- Specialty & Fine Chemicals

- Antiscalants and Dispersants Market

Antiscalants and Dispersants Market Size, Share, and Growth Forecast, 2026 - 2033

Antiscalants and Dispersants Markets by Chemical Substance Type (Phosphonates, Carboxylates Acid, Sulfonated Polymers, Others), Nature (Synthetic, Bio-based), End-user Industry (Oil & Gas, Water Treatment, Power Generation), and Regional Analysis 2026 - 2033

Antiscalants and Dispersants Market Size and Trends Analysis

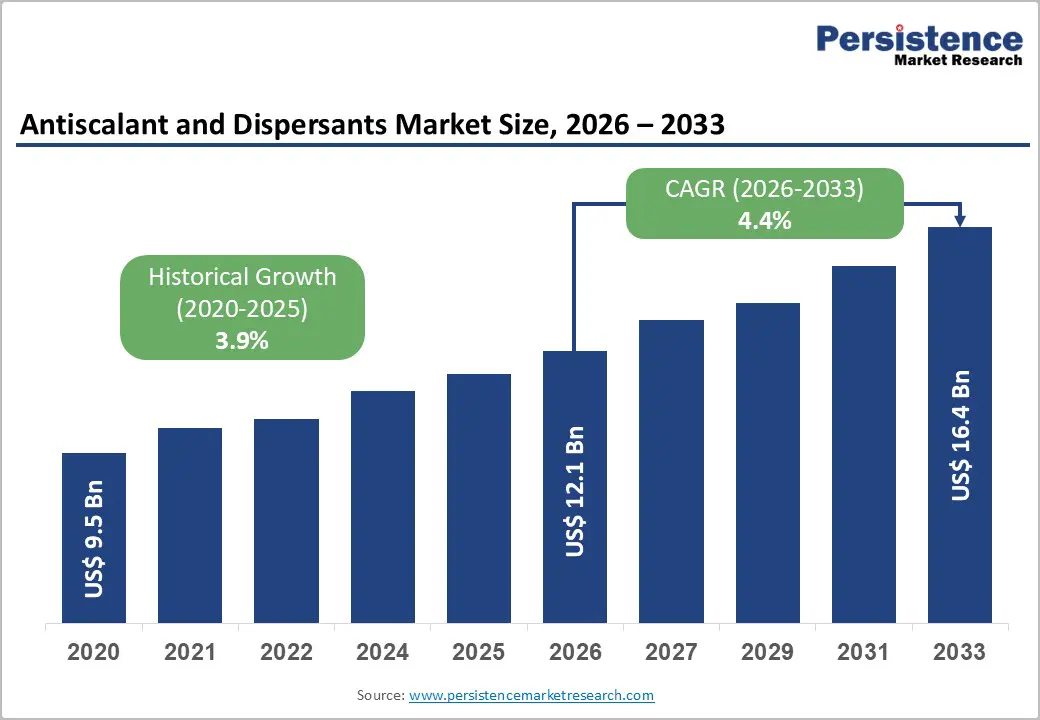

The global antiscalants and dispersants market size is likely to be valued at US$12.1 billion in 2026 and is expected to reach US$16.4 billion by 2033, growing at a CAGR of 4.4% during the forecast period from 2026 to 2033, driven by the increasing demand for efficient scale inhibition in the oil & gas industry, particularly in enhanced oil recovery (EOR) processes, as well as the rapid expansion of desalination infrastructure in water-stressed regions. Tightening environmental regulations are accelerating the adoption of sulfonated polymers and bio-based chemistries, further supporting steady market growth through improved operational efficiency.

Key Industry Highlights:

