- Automotive Components & Materials

- Automotive Timing Cover Market

Automotive Timing Cover Market Size, Share, and Growth Forecast, 2025 - 2032

Automotive Timing Cover Market by Vehicle Type (Two Wheelers, Passenger Cars and Commercial Vehicles), by Material Type (Metal and Alloys, Polycarbonate, Plexiglass and Carbon Fiber), by Sales Channel (Original Equipment Manufacturers (OEMs), and Aftermarket) and Regional Analysis for 2025 - 2032

Automotive Timing Cover Market Size and Trends Analysis

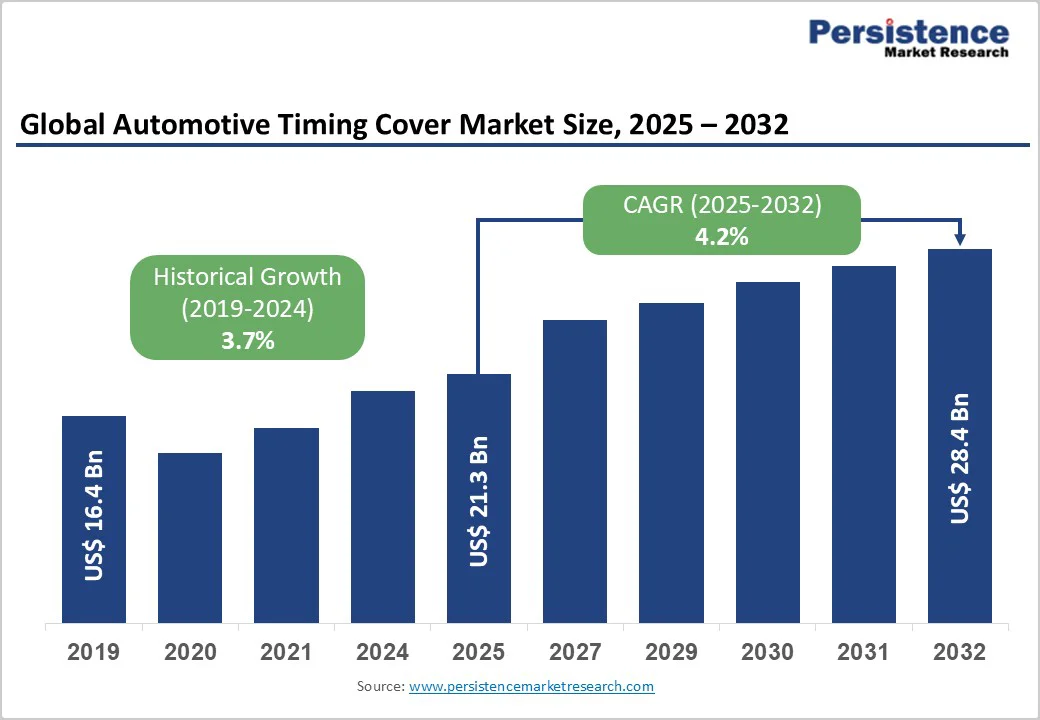

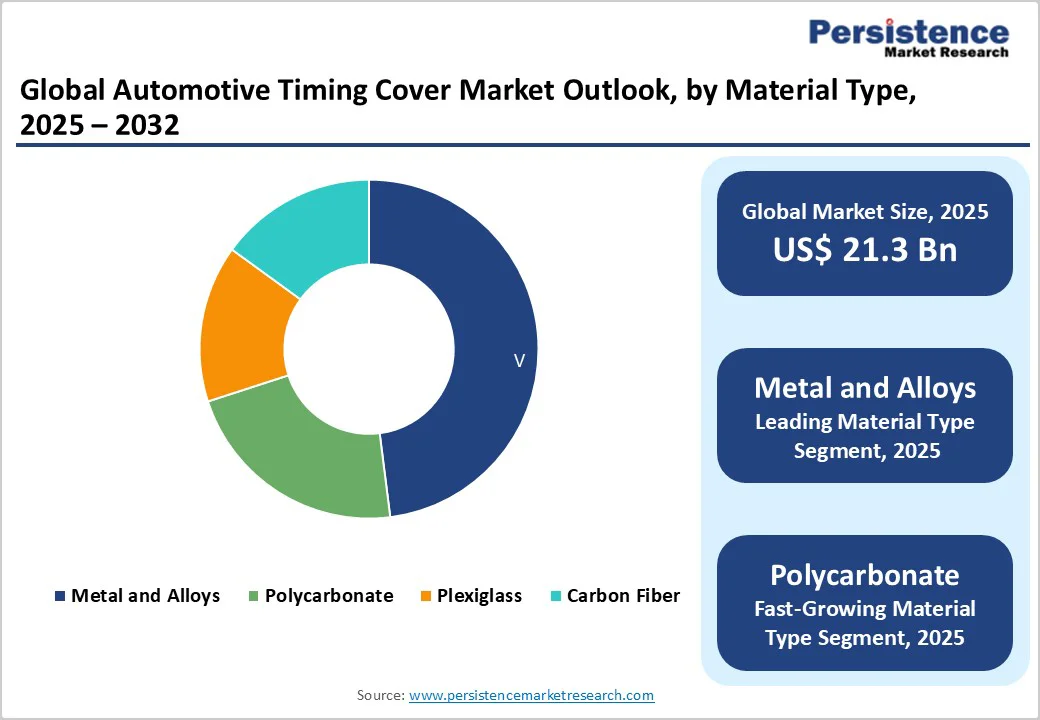

The global automotive timing cover market size was valued at US$ 21.3 billion in 2025 and is projected to reach US$ 28.4 billion by 2032, growing at a CAGR of 4.2% between 2025 and 2032. Timing covers representing critical engine components accounting for approximately 19% of global engine components market value serve essential protective function housing timing chains, gears, and synchronization mechanisms preventing contamination while maintaining precise valve-to-piston coordination.

Key Industry Highlights:

- Vehicle Segment Dynamics: Passenger cars dominate the market with 56.6% share, supported by the highest global production volumes across mainstream OEMs. Two-wheelers represent the fastest-growing segment (8–12% CAGR), driven by Asia Pacific expansion, particularly India, which produces 20+ million units annually, creating strong timing-cover demand.

- Material Leadership Trends: Metal and alloy timing covers command a 43.5% material share due to proven durability, heat resistance, and long-standing OEM preference. Polycarbonate emerges as the fastest-growing material (10–14% CAGR), offering weight reduction, lower manufacturing costs, and compliance with automotive lightweighting and fuel-efficiency mandates.

- Sales Channel Performance: OEM channel leads with 64.2% share, driven by direct integration into new vehicle production lines and long-term supplier partnerships. The aftermarket is the fastest-growing channel (6–8% CAGR) as aging vehicle fleets and expanding e-commerce platforms enhance replacement part accessibility

