- Pharmaceuticals

- BRCA Mutations Treatment Market

BRCA Mutations Treatment Market Size, Share, and Growth Forecast, 2026 - 2033

BRCA Mutations Treatment Market by Treatment Type (Targeted Therapies, Immunotherapy, Others), Drug Class (PARP Inhibitors, Others), Indication (Breast Cancer, Others), Administration Route (Oral, Intravenous, Subcutaneous), and Regional Analysis 2026 - 2033

BRCA Mutations Treatment Market Size and Trends Analysis

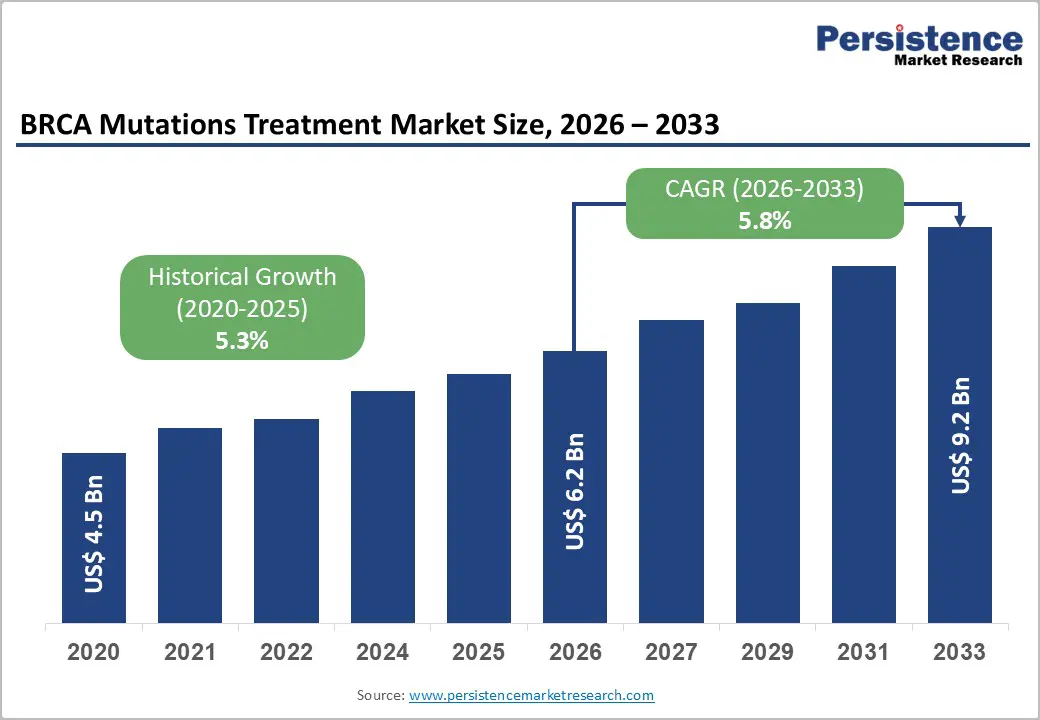

The global BRCA mutations treatment market size is likely to be valued at US$6.2 billion in 2026 and is expected to reach US$9.2 billion by 2033, growing at a CAGR of 5.8% during the forecast period from 2026 to 2033, driven by rising clinical emphasis on precision oncology and molecular diagnostics.

Advancements in genomic sequencing enable practitioners to identify specific hereditary risks within patient populations. Rising incidence of BRCA-associated cancers drives procurement of targeted interventions across oncology networks. Precision diagnostics expand eligible patient pools, while regulatory approvals accelerate therapy adoption. Manufacturers continue to invest in novel targeted therapies to improve patient survival rates. The increasing prevalence of breast and ovarian malignancies reinforces the demand for specialized treatments.

