- Power Generation, Transmission, & Distribution

- Electric Sub-meter Market

Electric Sub-meter Market Size, Share, and Growth Forecast, 2025 - 2032

Electric Sub-meter Market By Product Type (Electronic Sub-Meters, Other), Phase Type (Single Phase, Three Phase), Application (Commercial Establishments, SML Retail Stores, Data Centers, Industrial Sector, Others) and Regional Analysis for 2025 - 2032

Electric Sub-meter Market Size and Trends Analysis

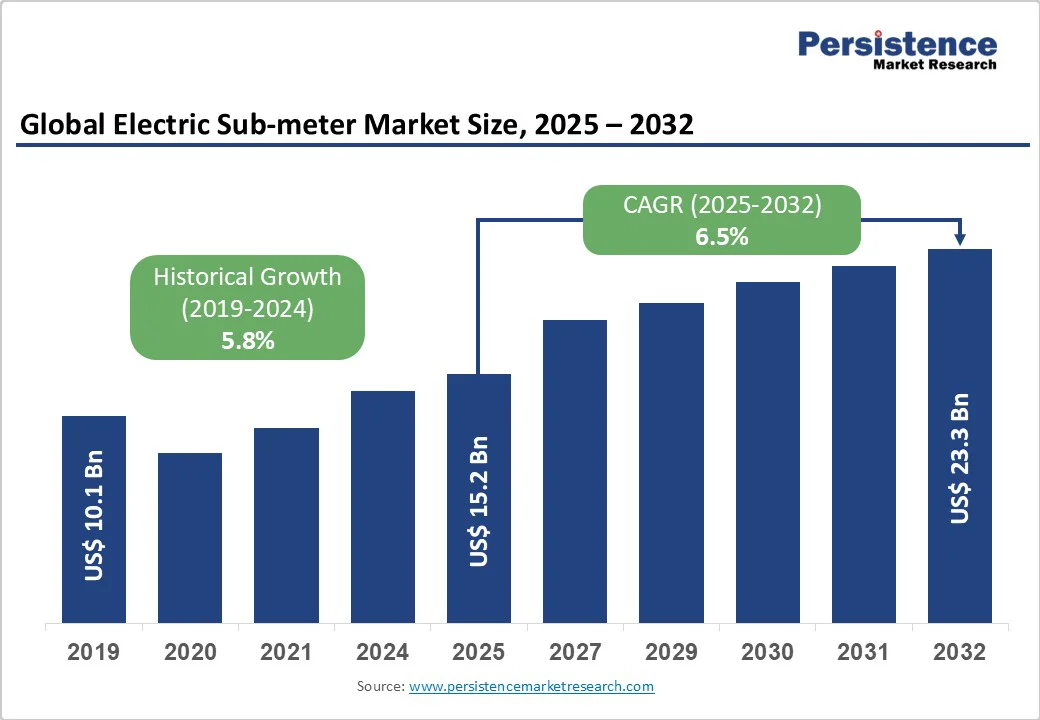

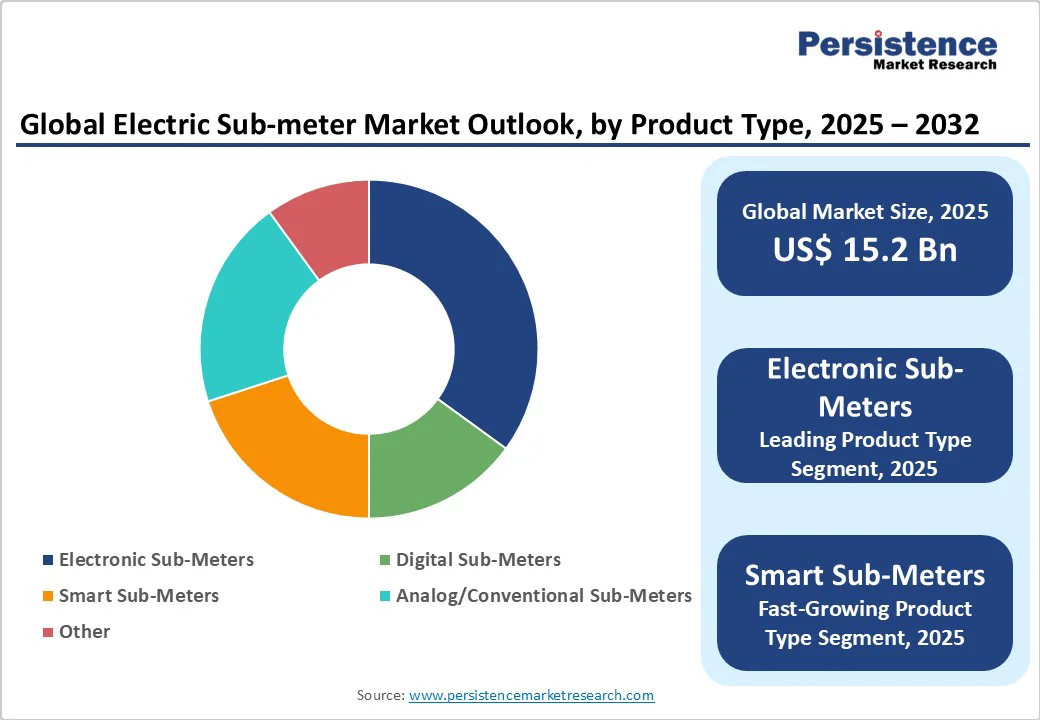

The global electric sub-meter market is expected to reach US$15.2 billion in 2025. It is expected to reach US$23.3 billion by 2032, growing at a CAGR of 6.5% during the forecast period from 2025 to 2032, driven by increasing urbanization, rising energy costs, and the critical need for accurate energy monitoring systems that enable cost allocation, waste reduction, and operational optimization across multi-tenant buildings and industrial facilities.

Key Industry?Highlights

- Product Segments: Electronic sub-meters hold a 32.1% market share in 2025, driven by reliability, cost efficiency, and broad industrial use. Smart sub-meters represent the fastest-growing segment, boosted by IoT connectivity, remote monitoring, and data-driven energy management.

- Phase Configuration Segments: Three-phase sub-meters are anticipated to lead with a 58.2% share, driven by demand in high-load commercial and industrial applications. Single-phase sub-meters are the fastest-growing, driven by rising adoption in residential and small-business settings for energy efficiency and cost control.

- Application Segments: Commercial establishments hold a 28.4% share, driven by tenant billing needs, energy code compliance, and performance benchmarking. The industrial sector is experiencing the fastest growth, driven by process optimization, smart factory adoption, and energy cost management.

