- Inks, Coatings, Adhesives & Sealants (ICAS)

- Automotive OEM Coating Market

Automotive OEM Coating Market Size, Share, and Growth Forecast 2026 - 2033

Automotive OEM Coating Market by Product Type (Clearcoat, Basecoat, Primer, E-coat, Others), Resin Type (Epoxy, Polyurethane, Acrylic, Other), Technology (Water-based, Solvent-based, Powder-based, UV Curable Coatings, Other), Vehicle Type (Passenger Cars, Commercial Vehicles), and Regional Analysis for 2026 - 2033

Automotive OEM Coating Market Size and Trend Analysis

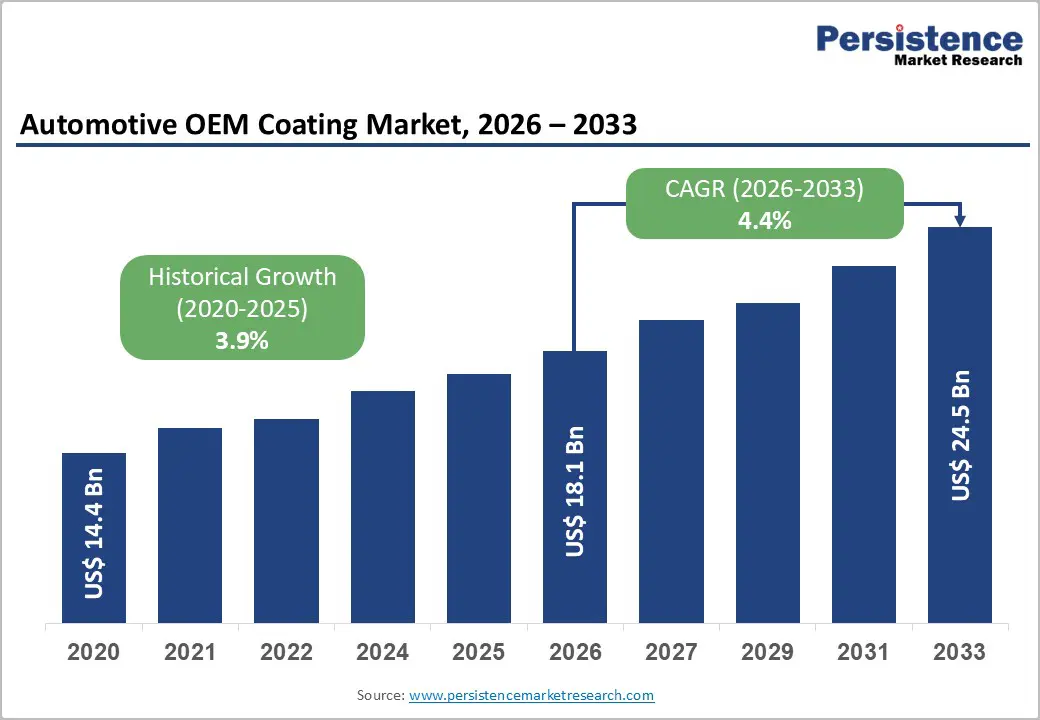

The global automotive oem coating market is valued at US$ 18.1 billion in 2026 and is projected to reach US$ 24.5 billion by 2033, growing at a CAGR of 4.4% between 2026 and 2033.

A rise in global vehicle production, tightening environmental regulations around volatile organic compound (VOC) emissions, and the rapid expansion of the electric vehicle (EV) segment are the primary forces propelling this market. According to the International Organization of Motor Vehicle Manufacturers (OICA), worldwide motor vehicle sales reached approximately 95 million units in 2024, directly elevating demand for multi-layer OEM coating systems. Simultaneously, regulatory mandates across North America, Europe, and the Asia Pacific are accelerating the adoption of waterborne and low-VOC technologies, enabling superior coating performance while meeting sustainability benchmarks.