Key Industry Highlights:

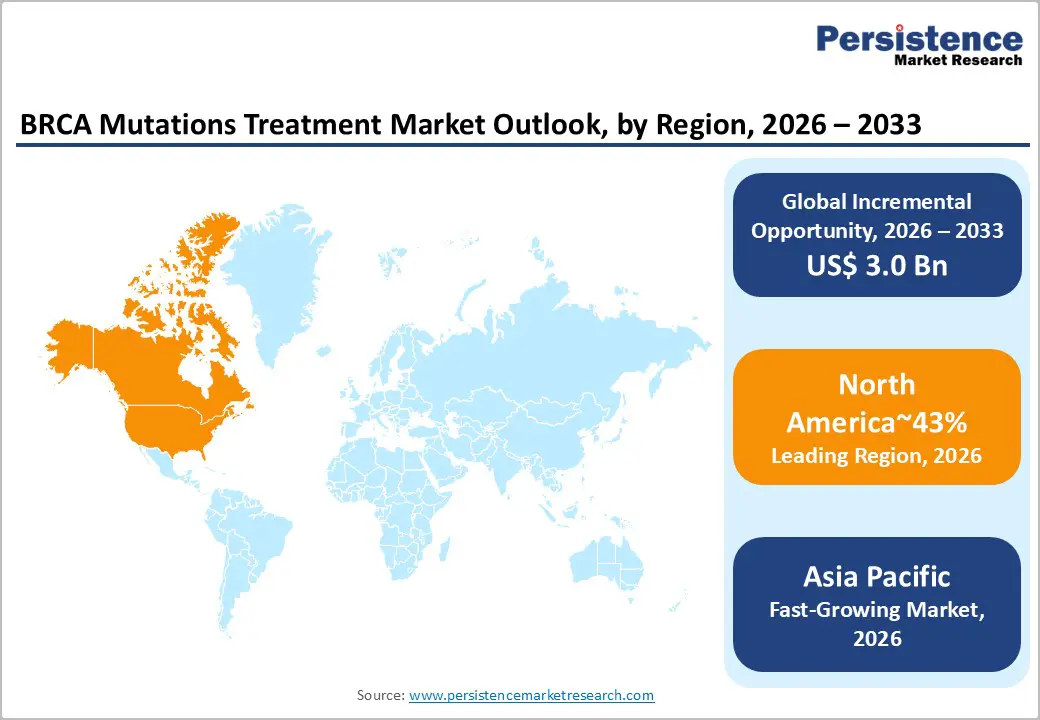

- Leading Region: North America is projected to lead, accounting for approximately 43% share in 2026, supported by robust healthcare infrastructure, high research investment, and early adoption of novel therapies.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest, driven by expanding healthcare access, rising awareness of genetic testing, and increasing middle-class populations.

- Leading Treatment Type: Targeted therapies are expected to lead, accounting for approximately 63% share in 2026, anchored by high clinical efficacy and reduced systemic toxicity compared to conventional chemotherapy.

- Leading Indication: Breast cancer is projected to dominate, holding approximately 80% share in 2026, driven by high disease incidence and established screening protocols for BRCA mutations.

| Key Insights | Details |

|---|---|

| BRCA Mutations Treatment Market Size (2026E) | US$6.2 Bn |

| Market Value Forecast (2033F) | US$9.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

DRO Analysis

Driver Analysis - Rising Integration of Precision Medicine Frameworks

The transition toward personalized medicine is restructuring therapeutic strategies across hereditary oncology treatment landscapes globally. Clinical decision-making increasingly prioritizes molecular profiling to align interventions with patient-specific genetic characteristics. This structural shift compels healthcare providers to adopt advanced diagnostic tools and targeted therapeutic protocols. Enhanced understanding of DNA repair pathways accelerates the development of biologics addressing precise oncogenic mechanisms. Regulatory frameworks support integration of companion diagnostics within treatment approval and reimbursement pathways. Cost structures evolve toward high-value targeted therapies and genomic testing infrastructure within oncology systems. These dynamics collectively expand the adoption of precision medicine within standardized clinical practice.

AstraZeneca with Lynparza exemplifies targeting of DNA damage response pathways across BRCA-associated malignancies. This therapeutic approach establishes efficacy benchmarks within precision oncology treatment protocols. Clinicians increasingly utilize such agents to disrupt tumor replication through pathway-specific biochemical interactions. Integration of molecular diagnostics enhances treatment accuracy and patient outcome predictability. Oncology care pathways shift toward personalized regimens supported by validated genomic insights. These developments reinforce the sustained expansion of targeted therapies within evolving precision medicine ecosystems.

