- Smart Packaging

- Automotive Tape Market

Automotive Tape Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Tape Market by Product Type (Specialty Tapes, Wire Harnessing Tapes, Others), Material (PVC, Polypropylene (PP), Others), Application, Adhesive Type, and Regional Analysis for 2026 - 2033

Automotive Tape Market Size and Trends Analysis

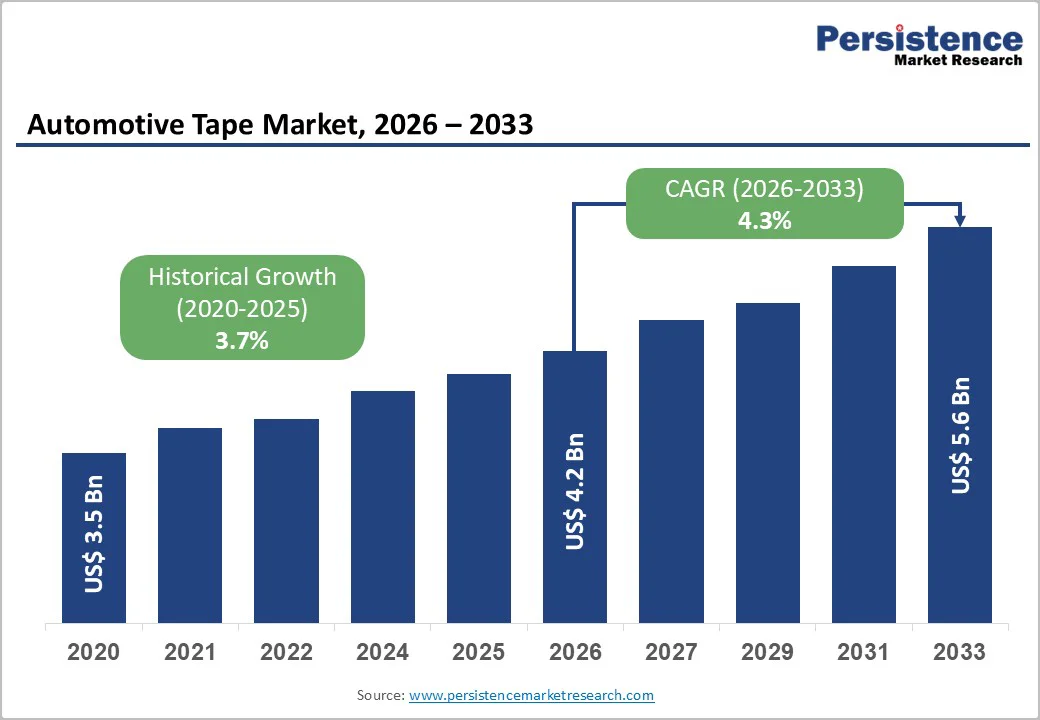

The global automotive tape market size is expected to be valued at US$4.2 billion in 2026, and is expected to reach US$5.6 billion by 2033, growing at a CAGR of 4.3% from 2026 to 2033, driven by steady expansion in electrification, rising adhesive-based bonding across vehicle platforms, and increased tape content per EV and hybrid vehicle.

Long-term demand is also shaped by lightweighting targets, strict quality and emission standards, and the ongoing shift away from mechanical fasteners. Supply-chain resilience and raw-material cost movements will influence year-to-year fluctuations around the baseline CAGR.