Key Industry Highlights:

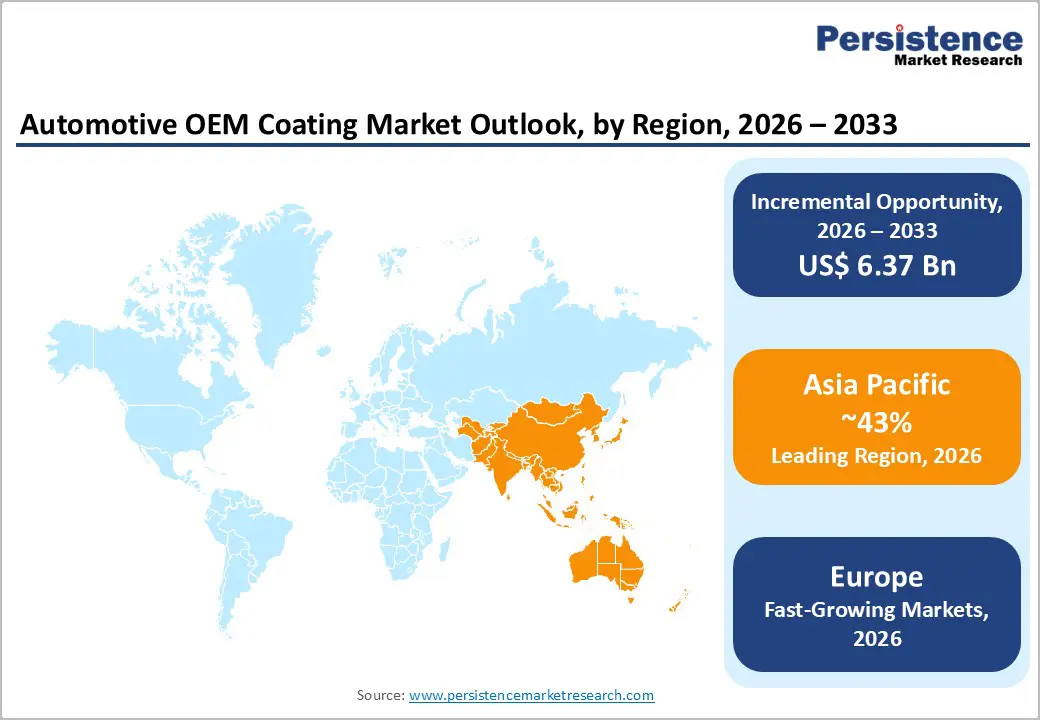

- Leading Region: Asia Pacific leads the Automotive OEM Coating market with 43% revenue share in 2025. China continues to lead global automotive production, supported by capacity expansions and strong export momentum that drives substantial coating consumption.

- Fastest Growing Region: Europe is the fastest growing region, driven by the EU's 2035 ICE ban, aggressive EV adoption targets under the Green Deal, and significant OEM investments in automated, low-emission waterborne paint shop systems.

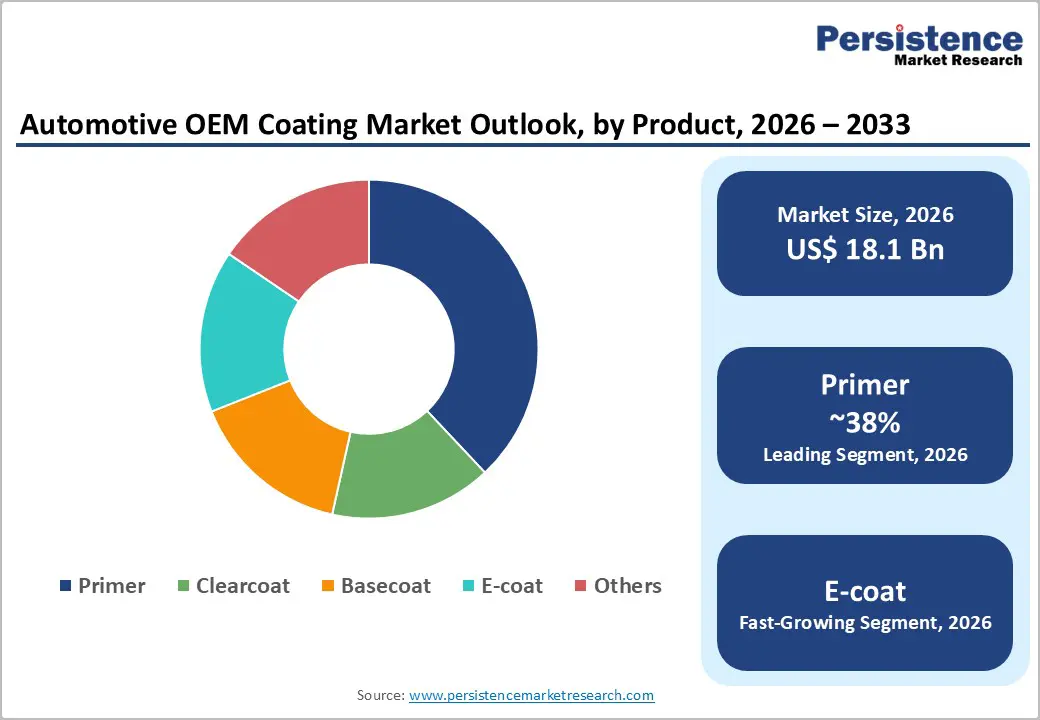

- Dominant Segment: The primer segment leads in product type with 38% revenue share, owing to its critical role in corrosion protection and adhesion preparation across all vehicle categories and OEM paint application lines globally.