Genetic Screening Proliferation in Precision Oncology

Genetic screening uptake increases due to sustained awareness initiatives and expanded access across healthcare systems globally. Population-based testing identifies mutation carriers earlier, enlarging addressable cohorts for targeted therapeutic regimens. Early detection strengthens preventive strategies and informs timely clinical intervention pathways within oncology care. These dynamic supports sustained consumption patterns aligned with precision medicine treatment frameworks. Regulatory bodies increasingly endorse screening programs linked to measurable clinical outcome improvements. Cost structures evolve toward scalable genomic testing and integrated diagnostic service delivery models. These factors collectively reinforce long-term expansion of precision-driven oncology markets.

Clovis Oncology with Rubraca aligns closely with screening-driven workflows integrated within modern oncology treatment pathways. Providers incorporate genetic results into structured clinical decision trees, accelerating therapy initiation processes. Diagnostic integration enhances treatment precision and improves patient stratification across targeted therapy segments. Manufacturers utilize real-world screening data to refine product positioning and therapeutic differentiation strategies. Healthcare systems increasingly embed genomic insights within standardized oncology protocols and reimbursement frameworks. These interdependencies strengthen sustained adoption of targeted treatments within expanding precision oncology ecosystems.

Restraint Analysis - Emergence of Therapeutic Resistance Mechanisms in Oncology

Prolonged exposure to targeted therapies induces adaptive mutations within tumor cells, reducing sustained treatment efficacy. These resistance mechanisms alter signaling pathways, enabling malignant cells to bypass therapeutic inhibition strategies. Clinical management becomes increasingly complex as standard regimens lose effectiveness over extended treatment durations. The development of next-generation inhibitors and salvage therapies introduces additional cost and research burdens. Healthcare systems allocate greater resources toward monitoring, combination therapies, and sequential treatment planning. Regulatory expectations emphasize continuous evidence generation addressing resistance pathways and long-term clinical outcomes. These factors collectively constrain the durability of targeted therapies within evolving oncology treatment landscapes.

AstraZeneca, with Lynparza, undergoes an ongoing investigation to address secondary mutations circumventing PARP inhibition mechanisms. Research initiatives focus on overcoming resistance through combination approaches and novel pathway targeting strategies. Manufacturers must sustain innovation cycles to preserve the clinical relevance of established therapeutic portfolios. Resistance patterns necessitate continuous clinical trials and biomarker refinement within precision oncology frameworks. Treatment pathways increasingly incorporate adaptive strategies to counter the biological evolution of tumors. These dynamics intensify research expenditure and complicate long-term management of targeted cancer therapies.

Elevated Economic Burden of Specialized Therapies

The high costs associated with developing and manufacturing biological therapies creates persistent pricing pressures globally. Targeted agents command premium pricing due to complex production processes and specialized clinical validation requirements. Public healthcare systems face budgetary constraints that restrict reimbursement coverage for high-cost oncology treatments. Limited insurance support increases out-of-pocket expenses, reducing patient adherence and delaying treatment initiation. Cost sensitivity within emerging markets further constrains access to advanced therapeutic options. Regulatory bodies intensify value-based assessments linking pricing approvals with demonstrated clinical and economic outcomes. These financial barriers collectively limit widespread adoption of modern precision oncology interventions.

Novartis, with Piqray, encounters pricing scrutiny across multiple healthcare systems, evaluating cost-effectiveness and reimbursement viability. Healthcare providers in cost-sensitive environments moderate adoption due to constrained institutional budgets and funding allocations. Reimbursement negotiations with health technology assessment bodies introduce delays in therapy accessibility across regions. Pricing pressures influence procurement strategies and treatment prioritization within oncology care frameworks. Manufacturers must balance innovation costs with affordability expectations to maintain market competitiveness. These dynamics constrain penetration of specialized therapies within developing and resource-limited healthcare ecosystems.