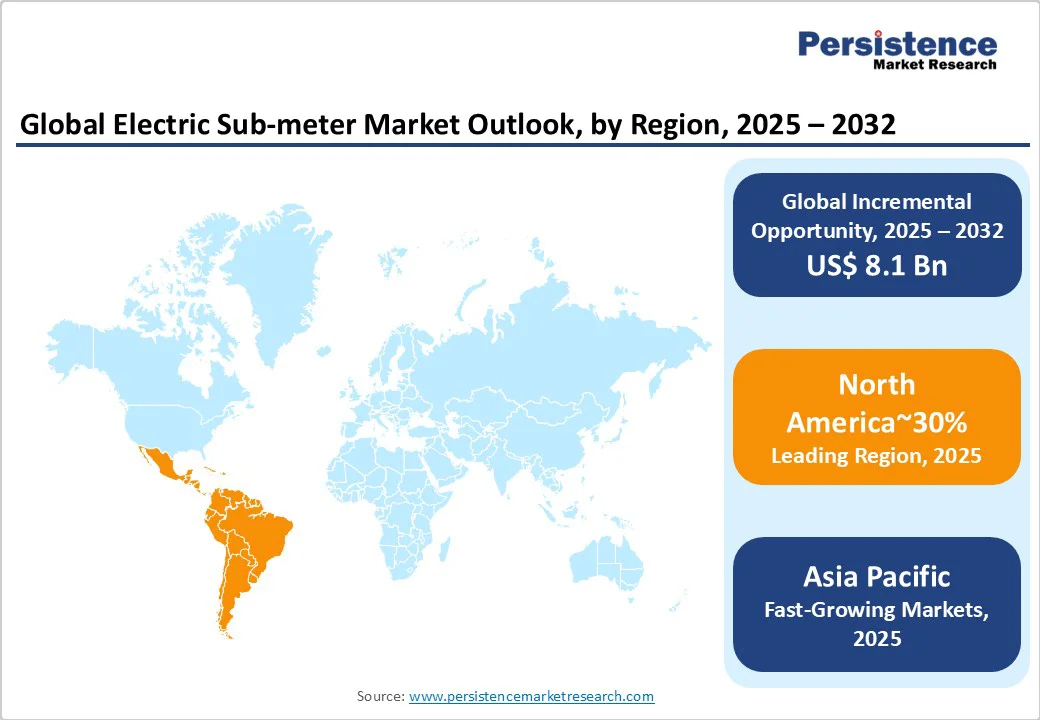

- Regional Leaders: North America leads with a 31% market share valued at US$4.7 billion, supported by mature infrastructure, regulatory mandates, and sustainability-driven retrofitting projects. Asia Pacific is the fastest-growing region, projected to expand at a 7.8% CAGR through 2032, driven by rapid urbanization, manufacturing growth, and government-backed energy efficiency programs.

| Key Insights | Details |

|---|---|

|

Electric Sub-meter Market Size (2025E) |

US$15.2 Bn |

|

Market Value Forecast (2032F) |

US$23.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Stringent Energy Efficiency Regulations and Compliance Requirements

Global regulations are driving strong market growth through mandatory energy-monitoring standards. ASHRAE 90.1 requires separate tracking of building systems and tenant usage, with data recorded every 15 minutes. The EU’s Energy Efficiency Directive targets a 32.5% improvement in efficiency by 2030, boosting sub-meter adoption for compliance.

In the U.S., the DOE’s Energy Star program has supported over 70 million smart meter installations. These policies create non-discretionary demand as building owners and facility managers deploy sub-metering systems to meet regulatory requirements, enhance efficiency, and avoid penalties, ensuring steady long-term market expansion worldwide.

Rapid Urbanization and Infrastructure Development

Rising global urbanization is driving strong demand for energy management solutions in multi-tenant and commercial buildings. The world’s population reached 8 billion in 2022 and is projected to hit 9.7 billion by 2050, with Asia Pacific accounting for 60% of this growth. This expansion fuels large-scale construction of residential, commercial, and industrial facilities requiring advanced energy monitoring.

Developers increasingly integrate sub-metering systems during construction to ensure accurate tenant billing, minimize disputes, and enhance energy efficiency. Rapid urban development across China, India, and ASEAN nations presents significant growth opportunities for sub-meter manufacturers and system integrators in emerging markets.

Barrier Analysis - High Initial Installation and Infrastructure Costs

High upfront costs hinder sub-meter adoption, especially for smart and IoT-enabled systems. Installation can cost US$500–US$2,000 per unit, while retrofitting older buildings demands electrical upgrades and downtime. These financial and technical challenges restrict deployment in established urban areas with outdated infrastructure, limiting overall market penetration.

Technical Integration Challenges and Compatibility Issues

The absence of standardized protocols and interoperability among sub-meter brands hinders integration with building management systems and utility networks. IoT-enabled models raise cybersecurity and data privacy concerns, while limited technical expertise, especially in developing regions, restricts adoption. These challenges increase reliance on specialized support, raising ownership costs and operational complexity for facility managers.

