- Industrial Machinery

- Firewood Processors Market

Firewood Processors Market Size, Share, and Growth Forecast 2026 - 2033

Firewood Processors Market by Processor Type (Circular Saw Firewood Processors, Chainsaw Firewood Processors, Hydraulic Firewood Processors, Kinetic Firewood Processors), Power Source (PTO Driven Processors, Electric Firewood Processors, Diesel Engine Processors, Gasoline Engine Processors), Processing Capacity (Small Capacity Processors <3 Cords/Hour, Medium Capacity Processors 3-6 Cords/Hour, High Capacity Processors >6 Cords/Hour), End-user, and Regional Analysis for 2026 - 2033

Firewood Processors Market Size and Trend Analysis

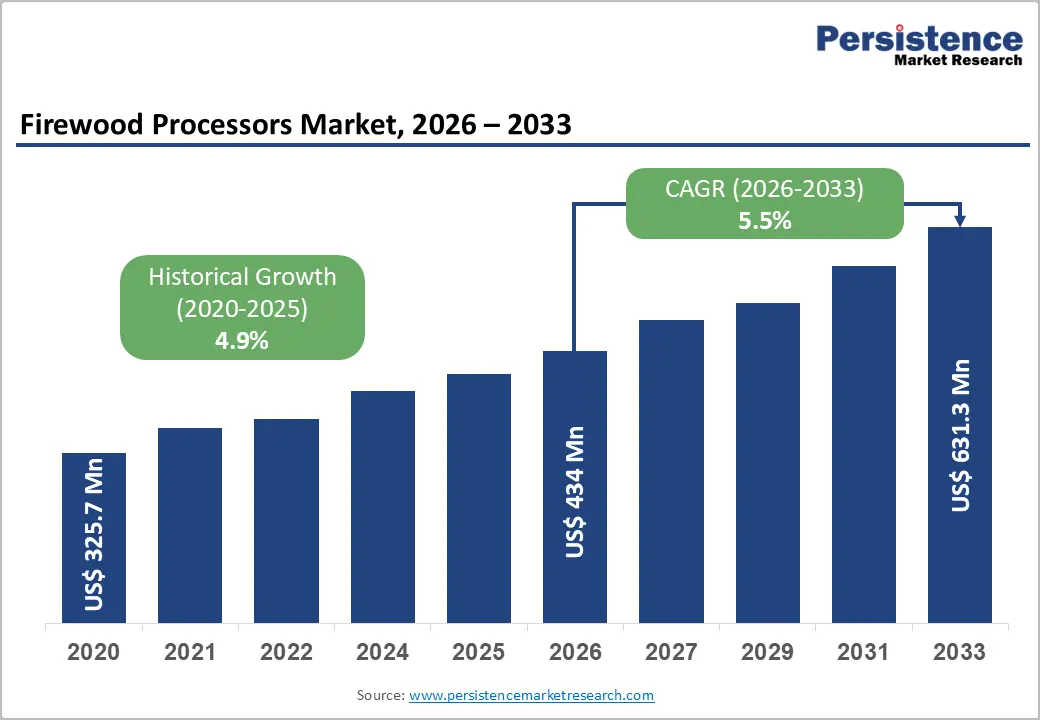

The global firewood processors market size is estimated to be valued at US$ 434 million in 2026 and is projected to reach US$ 631.3 million growing at a CAGR of 5.5% between 2026 and 2033.

The demand for biomass and solid wood fuel across residential and industrial heating applications, particularly in cold-climate regions of North America and Europe, contributes to its growth. Traditionally, firewood processing depended heavily on chainsaws, manual splitters, and intensive physical labor.

Modern firewood processors now integrate cutting, splitting, and loading functions into a single automated system, significantly streamlining operations. Advanced features such as live decks, hydraulic log handling systems, integrated conveyors, and multiple wedge configurations allow manufacturers and operators to process large volumes of wood more safely, quickly, and consistently while minimizing manual handling and operational downtime.