Key Industry Highlights

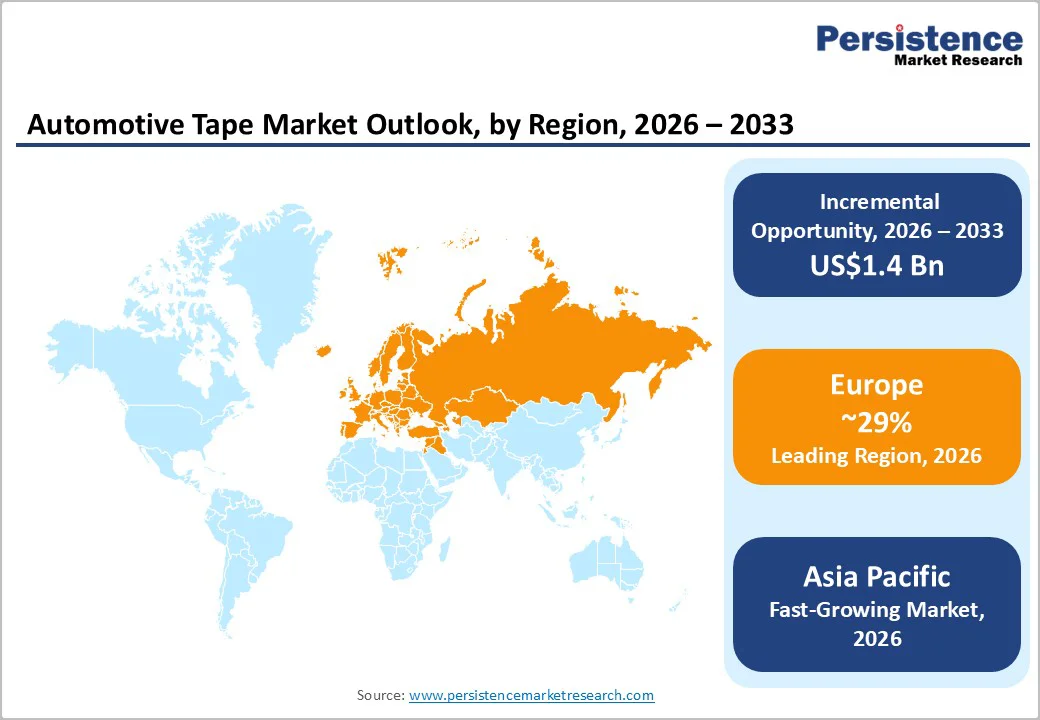

- Leading Region: Europe projected to lead the market with 29% share in 2026, driven by strong regulatory compliance, high vehicle production quality standards, and rapid adoption of advanced interior and electronics bonding technologies.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, expanding rapidly due to high-volume automotive manufacturing in China, Japan, India, and ASEAN markets, supported by EV investments and cost-efficient production systems.

- Investment Plans: Global manufacturers are increasing investments in thermal-management tapes, high-bond structural adhesives, PP-based lightweight tapes, and clean-room converting facilities to support EV platforms and electronics-heavy vehicle architectures.

