- Power Generation, Transmission, & Distribution

- Thermoelectric Generators Market

Thermoelectric Generators Market Size, Share, and Growth Forecast 2026 - 2033

Thermoelectric Generators Market by Material (Bismuth Telluride, Lead Telluride, Skutterudites, Magnesium Silicide, Others), Application (Waste Heat Recovery, Energy Harvesting, Direct Power Generation, Others), Industry (Automotive, Industrial Manufacturing, Energy & Utilities, Consumer Electronics & Wearables, Telecommunications, Healthcare, Aerospace & Defense, Others), and Regional Analysis, 2026 - 2033

Thermoelectric Generators Market Size and Trend Analysis

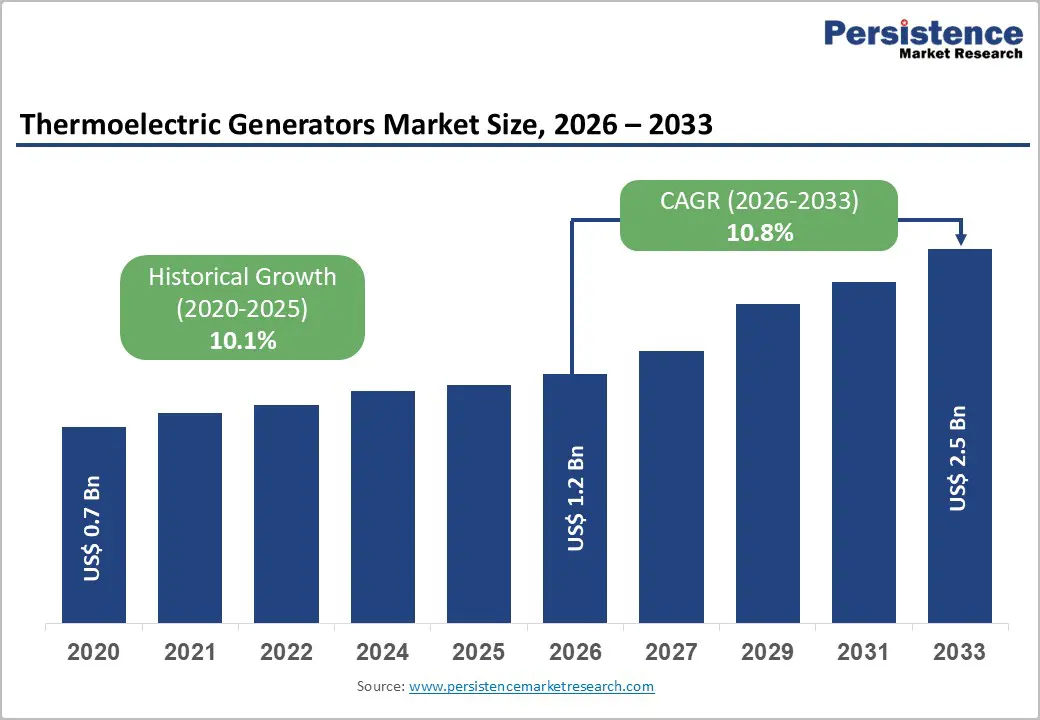

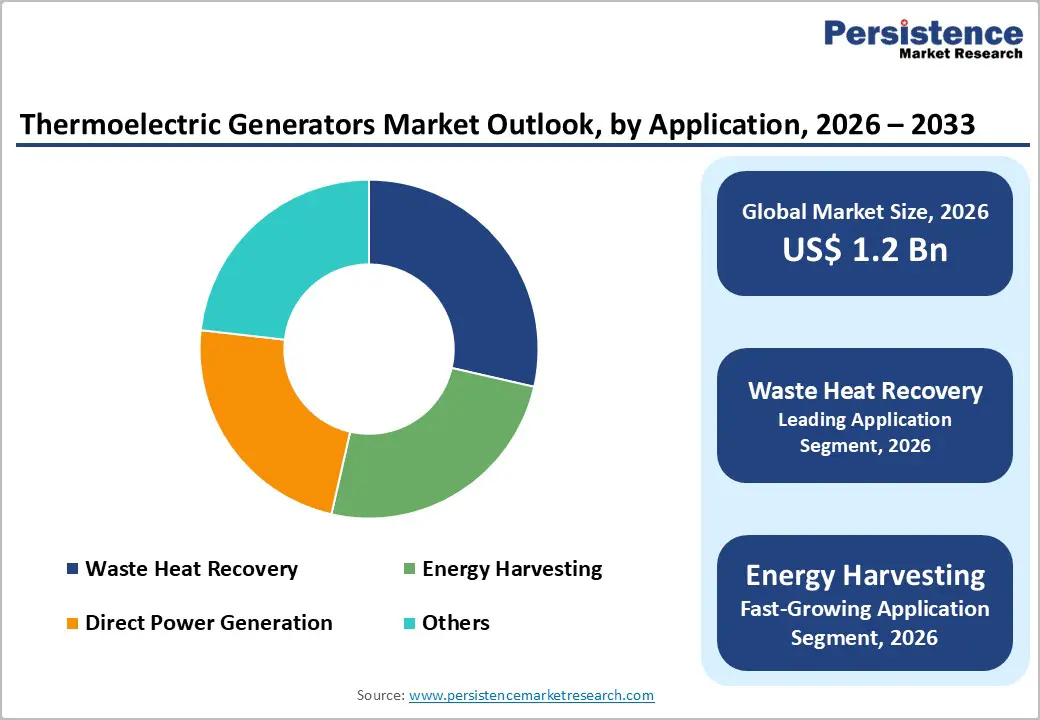

The global thermoelectric generators market size is expected to be valued at US$ 1.2 billion in 2026 and projected to reach US$ 2.5 billion by 2033, growing at a CAGR of 10.8% between 2026 and 2033.

