- Advanced Materials

- Wood Plastics Composites Market

Wood Plastics Composites Market Size, Share, and Growth Forecast 2026 - 2033

Wood Plastics Composites Market by Product (Polyethylene, Polypropylene, Polyvinyl Chloride), by Application (Building and Construction, Automotive Components), by Distribution Channel, and Regional Analysis for 2026 - 2033

Wood Plastics Composites Market Size and Trend Analysis

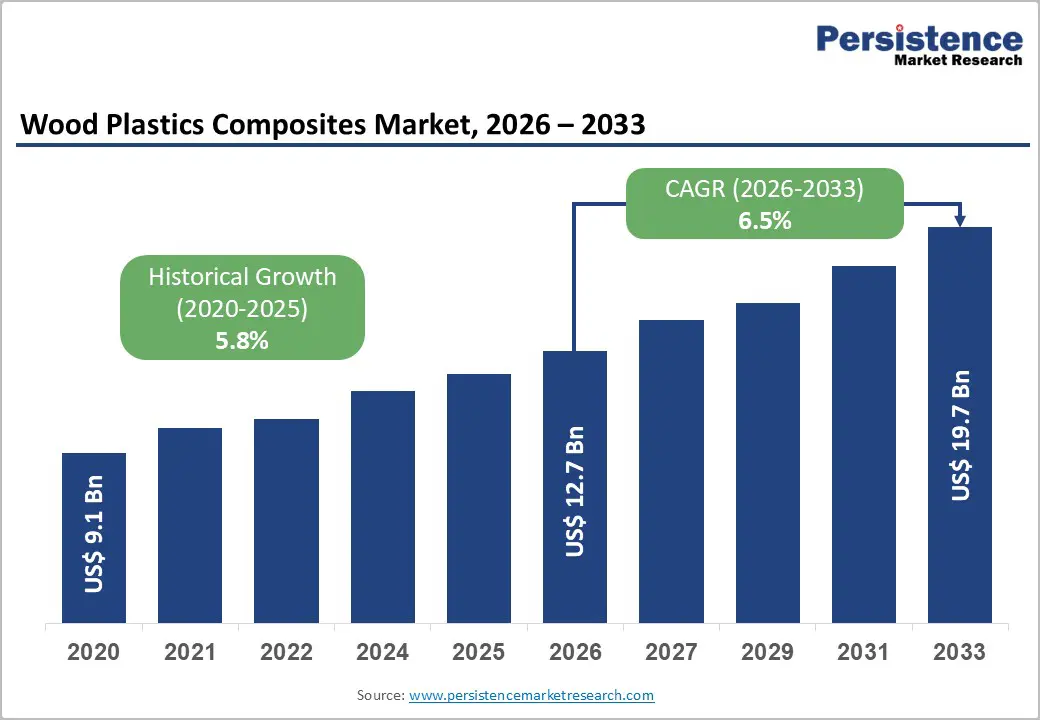

The global wood plastics composites market size is supposed to be valued at US$ 12.71 billion in 2026 and is projected to reach US$ 19.7 billion by 2033, growing at a CAGR of 6.5% between 2026 and 2033.

Wood Plastic Composites (WPCs) emerge as a smart alternative to both conventional timber and virgin polymers. These hybrid materials are reshaping how consumers and manufacturers think about product durability, aesthetics, and environmental responsibility. As construction, automotive, and furniture industries pursue solutions that reduce lifecycle costs while complying with evolving environmental norms, the versatility of WPCs is unlocking new design and engineering frontiers.

