- Electric Mobility

- Hybrid and Electric Buses and Trucks Market

Hybrid and Electric Buses and Trucks Market Trends, Size, Share, Growth, Forecasts, 2025 - 2032

Hybrid and Electric Buses and Trucks Market By Battery Electric Vehicles (BEVs), Fuel Cell Electric Vehicles (FCEVs), Hybrid Electric, Vehicle Type (Buses and Trucks), Application (Public Transport, Long-Haul Freight, Last-Mile Delivery, Waste Management, Municipal/Utility, School & Institutional Fleets, Misc.), Range (Up to 150 km, 151-300 km, Above 300 km), Sales Channel, and Regional Analysis from 2025 - 2032

Hybrid and Electric Buses and Trucks Market Share and Trends Analysis

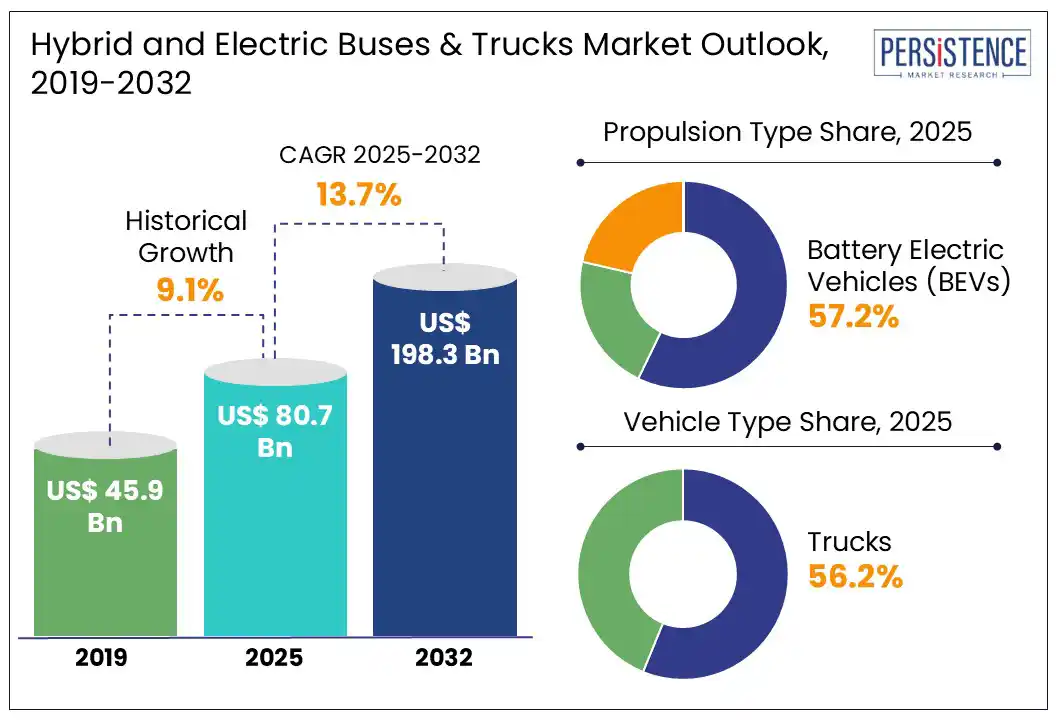

The global hybrid and electric buses and trucks market size is likely to be valued at USD 80.7 Bn in 2025 and is expected to reach USD 198.3 Bn by 2032, growing at a CAGR of 13.7% during the forecast period 2025 to 2032. The demand for hybrid and electric transport vehicles is expected to grow on account of the accelerating climate policies, large-scale fleet electrification, and steady battery cost reductions. Government mandates and clean mobility targets are pushing commercial fleets to adopt electric alternatives across the transit and logistics sectors.

Electric truck adoption is also gaining ground, especially in China and across Europe, with a positive sales trend. Battery prices dipping below $100/kWh and innovations from players such as Tesla and GM are making electric trucks and buses more competitive. This global shift is setting the stage for long-term growth, with North America, Europe, and emerging markets such as India becoming key pillars in the transition.

Key Industry Highlights:

- China commands over 36% of the global market, selling more than 230,000 zero-emission commercial vehicles in 2024.

- Europe records a 26.8% growth in electric bus registrations, with Italy becoming the largest market by volume.

- Electric truck sales globally surpassed electric buses for the first time in 2023, led by China’s 70% share and strong growth in Europe and the U.S.

- U.S. policies like IRA and IIJA fuel adoption, with 45 states offering incentives and 74.4% of EVs sold in Q2 2024 being domestically built.

- UK’s ZEBRA program has supported over 5,200 electric buses since 2020, while public charging infrastructure crosses 76,000 units.