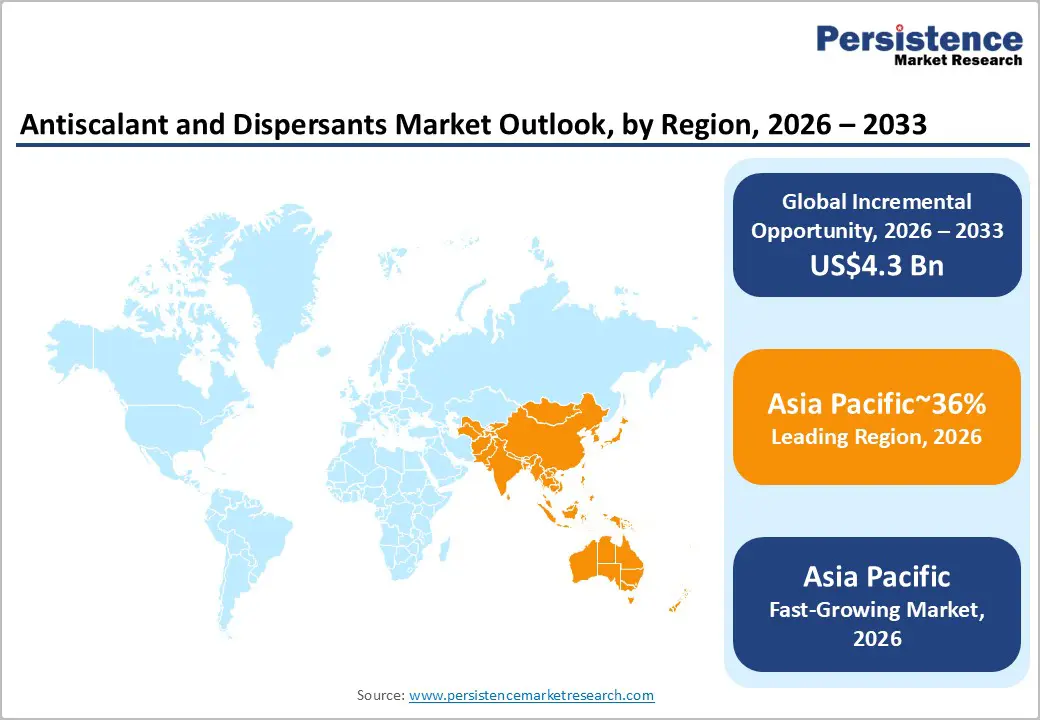

- Leading Region: Asia Pacific is projected to lead due to large-scale industrialization, rapid expansion of desalination capacity, and strong upstream oil & gas activity, accounting for approximately 36% share.

- Fastest-growing Region: Asia Pacific is anticipated to grow fastest due to accelerating industrial output, policy support for wastewater recycling, and the rising deployment of large-scale desalination plants.

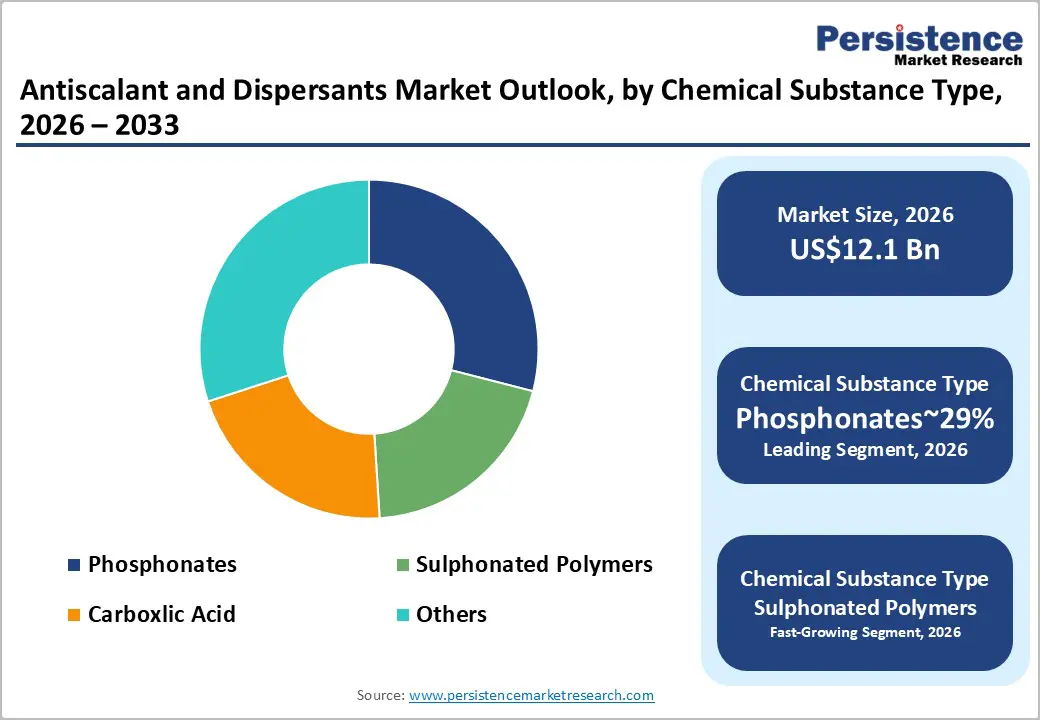

- Leading Chemical Substance: Phosphonates are expected to lead, accounting for approximately 29%, supported by proven scale inhibition efficiency, strong compatibility in high-pressure oilfield systems, and widespread industrial acceptance.