Growing adoption of mechanized log processing equipment to replace manual splitting labor, combined with expanding commercial firewood supply chains and biomass energy programs supported by governments across the European Union and the United States, continues to drive strong market growth.

Key Industry Highlights:

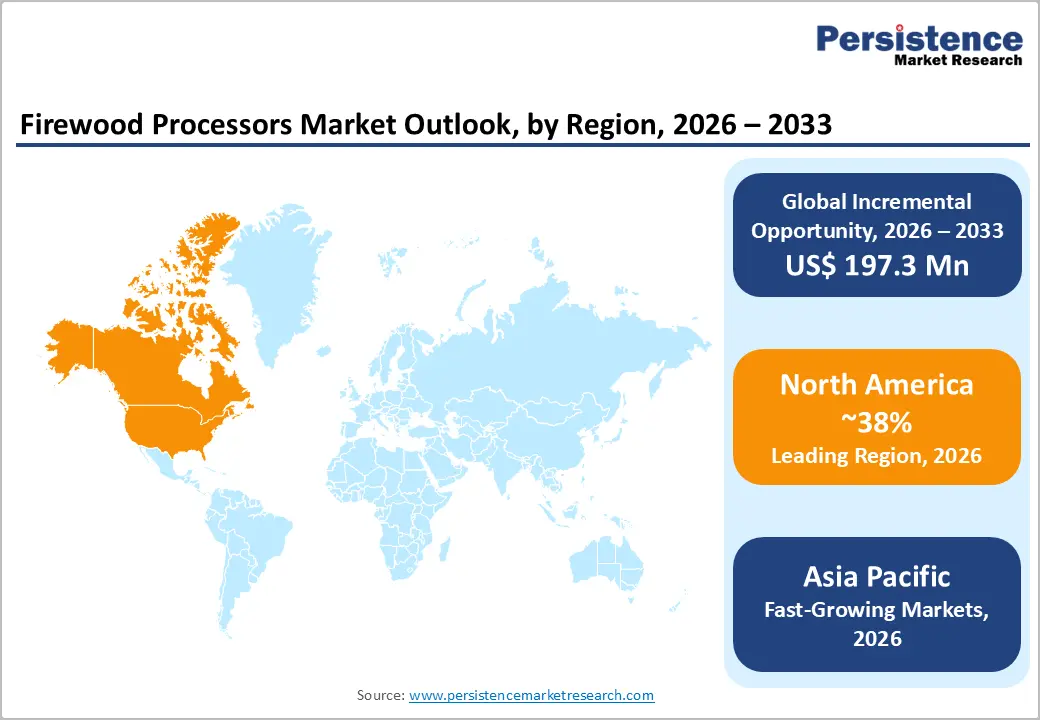

- Leading Region - North America: North America holds approximately 38% of global market share, supported by strong residential wood heating demand, extensive forestry contractor networks, and well-developed commercial firewood supply chains across the U.S. and Canada.

- Fastest Growing Region - Asia Pacific: Asia Pacific is the fastest growing region, driven by China's biomass energy programs, India's agricultural mechanization subsidies, and South Korea's forestry modernization initiatives, expanding firewood processor adoption at an above-average CAGR.