- Fastest Growing Segment: Water-based (waterborne) coatings represent the fastest-growing technology segment, propelled by stringent EPA and EU VOC regulations that reward lower-emission coating systems with up to 80% less VOC compared to solvent-borne alternatives.

- Key Market Opportunity: The rapid expansion of EV manufacturing, with EVs projected to account for 30% of global new-car sales by 2032, presents a high-value revenue opportunity for EV-specific coatings to protect batteries, manage thermal performance, and enable lightweight substrate compatibility.

| Key Insights | Details |

|---|---|

| Automotive OEM Coating Market Size (2026E) | US$ 18.1 Bn |

| Market Value Forecast (2033F) | US$ 24.5 Bn |

| Projected Growth CAGR (2026 - 2033) | 4.4% |

| Historical Market Growth (2020 - 2025) | 3.9% |

Market Dynamics

Drivers - Surge in Global Vehicle Production and EV Adoption

The ongoing recovery and expansion of global vehicle production remain a primary catalyst for growth in the Automotive OEM Coating market. According to OICA data, global motor vehicle production surpassed 92.5 million units in 2024, with Asia Pacific alone contributing nearly 60% of total output. Concurrently, the accelerating shift toward electric vehicles is reshaping industry requirements, as EV manufacturers demand advanced coating solutions for battery protection, adhesion to lightweight composite substrates, and effective thermal management.

In the United States alone, EV sales are projected to reach 1.5 million units in 2024. Globally, electric vehicles are expected to represent 30% of all new car sales by 2032, prompting a surge in innovation, including more than 120 EV-specific coating patent filings in 2024. These evolving needs are driving significant opportunities for OEM coating suppliers.

Accelerating Electric Vehicle Adoption: Generating Specialized Coating Requirements

The accelerating global shift toward electric mobility is generating a rapidly expanding and distinct demand segment within the Automotive OEM Coating Market. Electric vehicles introduce specialized coating requirements, including advanced battery protection layers, thermal-management coatings, and materials compatible with lightweight aluminum and composite substrates, alongside enhanced corrosion resistance for high-voltage components. Industry projections indicate that EVs will account for nearly 30% of global new vehicle sales by 2032, driving strong demand for EV-oriented formulations.

More than 120 EV-specific coating patents were filed worldwide in 2024, underscoring significant innovation activity. Furthermore, the U.S. government’s plan to establish 500,000 public charging stations by 2030 reinforces long-term EV ecosystem growth. Leading manufacturers such as PPG Industries and AkzoNobel continue to invest in R&D focused on advanced chemistries, heat-dissipating exterior coatings, and polymers optimized for multi-material vehicle architectures.

Restraints - Volatility in Raw Material Prices

Raw materials such as titanium dioxide (TiO), epoxy resins, polyurethane precursors, and specialty pigments account for approximately 60-70% of total automotive coating production costs. Volatility in crude oil prices directly influences the cost of solvents and resins, while supply constraints in the TiO- market further compress margins across the value chain.

Between 2021 and 2023, global supply chain disruptions resulted in a 25-35% increase in petrochemical-derived raw material costs, compelling OEM coating manufacturers to absorb reduced margins or renegotiate long-term supply agreements. This persistent volatility limits R&D investment and hinders market expansion strategies, particularly among mid-tier and regional producers.

Extended Product Development Cycles and Technical Complexity

Developing a new OEM coating formulation, from initial laboratory research to full-scale production, typically requires two to three years of rigorous evaluation. This process includes extensive adhesion testing, corrosion-resistance validation, color-consistency benchmarking, and the completion of OEM homologation protocols. Increasing adoption of multi-material vehicle architectures, integrating aluminum, carbon fiber-reinforced polymers (CFRP), and high-strength steel, adds further complexity to formulation development.

As highlighted by Toyota in January 2025, expanded assessments of paint adhesion on aluminum and composite panels for forthcoming electric SUV models illustrate the practical challenges associated with coating multi-substrate body structures. These factors collectively slow the commercialization of next-generation coating technologies.