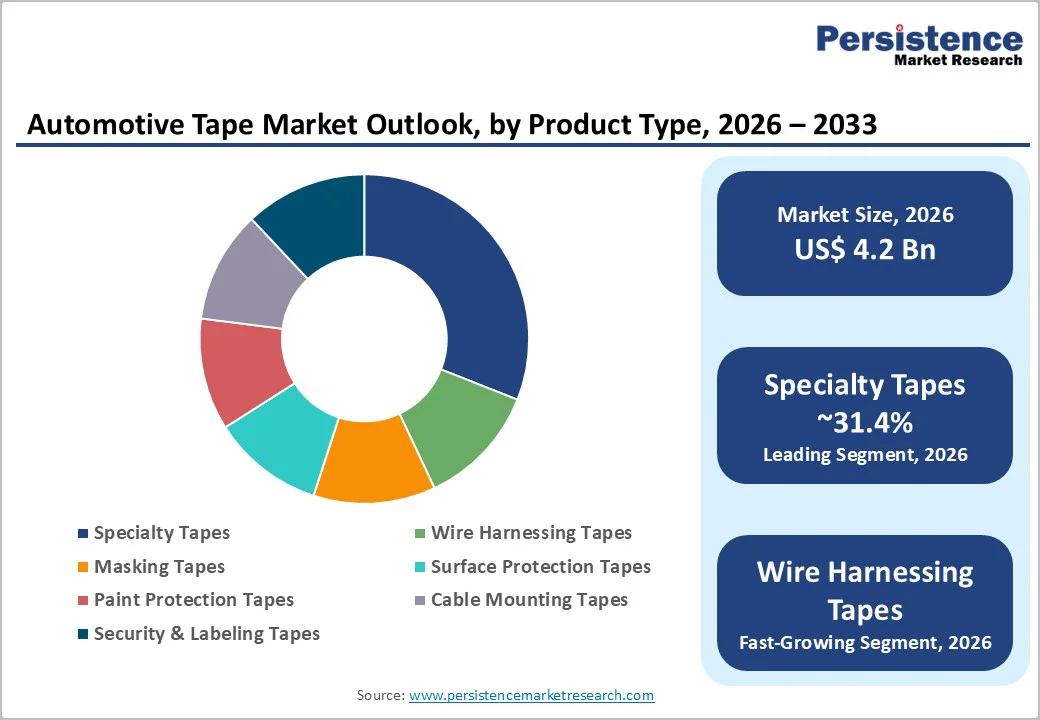

- Dominant Product Type: Specialty tapes to remain the dominant segment with 31.4% market share in 2026, supported by demand for dielectric strength, flame resistance, and thermal-stability applications in EV batteries and powertrain systems.

- Leading Material Type: PVC is anticipated to maintain its leadership with a 30.6% share, driven by its proven performance in wire harnessing, abrasion resistance, and interior masking applications, as well as its cost-effectiveness and durability.

| Key Insights | Details |

|---|---|

| Automotive Tape Market Size (2026E) | US$4.2 Bn |

| Market Value Forecast (2033F) | US$5.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Electrification and Increasing Tape Content per EV

The rapid shift toward battery electric vehicles significantly increases demand for specialized tapes used in wire harnessing, thermal insulation, temperature management, power electronics, and battery assembly. EVs require more complex wiring and additional heat-management layers compared to traditional internal combustion platforms, raising the tape content per vehicle by several percentage points.

This fuels innovation in silicone and acrylic adhesives engineered for high-temperature performance, flame resistance, and low outgassing, attributes essential in battery and high-voltage environments. Manufacturers that obtain early OEM or tier-1 approvals for EV-specific modules secure recurring, high-margin programs and gain a strong competitive advantage in long-cycle automotive platforms.

Light Weighting and Replacement of Mechanical Fasteners

Automakers are aggressively replacing mechanical fasteners with adhesive tapes to meet regulatory and corporate targets for fuel efficiency, emissions reduction, and assembly simplification. High-bond structural tapes and double-sided adhesive solutions allow secure joining of dissimilar materials such as composites, plastics, and metals while eliminating heavy metal hardware.

Industry analyses show that adhesive-based fastening can remove components and reduce vehicle body weight by 1-5% in certain application areas. This creates premium opportunities for tapes that meet strict crash-performance, durability, and aging standards. As a result, carriers such as PET and PP, paired with advanced adhesive chemistries, are increasingly preferred for next-generation lightweight designs.

Regulatory and Quality Standards

Tightening global regulations on safety, emissions, volatile organic compounds (VOCs), and recyclability are accelerating adoption of certified, high-specification automotive tapes. Manufacturers must comply with rigorous OEM qualification systems and governmental chemical-use restrictions, which favor suppliers capable of delivering low-VOC adhesives, recyclable carrier materials, and traceable supply-chain documentation.

These standards raise barriers to entry and encourage long-term partnerships with established suppliers that maintain in-house testing, validated flame-retardant systems, and comprehensive technical dossiers. For tape producers, investments in compliance infrastructure are essential to winning multi-year platform contracts while reducing business risk associated with non-compliance or delayed approvals.

Barrier Analysis - Raw Material Price Volatility

Automotive tape production relies heavily on polymers such as PVC, PET, and PP, as well as petrochemical-derived adhesive precursors. Price volatility in these raw materials directly affects manufacturing economics, especially in highly competitive, low-differentiation product segments.

When supplier contracts lack cost-indexation mechanisms, sudden increases in feedstock prices reduce margins or delay procurement decisions. Historically, swings in input costs have compressed profitability by several percentage points in certain tape categories. Producers commonly mitigate these risks through diversified sourcing, long-term supply agreements, and a shift toward higher-value product portfolios.