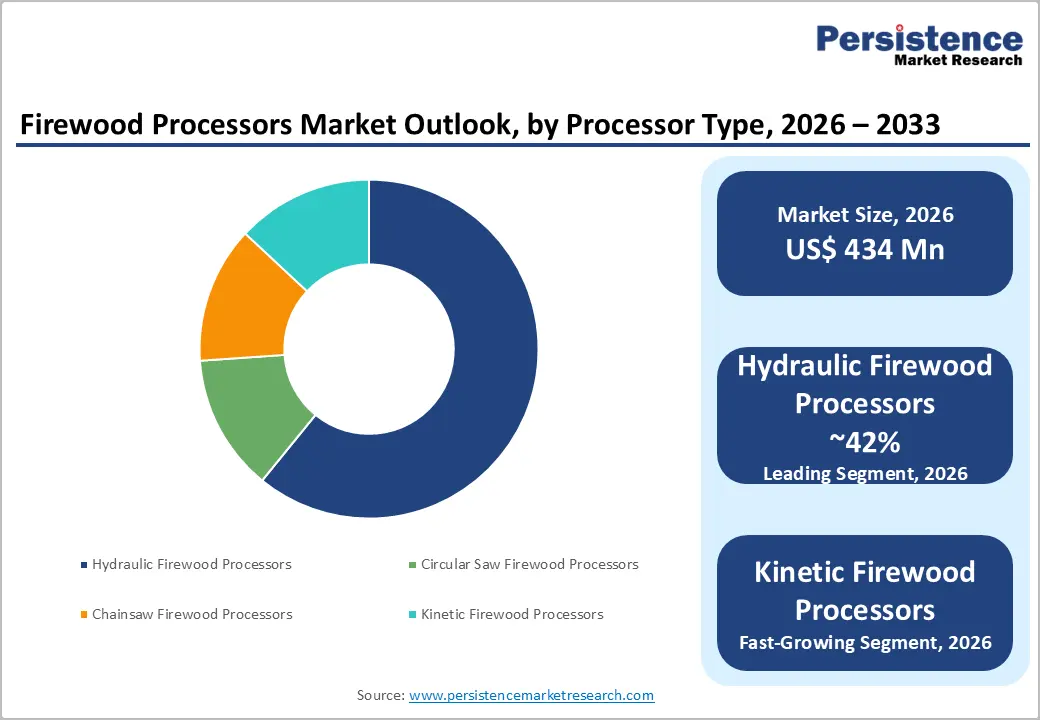

- Dominant Segment - Hydraulic Firewood Processors: Hydraulic Firewood Processors lead the Processor Type category with approximately 42% share in 2025, favored for their versatility, force consistency, and compatibility across residential, commercial, and industrial end-use applications globally.

- Fastest Growing Segment - Biomass Fuel Companies: Biomass Fuel Companies represent the fastest growing end-user segment at a projected CAGR of 8.4%, propelled by EU Renewable Energy Directives and U.S. Renewable Fuel Standards expanding wood-based fuel supply chain infrastructure.

- Key Opportunity - Electrification and Smart Technology: Integration of electric drivetrains, rechargeable battery systems, and IoT-enabled monitoring in next-generation firewood processors presents significant differentiation opportunities for manufacturers targeting emission-restricted commercial environments.

Market Dynamics

Drivers - Rising Biomass Energy Demand and Government Incentives Fueling Equipment Procurement

The growing global emphasis on renewable heating fuels has significantly accelerated demand for efficient firewood processing equipment. According to the International Energy Agency (IEA), solid biomass - including firewood - accounted for approximately 6% of global total energy supply in recent years, with residential and district heating applications representing the dominant consumption channel. In Europe, the Renewable Energy Directive (RED III) mandates increasing the share of renewables in heating and cooling, encouraging households and biomass fuel companies to scale up wood fuel production.

Countries such as Finland, Sweden, and Austria have seen sustained investment in firewood infrastructure due to their traditional reliance on wood heating. This regulatory environment is directly translating to the procurement of automated firewood processors that can process high volumes efficiently. Additionally, U.S. Department of Agriculture (USDA) forest management programs encourage commercial thinning and fuel reduction activities, generating raw log supply that supports firewood processor demand across the forestry contractor segment.

Mechanization Trend Replacing Manual Labor in Commercial Firewood Production

Rise in labor costs and declining rural workforce availability across developed markets is compelling commercial firewood producers and forestry contractors to invest in mechanized processing solutions. The average productivity of a hydraulic firewood processor can range from 3 to 10+ cords per hour, depending on configuration, vastly outperforming manual splitting methods. According to data from the Food and Agriculture Organization (FAO), global industrial roundwood production exceeded 2 billion cubic meters in recent years, indicating a broad raw material base available for firewood processing operations.

