- Electric Mobility

- Electric Vehicle (EV) Transmission Market

Electric Vehicle (EV) Transmission Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Electric Vehicle (EV) Transmission Market by Transmission Type (Single-speed, Dual-speed, Multi-speed), Transmission System (Automated Manual Transmission (AMT), Continuous Variable Transmission (CVT), Automatic Transmission (AT), Others), Vehicle Type ((BEVs), (PHEVs), (HEVs)), and Regional Analysis for 2025 - 2032

Electric Vehicle (EV) Transmission Market Share and Trends Analysis

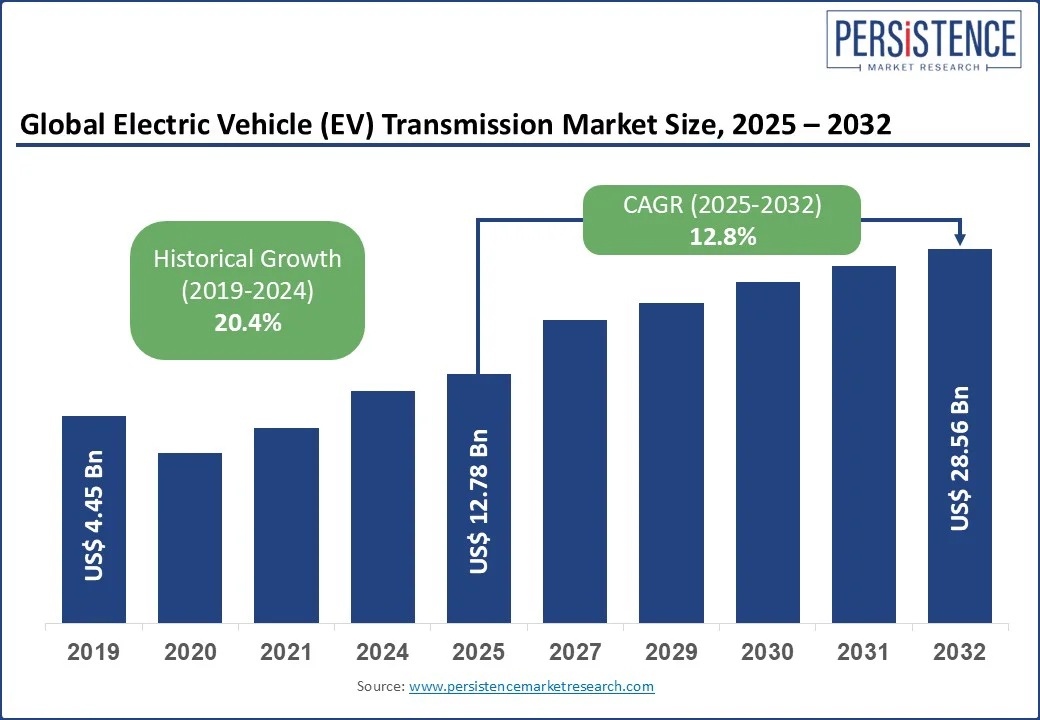

The global electric vehicle (EV) transmission market size is likely to be valued at US$ 12.78 Bn in 2025, and is estimated to reach US$ 28.56 Bn by 2032, growing at a CAGR of 12.8% during the forecast period 2025 to 2032.

The rising adoption of multi-speed transmissions in heavy-duty electric vehicles (EVs) and the integration of e-axles and Transmission Control Units (TCUs) by original equipment manufacturers (OEMs) are the two major growth determinants.

Electric vehicle (EV) transmissions are the critical drivetrain component that translates electric motor torque into optimized wheel performance across various EV types. With drivetrain innovation forming the core engine of advancement for electric mobility, the market for EV transmissions stands at the precipice of enormous expansion due to tightening regulations to curb tailpipe emissions, widespread electrification of commercial fleets, and the urgent requirement for high-efficiency torque conversion.

Intelligent gearboxes capable of real-time power management are finding momentum, especially in fleet and commercial EVs. Some of the most lucrative opportunities in the market are emerging in niche areas such as grid-capable transmission systems aligned with vehicle-to-grid (V2G) technology. These developments are transforming the EV transmission landscape into a strategic focal point for innovation, efficiency, and scalable electrification.