OEM Qualification and Approval Timelines

Automotive OEM approval cycles can take 12-24 months, particularly for safety-critical or engine-bay applications. Rigorous testing, documentation, and validation requirements slow down new product introductions and limit how quickly suppliers can respond to shifts in demand.

These long timelines create cash-flow challenges for smaller players and raise the upfront investment required for new technologies. The process favors larger suppliers with established testing facilities, regional labs, and existing platform approvals, creating a structural barrier for emerging competitors attempting to enter high-value segments.

Opportunity Analysis - EV Battery and Thermal-Management Tapes

Battery modules require insulation, flame-resistant barriers, thermal interface layers, and precision bonding solutions, each representing high-value tape categories. As OEMs focus on battery longevity, safety, and thermal performance, demand for specialized silicone and flame-retardant acrylic tapes is increasing rapidly.

Tape content per EV platform can translate into multi-million-dollar program value over a model’s lifecycle, making early design wins strategically important. Suppliers that prioritize R&D collaborations with tier-1 battery integrators and participate in early pilot builds are well-positioned to capture these premium, high-growth opportunities.

Emerging Markets and Localized Manufacturing

Expanding vehicle production in Asia Pacific, combined with OEM and government initiatives for local sourcing, creates strong incentives for regional tape manufacturing. Establishing facilities in China, India, and ASEAN markets reduces logistics costs, shortens lead times, and aligns with local-content rules.

Even moderate share capture in these large-volume markets yields significant incremental revenue. Joint ventures, modular coating lines, and regional technical service centers are attractive strategies for suppliers seeking to deepen engagement with domestic OEMs while diversifying global supply chains.

High-Value Specialty Tapes

Modern vehicles rely on increasing numbers of sensors, cameras, electronic modules, and displays, driving accelerated demand for specialty tapes used in thermal management, EMI shielding, precision bonding, and ultra-thin die-cut components.

These tapes command premium margins due to stringent performance needs and clean-room converting requirements. Suppliers that integrate advanced adhesive development with precision converting and co-engineering support attract OEMs looking for consolidated, technically sophisticated partners. Offering rapid prototyping kits and application-specific solutions enhances competitiveness in this fast-growing electronics-focused vertical.

Category-wise Analysis

Product Type Insights

Specialty tapes are expected to account for about 31.4% of market revenue in 2026, driven by their essential role in electronics modules, powertrain assemblies, thermal-management systems, and structural bonding, applications requiring high dielectric strength, flame resistance, thermal conductivity, solvent endurance, and long-term temperature stability.

Their ability to support advanced die-cutting, laser-slitting, and clean-room converting further elevates their value. Growth is strengthened by the rising electronic content in vehicles and the expansion of EV battery packs. OEMs increasingly use thin-film PET thermal-barrier tapes, high-bond acrylic structural tapes, and aramid-reinforced insulation tapes for cell wrapping and module spacing.

For example, PET-based flame-retardant tapes are now integrated into EV battery bundles to meet UL 94 V-0 standards.

Wire harnessing tapes are anticipated to be the fastest-growing segment, driven by rising wiring complexity in EVs and ADAS-equipped vehicles. These tapes require abrasion resistance, flame retardancy, vibration damping, and flexibility to support routing across modern vehicle architectures.

The shift toward zonal electrical systems and high-current battery cables is increasing demand for PET-fleece insulation tapes, high-voltage orange harness tapes, and heat-shield aluminum laminates. Growth is further supported by OEM initiatives to standardize harness designs across platforms, such as aligning next-generation EV layouts with ISO 6722-2 standards.

Investments in automated wrapping equipment and predictive quality systems are boosting supplier competitiveness, with strong opportunities for low-noise fleece tapes for cabins and high-abrasion PET tapes for engine compartments.

Material Type Insights

Polyvinyl chloride (PVC) is anticipated to be the leading carrier material in 2026, holding about 30.6% of the market due to its flexibility, abrasion resistance, dielectric strength, and cost efficiency. Its proven durability in automotive environments supports widespread use in wire harnessing, masking, interior protection, and panel sealing.