In North America, the commercial firewood market has witnessed consolidation, with large-scale producers deploying multi-station processor systems that incorporate automated conveyor feeds and log tables. These advancements reduce operational headcount while simultaneously improving throughput consistency, supporting the transition from small-scale to medium- and high-capacity processing equipment. Rechargeable Battery Systems have also begun emerging as power supplements in electric processor models, addressing off-grid deployment needs.

Restraints - High Capital Expenditure Limiting Adoption Among Small-Scale and Residential Users

The relatively high upfront cost of commercial-grade firewood processors represents a significant barrier to market penetration, particularly among residential users and small-scale operators. Industrial hydraulic and kinetic firewood processors can range from US$ 8,000 to over US$ 60,000 depending on capacity and configuration, making adoption economically prohibitive for budget-constrained buyers. This limits volume growth in the residential segment, and steers demand toward lower-margin entry-level models, compressing average selling prices and overall revenue per unit.

Equipment financing barriers further restrict adoption in emerging markets, where access to agricultural credit is limited and return-on-investment timelines are uncertain.

Seasonal Demand Fluctuations Creating Inventory and Revenue Management Challenges

The firewood processors market is inherently tied to seasonal heating cycles, resulting in concentrated procurement activity during late summer and early autumn months. This seasonal concentration strains supply chains and manufacturing schedules, often resulting in order backlogs or excess inventory at opposite points in the year. Manufacturers and distributors face elevated working capital requirements to manage inventory across low-demand periods.

According to U.S. Energy Information Administration (EIA) data, residential wood fuel consumption peaks dramatically in Q4 and Q1, directly aligning firewood processor demand with pre-season procurement windows. This cyclicality reduces year-round operational efficiency and limits consistent revenue recognition across fiscal periods.

Opportunities - Expansion of Biomass Fuel Supply Chains Creating High-Capacity Processor Demand

The rapid scaling of biomass fuel companies and district heating utilities across Europe and North America presents a substantial demand opportunity for high-capacity firewood processor manufacturers. The European Biomass Association (AEBIOM) reports that wood-based biomass heating has grown consistently, with installed district heating systems using solid biomass fuel expanding across Germany, Austria, and Scandinavia. These industrial end-users require processors capable of throughputs exceeding 6 cords per hour with automated log in-feed and split-wood discharge systems.

Biomass fuel companies, unlike residential users, operate year-round with consistent volume requirements, providing manufacturers with more stable demand pipelines. Firms that develop modular, high-throughput processor lines capable of integrating with conveyor and screening equipment will be favorably positioned to capture this growing industrial segment. The shift toward contracted biomass fuel supply also reduces revenue volatility, enhancing investment returns for processor end-users.

Electrification and Smart Technology Integration: Opening New Market Avenues

The integration of electric drivetrains and digital control systems in next-generation firewood processors represents a significant opportunity, particularly in regions with stringent emission regulations. Electric firewood processors are gaining traction in enclosed farm buildings and urban utility yards where diesel engine emissions are restricted. The adoption of rechargeable battery systems as auxiliary power for portable electric splitters is enabling deployment in remote forestry zones without grid access.

Furthermore, the incorporation of IoT-enabled monitoring - tracking cycle times, hydraulic pressure, and component wear - creates opportunities for predictive maintenance service models, enhancing total cost of ownership for commercial operators. According to Eurostat, over 41% of EU households used wood as a primary or secondary heating fuel as of recent survey data, underscoring the scale of downstream demand. Equipment manufacturers that align product development with electrification trends and connected features stand to differentiate strongly in an otherwise commoditized market.

Category-wise Analysis

Processor Type Insights

Within the processor type category, hydraulic firewood processors dominate the global market, accounting for approximately 42% of total market share in 2025. This dominance is underpinned by the versatility and power delivery of hydraulic splitting mechanisms, which can handle logs of varying diameter and wood density with consistent force output. Hydraulic processors are available across all capacity ranges, from compact residential units to large commercial machines, making them the most universally applicable processor type. Their compatibility with both PTO-driven and engine-powered configurations further extends their addressable market across diverse farm, forestry, and industrial end-uses.