- Leading End-user Industry: Oil & gas is projected to dominate, holding approximately 30%, driven by extensive application in enhanced oil recovery, pipeline scale control, and offshore production systems.

| Key Insights | Details |

|---|---|

|

Antiscalants and Dispersants Market Size (2026E) |

US$12.1 Bn |

|

Market Value Forecast (2033F) |

US$16.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Increasing Industrial Water Demand

Escalating industrial water consumption is structurally reinforcing demand for antiscalants and dispersants across process-intensive sectors. Manufacturing expansion in power generation, refining, chemicals, and metals intensifies water throughput requirements. Higher recirculation rates within cooling and boiler systems elevate scaling and fouling risks. This operational stress increases chemical treatment intensity to preserve heat transfer efficiency. Desalination and zero liquid discharge systems further heighten concentrate management complexity. Advanced membrane installations remain vulnerable to mineral precipitation and particulate deposition. Regulatory scrutiny over water discharge quality compels tighter process control regimes. Consequently, chemical dosing strategies become embedded within core plant reliability frameworks.

Sustained water demand reshapes procurement toward performance-optimized treatment chemistries. Facilities prioritize formulations compatible with high salinity and variable feedwater compositions. Technology evolution in membrane materials necessitates tailored antiscalant chemistries and dispersion stability. Compliance obligations around effluent quality increase monitoring sophistication and treatment consistency. These requirements elevate formulation complexity and quality assurance burdens for suppliers. Cost structures shift toward specialty additives with higher performance thresholds. Margin realization increasingly depends on technical differentiation and application-specific customization. Collectively, industrial water intensity structurally anchors recurring chemical consumption across regulated infrastructures.

Escalating Water Scarcity and Desalination Projects

Escalating freshwater scarcity is accelerating structural investment in large-scale desalination infrastructure globally. Reverse osmosis and thermal desalination systems operate under extreme concentration gradients. Such operating conditions intensify mineral precipitation and membrane fouling risks. Calcium carbonate and sulfate scaling directly compromise flux stability and energy efficiency. Antiscalants, therefore, become process-critical inputs within desalination treatment trains. Their functional role extends beyond protection toward sustaining asset lifecycle performance. Regulatory mandates on potable water quality reinforce stringent process control requirements. Consequently, desalination expansion structurally elevates recurring chemical consumption across water utilities.

Expanding desalination capacity reshapes demand toward high-performance scale inhibitors. Plants in water-stressed regions deploy advanced membranes requiring formulation compatibility and dosing precision. Technology evolution toward higher recovery rates increases concentrate saturation thresholds. This amplifies reliance on predictive monitoring and tailored antiscalant chemistries. Procurement frameworks prioritize reliability and lifecycle cost containment over commodity pricing. Regulatory oversight in strategic water markets tightens discharge and brine management compliance. These dynamics embed antiscalants within critical infrastructure cost structures. Desalination growth thus anchors stable, volume-driven demand across regulated water ecosystems.

Barrier Analysis - Availability of Substitutes

The availability of substitute treatment approaches constrains the structural expansion of antiscalants and dispersant demand. Mechanical descaling, magnetic treatment devices, and physical filtration systems offer alternative scale mitigation pathways. Certain industrial operators deploy acid cleaning protocols instead of continuous chemical dosing strategies. These alternatives appeal where cost containment pressures dominate procurement decisions. In low complexity water systems, operators may tolerate periodic shutdowns for manual maintenance. This reduces reliance on specialty chemical formulations within non-critical process streams. Competitive substitution intensifies pricing pressure across standardized product categories. Market participants also face margin compression within commoditized treatment segments.