Key Industry Highlights:

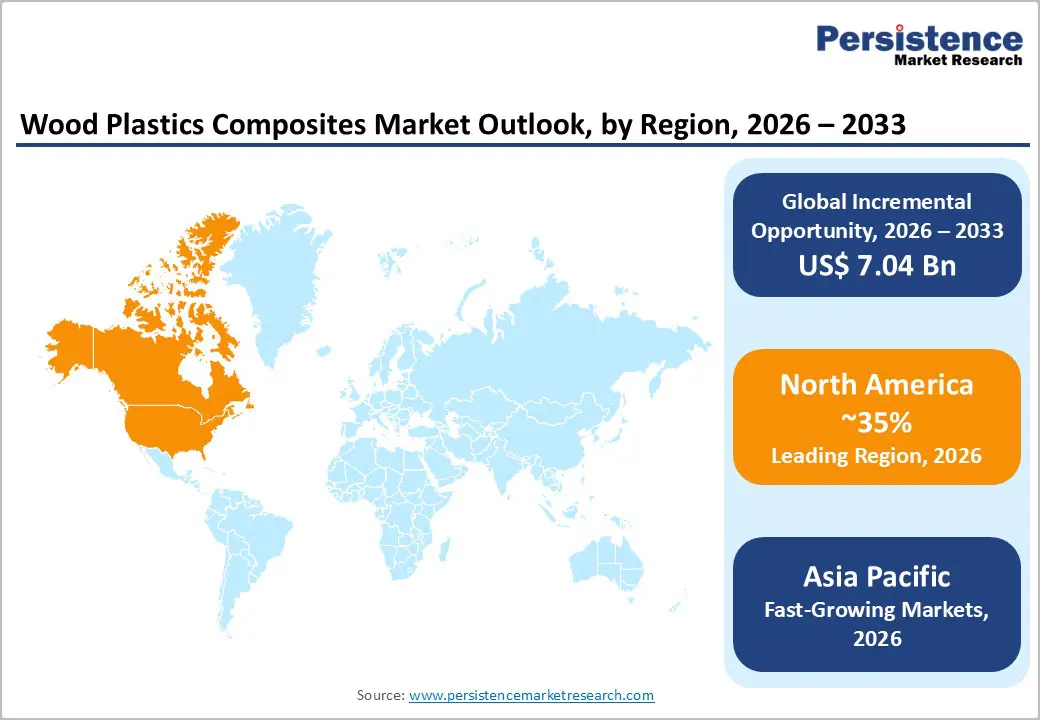

- Leading Region: North America’s mature home renovation and remodeling market favors durable, low-maintenance alternatives such as WPCs. Homeowners and contractors increasingly prefer composite decking and exterior solutions that reduce upkeep costs while delivering long-term performance and aesthetic appeal.