The American Firewood & Forestry Association highlights that commercial firewood producers overwhelmingly favor hydraulic systems for their durability and low maintenance requirements under sustained operational cycles. Improvements in hydraulic valve technology and auto-cycle controls have also boosted efficiency, enabling processing speeds of up to 15-20 seconds per log on premium models, reinforcing the segment's dominance.

Kinetic firewood processors represent the fast-growing segment within the processor type category, projected to reach a CAGR of approximately 7.2% in the coming years. Kinetic processors use a flywheel-based mechanism that stores and releases rotational energy, enabling rapid single-stroke splitting at speeds significantly faster than hydraulic counterparts. The adoption among residential users and small commercial operators seeking high-speed performance without hydraulic complexity is driving this segment's exceptional growth trajectory.

Power Source Insights

The PTO driven processors segment leads the power source category, holding an estimated market share of approximately 35% in 2025. PTO (Power Take-Off) driven processors leverage the existing hydraulic and mechanical power infrastructure of agricultural tractors, making them a cost-effective choice for farm operators and forestry contractors who already own compatible tractor equipment.

The elimination of a separate engine reduces both capital expenditure and maintenance overhead, improving lifecycle economics. This segment benefits from deep penetration in the agricultural heartlands of North America, Germany, Poland, and Scandinavia, where tractor ownership rates are high.

According to Eurostat agricultural machinery statistics, farm tractor density in core EU markets exceeds 60 tractors per 1,000 hectares of agricultural land in several countries, representing a large installed base of compatible prime movers. The robustness and high-torque delivery of PTO connections also make this power source suitable for commercial-grade processing demands.

Electric firewood processors are the fastest-growing power source segment, anticipated to expand at a CAGR of 8.1% through 2033. Driven by stricter emission norms in indoor and urban settings, declining battery costs, and rising grid connectivity in rural areas, electric models are gaining rapid market acceptance. The integration of rechargeable battery systems is further extending their usability to off-grid applications, signaling a structural shift in power preferences.

Processing Capacity Insights

The medium capacity processors (3-6 Cords/Hour) segment commands the leading share within the Processing Capacity category, accounting for approximately 38% of the market in 2025. This segment occupies the strategic middle ground between low-output residential units and expensive high-capacity industrial machines, making it the preferred choice for commercial firewood producers, forestry contractors, and large farm operations.

Medium-capacity processors offer an optimal balance between cost, throughput, and operational flexibility, enabling operators to service both retail firewood markets and institutional biomass fuel buyers. Their compatibility with trailer-mounted configurations further expands deployment versatility across multiple worksites. Industry surveys indicate that medium-capacity machines achieve the best return on investment for operations producing between 500 and 2,000 cords annually, which describes the majority of commercial firewood businesses in developed markets.

High capacity processors (>6 Cords/Hour) constitute the fastest-growing processing capacity segment, projected to advance at a CAGR of 7.8% through 2033. Demand from biomass fuel companies, district heating suppliers, and large-scale forestry operations requiring sustained throughput is catalyzing adoption. Automation features, including auto-feed log tables and high-pressure hydraulic systems, further distinguish this segment's rapid growth trajectory.

End-user Insights

Among end-user categories, commercial firewood producers hold the dominant position, representing approximately 36% share in 2026. The commercial firewood production industry has undergone significant professionalization over the past decade, with larger operators investing in purpose-built processing lines to meet growing demand from retail fuel distributors, camping supply chains, and restaurant wood fuel buyers.

The U.S. Census Bureau and USDA Forest Service reports indicate that commercial wood fuel supply chains have expanded considerably in the Northeast and Pacific Northwest regions of the United States, mirroring similar trends in Scandinavia and Central Europe. Commercial producers require machines with high reliability, consistent split quality, and low downtime to maintain production schedules, all factors that favor investment in mid-to-high-grade hydraulic and PTO-driven processors. Their year-round operational requirements also generate stronger aftermarket parts and service demand.