Rising sustainable energy demand is accelerating adoption, as thermoelectric generators (TEGs) convert waste heat into reliable electricity without moving parts. According to the U.S. Department of Energy, industrial waste heat accounts for 20-50% of input energy, nearly 1 quadrillion BTU annually in the U.S., creating strong recovery potential. Efficiency improvements from 5-8% to 12-15%, supported by research from NASA, further strengthen TEG deployment aligned with global net-zero and energy-efficiency targets.

Key Industry Highlights:

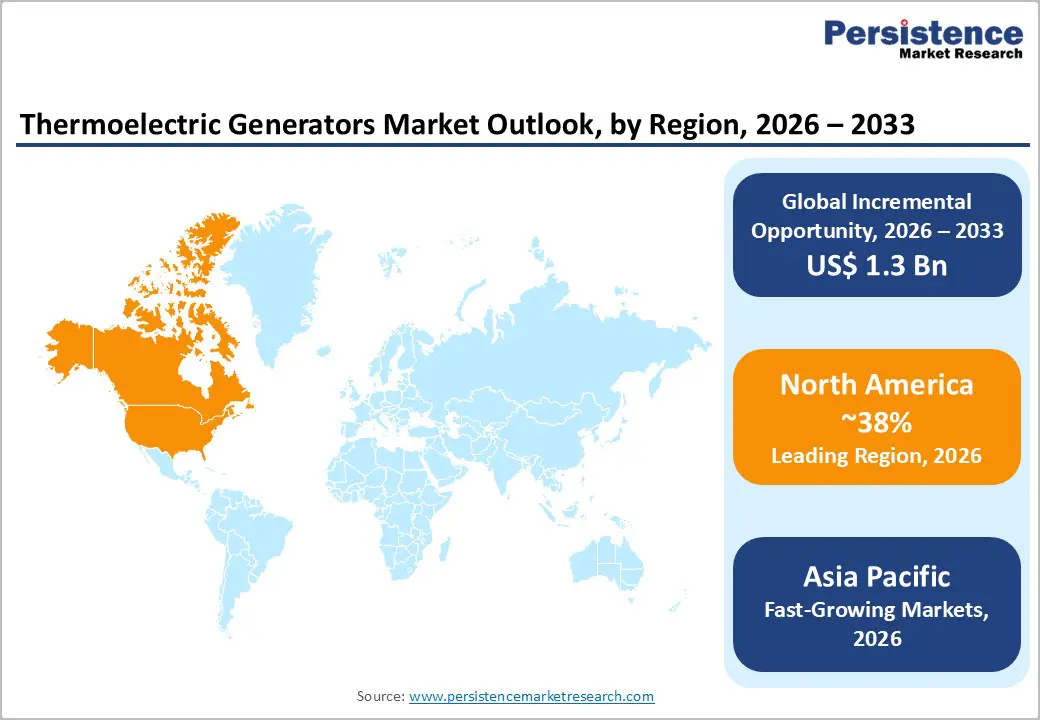

- Leading Region: North America dominates with ~38% market share, supported by strong R&D funding, policy incentives, and advanced industrial and aerospace integration.

