicide formulations. The competitive North American market features numerous safener-herbicide combinations available through diverse agricultural input distribution channels, supporting farmer choice and driving market penetration across diverse farming scales and operational philosophies.

Europe Herbicide Safener Market Trends and Insights

Europe represents a significant herbicide safener market, commanding approximately 26% market share in 2025, characterized by stringent environmental regulations, emphasis on sustainable agriculture practices, and established herbicide safener adoption in cereal and corn production. The European Union’s regulatory harmonization initiatives create standardized safener approval processes across member states, facilitating product registration and supporting efficient market expansion. Germany, the United Kingdom, France, and Spain maintain substantial cereal production acreage requiring herbicide protection, supporting robust safener demand across grain crops, including wheat, barley, and corn.

European manufacturers and distributors emphasize safener solutions aligned with EU Farm to Fork Strategy objectives for reducing chemical pesticide applications by 50% by 2030, positioning herbicide safeners as critical enabling technologies for sustainable agriculture transitions. Regulatory emphasis on environmental protection and integrated pest management principles supports safener adoption as preferred solutions, minimizing total herbicide application volume while maintaining crop safety and effective weed control. European research institutions and agricultural extension services promote safener adoption through scientific evidence demonstrating crop protection benefits, supporting farmer confidence and accelerating technology diffusion across varied farming systems.

Asia Pacific Herbicide Safener Market Trends and Insights

Asia Pacific emerges as the fastest-growing herbicide safener market, projected to expand at approximately 8.3% CAGR through 2033, driven by agricultural intensification, expanding herbicide usage, rising herbicide-resistant weed populations, and government support for advanced crop protection technologies. China and India represent the largest regional markets, with massive corn, rice, wheat, and soybean production acreages requiring integrated herbicide management incorporating safeners. China’s extensive corn production, reaching tens of millions of acres annually, combined with rapid agricultural modernization and expanding farmer adoption of advanced crop protection inputs, supports robust herbicide safener demand growth.

India’s robust agricultural sector intensification, documented by herbicide segment revenues exceeding INR 8,200 crore in 2024, reflects expanding farmer adoption of safener-enhanced herbicide formulations. Agricultural extension services and government initiatives promoting productivity enhancement drive farmer awareness and adoption of herbicide safener technologies previously concentrated in developed markets. ASEAN region countries, including Vietnam, Thailand, and Indonesia, are experiencing agricultural modernization supporting increased herbicide adoption and safener utilization across diverse crop systems. Lower manufacturing costs, expanding distribution infrastructure, and development of cost-effective safener formulations optimized for regional crops create manufacturing and commercial opportunities, attracting both multinational and regional agrochemical companies to Asia-Pacific market expansion initiatives.

Competitive Landscape

Regional and mid-sized players compete by focusing on localized formulations, cost efficiency, and adaptation to region-specific cropping systems, particularly in emerging agricultural markets. Across the industry, companies are investing in sustainable chemistry, biotechnology, and precision agriculture tools to enhance product effectiveness and regulatory compliance. Smaller participants strengthen their positions through niche targeting, strong local distribution, and agronomic support.

Key Developments:

- December 2025: Syngenta Canada launches Storen™ corn herbicide with four active ingredients for burndown and residual control against resistant weeds like waterhemp and Palmer amaranth, available in limited quantities for 2026.

- December 2025: BASF launches Centurion ADV, a Group 1 post-emergent herbicide with clethodim and built-in adjuvant, targeting grassy weeds and volunteer corn in soybeans up to flowering. Available now in Eastern Canada for 2026 use, tank-mixable with Liberty or glyphosate.

Companies Covered in Herbicide Safener Market

- Bayer AG

- DuPont

- Syngenta AG

- BASF SE

- Nufarm Limited

- Adama Agricultural Solutions

- UPL Limited

- Drexel Chemical Company

- Winfield Solutions LLC

- Sipcam Agro

- Subaru Corporation

- Helm AG

- Land O’Lakes, Inc.

- Corteva Agriscience

- Arysta LifeScience

- FMC Corporation

- Sumitomo Chemical Co., Ltd.

Frequently Asked Questions

The herbicide safener market is projected to reach approximately US$ 1.5 billion in 2026.

Growth is driven by agricultural intensification, rising herbicide-resistant weeds, and support for sustainable farming practices.

North America leads the market with about 38% share.

Seed-applied herbicide safeners represent the most attractive growth opportunity.

Major participants include Bayer, BASF, Syngenta, Corteva, UPL, and Nufarm.