Opportunity Analysis - Integration of Artificial Intelligence in Patient Selection

Artificial intelligence transforms the analysis of complex genomic datasets for clinical decision-making within oncology treatment systems. Machine learning algorithms detect subtle correlations in patient profiles, enabling the prediction of optimal therapeutic responses. This capability advances the development of precise companion diagnostics aligned with targeted treatment strategies. AI-driven platforms reduce diagnostic timelines and accelerate initiation of personalized oncology care pathways. Regulatory frameworks increasingly recognize algorithm-supported diagnostics within precision medicine validation processes. Cost structures evolve toward cloud infrastructure, data integration, and advanced analytics deployment across healthcare networks. These dynamics collectively enhance clinical outcomes through refined patient selection and optimized therapeutic alignment.

Roche, with FoundationOne CDx, utilizes advanced data processing to align patients with appropriate targeted therapies. Integration of digital analytics improves the accuracy of treatment selection across genomically defined cancer populations. Healthcare providers incorporate such platforms to streamline precision medicine workflows within hospital systems. Data-driven insights strengthen clinical decision frameworks and enhance treatment success probabilities. Interoperable systems enable seamless coordination across diagnostic, therapeutic, and monitoring stages of care. These developments reinforce the expansion of artificial intelligence applications within precision oncology ecosystems.

Combination Therapy Synergies in Precision Oncology

Combination regimens integrating PARP inhibition with immunotherapy address resistance pathways across advanced oncology treatment settings. Synergistic mechanisms enhance response durability and deepen therapeutic efficacy beyond outcomes achieved through monotherapy approaches. This evolution expands treatment sequencing options, enabling multi-line strategies within precision-driven clinical frameworks. Regulatory pathways increasingly support combination trials demonstrating additive or complementary biological effects. Healthcare systems incorporate such regimens to optimize outcomes in refractory and high-risk patient cohorts. Cost structures adjust toward complex combination protocols and integrated biomarker-guided treatment planning. These dynamics collectively strengthen the clinical and commercial relevance of multi-mechanism oncology therapies.

Merck & Co., with Keytruda, advances combination trials alongside PARP inhibitors targeting unmet therapeutic needs in resistant cancer populations. Strategic clinical alignments enhance efficacy signals through coordinated targeting of immune and DNA repair pathways. Providers anticipate expanded utility of such regimens within refractory and previously treated patient segments. Trial outcomes inform integration into standardized treatment protocols across precision oncology settings. Collaborative development models accelerate validation of combination-based therapeutic strategies. These interdependencies reinforce the adoption of synergistic treatment approaches within evolving oncology care paradigms.

Category-wise Analysis

Treatment Type Insights

Targeted therapies are expected to lead the market, accounting for approximately 63% share in 2026, underpinned by high specificity toward malignant cells with deficient DNA repair mechanisms. These biological agents exploit the concept of synthetic lethality to induce tumor cell death while sparing healthy tissues. Adoption remains anchored in the superior clinical profiles of these drugs compared to conventional cytotoxic regimens. Healthcare providers prioritize these interventions to minimize systemic side effects and improve long-term patient survival outcomes. Ongoing refinements in molecular targeting further strengthen the utilization of these specialized pharmaceutical products. This structural alignment between clinical efficacy and patient safety sustains the segment's leadership within the global oncology landscape.

Immunotherapy is forecast to be the fastest-growing segment, driven by increasing clinical evidence supporting its synergistic potential with targeted agents. Modern oncology workflows are shifting toward activating the host's immune system to recognize and eliminate genetically unstable cancer cells. Merck with Keytruda and Bristol Myers Squibb with Opdivo exemplify this transition toward durable immune-mediated clinical responses. Integration of these agents into frontline and maintenance settings supports improved remission rates across various patient populations. As researchers uncover new biomarkers for immune sensitivity, these treatments are gaining traction across evolving cancer care ecosystems.

Indication Insights

Breast cancer is anticipated to dominate the market, accounting for approximately 80% share in 2026, anchored by high global incidence rates and established genetic testing protocols. Screening for BRCA1 and BRCA2 mutations is standard practice for many patients diagnosed with early or advanced mammary malignancies. This established clinical pathway ensures a consistent flow of eligible candidates for specialized targeted therapies. Healthcare systems allocate significant resources toward treating this indication due to its high socioeconomic impact and prevalence. Novartis with Kisqali and Eli Lilly with Verzenio are frequently integrated into these established treatment paradigms. This convergence of high patient volume and standardized clinical care reinforces the segment's market dominance.