- Fastest Growing Region: Asia Pacific holds nearly 30% share and is projected to expand rapidly at around 12% CAGR, driven by EV production, industrial expansion, and supportive manufacturing policies.

- Leading Material Category: Bismuth Telluride leads with approximately 60% share due to its superior ZT performance (1.0-1.2) and established use in mid-temperature automotive and electronics applications.

- Leading Application Category: Waste Heat Recovery accounts for over 50% share, fueled by the need to capture 20-50% industrial energy losses and improve operational efficiency.

- Key Opportunity: EV auxiliary power and range extension present strong growth potential, aligned with projections of 60% global EV sales by 2030.

| Key Insights | Details |

|---|---|

| Thermoelectric Generators Size (2026E) | US$ 1.2 billion |

| Market Value Forecast (2033F) | US$ 2.5 billion |

| Projected Growth CAGR (2026 - 2033) | 10.8% |

| Historical Market Growth (2020 - 2025) | 10.1% |

Market Dynamics

Drivers - Industrial Waste Heat Recovery Accelerates TEG Adoption

Industries lose substantial energy as waste heat, creating strong demand for thermoelectric generators (TEGs) to improve efficiency and reduce operational costs. The U.S. Department of Energy estimates that 20-50% of energy used in U.S. manufacturing is discharged as heat, equivalent to nearly 1 quadrillion BTU annually. Capturing even a fraction can lower industrial energy costs by 10-20%.

Policy frameworks such as the European Commission’s Green Deal target major industrial emission reductions by 2030, reinforcing adoption of waste heat technologies. TEGs, with no moving parts and minimal maintenance, operate reliably in harsh, high-temperature environments. Pilot installations demonstrate megawatt-scale recovery potential, strengthening sustainability and energy optimization initiatives globally.

Automotive Efficiency Regulations Strengthen Market Demand

Stringent fuel-efficiency and emission standards are accelerating thermoelectric generator integration in vehicles. Regulations from the U.S. Environmental Protection Agency and European authorities require significant fuel savings, encouraging technologies that recover exhaust heat. TEG systems can convert 3-5% of exhaust energy into usable power, directly improving vehicle efficiency.

Testing by the SAE International shows outputs of approximately 146W at 600K exhaust temperatures, supporting hybrid and electric vehicle architectures. As highlighted by the International Energy Agency, rapid EV adoption further expands opportunities, with TEGs powering auxiliary systems and aiding compliance with global fuel economy standards.

Restraints - High Material and Production Costs Limit Widespread Adoption

Thermoelectric generators rely heavily on specialty materials such as bismuth telluride and tellurium, creating cost pressures and supply risks. The U.S. Geological Survey reports annual global bismuth production of roughly 8,500 tons, reflecting constrained availability despite recent output increases. Limited material supply directly influences module pricing and long-term procurement stability.

According to the U.S. Department of Energy, TEG systems typically cost between US$50-100 per kW, with return on investment periods extending to 5-7 years compared to competing waste heat recovery technologies. Dependence on tellurium further complicates supply chains, especially amid growing demand from solar and semiconductor industries.

Limited Commercial Efficiency and Scalability Challenges

Despite technological progress, commercial thermoelectric generators generally achieve only 5-8% conversion efficiency, limiting competitiveness against alternative heat-to-power systems. The U.S. Department of Energy notes performance scalability constraints, particularly beyond 1 kW output, restricting deployment in large-scale industrial operations.

Long-term durability also remains a concern, with studies indicating up to 20% performance degradation after 10,000 operating hours under continuous thermal stress. Thermal mismatch between materials and fluctuating heat sources further reduces system stability, hindering broader adoption in high-capacity and variable-temperature industrial environments.