Manufacturers with advanced compounding and coating capabilities are meeting rising demand for low-VOC, heat-aging, and chemically resistant variants. Many Tier-1 suppliers have transitioned to lead-free PVC to meet REACH and RoHS standards. Despite new alternatives, PVC maintains dominance in harness-wrapping and standard masking applications.

Polypropylene is the fastest-growing carrier material, driven by lightweighting goals, strong resistance to automotive fluids, and better environmental performance than PVC. Adoption is rising in masking, exterior assembly, acoustic insulation, and select structural uses. Its low density delivers measurable weight savings that support emission and efficiency targets.

Advances in engineered PP tapes, such as corona-treated and plasma-treated surfaces, have improved adhesion, allowing PP to replace PVC or PET in mid-temperature applications. Automakers now use PP in exterior trim bonding, transit protection, and paint-shop masking. In Asia Pacific, PP-based heat-resistant masking tapes increasingly replace crepe-paper systems, strengthening PP’s role in next-generation tape applications.

Regional Insights

North America Automotive Tape Market Trends - Electrification-Driven, OEM-Centered Innovation Hub

North America represents one of the most mature and technically advanced markets for automotive tapes, supported by a large base of OEMs, tier-1 suppliers, and an extensive aftermarket ecosystem. The U.S. is the primary driver of regional demand, with strong production of trucks, SUVs, and premium vehicles, segments that rely heavily on high-performance bonding and sealing solutions.

Rapid introduction of new EV models increases the need for specialized battery, insulation, and thermal-management tapes. The region benefits from advanced converter networks in the U.S., Canada, and Mexico, each supporting localized component production. Mexico has become an important hub for wiring harnessing and interior component manufacturing, further strengthening tape consumption tied to assembly operations.

Key growth drivers in North America include electrification, localized supply-chain buildout, and automation initiatives targeting improved assembly efficiency. EV and truck electrification in particular raises the need for thermal interface tapes, flame-resistant adhesives, and high-bond mounting solutions.

Growing regulatory focus on VOC reduction and material traceability is also pushing tape manufacturers toward low-VOC chemistries and better documentation practices.

Investments across the region include expansions of regional technical labs, enhanced PPAP support centers, and automated manufacturing lines designed to meet tight OEM delivery schedules. Suppliers are increasingly forming joint development agreements with tier-1 battery module integrators to optimize tape performance in real-world, high-temperature EV environments. Overall, North America continues to serve as an innovation hub for advanced tape solutions and remains among the top revenue contributors globally.

Europe Automotive Tape Market Trends - Regulation-Led, Sustainability-Focused High-Performance Tape Market

Europe is anticipated to lead in 2026, representing roughly 29% of worldwide revenue. The region’s leadership stems from a robust base of premium automotive manufacturers, extensive EV and hybrid production, and a regulatory environment that emphasizes sustainability, emissions reduction, and material recyclability. Germany is the central engine of demand, owing to its sophisticated production lines for powertrain, electronics, and high-performance vehicles.

The U.K. contributes through specialist engineering firms and converters, while France and Spain anchor high-volume production for multiple international OEMs. Primary demand drivers across Europe include stringent environmental regulations, strong EV penetration, and an emphasis on lightweighting to meet strict emissions and efficiency targets.

These trends boost consumption of high-performance tapes with low-VOC properties, recyclable carriers, and advanced flame-retardant characteristics for EV battery enclosures. The regulatory environment significantly shapes material choices, with the EU pressing for compliance with chemical safety directives, end-of-life vehicle requirements, and circular-economy initiatives.

This regulatory complexity rewards established suppliers capable of demonstrating full documentation, sustainability pathways, and consistent quality across regions.

Investment activity in Europe is heavily focused on R&D, particularly developments in recyclable tapes, improved flame-retardant formulations, and adhesives tailored for electric powertrain safety. Consolidation across regional converters is accelerating as companies seek to expand technical capabilities and reduce duplication of testing and approval cycles. Collectively, Europe’s policy-driven demand profile is shifting the market toward higher-value and more sustainable tape solutions.