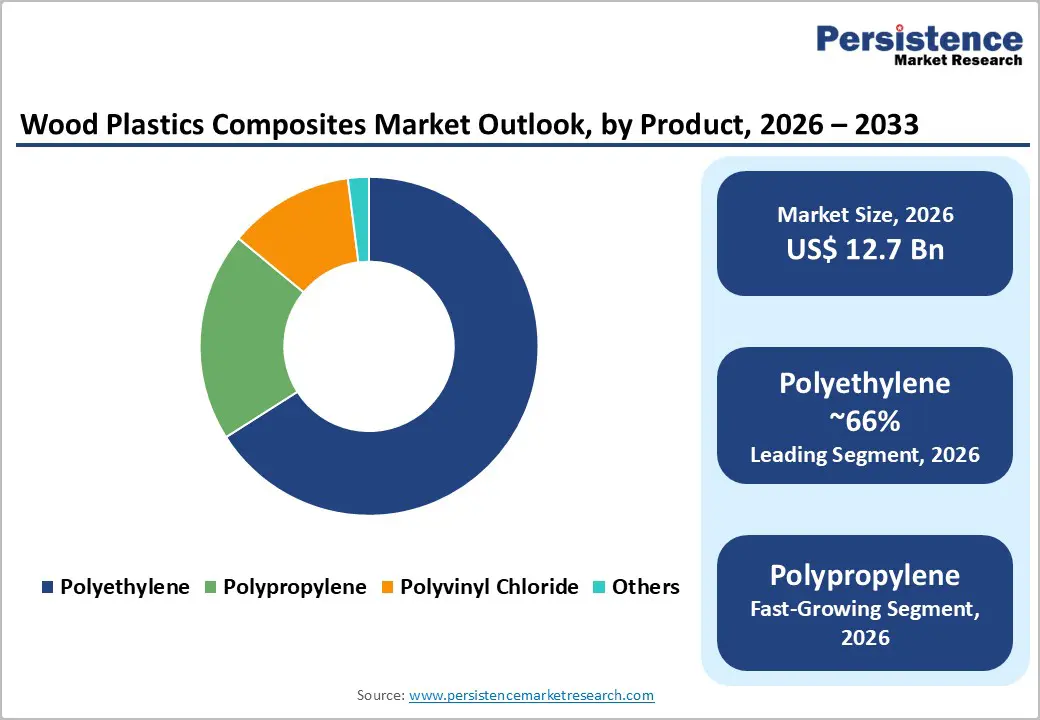

- Leading Segment: Polyethylene-based WPCs are projected to account for approximately 66.3% share in 2025, driven by their superior flexibility, impact resistance, and ease of processing. These properties enable the production of durable, weather-resistant profiles widely used in decking, fencing, and outdoor structures.

- Primary Demand Driver: WPCs replicate the natural appearance of wood while offering longer service life, resistance to rot and insects, and minimal maintenance requirements. These advantages are significantly increasing adoption in building and construction applications, particularly for decking, cladding, railing, and landscaping structures.

- Emerging Trend: Integration of wood plastic composites (WPCs) with smart materials and sensor-enabled additives is gaining traction, enabling enhanced structural performance, real-time condition monitoring, and improved durability. This trend supports next-generation building materials that combine sustainability with intelligent performance tracking.

- Opportunity : Adoption of WPCs in marine decking and waterfront infrastructure is creating new growth avenues, as their superior moisture resistance, anti-corrosion properties, and dimensional stability make them ideal for harsh coastal and high-humidity environments where traditional wood rapidly deteriorates.

| Key Insights | Details |

|---|---|

|

Wood Plastics Composites Market Size (2026E) |

US$ 12.7 Bn |

|

Market Value Forecast (2033F) |

US$ 19.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.5% |

|

Historical Market Growth (CAGR 2020 to 2024) |

5.8% |

Market Dynamics

Drivers - Cities turn to WPCs for weather-resistant, eco-certified public installations

The global push for smart and sustainable cities is directly spurring wood plastics composites market growth. WPCs, being recyclable and low maintenance, comply with green building codes and circular economy principles that several megaprojects now mandate. In Rotterdam, Netherlands, WPC was officially used in the construction of a 3.5km boardwalk along the waterfront. The boardwalk was installed using Recoplast WPC decking boards and was praised in local engineering reports for its long-term durability, low maintenance, and recyclability.

Similarly, in Vancouver, Canada, city procurement documents from 2023 specify the use of Trex Transcend WPC decking for park renovations, citing its 95% post-consumer recycled plastic content and 25-year residential warranty. In Singapore, on the other hand, a 2024 tender from the National Parks Board details the installation of WPC benches and footpaths in urban green spaces. It shows the installation of PVDF-coated composite benches made from 80% recycled plastic and reclaimed wood fiber.

Automotive Lightweighting Initiatives and EV Platform Integration Expanding Non-Construction Demand

The automotive industry's structural shift toward electric vehicle (EV) platforms is generating a significant and growing demand base for WPC beyond traditional building and construction end-markets. Automotive OEMs, including Ford Motor Company, are integrating WPC into door panels, dashboards, and interior trim components, achieving part-mass reductions of approximately 30% while simultaneously improving noise damping and sustainability performance for EV platforms that are highly weight-sensitive. Underbody shields manufactured from WPC blends incorporating mineral fillers are further unlocking incremental mileage range efficiency, a commercially critical differentiator in the EV segment. As the global EV fleet continues to scale with the International Energy Agency (IEA) projecting over 40% of all new car sales to be electric by 2030 in key markets demand for weight-reducing, interior-grade WPC formulations is expected to grow at double-digit rates within the automotive sub-segment, further diversifying the revenue base of the Wood Plastics Composites Market and buffering participants against single-sector demand cyclicality.