Key Industry Highlights:

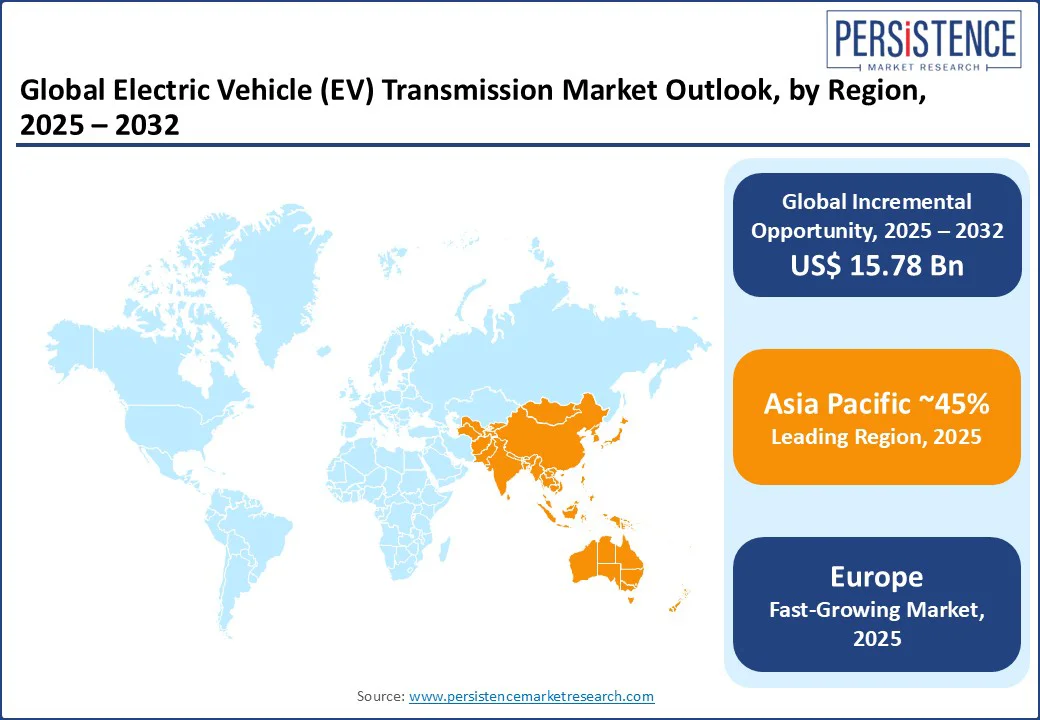

- Dominant Region: Asia Pacific is projected to dominate among the regional markets with an approximate share of 45% in 2025, powered by China’s stranglehold on global EV production and domestic sales.

- Fast-growing Region: Fueled by a huge demand for dual-mode transmission and a strong uptake in transitional EVs in the highly prosperous markets of North America and Europe, plug-in hybrid electric vehicles (PHEVs) are forecast to register the highest CAGR through 2032.

- Leading Vehicle Type: Battery electric vehicles (BEVs) are expected to dominate the vehicle type segment with a projected share of nearly 90% in 2025, owing to the vast electrification drives by OEMs and streamlined single-speed gearbox architecture.