Opportunities - Waterborne and Powder Coating Adoption Driven by Global Sustainability Mandates

The rapid global transition toward waterborne and powder-based automotive OEM coatings presents a substantial commercial opportunity for industry participants. Waterborne technologies reduce VOC emissions by up to 80% compared to traditional solvent-borne systems and now dominate several European OEM basecoat lines, with manufacturers such as Mazda achieving emissions as low as 15 g VOC/m². In the United States, waterborne coatings accounted for 63.8% of OEM usage in 2024, lowering VOC emissions by nearly 39% relative to solvent-based alternatives.

As automakers restructure paint shop operations to meet carbon-neutrality targets for 2030-2040, companies advancing high-performance waterborne formulations are positioned to gain a competitive advantage. PPG Industries’ March 2025 inauguration of a dedicated waterborne coatings facility in Tennessee underscores this strategic shift. Early leadership in next-generation low-emission technologies, particularly those integrating UV-curable and waterborne chemistries, will enable suppliers to secure long-term OEM partnerships.

Growth of Automotive Production in Emerging Economies Expanding Addressable Market

Emerging markets across South Asia, Southeast Asia, and Latin America are rapidly evolving into significant automotive manufacturing hubs, creating substantial expansion opportunities for coating suppliers. India’s Ministry of Heavy Industries reported a record 4.8 million passenger vehicles produced in FY 2023-2024, marking a 14% year-on-year increase. Similarly, Brazil registered a 10% rise in vehicle production in 2024, the highest growth among leading global producers. These fast-growing regions are also adopting stricter domestic environmental regulations, accelerating demand for advanced, sustainable coating technologies.

Companies that invest in localized manufacturing, robust distribution infrastructure, and technically skilled regional sales teams are well positioned to capitalize on long-term structural growth driven by rapid urbanization, rising disposable incomes, and increasing consumer preference for personal mobility, particularly in the passenger car and light commercial vehicle segments.

Category-wise Analysis

Product Type Insights

Among all product categories, the primer segment maintains the highest revenue share, representing approximately 38% of the global market in 2025. Primers function as the foundational layer within the multi-coat OEM application process, delivering critical attributes such as corrosion resistance, improved adhesion for subsequent layers, and enhanced surface uniformity. Their extensive adoption within electrocoat (e-coat) systems, known for enabling uniform coating deposition on complex vehicle geometries, further strengthens their dominant position.

According to the U.S. Bureau of Economic Analysis, domestic motor vehicle production grew by 9.3% year-over-year in May 2024, with light trucks and SUVs comprising over 65% of total production in Q1-2024, categories that rely heavily on durable primer systems. The e-coat segment is projected to record the fastest CAGR through 2032, supported by its superior corrosion protection, low VOC emissions, and efficiency in high-volume OEM operations.

Resin Type Insights

Within the resin type segment, epoxy resins hold the largest revenue share, accounting for approximately 30% of the global market. Their dominance stems from their essential role in cathodic e-coat systems, where they offer exceptional corrosion resistance, strong adhesion to metallic substrates, and superior chemical durability, qualities crucial for protecting underbody structures and key body panels. Their thermal stability and resistance to blistering further reinforce their widespread use in primer applications. Growing electric vehicle production is also increasing demand, as battery enclosures require high-performance corrosion protection.

However, the polyurethane segment is expected to record the fastest CAGR during the forecast period, driven by its superior UV resistance, flexibility, and suitability for premium clearcoat and basecoat coatings. Ongoing advances in aliphatic diisocyanate chemistry continue to enhance polyurethane performance in stringent yellowing resistance tests mandated by European OEMs.

Technology Insights

The water-based (waterborne) technology segment represents the leading share of the Automotive OEM Coating Market, accounting for approximately 48% of global OEM coating usage in 2025. Its dominance is driven by increasingly stringent global regulations aimed at reducing VOC emissions across automotive manufacturing operations. Key frameworks, including the EU’s Directive 2004/42/EC and China’s National Standard GB 30981-2020, have compelled major OEMs and tier-one suppliers to accelerate the transition toward waterborne formulations for primers, basecoats, and intermediate coats.

Advances in resin emulsification, flash-off control, and anti-sag additives have substantially narrowed the historical performance gap with solvent-borne systems, enabling waterborne coatings to meet the requirements of premium metallic and pearlescent finishes. Meanwhile, solvent-borne coatings retain a 38% market share, particularly in high-performance topcoat and commercial vehicle applications where superior flow and color depth remain essential.