Biomass fuel companies represent the fast-growing end-user segment, forecast to expand at a CAGR of 8.4% between 2026 and 2033. As energy utilities and district heating operators scale wood chip and split wood procurement, the demand for automated high-capacity processors grows correspondingly. Policy support from EU Renewable Energy Directives and U.S. Renewable Fuel Standards continues to accelerate this segment's ascent.

Regional Insights

North America Firewood Processors Trends

North America remains the leading regional market for firewood processors, underpinned by widespread residential wood heating traditions, extensive forestry contractor networks, and a well-developed commercial firewood supply chain. The United States and Canada collectively account for the majority of regional demand, driven by cold-climate demographics and robust farmstead and rural household ownership of log-splitting equipment. The U.S. Energy Information Administration (EIA) reports that approximately 2.5 million U.S. households rely on wood as their primary heating fuel, and millions more use it as a supplemental heat source, sustaining consistent consumer-grade processor demand.

On the commercial side, USDA Forest Service timber sale programs and fuel reduction initiatives in western states generate substantial log volumes available for firewood processing. The region benefits from a mature dealer and distribution network for agricultural and forestry machinery, supporting both new equipment sales and aftermarket service channels. Canada's forestry sector, one of the world's largest, also contributes meaningfully to demand for industrial and commercial-grade processors, particularly in British Columbia and Ontario.

- U.S.: The Epicenter of Commercial Firewood Processing Equipment Demand

The United States dominates the North American firewood processors market, accounting for approximately 78-80% of regional revenue in 2026. The country's vast and diverse geography, spanning cold northern states and high-elevation western regions, sustains strong residential and commercial demand for wood heating fuels.

The U.S. commercial firewood industry is particularly well-developed, with concentrated production regions in the Northeast, Midwest, and Pacific Northwest. The domestic market is growing at a CAGR of approximately 5.0%, broadly in line with the North America regional average. Government forestry management programs, timber processing subsidies, and robust agricultural equipment financing channels collectively support the procurement of mid-to-high-capacity processors. The country's extensive tractor ownership base also reinforces the dominance of PTO-driven processor configurations.

Europe Firewood Processors Trends

Europe represents the second-largest regional market, with strong demand driven by the continent's deep-rooted wood heating culture and accelerating policy mandates for renewable energy adoption. Northern and Central European countries, including Germany, Finland, Sweden, Austria, and Poland, are among the world's highest per-capita consumers of firewood and wood pellets for residential heating. The European Commission's Fit for 55 package and RED III directive actively incentivize biomass heating deployment, creating tailored demand for commercial firewood processing infrastructure.

The European market also benefits from growing forestry contractor mechanization and EU-funded rural development programs that support agricultural machinery investment. Eastern European countries, notably Poland, Romania, and the Czech Republic, are emerging as dynamic growth markets within the region, driven by relatively lower penetration of mechanized firewood processing and expanding commercial wood fuel supply sectors.

- Germany: Leading European Market for High-Efficiency Firewood Processing Equipment

Germany holds the largest share within the European firewood processors market, representing approximately 22-24% of regional revenue in 2025 and reaching a CAGR of approximately 5.3%. The country's commitment to the Energiewende energy transition program, which emphasizes renewable heating sources, including solid biomass, underpins sustained demand for firewood processing infrastructure. Germany's large agricultural sector and dense network of forestry cooperatives provide a strong installed base for both PTO-driven and standalone processor models.

- U.K.: Growing Residential and Rural Firewood Processor Adoption Amid Energy Transition

The United Kingdom accounts for approximately 12% share, with the firewood processors segment growing at approximately 4.8% CAGR. The U.K.'s Renewable Heat Incentive (RHI) program historically supported biomass heating adoption, creating downstream firewood and wood chip demand. Post-2022 energy market volatility has further accelerated interest in domestic wood heating solutions, driving equipment procurement across rural residential and small commercial segments.