- Volvo’s electric trucks operate in over 50 countries, with models now reaching 600 km range, advancing long-haul electrification readiness.

| Global Market Attribute | Details |

| Market Size (2024A) | US$ 71.0 Bn |

| Estimated Market Size (2025E) | US$ 80.7 Bn |

| Projected Market Value (2032F) | US$ 198.3 Bn |

| Value CAGR (2025 to 2032) | 13.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 9.1% |

Market Dynamics:

Driver - Government Push Shapes the Global Hybrid and Electric Commercial Fleet Landscape

The global hybrid and electric buses and trucks market is advancing steadily due to strong, coordinated efforts by governments to transform public and commercial transport. India is building a holistic ecosystem from subsidizing vehicle acquisition to backing local manufacturing and deploying charging stations to promote electric mobility in high-volume segments such as buses and freight trucks. Programs such as FAME II and PM e-Bus Sewa not only make vehicles financially accessible but also encourage private sector participation by de-risking operations. Under FAME II alone, over 6,800 electric buses have been sanctioned, and more than 5,100 are already deployed across Indian cities, reflecting real progress in fleet electrification.

The U.S. is focusing on long-term fleet transition, backed by successful pilot programs in cities like Seneca and Seattle, and supported by federal investments such as the $85 million disbursed under the Low or No Emission Program. In the UK, government-backed funding and clear long-term goals are pushing the zero-emission agenda forward. While a full diesel bus phase-out date is pending, the ZEBRA program has already supported more than 5,200 electric buses since 2020. Moreover, with over 76,000 public chargers, 20% of which are rapid, the UK is signaling clear readiness for broader adoption.

Restraint - Electrification of Freight Segment Lags Behind Passenger Adoption

Despite visible momentum in the electrification of public buses, the freight segment especially medium and heavy-duty trucks, continues to fall behind. Operators face barriers beyond high costs, including insufficient charging infrastructure along key logistics corridors and persistent concerns over vehicle range and uptime.

These operational challenges limit adoption in countries with slow grid development. For instance, in the UK, electric HGVs made up just 0.2% of the fleet by mid-2024. Even in Germany, where progress has been stronger, buses still outpace electric trucks due to clearer policies and infrastructure readiness.

Fleet managers remain cautious, as reliability and turnaround time are critical for logistics. While some governments offer incentives, they often lack scale or coordination, delaying broader freight transition. Without targeted freight-focused strategies, trucks will continue to lag in the global shift toward zero-emission transport.

Opportunity - Hybrid Technologies Present Scalable Entry Point for Commercial Electrification

The global shift toward sustainable mobility is accelerating, but full battery-electric adoption still faces infrastructure and cost-related challenges in many regions. In this transition, hybrid and plug-in hybrid technologies have emerged as a practical and scalable middle ground, especially for commercial buses and trucks. These solutions offer an efficient blend of emission reduction and operational reliability, making them increasingly attractive for fleet operators navigating logistical and budgetary constraints.

In markets such as Australia and the U.S., hybrid vehicles are shaping fleet electrification strategies. Australia has witnessed hybrids and plug-in hybrids exceed 19% of total vehicle sales, consistently outpacing battery-electric options. In the U.S., hybrid sales grew by over 30% year-over-year by Q2 2024, signaling strong market traction.

Fleet operators favor hybrids as they align with existing operational workflows without demanding major investment in charging infrastructure. With global automakers expanding hybrid offerings across their commercial portfolios, these technologies are becoming a trusted route for transitioning toward lower-emission transport in both public and freight mobility.

Key Trends

- Policy Roadmaps

Governments worldwide are establishing clear, long-term electrification roadmaps backed by legislation and targets, especially for high-volume sectors such as public transit and last-mile delivery.

- Market Growth

Significant increases in electric bus deployment, such as India’s PM e-Bus Sewa and the UK’s tenfold rise in electric bus registrations, demonstrate the shift from ambition to execution.

- Investment Confidence

With clearer policy frameworks and infrastructure plans, operators, manufacturers, and investors show greater commitment, accelerating adoption rates across regions with active support programs.

- Domestic Manufacturing

The U.S. leads in EV production, with over 74% of electric vehicles sold built locally, boosted by incentives, signaling stronger commercial sector growth for hybrid and electric buses and trucks.

Category-wise Analysis

Propulsion Type Insights

Battery Electric Vehicles (BEVs) hold the largest share of the hybrid and electric buses and trucks market at 67.2%, reflecting their central role in global fleet electrification. This dominance is driven by strong government mandates, city-level clean air goals, and ongoing improvements in battery range and efficiency.

European nations, including Italy, Spain, and Germany, are pushing BEV adoption across public transport, with Italy alone recording a 161.7% surge in electric bus registrations in 2024.