Vehicle Type Insights

The passenger cars segment holds the leading position in the Automotive OEM Coating Market by vehicle type, accounting for the 65% share in 2025. This dominance reflects the substantial scale of global passenger car production, over 68 million units in 2024. The segment’s strength is further supported by increasing consumer preference for premium aesthetics, customization, and advanced surface protection, which are elevating coating content per vehicle, particularly in premium and electric vehicle categories.

Demand for metallic, pearlescent, and matte finishes continues to rise, reinforcing the segment’s market leadership. The commercial vehicles segment is projected to record the fastest growth through 2033, driven by expanding requirements for heavy-duty trucks, logistics fleets, and last-mile delivery vehicles, aligned with rapid e-commerce expansion, infrastructure development, and urbanization across emerging markets.

Regional Insights

North America Automotive OEM Coating Market Trends

North America remains the largest regional market for Automotive OEM Coatings, accounting for approximately 27.6% of global revenue in 2025, with the United States retaining a clear leadership position. According to U.S. Federal Reserve Economic Data, sales of lightweight vehicles reached 15 million units in January 2024, up 11.7% year over year. Light trucks now comprise 84% of monthly U.S. auto sales, driving substantial demand for premium scratch-resistant clearcoats and corrosion-protective primers.

Regulatory mandates, including EPA NESHAP standards and CAFE requirements, are accelerating industry investment in waterborne coating solutions and energy-efficient paint shop technologies. In May 2024, PPG Industries announced a USD 300 million investment to construct a 250,000 sq. ft. facility in Tennessee capable of producing over 11 million gallons of coatings annually, underscoring the region’s continued commitment to expanding domestic OEM coating capacity.

Europe Automotive OEM Coating Market Trends

Europe constitutes one of the largest regional markets for Automotive OEM Coatings and is distinguished by its strong commitment to sustainable and technologically advanced coating solutions. Germany, France, and Spain serve as the region’s principal manufacturing bases, hosting major automotive groups such as Volkswagen Group, Stellantis, and Renault Group. Regulatory frameworks, including the European Union’s Industrial Emissions Directive (IED) and the EU Green Deal, are driving OEMs to invest in automated paint shops, waterborne basecoat lines, and low-bake coating systems aimed at reducing VOC emissions and energy consumption.

Europe is also projected to record the fastest CAGR during the forecast period, supported by ambitious EV transition goals and the mandated phase-out of internal combustion engine vehicles by 2035. In 2025, BASF Coatings, in collaboration with Renault Group and Dürr, received recognition for the Overspray-Free Application (OFLA) process, reinforcing Europe’s position as a hub for coating innovation.

Asia Pacific Automotive OEM Coating Market Trends

Asia Pacific remains the dominant region in the global Automotive OEM Coating Market, accounting for nearly 43% of total volume in 2025. China continues to lead global automotive production, supported by capacity expansions and strong export momentum that drives substantial coating consumption. Japan’s emphasis on precision engineering and its leadership in hybrid and electric vehicle platforms further stimulate demand for advanced, low-emission coating technologies.

India also demonstrates robust growth, with the Ministry of Heavy Industries reporting 4.8 million passenger vehicles produced in FY-2023-24, reflecting a 14% year-on-year increase. Meanwhile, ASEAN markets, particularly Thailand, Indonesia, and Vietnam, are emerging as key manufacturing hubs, attracting significant FDI. In March 2025, PPG Industries inaugurated a waterborne OEM coatings facility in Thailand, while Nippon Paint Holdings and Uchihamakasei Corp. jointly introduced next-generation in-mold coating (IMC) technology to support carbon-neutral automotive processes.

Competitive Landscape

The global Automotive OEM Coating market remains moderately consolidated, with major multinational firms, such as PPG Industries, BASF SE, AkzoNobel, and Axalta Coating Systems, commanding a substantial share of overall revenues. These companies maintain competitive strength through extensive manufacturing networks, long-standing OEM partnerships, and sustained investment in advanced R&D initiatives. Their differentiation is further supported by proprietary waterborne, low-VOC, and EV-specific coating technologies. In November 2025, AkzoNobel and Axalta announced an all-stock merger of equals, forming a USD 17 billion coatings entity and reinforcing industry consolidation. Emerging business strategies increasingly emphasize OEM co-development models, sustainability-linked long-term contracts, and digitally integrated paint-shop solutions.