Barrier Analysis - Renewable Energy Integration and Grid Modernization

The global transition toward renewable energy sources creates significant opportunities for advanced sub-metering solutions supporting distributed energy systems and microgrid implementations. Electric sub-meters enable precise measurement and monitoring of renewable energy generation, consumption, and grid interaction, supporting net metering programs and energy trading platforms. Smart grid modernization initiatives require sophisticated monitoring capabilities for demand-side management, load balancing, and real-time energy optimization. The renewable energy integration market represents approximately US$1.5 billion in additional sub-meter demand through 2030, driven by solar panel installations, battery storage systems, and electric vehicle charging infrastructure requiring detailed energy monitoring capabilities.

Emerging Market Expansion and Smart City Development

Rapid economic development in the Asia Pacific, Latin America, and the Middle East regions presents substantial growth opportunities for sub-meter manufacturers. Countries including China, India, Brazil, and the UAE are implementing smart city initiatives requiring comprehensive energy management infrastructure. Government incentives and policies supporting energy efficiency programs create favorable conditions for sub-meter adoption in emerging markets. The availability of low-cost manufacturing capabilities in the Asia Pacific enables competitive pricing strategies supporting mass market adoption. Emerging markets collectively represent over US$800 million in additional market opportunity through 2032, driven by urbanization, infrastructure development, and increasing environmental awareness.

Category-wise Analysis

Product Type Insights

Electronic sub-meters hold 32.1% of the global market share, supported by their reliability, accuracy, and cost efficiency. These systems feature digital measurement circuits and data logging functions, enabling precise energy tracking across residential, commercial, and industrial sectors. Their durability, low maintenance needs, and compatibility with building management systems make them a preferred choice among utilities and facility operators.

Smart sub-meters are the fastest-growing segment, driven by rising demand for IoT connectivity and real-time data analytics. Equipped with wireless communication, cloud integration, and mobile interfaces, they enable remote monitoring and automated energy reporting. Enhanced with demand response, predictive maintenance, and optimization features, smart sub-meters are gaining traction due to falling hardware costs, longer battery life, and improved cybersecurity, marking a key shift toward intelligent, data-driven energy management solutions.

Phase Type Insights

Three-phase sub-meters dominate the market with a 58.2% share, driven by their extensive use in commercial, industrial, and multi-residential infrastructures with high energy demands. These meters provide precise monitoring, load balancing, and improved energy efficiency for heavy-duty applications, including manufacturing plants, data centers, and hospitals. Growing industrialization and increased investment in commercial infrastructure continue to boost demand for advanced three-phase solutions. Single-phase sub-meters are the fastest-growing segment, supported by rapid residential and small-scale commercial expansion. Ideal for apartments, small offices, and retail units, they offer affordable, easy-to-install energy tracking, driven by rising consumer awareness and regulatory focus on accurate tenant billing.

Commercial establishments hold 28.4% of the market share, largely due to widespread sub-meter deployment in offices, retail centers, hotels, and mixed-use buildings for tenant billing and energy management. The industrial sector is the fastest-growing application, with manufacturing, data centers, and process industries adopting sub-meters for granular energy tracking, cost optimization, and sustainability. Industry 4.0 adoption, rising energy costs, and environmental regulations further accelerate this growth, promoting detailed consumption reporting and predictive maintenance.

Regional Insights

North America Electric Sub-meter Market Trends

North America dominates the global market with a 31.0% share, valued at approximately US$4.7 billion in 2025, and is projected to reach US$7.2 billion by 2032. The U.S. anchors regional leadership, supported by mature energy regulations, advanced building infrastructure, and strong adoption of efficiency-driven initiatives. Standards such as ASHRAE 90.1, Energy Star, and state-level mandates sustain consistent demand across commercial, residential, and industrial sectors.

The region benefits from a robust manufacturer base, well-established distribution channels, and a skilled workforce. Major metropolitan areas, including New York, California, and Texas, enforce stringent energy monitoring policies for large buildings. Ongoing smart grid modernization, renewable integration, and IoT-enabled metering adoption continue to propel market expansion through digitalization and performance optimization.