Restraints - High upfront costs limit WPC adoption in budget-sensitive construction

The high initial cost of WPCs continues to be a significant barrier to widespread adoption, mainly in low-income construction segments and cost-sensitive markets. Unlike conventional materials such as softwood or virgin plastic, WPCs often come with a price premium of 15 to 25% at the point of purchase. It is fueled by the requirement for precision extrusion or injection molding equipment, the use of additives, including UV stabilizers and coupling agents, and processing complexity.

Small-scale builders and residential customers often opt for traditional timber or basic plastic alternatives owing to immediate affordability, even if those materials require frequent replacement. In addition, the specialized nature of WPC processing can inflate project budgets. Various regional manufacturers lack the technical infrastructure to produce high-quality WPCs, resulting in dependence on imports or licensed products. This raises procurement costs and delivery lead times, thereby hampering adoption in fast-paced infrastructure projects.

Elevated Production Costs Relative to Conventional Timber and Virgin Polymer Alternatives

Despite its long-term lifecycle cost advantages, WPC continues to carry a significantly higher upfront production cost compared to conventional pressure-treated lumber and standard virgin plastic profiles. Raw material procurement for high-quality recycled polyethylene or polypropylene feedstocks particularly post-consumer grades remains subject to price volatility tied to broader petrochemical market cycles. Compounding this, extrusion process controls required to maintain dimensional stability and surface finish uniformity for WPC products are technically demanding, necessitating capital-intensive machinery investments that smaller manufacturers find difficult to sustain. These cost barriers translate into price premiums of 30–50% over untreated wood on a per-linear-foot basis for decking applications, limiting penetration in price-sensitive residential segments, particularly in developing markets across Latin America, Southeast Asia, and Eastern Europe.

Opportunity - WPCs gain traction in premium outdoor furniture with wood-like appeal

Surging demand for outdoor furniture is creating lucrative opportunities for WPCs, as consumers and manufacturers increasingly prioritize materials that balance aesthetics, sustainability, and weather resistance. WPCs offer inherent moisture resistance, UV stability, and termite protection, making these ideal for outdoor applications, including poolside loungers, patio sets, and garden benches. Consumers in developed countries are increasingly shifting toward composite-based furniture due to maintenance-free performance. Manufacturers are responding to this trend by introducing design-centric, eco-friendly product lines made from WPCs.

What makes WPCs especially attractive for this segment is their ability to mimic natural wood grain and texture while offering superior durability in varying climates. This aesthetic advantage, combined with the surging trend of biophilic design in urban architecture, has boosted the popularity of WPCs in premium outdoor installations.

Recycled Material Integration and Circular Economy Positioning as a Differentiating Competitive Strategy

The growing institutional emphasis on recycled content verification, environmental product declarations (EPDs), and third-party lifecycle assessment (LCA) documentation is creating a durable competitive advantage for WPC manufacturers that have invested in vertically integrated recycling capabilities. The AZEK Company Inc. exemplifies this opportunity; in early 2025, the company acquired Northwest Polymers, an industry leader in post-industrial and post-commercial plastic recycling, to strengthen recycled feedstock supply for its Boise, Idaho manufacturing facility and expand its FULL-CIRCLE PVC Recycling® program across the western United States. Similarly, Trex Company, Inc. invested US$ 400 million in a new composite manufacturing campus in Little Rock, Arkansas, incorporating eco-friendly production systems and recycling polyethylene processing capabilities. These investments signal that circular economy positioning anchored in auditable recycled content percentages, EPD certifications, and recycling take-back programs is rapidly transitioning from a reputational differentiator to a procurement prerequisite in key regulated markets.