Asia Pacific Automotive Tape Market Trends - High-Volume EV Expansion with Localized Supply-Chain Acceleration

Asia Pacific is likely to be the fastest-growing region, supported by high vehicle production volumes, expanding EV manufacturing, and increasing domestic converter capabilities. China dominates regional output, benefiting from massive vehicle production numbers and the world’s largest EV market. Japan remains a center for high-specification materials, adhesives, and precision converting technologies.

India, meanwhile, is emerging as a fast-growing automotive hub, supported by local sourcing mandates and rising domestic vehicle demand. The region’s growth is fueled by three major factors: rising vehicle production, rapid expansion of EV platforms, and improving quality standards among domestic automakers.

China’s battery manufacturing ecosystem further accelerates demand for thermal, electrical insulation, and flame-resistant tape solutions tailored for high-voltage applications.

Regulatory conditions vary across the region, but national EV incentives, import-substitution strategies, and material safety standards are pushing manufacturers toward localizing supply chains. China’s increasingly strict battery safety guidelines, in particular, create substantial opportunities for high-value tape categories. Investment trends include greenfield coating and converting facilities, partnership expansions, and modular production lines that allow quick scale-up.

Technical collaborations between domestic and international suppliers are common, especially in thermal management and EV battery module applications. Asia Pacific’s dual role as both the largest demand generator and a cost-efficient manufacturing base positions it as the strategic center of global automotive tape growth over the next decade.

Competitive Landscape

The global automotive tape market occupies an intersection between large global chemical suppliers and a broad network of converters specializing in coating, slitting, die-cutting, and custom engineering. High-value specialty segments are dominated by a small group of multinational leaders with advanced R&D capabilities, while numerous regional converters focus on commodity tapes and localized OEM needs.

Competitive advantage is defined by scale, application expertise, OEM approvals, and the ability to support co-engineering across multiple regions. As electrification accelerates, suppliers with validated EV and battery-specific solutions are gaining disproportionate share.

Leading companies focus on differentiated adhesive chemistries, long-cycle OEM platform approvals, and regional production capabilities. High-value growth strategies center on EV-ready materials, co-engineering with tier-1 suppliers, and vertically integrated operations combining compounding, coating, and precision converting.

Key Industry Developments

- In January 2025, Lohmann GmbH & Co. KG announced a new low-emission adhesive tape portfolio for vehicle interiors, targeting OEMs with strict interior air-quality and low-VOC requirements.

- In April 2025, Tesa SE introduced its new “L-tape 869x,” a high-performance adhesive tape engineered for automotive applications.

Companies Covered in Automotive Tape Market

- 3M

- Avery Dennison Corporation

- Tesa SE

- Nitto Denko Corporation

- Scapa Group

- LINTEC Corporation

- Saint-Gobain Performance Plastics

- Henkel AG & Co. KGaA

- Intertape Polymer Group (IPG)

- Berry Global Inc.

- Sika AG

- Adchem Corporation

- Shurtape Technologies

- Lohmann GmbH & Co. KG

- ORAFOL Europe GmbH

- DuPont

- Johnson & Johnson (Industrial Tapes Division)

- CCT Tapes (Custom Converter Technology)

- Rogers Corporation

- Luxking Group

Frequently Asked Questions

The global automotive tape market size is estimated to be US$4.2 billion in 2026.

By 2033, the market value is projected to reach US$5.6 billion.

Key trends include the rising adoption of thermal-management tapes, high-bond structural adhesives, PP-based lightweight tapes, and advanced electronic bonding materials. Growth is supported by EV platform expansion, increasing ADAS integration, and the shift toward low-VOC and recyclable materials.

Specialty tapes dominate the product category with 31.4% market share, driven by high-performance requirements in electronics, powertrain systems, and thermal-management applications.

The automotive tape market is expected to grow at a CAGR of 4.3% between 2026 and 2033.

Major players include 3M, Avery Dennison Corporation, Tesa SE, Nitto Denko Corporation, and Henkel AG & Co. KGaA.