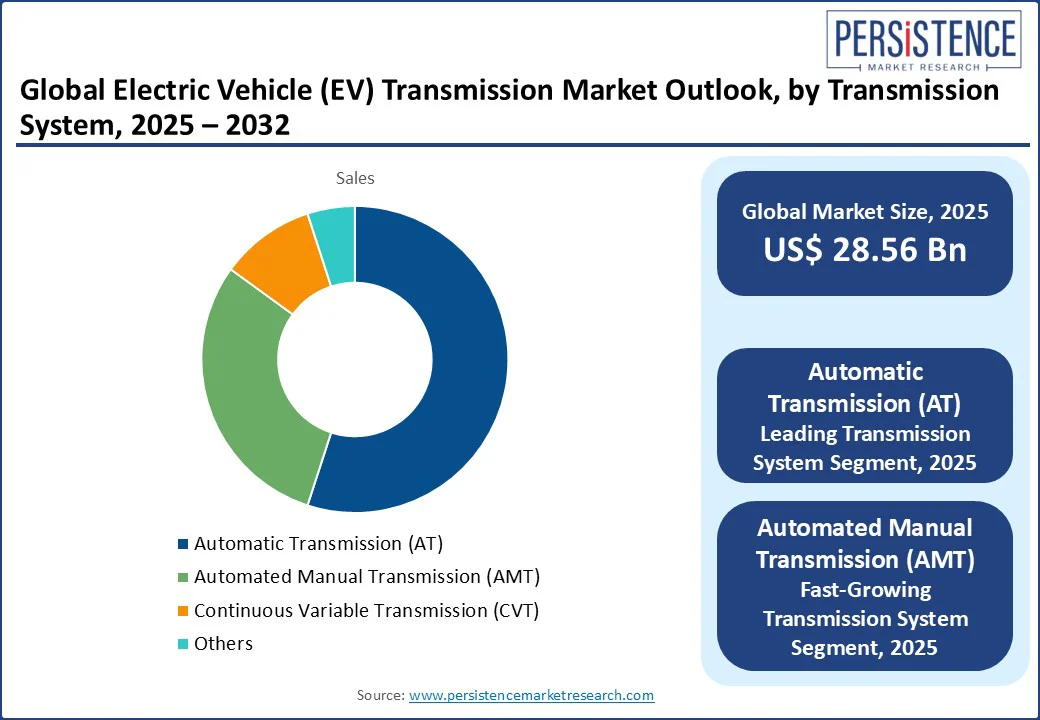

- Leading Transmission Type: In the transmission system segment, automatic transmission systems are anticipated to maintain a leading share of 55% in 2025, as OEMs are actively integrating automatic EV gearboxes that deliver seamless torque delivery with minimal mechanical complexity.

- Technical Compatibility: The integration of multi-speed and software-defined transmissions considerably improves the performance across commercial EV platforms and high-performance electric vehicles.

- Novel Opportunities: The designing and development of e-axles and modular gearbox systems are unlocking new opportunities, especially as OEMs seek scalable, lightweight drivetrain solutions for next-gen EV models. The industry-wide shift toward lightweight materials and high-efficiency gear is directed toward enabling better range optimization and reduced thermal loss in EV transmission systems.

- Strategic Aspect: The competitive landscape is intensified by strategic collaborations and system-level integration, with players such as ZF Friedrichshafen, Eaton, Dana, and BorgWarner investing in compact, adaptive, and software-integrated EV transmission solutions.

|

Global Market Attribute |

Key Insights |

|

EV Transmission Market Size (2025E) |

US$ 12.78 Bn |

|

Market Value Forecast (2032F) |

US$ 28.56 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

12.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

20.4% |

Market Dynamics

Driver - Soaring Demand for High Performance in Commercial EVs to Fuel Innovation in Multi-Speed Transmission

Given the exigency for developing advanced drivetrain solutions for EVs in the face of climate change challenges, the electric vehicle transmission market growth is likely to be upped by the high demand for performance and range efficiency of commercial EV fleets. While passenger EVs can function smoothly with single-speed gearboxes, electric light- and heavy-duty commercial vehicles require multi-speed EV transmissions to handle varying payloads, gradients, and duty cycles without compromising battery range or thermal stability.

- For instance, Daimler’s eActros 600, launched in late 2024, consists of a two-speed transmission to optimize power delivery for logistics across highways and cities, improving efficiency by over 10% compared to single-speed counterparts.

This engineering marvel is influencing procurement decisions across OEMs and tier-1 suppliers, which is particularly significant since fleet electrification is scaling rapidly across major economies.

Restraint - Complexities Involved in Software-Hardware Integration Complexities to Impede EV Transmission Scalability

The integration of transmission hardware with advanced control software, particularly in multi-speed and e-axle architectures, is a process that is rife with complexities. As EV powertrains evolve from mechanical systems into software-defined platforms, transmission modules must now synchronize seamlessly with motor control units (MCUs), automotive battery management systems (BMS), and vehicle dynamics controllers.

- For example, ZF Friedrichshafen’s 2-speed EV transmission for high-performance vehicles promised enhanced energy efficiency, but it has been facing delays due to calibration challenges across multiple ECUs and drive cycles. This bottleneck has become far more evident and particularly acute in OEM-supplier ecosystems where proprietary software is proving ineffective in dealing with real-time issues, slowing down time-to-market and inflating development costs.

Consequently, the mass adoption of multi-speed EV gearbox technologies is becoming increasingly difficult, especially for mid-market BEVs, where cost, system validation, and software support remain unresolved.

Opportunity - Emergence of e-Axle Architectures to Prove Highly Lucrative for Market Players

The electric vehicle transmission market is replete with opportunities, but one area that promises exceptional returns for EV companies is located in the rapid adoption of integrated e-axle systems. These systems unify the motor, inverter, and transmission into a single compact unit, drastically improving packaging efficiency, energy density, and vehicle performance.

Today, a central concern for EV manufacturers is to reduce vehicle weight and complexity while boosting range. The incorporation of e-axle EVs is emerging as a technically and financially feasible solution, especially in SUVs and crossovers where space constraints and torque demands intersect.