Prostate cancer is anticipated to be the fastest-growing segment, driven by the increasing identification of BRCA mutations in metastatic castration-resistant cases. Recent clinical breakthroughs have validated the use of targeted agents for men who have exhausted traditional hormonal and chemotherapy options. AstraZeneca with Lynparza and Pfizer with Talzenna have obtained regulatory clearances for these specific male-centric oncological applications. This emerging clinical focus is shifting the market toward broader gender-inclusive therapeutic strategies in precision medicine. As awareness of hereditary risk in men increases, screening and subsequent treatment volumes are expected to rise. This new application area is set to expand the market's reach into previously untapped patient segments.

Regional Insights

North America BRCA Mutations Treatment Market Trends

North America is expected to remain the leading regional market, accounting for approximately 43% share in 2026, supported by an advanced clinical research environment and high consumer health awareness. The region's dominance is anchored in the widespread availability of high-throughput genomic sequencing and specialized oncology centers. Healthcare providers emphasize the integration of molecular diagnostics into standard care for breast and ovarian cancers. Robust insurance coverage for targeted therapies further reinforces the high utilization of modern pharmaceutical agents. Secondary demand from expanded indications in prostate cancer is anticipated to broaden the region's overall therapeutic footprint.

The U.S. is expected to anchor regional momentum through sustained investments in precision oncology programs and genomic data integration. Federal initiatives promoting cancer moonshot goals are anticipated to accelerate the development of next-generation targeted treatments. AstraZeneca with Lynparza is expected to benefit from high prescription volumes across major hospital networks in this country. Regulatory streamlining for companion diagnostics is projected to increase the pace of therapeutic adoption among oncology specialists. Sustained focus on improving patient access to clinical trials continues to strengthen the domestic market for advanced BRCA treatments.

Europe BRCA Mutations Treatment Market Trends

Europe is expected to remain a mature and structurally stable regional market, with demand primarily anchored in established clinical guidelines and centralized healthcare procurement. The regional market is supported by strong public health systems that provide broad access to essential cancer screenings and treatments. European regulatory bodies are set to maintain rigorous standards for the safety and efficacy of targeted biological products. Innovation is likely to be driven by a focus on cost-effectiveness and long-term patient survival outcomes. Strategic partnerships between academic institutions and pharmaceutical vendors sustain a high level of clinical excellence across the region.

Germany is expected to anchor European demand through its highly efficient healthcare infrastructure and significant focus on molecular medicine. The national health system's emphasis on evidence-based treatment protocols is anticipated to drive the adoption of verified PARP inhibitors. Pfizer with Talzenna is positioned to capture demand within specialized breast cancer centers across the country. Government-led research clusters are projected to foster collaborations aimed at overcoming therapeutic resistance in hereditary cancers. Continuous investment in digital health records is expected to enhance the identification and management of high-risk genetic populations.

Asia Pacific BRCA Mutations Treatment Market Trends

Asia Pacific is expected to register the fastest growth trajectory, as expanding healthcare infrastructure and increasing investments in biotechnology accelerate market expansion. The region's growth is anchored in a large patient pool and rising clinical awareness regarding the benefits of genetic screening. Manufacturers are increasingly targeting this region to conduct clinical trials and establish localized manufacturing capabilities. Improving economic conditions are likely to increase the affordability of targeted therapies for urban populations.

India anchors regional momentum through rising cancer registries and NGS adoption. Government screening programs identify carriers, spurring therapy demand. Pfizer with Talzenna aligns with these shifts, supporting volume ramps. Investments position the market for rapid scaling. China is expected to anchor regional growth through comprehensive healthcare reforms and the rapid expansion of its domestic biotechnology sector. National policies aimed at reducing the burden of chronic diseases are anticipated to prioritize the adoption of targeted cancer treatments. Increasing local competition from Chinese biotech firms is projected to enhance the affordability of targeted agents for the general population. Strategic focus on building specialized oncology hospitals is expected to increase the delivery capacity for advanced biological therapies.