Substitute technologies reshape purchasing behavior toward capital expenditure tradeoffs. Some facilities prioritize one-time equipment investments over recurring chemical procurement contracts. Regulatory frameworks that favor non-chemical interventions further influence technology selection decisions. Advances in membrane materials with improved fouling resistance moderate chemical dependency. Process automation enables optimized cleaning cycles that reduce continuous inhibitor consumption. These shifts alter volume visibility and weaken long-term supply predictability. Suppliers must navigate differentiated demand across sectors with varying technical complexity. Collectively, substitution risk introduces structural volatility within otherwise recurring treatment chemical markets.

Opportunity Analysis - Advancements in Green Chemistry and Bio-based Formulations

Advancements in green chemistry are creating structural whitespace within antiscalants and dispersants portfolios. Bio-based formulations currently represent a meaningful minority share of market demand. Biodegradable polymers derived from polysaccharides and aspartic acid enable reduced ecotoxicity profiles. These chemistries address tightening discharge norms across industrial and municipal treatment systems. Regulatory scrutiny over phosphorus content and persistent residues accelerates substitution toward renewable inputs. Customers increasingly evaluate lifecycle environmental impact alongside functional scale inhibition performance. This dual performance compliance requirement reshapes product development priorities across the value chain. Consequently, research intensity shifts toward renewable feedstocks with comparable thermal and hydrolytic stability.

Sustainability mandates are influencing procurement frameworks and supplier qualification criteria. Corporate decarbonization strategies embed scope-based emissions accounting into chemical sourcing decisions. Bio-based formulations can reduce environmental liability exposure within regulated discharge environments. However, feedstock variability and higher input costs challenge margin parity with conventional chemistries. Technology maturation in polymer engineering is critical to achieving durability under high salinity conditions. Certification standards for biodegradability and toxicity testing introduce additional compliance expenditure. These factors elevate entry barriers while differentiating specialized suppliers. Green chemistry integration, therefore, reconfigures competitive positioning within performance-driven treatment markets.

Smart Monitoring Integration

The integration of smart monitoring technologies is transforming performance management within industrial water treatment systems. Digital sensors and automated dosing platforms enable continuous surveillance of scaling indices. Real-time analytics detect mineral saturation shifts before fouling compromises system efficiency. This predictive capability reduces unplanned shutdowns and preserves membrane and heat exchanger integrity. Antiscalant demand becomes linked to data-driven optimization rather than fixed dosing schedules. Integration with supervisory control systems enhances traceability and compliance documentation. Regulatory reporting requirements increasingly favor digitally validated chemical treatment records. Consequently, smart monitoring embeds chemical performance within broader industrial automation architectures.

Digital integration shifts value capture toward solution-oriented treatment ecosystems. Suppliers capable of coupling formulations with monitoring platforms gain structural differentiation. Data analytics enable optimized chemical consumption, influencing volume predictability and pricing models. Performance-based contracts become feasible where treatment outcomes are digitally verifiable. Technology convergence also raises cybersecurity and interoperability considerations across plant networks. Capital investment in instrumentation increases upfront cost intensity but stabilizes lifecycle economics. Regulatory oversight of effluent quality benefits from enhanced transparency and auditability. Smart monitoring, therefore, redefines competitive dynamics through technology-enabled treatment accountability.

Category-wise Analysis

Chemical Substance Type

Phosphonates are projected to lead, accounting for approximately 29% share in 2026, supported by their superior cost performance profile and strong threshold inhibition characteristics across industrial water systems. Their ability to sequester multivalent metal ions and suppress calcium carbonate and sulfate deposition reinforces entrenched adoption in cooling water circuits and boiler networks. High temperature stability and compatibility with diverse feedwater chemistries sustain utilization across oil and gas processing environments. Established formulation familiarity and predictable dosing economics strengthen procurement continuity in large-scale facilities. Portfolio depth from suppliers such as Solenis, Ecolab, and Kemira further anchors enterprise workflows. This combination of application breadth, operational reliability, and installed base momentum sustains segment dominance.

Sulfonated polymers are projected to be the fastest-growing segment, driven by their elevated thermal stability and robust performance under high-stress operating conditions. These polymers maintain inhibition efficiency where conventional phosphonates or carboxylates exhibit performance decline, particularly in high recovery desalination and concentrated brine environments. Resistance to calcium phosphate and zinc scale formation enhances suitability for advanced membrane systems. Growing deployment of high-temperature desalination infrastructure amplifies demand for durable chemistries capable of sustaining flux stability. Suppliers, including BASF, Arkema, and Italmatch Chemicals, are expanding polymer portfolios to address these requirements. Technology validation across stressed process regimes is accelerating early-cycle adoption and competitive differentiation.