In India, policy shifts under the PM E-DRIVE scheme, including INR 4,391 crore allocated for electric buses and INR500 crore for electric trucks, further strengthen BEV momentum in Asia’s largest developing market. BEVs are gaining traction because they align with long-term decarbonization goals while meeting operational needs for zero-emission urban transport.

The U.S. is also advancing BEV use through state-level funding programs like California’s HVIP and utility-backed infrastructure, proving BEVs are becoming the go-to propulsion type across developed and emerging economies alike.

Vehicle Type Insights

Trucks account for 56.8% of the hybrid and electric buses and trucks market, with Light-Duty Trucks (LDT) leading at 35-40% share. These vehicles are favored in urban logistics, e-commerce deliveries, and municipal services, where shorter routes and high daily utilization match well with available charging infrastructure.

In the U.S., states such as California and Colorado are accelerating electric truck deployment by offering direct subsidies and grants, which have helped OEMs like Volvo and BYD expand fleet penetration.

Medium- and Heavy-Duty Trucks, around 33% and 29% share, respectively, are showing early momentum, especially with recent technological breakthroughs. Volvo’s next-gen FH Electric with a 600 km range and growing interest in hydrogen-electric hybrids demonstrate the market’s readiness for long-haul electrification.

In Europe, Germany and Italy are experiencing a triple-digit growth in electric truck sales, backed by supportive policies and emissions mandates, while India’s PM E-DRIVE scheme directly targets freight electrification, setting the stage for trucks to lead the next wave of commercial EV growth globally.

Regional Insights

North America Hybrid and Electric Buses & Trucks Market Trends

North America accounts for 21% market share in 2025, driven by large-scale policy backing and early fleet adoption across the U.S. and Canada. The hybrid and electric buses and trucks market in the U.S. is gaining momentum, supported by transformative initiatives such as the IRA and IIJA. These policies are bridging the cost gap and expanding infrastructure for electric commercial vehicles.

Fleets have already committed to reaching 30% zero-emission truck purchases by 2030, signaling a decisive shift. Despite the high upfront cost and range limitations, the growing total cost of ownership advantage, coupled with health and operational benefits, continues to drive this market forward.

In Canada, adoption remains slow despite a strong manufacturing base and several homegrown clean bus and truck companies. Zero-emission vehicles accounted for just 2% of new truck and bus sales in 2023, putting Canada well behind global averages.

The country holds potential, with electric vans such as the BrightDrop Zevo 600 marking production milestones and early transitions seen in fleets such as the City of Toronto and P.E.I.’s school buses. Health concerns tied to diesel emissions and policy gaps continue to push the conversation. As the U.S. accelerates electrification through infrastructure mandates and fleet targets, Canada’s lag in adoption risks placing its domestic manufacturers at a global disadvantage.