Opportunity - Expanding Role in EV Auxiliary Power Systems

Rapid electric vehicle adoption is creating strong opportunities for thermoelectric generators in auxiliary power applications. The International Energy Agency projects EVs could account for nearly 60% of global vehicle sales by 2030, increasing demand for efficiency-enhancing technologies. TEGs can extend driving range by 5-10% by converting residual thermal energy into 300-600W of supplemental power.

Policy incentives under European decarbonization frameworks and prototype developments by BMW and Toyota validate commercial feasibility. As premium EV manufacturers prioritize range optimization and energy efficiency, auxiliary heat recovery systems present a multi-billion-dollar growth avenue through 2033.

Rising Demand for IoT and Wearable Energy Harvesting

The proliferation of connected devices is unlocking new markets for low-power thermoelectric harvesting. With an estimated 25 billion IoT devices globally by 2025, demand for maintenance-free, off-grid energy solutions is rising. Research highlighted by IEEE and DARPA shows TEGs can generate around 100μW/cm² from body heat, enabling wearable and sensor-based applications.

The GSMA and the United Nations report nearly 800 million people remain without reliable electricity access, expanding opportunities in remote healthcare monitoring and telecom infrastructure. These decentralized, low-power segments offer scalable and high-growth commercialization potential for TEG technologies.

Category-wise Analysis

Material Insights

Bismuth Telluride leads the thermoelectric materials segment, accounting for nearly 60% share in 2025 due to its optimal figure of merit (ZT 1.0-1.2) within the 200-400°C temperature range. The U.S. Department of Energy and National Renewable Energy Laboratory recognize its strong mid-temperature performance across automotive exhaust recovery and consumer electronics. Mature manufacturing processes, established supply chains, and improving recycling initiatives further strengthen its commercial dominance despite tellurium dependency risks.

Magnesium Silicide is emerging as the fastest-growing material segment due to its lower cost, environmental compatibility, and suitability for higher-temperature industrial waste heat applications. Research institutions and industrial developers are increasingly investing in silicon-based and eco-friendly compounds to reduce reliance on scarce elements. Advancements in nanostructuring and alloy engineering are enhancing performance stability, positioning alternative materials as promising next-generation solutions.

Application Insights

Waste heat recovery dominates the application segment with over 50% market share, driven by its direct ability to capture industrial heat losses that range between 20-50%, according to the International Energy Agency. Policy mechanisms such as the European Union Emissions Trading System encourage efficiency upgrades, while pilot installations demonstrating outputs above 115kW validate commercial feasibility. Reliability and low maintenance make TEGs attractive for continuous industrial operations.

Energy Harvesting is emerging as the fastest-growing application, fueled by the expansion of IoT devices, wearable electronics, and remote monitoring systems. Compact thermoelectric modules capable of operating across small temperature gradients are gaining traction in decentralized power solutions. Growing demand for autonomous sensors and low-maintenance energy systems in telecom, healthcare, and smart infrastructure is accelerating innovation in micro-scale TEG deployment.

Industry Insights

Automotive accounts for approximately 35% of total market share, primarily driven by exhaust heat recovery integration to enhance vehicle efficiency. Testing by SAE International and validation from the U.S. Environmental Protection Agency highlight measurable power gains of up to 53% when combined with heat pipe technologies. Regulatory pressure to reduce fuel consumption and emissions further strengthens automotive sector dominance.

Energy & Utilities is emerging as the fastest-growing industry segment as utilities seek decentralized and waste heat-based generation solutions. Power plants, refineries, and distributed energy facilities are increasingly deploying TEG systems to improve operational efficiency. As global decarbonization targets intensify, integration of solid-state heat recovery systems into grid and off-grid infrastructure is expected to accelerate adoption across energy-intensive sectors.

Regional Insights

North America Thermoelectric Generators Market Trends

North America accounts for approximately 38% of the global thermoelectric generators market share, led by strong R&D investments and supportive policy frameworks. The U.S. Department of Energy, through ARPA-E, allocated nearly US$50 million in 2024 for advanced TEG research, while the Inflation Reduction Act offers 30% tax credits encouraging automotive integration. NASA continues to deploy high-ZT materials in space missions, reinforcing innovation leadership.