End-user Industry Type

The oil and gas segment is projected to lead, with approximately 30% share in 2026, supported by the sector’s intensive fluid handling requirements across drilling, production, and topside processing systems. Large-scale injection of scale inhibitors into wells and pipelines is integral to maintaining flow assurance and asset integrity. Mineral deposition risks directly threaten throughput stability and pressure management across upstream and midstream infrastructure. Continuous chemical dosing mitigates calcium sulfate and carbonate precipitation under high temperature and high salinity conditions. Operational exposure to harsh reservoirs reinforces reliance on proven inhibitor chemistries supplied by providers such as Baker Hughes, Schlumberger, and Halliburton.

Water treatment is projected to be the fastest-growing, driven by accelerating desalination deployment and expanding municipal and industrial treatment infrastructure. Membrane-based technologies such as reverse osmosis and nanofiltration exhibit acute sensitivity to scaling and fouling. Rising freshwater scarcity and wastewater reuse mandates intensify investment in high recovery treatment systems. Advanced membrane materials require tailored inhibitor formulations compatible with variable feedwater chemistries. Industry participants, including Veolia, Suez, and DuPont, integrate chemical programs with membrane platforms. This convergence of infrastructure expansion and technology sensitivity accelerates segment growth relative to mature industrial applications.

Regional Insights

Asia Pacific Antiscalants and Dispersants Market Trends

Asia Pacific is expected to remain the leading regional market as well as the fastest growing region, accounting for approximately 36% share, supported by accelerated industrialization, expanding manufacturing clusters, and sustained infrastructure buildout across water-intensive sectors. The region is positioned to anchor global demand through large-scale deployment of power generation, petrochemical processing, and municipal water treatment assets. Industrial water throughput continues to expand alongside urbanization and export-oriented manufacturing ecosystems. Supply-side advantages, including integrated chemical production bases and cost-efficient feedstock access, reinforce regional competitiveness. Technology adoption in membrane desalination and high-pressure boiler systems increases reliance on advanced scale control chemistries.

China is expected to function as the primary regional anchor, shaping production capacity, pricing dynamics, and technology diffusion across Asia Pacific. National water quality enforcement and industrial discharge controls are anticipated to elevate performance specifications for antiscalants and dispersants. Domestic chemical manufacturers are expected to scale integrated production while global suppliers align joint ventures and localized supply chains to secure market access. Investment flows into coastal industrial corridors are likely to reinforce demand for high-performance water treatment chemistries. This ecosystem depth is set to consolidate Asia Pacific’s structural leadership within the global market.

North America Antiscalants and Dispersants Market Trends

North America is expected to remain a stable market region, supported by its mature industrial base and sustained upstream energy activity. The region is positioned to generate stable demand from power generation, refining, and shale-driven hydrocarbon production, requiring continuous scale control. Industrial operators are likely to prioritize process efficiency, asset integrity, and lifecycle optimization within established infrastructure networks. Advanced polymer research ecosystems and specialty chemical clusters are set to accelerate formulation innovation. This combination of regulatory enforcement, technical sophistication, and installed asset density is expected to sustain structural demand stability.

The U.S. is projected to function as the regional anchor, shaping technology pathways and procurement standards across North America. Federal water quality enforcement and discharge compliance frameworks are anticipated to elevate performance specifications for industrial treatment programs. Domestic innovation hubs are likely to expand advanced polymer chemistries aligned with non-toxic and biodegradable performance benchmarks. Vendor strategies are set to emphasize integrated treatment programs and digital monitoring capabilities to enhance operational transparency. This alignment of regulation, innovation, and industrial scale is expected to reinforce North America’s competitive positioning within the global market.

Europe Antiscalants and Dispersants Market Trends

Europe is expected to remain a mature and structurally stable market within the global antiscalants and dispersants landscape, supported by regulatory harmonization and sustainability-driven procurement frameworks. Growth is anticipated to originate primarily from retrofit cycles rather than greenfield capacity expansion, as legacy facilities upgrade treatment architectures to align with zero liquid discharge and circular water management mandates. Industrial operators are likely to emphasize premium formulations that balance performance with ecological compatibility, reinforcing a high-value, lower-volume demand profile. Advanced membrane deployment, energy transition infrastructure, and industrial decarbonization strategies are set to further embed specialty scale control solutions into process optimization initiatives.