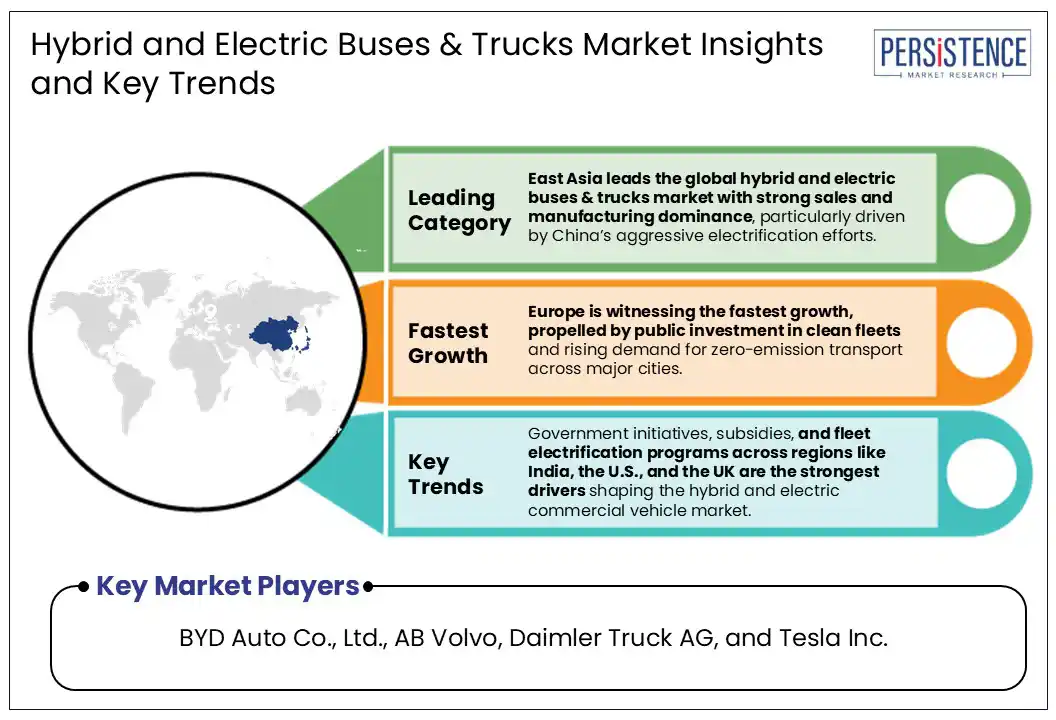

East Asia Hybrid and Electric Buses & Trucks Market Trends

East Asia holds around 36% of the global hybrid and electric buses and trucks market, anchored by China’s rapid electrification efforts and infrastructure rollout. China leads the region with strong policy support and commercial readiness, reflected in its near-full electrification of city buses and expanding adoption across industrial sectors. Battery electric trucks accounted for 13% of medium-duty and 14% of heavy-duty market share in 2024, marking a clear shift toward zero-emission freight solutions.

Japan follows a more measured approach, continuing its reliance on hybrid-electric platforms while outlining long-term goals to transition all domestic automaker output to xEVs by 2050. Although battery electric vehicle penetration remains limited, initiatives under the Green Growth Strategy are expected to push adoption gradually.

South Korea, meanwhile, shows stronger near-term traction. Backed by policy incentives and firm investments in EV infrastructure, domestic manufacturers such as Hyundai and Kia are scaling electric truck and bus production. While the country operates at a smaller scale than China, its strategic focus ensures sustained growth across the hybrid and electric commercial vehicle segments.

Competitive Landscape

The global hybrid and electric buses and trucks market exhibits a moderately consolidated structure, with a few major players holding significant market influence, especially across key regions such as Asia, North America, and Europe.

Companies such as BYD Auto Co., Ltd., AB Volvo, Daimler Truck AG, and Tesla Inc. are leading the global transition, investing heavily in product innovation, battery technology, and long-haul electric truck development. China’s dominance, led by BYD, highlights strong vertical integration and mass-scale deployment, while European manufacturers like Scania AB and Daimler focus on advanced battery systems and low-emission urban transport models.

In North America, Ford Motor Company and PACCAR Inc. are scaling up zero-emission commercial vehicle offerings through partnerships, pilot fleets, and infrastructure alliances. The current trend shows a shift toward long-range, heavy-duty electric trucks and hydrogen-electric hybrids, with manufacturers working on modular platforms to serve diverse duty cycles. With increasing government mandates and global OEM investments, the competition is intensifying pushing players to differentiate via range, cost-efficiency, and regional adaptability in the evolving hybrid and electric commercial fleet landscape.

Key Developments:

- In April 2025, Daimler Buses announced an expansion of its e-mobility portfolio by introducing new e-services aimed at extending the lifespan of electric bus batteries. Starting in 2026, customers can opt for remanufactured batteries or next-gen replacements with higher range, including NMC4 and LFP battery technologies. This initiative strengthens Daimler’s commitment to making e-buses as durable and economical as their diesel counterparts, reinforcing its leadership in sustainable public transport.

- In September 2024, Volvo Trucks announced the launch of its next-gen FH Electric truck with a 600 km range on a single charge, marking a breakthrough in long-haul zero-emission transport. The new model, set for release in late 2025, uses a newly developed e-axle to boost battery capacity and drivetrain efficiency. This positions Volvo to lead the shift toward fossil-free freight as part of its 2040 net-zero goal.

Companies Covered in Hybrid and Electric Buses and Trucks Market

- BYD Auto Co., Ltd.

- Tesla Inc.

- AB Volvo / Volvo Group

- Daimler Truck AG / Mercedes-Benz Group

- Ford Motor Company

- PACCAR Inc.

- Scania AB

- MAN Truck & Bus SE

- Tata Motors

- Ashok Leyland

- Iveco Group

- Mitsubishi Fuso Truck and Bus Corporation

- Isuzu Motors Ltd.

- Dongfeng Motor Corporation

- XL Fleet Corp.

- Bollinger Motors

Frequently Asked Questions

The global hybrid and electric buses & trucks market is projected to be valued at US$ 80.7 Bn in 2025.

BEVs are expected to hold a 67.2% market share in 2025, driven by global fleet electrification initiatives.

The hybrid and electric buses & trucks market is poised to witness a CAGR 13.7% from 2025 to 2032.

Government initiatives, emission mandates, and cost-effective hybrid technologies are driving the growth of the hybrid and electric buses and trucks market.

Hybrid and plug-in hybrid systems offer a scalable bridge to full electrification, especially in regions with limited charging infrastructure.

Key market players include BYD Auto Co., Ltd., AB Volvo, Daimler Truck AG, and Tesla Inc.