- Hyundai Motor Group’s E-GMP platform, for instance, employs an advanced e-axle with a reduction gear transmission that supports 800V fast charging and delivers sub-4.5 second 0-100 km/h acceleration. This has opened a new frontier for suppliers developing compact EV gear units, thermal-efficient transmission casings, and software-defined e-axle management systems tailored to high-volume platforms. The increasing insourcing of motor designs by OEMs has produced a compelling opportunity to own intellectual property (IP) in the form of patented EV transmission solutions, including e-axles.

Category-wise Analysis

Transmission System Insights

Among transmission systems, the automatic transmission (AT) sub-segment is estimated to account for a leading 55% revenue share in 2025. OEMs are visibly favoring automatic EV gearboxes that deliver seamless torque delivery with minimal mechanical complexity, which is a defining feature for battery electric vehicles.

- For example, Volkswagen’s MEB platform employs a refined single-speed reduction gearbox, which enables high torque while also ensuring a minimal footprint in terms of packaging and promoting superior energy efficiency in passenger-car lineups. The prevalence of AT systems is further underpinned by cost advantages, streamlined manufacturing, and ease of integration into high-volume modular EV platforms, making this transmission model the default choice for mass-market BEVs.

On the other hand, automated manual transmission systems are set to exhibit the highest CAGR by 2032. The upsurge of AMT systems reflects the deepening interest in dual-clutch and dual-speed automated gearboxes in light- and heavy-duty EVs where efficiency and torque modulation are imperative, especially in logistics fleets and long-haul electric trucks.

Recent OEM innovations, such as Allison’s introduction of the Egan Power 85S e-axle featuring an automated dual-speed gearbox at Bus World Europe in 2023, are testament to the traction smart transmission systems are gathering in commercial applications. Stakeholders seeking to minimize the total cost of ownership (TCO) and thermal efficiency are increasingly embracing multi-speed AMT models, especially in regions where range and payload flexibility are non-negotiable.

Vehicle Type Insights

Battery electric vehicles are slated to be the dominant sub-segment, projected to account for nearly 90% share in 2025. The enviable position of BEVs in the EV transmission market is because of their minimal reliance on plug-in hybrid or hybrid powertrains, allowing streamlined integration of single-speed EV gearboxes, direct-drive transmission systems, and a much simplified architecture. For example, renowned BEV platforms such as China’s BYD Seal and Tesla Model 3 depend on single-ratio or single-speed reduction gearboxes, enabling lower costs and easier thermal management in modular EV architectures. The demand for direct drive transmission and automatic transmission systems in BEVs unlikely to dampen as OEMs are expected to continue to scale mass-market offerings.

Even though the revenue share of plug-in hybrid electric vehicles is considerably than BEVs, this sub-segment is nonetheless anticipated to grow at the fastest CAGR through 2032. PHEVs are gaining prominence in markets where range anxiety is still a concern but infrastructure is nascent. These vehicles necessitate the utilization of dual-mode transmission systems that can facilitate hassle-free switching between electric single-speed direct drive and conventional combustion transmission. OEMs are actively tapping into the PHEV space with new releases such as Volvo’s XC60 Recharge PHEV and Mitsubishi Outlander PHEV that are armed with adaptive transmission modules designed for both EV torque characteristics and internal combustion engine (ICE) coupling.

Regional Insights

Asia Pacific Electric Vehicle (EV) Transmission Market Trends

At 45%, Asia Pacific accounts for the largest portion of the electric vehicle transmission market share, convincingly led by China’s command over EV production, sales, and exports. In 2024, according to the International Energy Agency (IEA), more than 11 million electric cars were sold in China. The regional market also accrues benefits from the vertically integrated EV supply chains, such as the battery-to-transmission structure, highly attractive government incentives promoting EV adoption (such as India’s FAME scheme), and OEMs such as SAIC and JATCO investing heavily in transmission R&D. As an outcome an intricate ecosystem is available for single-speed EV gearboxes, multi-speed transmission systems, and e-axle integration tailored for modular BEV platforms. Across the major economies of the region, government policies and corporate strategies are oriented towards making EV adoption affordable for the average consumer, encouraging fleet electrification of buses and trucks, and setting practical national targets on emissions and mobility.

North America Electric Vehicle (EV) Transmission Market Trends

North America commands roughly 41% share of the EV transmission systems market, attributable to the drivetrain advancements spearheaded by Tesla, GM, Ford, and Rivian, and strong public and private investments in scaling EV charging infrastructure and R&D activities in cutting-edge transmission technologies. Despite the winding down of the U.S. federal tax credit for EV makers, innovation in transmission systems remains well-received by investors.