- France: Expansion in Rural and Agricultural Firewood Processing Capacity

France is likely to represent approximately 15% share in 2026. The country has a long-standing tradition of wood fuel use in rural communities, and the French Environment and Energy Management Agency (ADEME) has consistently promoted solid biomass as a priority renewable heating fuel. France's large agricultural estate and rural property ownership create a strong base for farm-use firewood processors, particularly in PTO-driven configurations.

- Italy: Mediterranean Firewood Market Expanding Through Commercial and Agritourism Channels

Italy accounts for an estimated 11% share in 2026 at a CAGR of approximately 4.6% in the forecast period. Italian demand is characterized by strong rural residential consumption of firewood for traditional wood-burning stoves (stufe) and fireplaces. The agritourism sector, which uses outdoor fireplaces and pizza ovens extensively, also contributes to commercial firewood demand. Italian manufacturers including Posch (Austrian-Italian market presence) and domestic brands supply regionally adapted equipment suited to Mediterranean log species and farm scales.

Asia Pacific Firewood Processors Trends

The Asia Pacific region, while smaller in absolute terms compared to North America and Europe, is emerging as a dynamic growth market driven by expanding commercial forestry activities, government-supported biomass energy programs, and rising mechanization in agricultural and forestry sectors. China, Japan, and Australia are among the key contributors to regional demand, with each market presenting distinct growth catalysts.

In China, the government's push toward rural biomass energy development under the 14th Five-Year Plan for energy has spurred interest in wood fuel processing equipment. Japan's managed forestry sector, supported by Japan's Forest Agency subsidy programs, generates demand from forestry contractors deploying small-to-medium-capacity processors. Australia's farm and rural residential sector presents growing demand, particularly in cold southern states. The region is also characterized by lower average unit prices due to domestic manufacturing capabilities, particularly in China.

- China: Emerging Powerhouse for Biomass-Driven Firewood Processor Manufacturing and Demand

China accounts for approximately 42% of Asia Pacific firewood processors market revenue in 2025 and is growing at a positive CAGR. The country's dual role as both a major manufacturer and consumer of firewood processing equipment positions it uniquely within the global landscape. Government biomass energy promotion, combined with expanding rural woodlot management, is driving procurement of mid-range hydraulic processors. Chinese manufacturers are also increasingly exporting competitively priced units to Southeast Asia and Latin America.

- India: Rapid Agricultural Mechanization Driving Firewood Processor Market Entry

India represents approximately 15% of the Asia Pacific market and is expected to reach a CAGR of 7.1% by 2033. Rise in agricultural income, government subsidy schemes for farm machinery under the Sub-Mission on Agricultural Mechanization (SMAM), and expanding commercial wood fuel supply for brick kilns and hospitality sectors are key drivers. The Indian market is primarily served by small-to-medium-capacity processors, with adoption concentrated in Punjab, Haryana, and Northeastern states.

- South Korea: Forestry Modernization Accelerating High-Efficiency Processor Adoption

South Korea holds an estimated 10% of the Asia Pacific market share, with a CAGR projected at 6.2%. The Korea Forest Service's active forest thinning and biomass energy programs drive demand from forestry contractors deploying commercial-grade firewood processors. South Korea's relatively advanced agricultural mechanization rates and availability of equipment financing also support the adoption of mid-to-high-capacity processor models.

Competitive Landscape

The global firewood processors market exhibits a moderately fragmented competitive structure, with a mix of established European and North American manufacturers alongside emerging Asian producers. Leading firms such as Japa, Posch, Pilkemaster, Uniforest, and CORD KING command significant brand recognition and dealer network advantages in their respective regional markets.