A robust ecosystem of startups and research labs, particularly in Silicon Valley, is pushing prototype efficiencies toward 15%. Strong collaboration between national laboratories, universities, and automakers supports commercialization. Increasing adoption in industrial waste heat recovery and aerospace further consolidates the region’s technological and revenue dominance.

Europe Thermoelectric Generators Market Trends

Europe is projected to grow at a CAGR of approximately 10% through 2033, supported by aggressive decarbonization mandates. Germany leads innovation, with Fraunhofer-Gesellschaft demonstrating refinery heat recovery systems achieving up to 10% conversion gains. The European Commission’s Green Deal targets 55% emission reductions by 2030, driving industrial energy-efficiency upgrades across member states.

Countries such as the U.K. and France are advancing aerospace collaborations under the European Space Agency, while Spain’s manufacturing output growth strengthens regional deployment. Regulatory alignment and carbon pricing mechanisms continue to create a favorable environment for thermoelectric integration across automotive and heavy industries.

Asia Pacific Thermoelectric Generators Market Trends

Asia Pacific holds nearly 30% of the global market share and represents one of the fastest-expanding regions. China’s electric vehicle policies under the Ministry of Industry and Information Technology encourage waste heat recovery innovation, with companies like BYD testing thermoelectric prototypes. Rapid industrialization further strengthens adoption across manufacturing and power sectors.

Japan remains a materials innovation hub, led by firms such as Sumitomo Electric Industries, advancing high-performance thermoelectric compounds. Meanwhile, India and ASEAN economies are expanding industrial infrastructure, accelerating demand for energy-efficient technologies. Growing EV penetration and manufacturing scale are expected to sustain long-term regional growth momentum.

Competitive Landscape

The thermoelectric generators market is moderately consolidated, with leading players collectively accounting for a significant portion of global revenues. Competition centers on intensive R&D investments aimed at improving material performance beyond ZT>2 and enhancing conversion efficiency. Companies are expanding manufacturing footprints in Asia to optimize costs and strengthen supply chain resilience. Product differentiation increasingly focuses on customized modules tailored for automotive, industrial, and aerospace applications, enabling higher reliability in demanding thermal environments.

Business models are also evolving, with providers offering waste heat recovery-as-a-service solutions to reduce upfront capital burdens for end users. Strategic collaborations, pilot deployments, and long-term industrial contracts are becoming key competitive strategies.

Key Market Developments

- In March 2025, Ferrotec Holdings introduced advanced skutterudite-based thermoelectric modules engineered for industrial waste heat recovery, achieving conversion efficiencies of around 12% and targeting high-temperature manufacturing environments requiring durable, scalable, and performance-optimized heat-to-power solutions.

- In July 2024, Gentherm expanded its automotive thermoelectric generator production capacity by adding approximately 50,000 square feet of manufacturing space to support rising demand for vehicle exhaust heat recovery integration.

- In November 2023, Laird Thermal Systems launched high-temperature thermoelectric modules designed for aerospace and defense applications, offering enhanced durability, thermal stability, and reliable power generation in extreme operating conditions.

Companies Covered in Thermoelectric Generators Market

- Gentherm Inc.

- Ferrotec Corporation

- II-VI Marlow

- Laird Thermal Systems

- Tecteg Power Generator

- Tellurex Corporation

- Thermonamic Electronics Corp. Ltd.

- Hi-Z Technology Inc.

- KELK Ltd.

- RMT Ltd.

- Global Thermoelectric Inc.

- GreenTEG AG

- Micropelt GmbH

- Komatsu Ltd.

- Cristopia Energy Systems

Frequently Asked Questions

The global Thermoelectric Generators market is valued at US$ 1.2 billion in 2026.

Demand is primarily driven by waste heat recovery, capturing 20-50% industrial energy losses as highlighted by the U.S. Department of Energy.

Bismuth Telluride leads with approximately 60% market share due to its superior ZT performance in mid-temperature applications.

North America leads with around 38% market share, supported by strong R&D and policy incentives.

EV integration presents a major opportunity, enabling 5-10% vehicle range extension alongside rising global EV adoption.

Key players include Gentherm, Ferrotec Holdings, and Laird Thermal Systems.