- Tesla’s Semi truck, for example, demonstrates dual-speed transmission potential in heavy-duty applications. The growth of the market in North America is also bolstered by OEM-driven co- development of transmission modules, increasing stress on TCU integration, and the need for adaptive gearbox solutions in commercial EVs.

Europe Electric Vehicle (EV) Transmission Market Trends

Europe, representing a 14% share in 2025, is set to be the fastest-growing regional market of electric vehicle transmission systems during the forecast period 2025-2032. The market is fueled by uncompromising vehicular emissions mandates by the European Union (EU), expansion of zero-emission zones across the continent, and looming bans on ICE sales in Norway, the U.K., and Germany. European OEMs, such as Volkswagen, Mercedes Benz, and BMW, are speedily pivoting to modular EV platforms with integrated transmissions and e-axles, often embedding multi-speed systems for performance and efficiency. Moreover, the regulatory push for reducing carbon emissions is stimulating demand for energy-optimizing transmissions in passenger BEVs and plug-in commercial fleets.

Competitive Landscape

With the rush for efficient and clean mobility gaining pace worldwide, the global EV transmission market landscape is undergoing a transformative phase, driven by an accelerated convergence of drivetrain innovation, supply-chain control, and system-level differentiation. At the strategic core is the relentless pursuit of the integration of transmission hardware with electrified propulsion systems that will empower suppliers and OEMs to deliver compact, high-efficiency e-axle units and multi-speed gearbox modules.

Top firms such as ZF, Eaton, and Continental are in an overdrive mode to incorporate software-defined transmission control, optimized thermal management, and materials-engineered lightweight casings to reduce cost and improve performance of their products. For example, ZF Friedrichshafen’s modular multi-speed unit and Eaton’s record-level production orders are expected to buttress supplier confidence in transmission systems as a value-added, margin-rich domain. At the same time, industry consolidation through alliances and M&A activities is synergizing R&D operations on adaptive transmission control units integrated with motor inversion systems.

Key Industry Developments

- In July 2025, Linamar Corporation committed US$ 1.1 billion to its Ontario operations to advance EV manufacturing and innovation, including e-Axle systems, battery and semiconductor packaging, hydrogen fuel cells, and energy storage technologies. This investment, supported by US$ 169.4 million from the Canadian federal government and US$ 100 million from Ontario, aims to create up to 2,300 new jobs, protect 10,000 existing positions, and strengthen Ontario’s domestic EV supply chain amid global market challenges and US tariff threats.

- In July 2025, ZF Transmissions Shanghai Co., Ltd. deployed its first reduction drive specifically for the new energy vehicle (NEV) market in China, marking a significant advancement in ZF’s localized e-mobility solutions. This reducer combines ZF’s global cutting-edge e-drive technologies with local manufacturing expertise, featuring high efficiency, low noise, and a compact axial parallel design tailored to meet the stringent requirements of mainstream NEV platforms in China. This initiative is part of ZF’s broader strategy to fuel the electrification of China’s automotive industry through innovation and local partnerships.

- In June 2025, Allison Transmission announced a definitive agreement to acquire Dana Incorporated’s Off-Highway business for approximately US$2.7 Bn, pending regulatory approvals. The acquisition expands Allison’s commercial-duty powertrain and industrial solutions globally by integrating Dana’s drivetrain, propulsion, hybrid, and electric drive technologies for off-highway applications in sectors such as construction, agriculture, mining, and forestry. The deal is expected to be immediately accretive to Allison’s earnings and generate an annual value of around US$ 120 Mn, enhancing Allison’s ability to serve a broadening customer base for EVs and accelerate growth in electrification.

Companies Covered in Electric Vehicle (EV) Transmission Market

- ZF Friedrichshafen AG

- Eaton Corporation plc

- Continental AG

- AISIN CORPORATION

- Dana Limited

- Allison Transmission, Inc.

- AVL List GmbH

- BorgWarner Inc.

- JATCO Ltd.

- Schaeffler Technologies AG & Co. KG

Frequently Asked Questions

The global electric vehicle (EV) transmission market is projected to reach US$ 12.78 Bn in 2025.

Tightening regulations to curb tailpipe emissions and widespread electrification of commercial fleets are driving growth.

The market is poised to witness a CAGR of 12.8% from 2025 to 2032.

The increasing urgency for high-efficiency torque conversion in EVs and the development of intelligent gearboxes capable of real-time power management are key market opportunities.

ZF Friedrichshafen AG, Eaton Corporation plc, and Continental AG are a few leading market players.