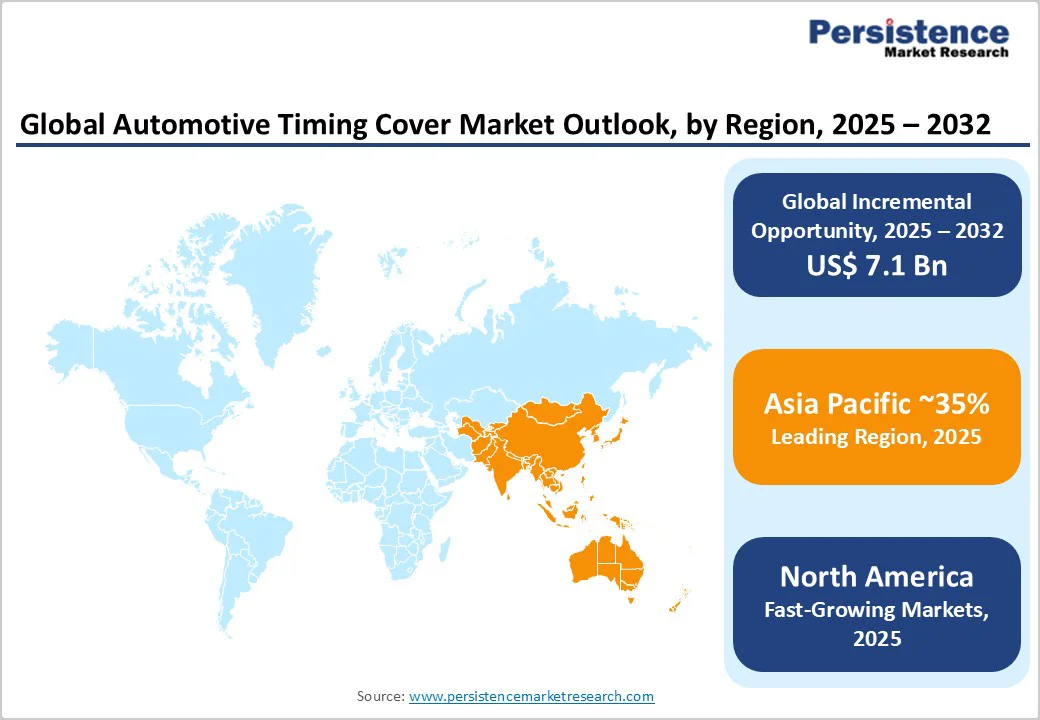

- Regional Growth Patterns: Asia Pacific dominates with 40% global share and 8.2% CAGR, led by China contributing 46% of regional output with over 26 million vehicles produced, and India recording 10% CAGR. North America accounts for 23% share at 5.1% CAGR, while Europe holds 21% at 4.8% CAGR, supported by premium vehicle manufacturing strength.

- Competitive and Innovation Landscape: MAHLE leads with 15% market share, supported by extensive global OEM relationships. Key competitors such as ElringKlinger, Dana, and Röchling maintain strong positions. Polycarbonate timing covers represent the fastest-advancing innovation, achieving cost competitiveness and supporting OEM lightweighting objectives across ICE and hybrid platforms.

| Report Attribute | Details |

|---|---|

|

Automotive Timing Cover Market Size (2025E) |

US$ 21.3 Bn |

|

Market Value Forecast (2032F) |

US$ 28.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.7% |

Market Dynamics

Growth Drivers

Rising Global Vehicle Production and Passenger Car Dominance

Automotive industry recovery post-pandemic with global vehicle production exceeding 90 million units annually and passenger cars representing 70+ million units creates sustained baseline demand for timing covers as essential engine components universally specified across internal combustion engine architectures. Passenger car segment commanding 56.6% market share reflects largest production volumes with established OEM supply relationships, multi-decade vehicle lifespan creating aftermarket replacement cycles, and regional market expansion particularly across Asia Pacific where vehicle ownership rates increase proportionally with rising middle-class affluence.

Asia Pacific region representing most attractive market with projected absolute dollar opportunity exceeding US$1.9 billion reflects China's position as world's largest automotive manufacturer producing 26+ million vehicles annually, India's rapidly expanding automotive sector, and ASEAN nations' growing manufacturing bases supporting regional and export production.

Lightweight Material Innovation and Fuel Efficiency Regulatory Mandates

Automotive industry lightweighting initiatives compelled by global fuel efficiency regulations including EU 95g CO2/km standards and Corporate Average Fuel Economy (CAFE) requirements drive accelerating adoption of advanced polycarbonate, composite, and carbon fiber timing covers achieving 40-60% weight reduction versus traditional cast aluminum alternatives. Polycarbonate timing covers representing fastest-growing material segment achieving cost-effectiveness combined with 30-50% weight savings enable automotive manufacturers to achieve meaningful vehicle mass reductions contributing to overall fuel economy improvements, with every 10% vehicle weight reduction translating to 6-8% fuel efficiency gain supporting regulatory compliance.