Key Developments:

- November 2025: AkzoNobel N.V. and Axalta Coating Systems signed a definitive all-stock merger of equals, forming a global coatings leader with a combined revenue of approximately USD 17 billion and an enterprise value of USD 25 billion, targeting USD 600 million in cost synergies.

- March 2025: PPG Industries inaugurated an advanced waterborne automotive coatings manufacturing plant in Thailand, featuring an automated spray application centre to boost eco-friendly coating production capacity across Southeast Asia.

- November 2025: BASF Coatings has successfully commissioned a state-of-the-art production plant for automotive OEM coatings at its Muenster site in Germany. The new facility is designed to produce high-runner products, namely colors that currently represent most of the market demand, and ensure consistent product quality and enhanced production efficiency.

Top Companies in the Automotive OEM Coating Market

- PPG Industries, Inc. (Pittsburgh, USA) is the global market leader in automotive OEM coatings, commanding the broadest product portfolio spanning e-coats, primers, basecoats, and clearcoats across passenger and commercial vehicle segments. The company derives approximately 44% of its total revenue from sustainably advantaged product lines. With a US$ 300 million investment in a new Tennessee facility and consistent above-market growth in its automotive OEM division, PPG maintains unparalleled scale and depth of innovation.

- BASF SE (Münster, Germany) Coatings is among the top-three global OEM coating suppliers, known for pioneering sustainable technologies. In 2025, BASF earned an innovation award for the Overspray-Free Application (OFLA) process jointly developed with Renault Group and Dürr. BASF has also signed a Letter of Intent with NIO for strategic EV coating partnerships, positioning itself at the EV-OEM intersection.

- Axalta Coating Systems, LLC (Philadelphia, U.S.) is a specialized global coating leader, with particular strength in collision repair solutions and OEM topcoat technologies. The company's partnership with inkjet manufacturer Xaar to pioneer digital spray systems capable of complex color gradients represents a transformative approach to vehicle customization, reinforcing its technological differentiation in both OEM and refinish markets.

Companies Covered in Automotive OEM Coating Market

- PPG Industries, Inc.

- BASF SE

- Axalta Coating Systems, LLC

- AkzoNobel N.V.

- Nippon Paint Holdings Co., Ltd.

- The Sherwin-Williams Company

- Kansai Paint Co., Ltd.

- Covestro AG

- Berger Paints India Ltd.

- RPM International Inc.

- 3M Company

Frequently Asked Questions

The global Automotive OEM Coating market is valued at US$ 18.1 Bn in 2026 and is projected to reach US$ 24.5 Bn by 2033, growing at a CAGR of 4.4% during the forecast period 2026-2033. The market recorded a historical CAGR of 3.9% during 2020-2025, supported by steady vehicle production growth and technological advancements in coating formulations.

The primary demand drivers are rising global vehicle production volumes, with OICA reporting approximately 92.5 million units produced in 2024, the rapid expansion of electric vehicles requiring specialized coating solutions, and tightening environmental regulations worldwide mandating the adoption of low-VOC waterborne and powder coating technologies. Growing consumer preference for premium finishes, metallic and pearlescent effects, and durable surface protection also contributes to increasing coating value per vehicle.

The primer segment dominates the product type category with an approximate 38% revenue share in 2025. Primers are essential across all vehicle categories for corrosion protection and inter-coat adhesion, and the segment benefits from the widespread adoption of high-efficiency electrocoat (e-coat) primer systems in OEM paint shops globally.

Asia Pacific is the leading regional market, holding approximately 43% of global revenue in 2025. China produced over 31.28 million vehicles in 2024, representing approximately one-third of total global output, per OICA, with domestic new energy vehicle production exceeding 10 million units for the first time.

The most significant market opportunity lies in the rapid expansion of electric vehicle (EV) manufacturing globally. EVs require highly specialized coating systems for battery enclosures, lightweight composite substrates, EMI shielding, and thermal management, creating premium product development opportunities. With EVs projected to account for 30% of global new car sales by 2032, early-mover R&D investments in EV-specific coating platforms offer a substantial competitive advantage.

The leading players in the global Automotive OEM Coating market include PPG Industries, Inc., BASF SE, Axalta Coating Systems LLC, AkzoNobel N.V., Nippon Paint Holdings Co., Ltd., The Sherwin-Williams Company, Kansai Paint Co., Ltd., Covestro AG, Berger Paints India Ltd., RPM International Inc., and 3M Company. These companies collectively shape the competitive landscape through continuous R&D, strategic partnerships, mergers, and global manufacturing capacity expansions.