Germany is expected to function as the regional anchor, shaping technology standards and procurement specifications across Europe’s industrial water ecosystem. Regulatory enforcement around industrial effluent quality is likely to accelerate the adoption of biodegradable inhibitors within process-intensive sectors. Domestic specialty chemical producers are anticipated to expand green chemistry portfolios while aligning with circular economy objectives. Investment in wastewater modernization and renewable energy-linked industrial clusters is set to sustain steady replacement demand. This regulatory depth and industrial sophistication are expected to reinforce Europe’s positioning as the benchmark market for sustainable water treatment chemistries.

Competitive Landscape

The global antiscalants and dispersants market is moderately consolidated, with leadership concentrated among global suppliers such as BASF, Ecolab, Dow, Solvay, and Clariant. These firms exert structural influence through integrated manufacturing assets, proprietary polymer chemistries, and globally harmonized compliance capabilities. Their scale supports multi-regional supply continuity and embedded relationships with industrial water operators across energy, desalination, and process industries. Extensive patent estates and formulation depth enable performance benchmarking that shapes procurement specifications and treatment standards.

Competitive positioning turns on technical service intensity and diagnostic integration rather than commodity chemical supply. Market leaders differentiate through bundled offerings that combine inhibitors, on-site monitoring, analytics platforms, and lifecycle performance optimization. Vertical integration across raw materials, formulation science, and field engineering strengthens switching barriers and reinforces enterprise account retention. Digital monitoring integration and data-driven dosing optimization are expected to deepen competitive stratification between platform providers and transactional suppliers.

Key Industry Highlights:

- In September 2025, Kemira acquired Water Engineering, Inc. to double its water revenue and establish a dominant position in industrial water treatment services. The partnership enables Kemira to scale its service offerings and deliver high-quality chemical solutions to manufacturing and healthcare sectors in North America.

- In January 2025, NALCO (National Aluminium Company) appointed Shri Brijendra Pratap Singh as CMD to lead technology-driven sustainable growth initiatives. The leadership shift is expected to accelerate the implementation of nano-based technologies for effluent treatment and environmental security.

- In November 2024, BASF completed the divestment of its flocculant mining business to Solenis, including the Magnafloc and Rheomax trademarks. This acquisition allows Solenis to strengthen its position as a leading specialty chemical provider for water-intensive mining operations.

Companies Covered in Antiscalants and Dispersants Market

- Ecolab (Nalco Water)

- BASF

- Dow

- Solenis

- Kemira

- Solvay

- Clariant

- SNF Floerger

- Arkema

- Kurita Water Industries

- Veolia Water Technologies

- Italmatch Chemicals

- LANXESS

- Evonik Industries

- Thermax

- BWA Water Additives

Frequently Asked Questions

The global antiscalants and dispersants market is projected to be valued at US$12.1 billion in 2026 and is expected to reach US$16.4 billion by 2033, driven by intensifying demand for scale inhibition in oil & gas enhanced oil recovery (EOR) processes and the critical expansion of desalination infrastructure in water-scarce regions.

Reverse osmosis and thermal desalination systems operate under extreme concentration gradients, making them highly susceptible to mineral scaling that compromises flux stability and energy efficiency. Antiscalants are therefore process-critical inputs that protect asset performance and longevity, with their consumption directly linked to the global build-out of water treatment capacity.

The antiscalants and dispersants market is forecast to grow at a CAGR of 4.4% from 2026 to 2033, reflecting steady demand from industrial water treatment, oil & gas operations, and municipal desalination projects.

Asia Pacific is both the leading and fastest-growing regional market, accounting for approximately 36% share, underpinned by large-scale industrialization, rapid desalination capacity expansion in China and India, and strong upstream oil & gas activity.

The antiscalants and dispersants market is moderately consolidated, with leadership concentrated among global specialty chemical suppliers such as BASF, Ecolab (Nalco Water), Dow, Solvay, and Kemira. These firms compete through integrated manufacturing assets, proprietary polymer chemistries, and bundled offerings that combine inhibitors with on-site monitoring and analytics platforms.