Advanced thermoplastic materials including reinforced polypropylene and polyamide increasingly specified for timing covers deliver superior thermal resistance, design flexibility enabling complex integrated geometries, and recyclability aligning with circular economy objectives while maintaining structural integrity and durability requirements. Composite timing covers incorporating fiber-reinforced polymers achieve exceptional strength-to-weight ratios enabling premium vehicle applications where performance characteristics justify 20-35% cost premiums, with carbon fiber variants commanding further price advantages through superior thermal stability and vibration dampening characteristics.

Market Restraints

Supply Chain Complexity and Raw Material Cost Volatility

Automotive timing cover manufacturing dependent on aluminum alloy, polycarbonate resin, and specialty composite material sourcing faces commodity price fluctuations and supply chain disruptions affecting production costs and pricing stability, with aluminum demonstrating 20-30% annual price volatility correlated with global commodity markets. Polycarbonate and engineering thermoplastic supply chains concentrated among limited producers including Covestro, SABIC, and regional suppliers create procurement dependencies constraining manufacturer flexibility and exposing smaller tier suppliers to significant margin compression during material cost escalation periods.

COVID-19 pandemic highlighting supply chain fragility with semiconductor shortages causing automotive production disruptions demonstrates timing cover market vulnerability to broader automotive industry supply constraints affecting demand predictability and inventory management. Geographic concentration of automotive component manufacturing in Asia Pacific creates logistics complexity and tariff exposure for North American and European automotive manufacturers increasingly prioritizing supply chain resilience and regional sourcing strategies.

Technology Transition Risks from Internal Combustion to Electric Powertrains

Automotive industry electrification trajectory with battery electric vehicles projected to represent 50% of new vehicle sales by 2035 in developed markets creates structural uncertainty for timing cover demand as pure electric architectures eliminate traditional timing systems entirely, constraining long-term market growth potential. Hybrid vehicle architectures maintaining internal combustion components provide transitional demand supporting timing cover market through 2030-2035 period, however eventual migration toward pure EV platforms represents existential challenge requiring market participants to diversify product portfolios toward electric powertrain components or face revenue decline. Timing cover manufacturers lacking strategic positioning in electric vehicle component supply chains risk market marginalization as automotive industry capital allocation prioritizes electrification technology development over traditional powertrain component innovation.

Market Opportunities

Two-Wheeler Market Expansion in Emerging Economies

Rapidly growing two-wheeler segment particularly across India, Indonesia, Vietnam, and Sub-Saharan Africa experiencing 8% annual production growth creates substantial timing cover opportunity as motorcycles and scooters universally require timing system protection while demonstrating higher replacement frequency than passenger vehicles. India two-wheeler market producing 20+ million units annually represents single largest segment opportunity with domestic manufacturers including Hero MotoCorp, Bajaj Auto, and TVS Motor Company specifying timing covers across comprehensive product portfolios from economy to premium motorcycles.

Electric two-wheeler adoption accelerating across Asia creates mixed dynamics where traditional timing cover demand continues for internal combustion models while manufacturers develop lightweight covers for hybrid scooter platforms maintaining small displacement engines supplemented by electric assist. Two-wheeler aftermarket demonstrating robust growth through independent mechanics, parts distributors, and growing e-commerce penetration creates accessible market entry pathway for timing cover suppliers targeting price-sensitive segments.

Advanced Manufacturing Technologies and Precision Engineering

Additive manufacturing adoption enabling rapid prototyping and small-batch production of timing covers supports automotive industry trend toward platform diversification and regional market customization, with 3D printing reducing development timelines 40-60% versus traditional tooling approaches. Precision injection molding advances enabling tighter tolerances and complex geometries integrated directly into timing cover designs reduce assembly complexity and enable acoustic dampening features previously requiring multi-component solutions, supporting OEM preference for integrated designs reducing assembly costs 15-25%.