Market leaders differentiate through processing speed, hydraulic system engineering, and after-sales service capabilities. Strategic trends include product line expansion into electric and battery-assisted models, geographic distribution partnerships, and integration of auto-cycle controls for operational efficiency. Emerging competitors from China are intensifying price competition, prompting established players to focus on premium performance, reliability warranties, and value-added service models to defend margin positions.

Key Developments:

- In March 2026, Timberwolf Firewood Processing Equipment launched the Pro-LP XL and Pro-LP XL Diesel firewood processors, featuring enhanced size, performance, and processing capability while maintaining durability and operational simplicity.

- In February 2024, Hakki Pilke launched mobile versions of its Raven 33, Falcon 37, and 38 Pro firewood processors, offering towable solutions designed to improve portability, operational flexibility, and customer convenience.

- January 2024: Posch GmbH (Austria) launched the updated SplitMaster 40 T hydraulic firewood processor series, featuring an enhanced auto-cycle control system and increased log table capacity, targeting commercial firewood producers in Central Europe.

- March 2024: Pilkemaster (Finland) expanded its dealer network into Poland and Czech Republic, capitalizing on the demand for mechanized firewood processing equipment in Eastern European markets with new PTO-driven and tractor-mounted processor models.

- September 2023: CORD KING (Canada) introduced the CS-36 Firewood Processor with a fully automated hydraulic-electric hybrid drive system, aimed at commercial firewood operations in North America seeking reduced fuel consumption and indoor operability.

Companies Covered in Firewood Processors Market

- Cord King

- Multitek

- Hakki Pilke

- Posch

- Tajfun

- Pilkemaster

- Japa

- Balfor

- Eastonmade

- DYNA Products

- Fuelwood

- Rabaud

- Hud-Son Forest Equipment

- Wallenstein

- Uniforest

Frequently Asked Questions

The global Firewood Processors market is projected to reach US$ 631.3 Mn by 2033, growing at a CAGR of 5.5% from an estimated US$ 434.0 Mn in 2026. This growth is underpinned by rising biomass energy demand, commercial firewood production mechanization, and increasing adoption of high-capacity processing equipment by biomass fuel companies and forestry contractors worldwide.

The primary demand drivers include growing biomass and renewable heating fuel mandates under regulatory frameworks such as the EU Renewable Energy Directive (RED III), rising labor costs, accelerating mechanization in commercial firewood production, and expanding government forestry management programs generating raw log supply. The shift toward automated hydraulic and kinetic processor systems also enhances operational efficiency, further stimulating market demand.

Hydraulic firewood processors dominate the processor type category, accounting for approximately 42% of global market share in 2025. Their dominance is attributed to wide applicability across residential, commercial, and industrial end-uses, compatibility with multiple power source configurations, consistent force output for varied log diameters, and strong durability credentials supported by commercial operator preferences across North America and Europe.

North America is the leading regional market, holding approximately 38% of global revenue in 2025. The region benefits from widespread residential wood heating practices, a mature commercial firewood supply chain, high tractor ownership rates supporting PTO-driven processor adoption, and active USDA forest management programs generating log supply. The United States accounts for the majority of North American demand, growing at approximately 5.0% CAGR.

A key market opportunity lies in the electrification and smart technology integration of firewood processors. The growing adoption of electric drivetrains, rechargeable battery systems enabling off-grid deployment, and IoT-based operational monitoring creates significant differentiation potential for manufacturers. This aligns with emission regulations in enclosed workspaces and the broader global decarbonization trend, opening premium product segments with higher margins and service revenue potential.

Leading companies in the global Firewood Processors market include Posch GmbH (Austria), Pilkemaster Oy (Finland), CORD KING (Canada), Japa Oy (Finland), Uniforest d.o.o. (Slovenia), Tajfun d.o.o. (Slovenia), Hakki Pilke (Finland), Palax (Laitilan Metalli Oy), Multitek, Dyna Products, Wood-Mizer, Rabaud SAS (France), Boss Log Splitters, and Champion Power Equipment, among others. These firms compete on processing speed, hydraulic engineering quality, product range breadth, and after-sales service capabilities.