Competitive Landscape

The global BRCA mutations treatment market is moderately consolidated, with leadership shared between global rendering conglomerates and regional processing operators. This structure reflects capital-intensive infrastructure requirements alongside localized raw material collection networks supporting distributed production systems. Leading participants influence procurement through advanced drying technologies, pathogen control standards, and consistent nutrient profiling across feed applications. Their scale enables stable supply relationships with major meat processors and commercial feed manufacturers globally. Established players such as Darling Ingredients, Tyson Foods, and Saria Group set benchmarks for traceability and operational reliability. Their integrated capabilities reinforce quality assurance and regulatory compliance across diverse livestock and aquaculture markets.

Competitive positioning reflects vertical differentiation between premium spray-dried products and value-oriented bulk meal offerings for livestock nutrition. Premium providers emphasize enhanced protein bioavailability and functional benefits, while value players prioritize cost efficiency and volume scalability. Companies such as APC advance specialized formulations targeting immunological performance and feed efficiency improvements. Industry dynamics include consolidation of regional rendering assets to secure raw material access and optimize processing capacity. Platform evolution increasingly integrates digital traceability and sustainability metrics aligned with regulatory requirements. Forward-looking strategies prioritize environmental efficiency and supply chain transparency across global animal nutrition ecosystems.

Key Industry Developments:

- In April 2026, AstraZeneca announced high-level results from the EMERALD-3 trial evaluating combinations of Imfinzi and targeted agents in gastrointestinal cancers. Expanding indications for these drugs into broader solid tumor categories (often including BRCA carriers) allows for massive cross-indication revenue growth.

- In March 2026, Pfizer reported positive phase III results from the TALAPRO-3 trial for Talzenna plus Xtandi in metastatic prostate cancer. The trial met its primary endpoint of radiographic progression-free survival, potentially expanding Pfizer's market share in the early-stage metastatic setting.

- In December 2025, the FDA converted the accelerated approval of Rubraca (rucaparib) to full (regular) approval for chemotherapy-naïve patients with BRCA-mutated mCRPC. Full approval validates the drug's long-term efficacy and safety, solidifying its competitive position against other PARP inhibitors such as olaparib in the prostate cancer space.

Companies Covered in BRCA Mutations Treatment Market

- AstraZeneca PLC

- Pfizer Inc.

- F. Hoffmann-La Roche Ltd

- Novartis AG

- Merck & Co., Inc.

- GlaxoSmithKline (GSK) PLC

- Bristol Myers Squibb

- Eli Lilly and Company

- Gilead Sciences, Inc.

- Amgen Inc.

- AbbVie

- Clovis Oncology, Inc.

- BeiGene

- Johnson & Johnson

- Exelixis

- Myriad Genetics, Inc.

Frequently Asked Questions

The global BRCA mutations treatment market is projected to be valued at US$6.2 billion in 2026 and is expected to reach US$9.2 billion by 2033, driven by increasing adoption of precision oncology, rising genetic screening rates, and expanding use of targeted therapies across hereditary cancer indications.

The integration of molecular diagnostics and genomic profiling is a primary driver, as it enables the identification of BRCA mutations and supports targeted therapeutic interventions such as PARP inhibitors, improving treatment specificity, clinical outcomes, and optimizing patient stratification across oncology care pathways.

The BRCA mutations treatment market is forecast to grow at a CAGR of 5.8% from 2026 to 2033, reflecting sustained demand for targeted therapies, increasing awareness of hereditary cancers, and continuous advancements in biomarker-driven treatment strategies.

North America is the leading regional market, accounting for approximately 43% share in 2026, supported by advanced healthcare infrastructure, strong reimbursement systems, widespread adoption of genetic testing, and high investment in oncology research and precision medicine initiatives.

The BRCA mutations treatment market is moderately consolidated, with key players including AstraZeneca, Pfizer, Roche, Hoffmann-La Roche Ltd, Novartis, and Merck.