Surface treatment innovations, including plasma coating and nano-ceramic applications enhance timing cover durability and oil resistance extending service life 30-50% justifying premium pricing for commercial vehicle and heavy-duty applications, where extended maintenance intervals generate operational savings.

Category-wise Analysis

Vehicle Type Insights

Passenger cars hold a 56.6% market share, driven by global production exceeding 70 million units, universal timing cover requirements, and long-standing OEM supplier relationships. High-volume compact and mid-size segments ensure strong scale economies, while luxury brands increasingly adopt lightweight polycarbonate covers to meet performance and efficiency targets.

Two-wheelers represent the fastest-growing segment at 8% CAGR, supported by rapid expansion in Asia Pacific, where motorcycles and scooters are primary transportation modes. India alone produces over 20 million two-wheelers annually, creating substantial demand. Rising electric two-wheeler adoption further supports lightweight timing cover development. Aftermarket demand remains strong due to higher replacement frequency from intensive usage and cost-conscious maintenance practices, sustaining recurring revenue opportunities.

Material Type Insights

Metal and alloy timing covers dominate with a 43.5% market share due to proven durability, established production infrastructure, and long-standing OEM validation across high-temperature and high-vibration environments. Cast aluminum remains the largest segment, offering an ideal balance of strength, weight, and thermal conductivity for passenger and commercial vehicles. Steel covers serve heavy-duty and off-highway applications where maximum impact resistance is required. Polycarbonate is the fastest-growing material at 10–14% CAGR, driven by lightweighting mandates and 20% cost advantages over aluminum. Offering 40% weight reduction and strong design flexibility, polycarbonate supports integrated geometries and reduced assembly complexity. Reinforced formulations now withstand 150–180°C continuous temperatures, enabling wider adoption in modern high-performance engines.

Sales Channel Analysis

OEM sales channels dominate with 64.2% market share, driven by new vehicle production volumes, long-term tier-1 supplier partnerships, and stable multi-year supply contracts. Major automakers such as Toyota, Volkswagen, GM, Ford, and Stellantis specify timing covers across extensive model portfolios, ensuring consistent baseline demand. OEM channels command higher margins due to strict quality certifications, JIT logistics, and warranty compliance, while collaborative engineering with suppliers like MAHLE, ElringKlinger, and Dana supports design optimization and production efficiency.

The aftermarket channel is the fastest-growing segment at 6% CAGR, supported by an aging global vehicle fleet and rising independent repair activity. Replacement demand increases as vehicles exceed 100,000–150,000 km, with e-commerce platforms expanding access and offering 30% lower prices than OEM dealers. Emerging markets further accelerate growth through cost-focused repair networks reliant on aftermarket components.

Regional Market Insights

North America Automotive Timing Cover Market Trends

North America generates approximately US$5.6 billion market value in 2025 representing 23% global market share growing at 5.1% CAGR through 2032, driven by established automotive manufacturing base, premium vehicle segment prevalence, and robust aftermarket supporting aging vehicle fleet. The United States dominates regional market with 70% North American share through automotive production exceeding 10 million units annually, extensive tier-1 supplier base including Dana and MAHLE maintaining regional manufacturing facilities, and aftermarket distribution networks serving independent repair shops nationwide.

U.S. light truck and SUV market commanding 80% domestic production preference drives timing cover specifications toward larger displacement engines requiring robust timing system protection, with commercial vehicle segment including Class 8 trucks representing specialized high-value applications. Canadian automotive sector contributing 13% regional share through integrated North American supply chains supporting cross-border component flows and USMCA trade agreement facilitating duty-free automotive parts exchange.