Europe Electric Sub-meter Market Trends

Europe holds a strong position in the market with approximately 25% share, valued at US$3.8 billion in 2025 and projected to reach US$5.8 billion by 2032. Leading countries, including Germany, the U.K., and France, are driving adoption through stringent EU Energy Efficiency Directives, carbon-reduction targets, and smart city initiatives. The EU’s mandate for a 32.5% efficiency improvement by 2030 fuels the widespread deployment of advanced energy monitoring systems across the commercial and residential sectors.

The region benefits from renewable energy integration, building renovation programs, and modernization of district heating systems. A harmonized regulatory framework emphasizing interoperability, data protection, and standardized performance criteria supports technological innovation. Competitive dynamics feature established European manufacturers and global entrants investing in smart grids, automation, and IoT-enabled sub-metering technologies to enhance energy transparency and sustainability.

Asia Pacific Electric Sub-meter Market Trends

Asia Pacific stands out as the fastest-growing regional market, projected to grow at a 7.8% CAGR through 2032, driven by industrialization, urbanization, and robust government-led energy efficiency programs. China, Japan, and India dominate regional demand, driven by large-scale infrastructure projects, smart city development, and expanding manufacturing. The region benefits from cost-efficient production, a large consumer base, and rising residential and commercial construction supported by economic growth.

Governments across China and India are implementing national energy efficiency mandates, building codes requiring sub-metering, and smart grid modernization initiatives, fostering strong market potential. Japan leads in IoT and AI-enabled sub-metering systems, reflecting its focus on technology and sustainability. Competitive dynamics combine global OEMs and local manufacturers expanding through regional partnerships, capacity investments, and customized low-cost solutions tailored to diverse market needs across developing economies.

Competitive Landscape

The global electric sub-meter market exhibits moderate concentration with leading players maintaining significant market positions through comprehensive product portfolios, established distribution networks, and technological capabilities. Schneider Electric, Siemens AG, and Landis+Gyr AG command substantial market shares through international presence, innovation leadership, and strategic partnerships with utility companies and building developers.

The market structure includes multinational corporations, specialized metering companies, and regional players competing across different price segments and application areas. Market concentration analysis reveals opportunities for consolidation as companies seek scale advantages, technology integration, and geographic expansion capabilities.

Key Industry Developments

- In August 2025, Kerala State Electricity Board (KSEB) launched a dedicated sub-division to oversee smart electricity metering across the state. This unit aims to ensure efficient deployment, monitoring, and management of advanced metering, boosting energy efficiency, billing accuracy, and supporting KSEB’s digitalization and sustainable energy goals.

- In September 2024, Trilliant Holdings Inc. partnered with Milton Hydro Services Inc. to launch a community-wide sub-metering initiative using Trilliant’s Smart Building platform. This collaboration aims to enhance customer experience and promote energy savings by providing innovative energy management solutions that support efficient consumption and sustainability during the energy transition.

Companies Covered in Electric Sub-meter Market

- Schneider Electric

- Landis+Gyr

- Itron, Inc

- Siemens AG

- Honeywell International

- General Electric

- Mitsubishi Electric Corporation

- HPL Electric & Power Limited

- ABB

- Osaki Electric Co. Ltd

- Xylem Inc

- BENTEC India Ltd

- Genus Power Infrastructures Ltd

- Socomec

- Leviton Manufacturing Company

Frequently Asked Questions

The electric sub-meter market is estimated to be valued at US$15.2 Billion in 2025.

The electric sub-meter market is driven by the growing need for precise energy monitoring to enhance efficiency, reduce costs, and ensure sustainability compliance across commercial, industrial, and residential sectors.

In 2025, the North America region will dominate the market with an exceeding 30% revenue share in the electric sub-meter market.

Among the product types, electronic sub-meters hold the highest preference, capturing beyond 32.1% of the market revenue share in 2025, surpassing other parts.

The key players in the electric sub-meter market include Schneider Electric, Landis+Gyr, Itron, Inc., and Siemens AG.