Europe Automotive Timing Cover Market Trends

Europe represents approximately US$4.5 billion market in 2025 capturing 21% global market share growing at 4.8% CAGR through 2032, characterized by premium automotive positioning, advanced material adoption, and stringent environmental regulations driving lightweighting initiatives. Germany leads European market with 30% regional share through automotive manufacturing excellence including BMW, Mercedes-Benz, Volkswagen, and Audi specifying advanced timing covers incorporating polycarbonate and composite materials supporting weight reduction objectives.

United Kingdom contributing 14% European share maintains automotive component manufacturing expertise through tier suppliers serving domestic and export markets, while Brexit considerations influence supply chain strategies and regulatory compliance frameworks. France, Italy, and Spain demonstrating steady growth through automotive manufacturing presence including Stellantis operations, Renault production facilities, and emerging electric vehicle manufacturing capacity requiring transitional timing cover demand for hybrid powertrains.

Asia Pacific Automotive Timing Cover Market Trends

Asia Pacific represents the dominant region at approximately 38% global market share with an estimated market value of US$11.1 billion by 2025, growing at 8.2% CAGR through 2032, driven by automotive manufacturing leadership, expanding two-wheeler production, and emerging market vehicle ownership growth. China dominates Asia Pacific with 42-46% regional share through automotive production leadership exceeding 26 million vehicles annually, established timing cover manufacturing capacity serving domestic OEMs and export markets, and government support for automotive industry modernization.

India emerges as a high-growth market at 11% regional share and 10-12% CAGR through expanding passenger car production from domestic OEMs Tata Motors and Mahindra, two-wheeler market leadership producing 20+ million units annually, and government "Make in India" initiatives supporting component manufacturing localization.

Competitive Landscape

Over the past decade, an increase in acquisitions and expansions has been witnessed to improve the supply of automotive components. Most market players are also focusing on enhancing the efficiency of automotive timing covers.

The emergence of new market players has also been seen in the global business. A few of the prominent players in the market include NITTO PERFORMANCE ENGINEERING PTY LTD, PROFORM, Spectre Performance, Holley Performance Products INC, Cloyes, and Dorman Products.

Key Industry Developments:

- In February 2024, Cloyes Gear & Products, Inc., a global manufacturer and designer of mission-critical timing drive systems and components for the automotive aftermarket, declared the acquisition of Automotive Tensioners, Inc., a leading supplier of front-end accessory drive pulling chains and tensioners to the automotive market.

- In December 2023, Dayco, a top provider of engine parts and drive systems to the auto, industrial, and aftermarket sectors, revealed that Tony Stewart Racing (TSR) has agreed to utilize Dayco's blower belts once more in the 2024 NHRA Mission Foods Drag Racing Series, following their successful collaboration in 2023.

- In September 2022, Aftermarket supplier BGA (BG Automotive) expanded its product offering with eight new references across various product categories – timing chain covers, camtrain, sump pans, crankshaft pulleys & transmission.

Companies Covered in Automotive Timing Cover Market

- NITTO PERFORMANCE ENGINEERING PTY LTD

- PROFORM

- Spectre Performance

- Holley Performance Products INC

- Cloyes

- Dorman Products

- Pioneer Automotive Industries

- Aisin Group

- KC Auto Products

- ICT Billet

- COMP Cams

- Moroso

- Ichiban Engineering

- Others Key Players

Frequently Asked Questions

The Automotive Timing Cover market is estimated to be valued at US$ 21.3 Bn in 2025.

The primary demand driver for the automotive timing cover market is the rising production of internal combustion engine (ICE) vehicles and the ongoing need for efficient engine sealing and protection systems.

In 2025, the Asia Pacific region will dominate the market with an exceeding 40% revenue share in the global Automotive Timing Cover market.

Among the Vehicle Type, Passenger Cars holds the highest preference, capturing beyond 56.6% of the market revenue share in 2025, surpassing other vehicles.

The key players in Automotive Timing Cover are NITTO PERFORMANCE ENGINEERING PTY LTD, PROFORM, Spectre Performance and Holley Performance Products INC