Category-wise Analysis

Product Insights Insights

In terms of product, the market is trifurcated into polyethylene, polypropylene, and polyvinyl chloride. Among these, polyethylene is predicted to lead with a share of approximately 66.3% in 2026 due to its excellent compatibility with wood fibers and cost-efficiency in large-scale production. It provides a balanced combination of flexibility, moisture resistance, and ease of processing, making it ideal for extrusion-based manufacturing of wood and composite decking boards. As per the European Wood and Natural Fiber Composite Study 2023, more than 65% of all WPCs in Europe use polyethylene as the base resin, with similar dominance seen in North America and Asia Pacific.

Polyvinyl chloride is speculated to witness a decent CAGR from 2025 to 2032 with its inherent dimensional stability, rigidity, and fire resistance. These characteristics make the material ideal for high-end applications such as interior wall panels, railings, window profiles, and cladding. Polyvinyl chloride also exhibits low thermal expansion and high resistance to warping and deformation. It is essential in applications requiring precise tolerances and long-term structural integrity.

Application Insights

In terms of application, the market is segregated into building and construction, automotive components, and industrial and consumer goods. Out of these, the building and construction segment is poised to hold nearly 72.1% share in 2026, backed by the ability of WPCs to address durability challenges in outdoor environments while meeting sustainability expectations. WPCs offer superior resistance to UV radiation, termites, and moisture, qualities that are required in façade cladding, fencing, and decking. The design versatility of WPCs also adds aesthetic value to architectural projects without compromising on function.

Automotive components have emerged as a key application of WPCs owing to the material’s ability to reduce vehicle weight while maintaining mechanical strength and design flexibility. In electric and fuel-efficient vehicles, lightweighting is directly tied to energy efficiency and emissions reduction. WPCs provide a 20 to 30% weight advantage over conventional interior materials such as pure thermoplastics or solid wood. This makes the materials suitable for seatbacks, trunk liners, rear shelves, and door panels.

Distribution Channel Insights

Wholesalers and Retailers represent the dominant distribution channel in the Wood Plastics Composites Market, holding the largest revenue share driven by the established procurement infrastructure within the building materials supply chain. Contractors, homebuilders, and renovation professionals continue to source WPC decking, railing, and trim products primarily through regional and national building material distributors, lumber yards, and home improvement retailers such as The Home Depot and Lowe's Companies, Inc. in North America channels that offer on-hand inventory, technical support, and job-lot pricing that are difficult to replicate through alternative models. However, the E-commerce Platforms channel is exhibiting the fastest growth trajectory, reflecting shifting consumer procurement patterns for home improvement categories and the deliberate digital channel investments made by market leaders.

Regional Insights

North America Wood Plastics Composites Market Trends

In 2026, North America will likely account for around 42.6% of the wood plastics composites market share due to a well-established residential decking sector in the U.S. As per an online 2024 report, decking accounts for more than 65% of total WPC demand in the U.S., propelled by consumer preference for durable and low-maintenance alternatives to natural wood. Virginia-based Trex Company, for example, recently extended its manufacturing footprint with a new facility in Arkansas, focusing on meeting the high demand from southeastern U.S.

The U.S. wood plastics composites market is further predicted to see rapid growth amid a surging focus of manufacturers on sustainability. Leading companies are using recycled polyethylene and reclaimed wood fibers to attract eco-conscious consumers. Trex alone sources more than 1 Bn pounds of reclaimed materials annually, found Trex Sustainability Report 2023. Also, WPCs are gradually expanding beyond decking into areas such as cladding, outdoor furniture, and fencing. Recently, AZEK Building Products, for instance, introduced a new TimberTech cladding line to target the commercial real estate sector.

Europe Wood Plastics Composites Market Trends

Decking remains the leading WPC application in Europe, with solid profiles gaining traction over hollow types. The automotive industry, however, is increasingly adopting WPCs for interior trim, dashboard components, and door panels. Automakers are being encouraged to use these materials with Europe’s emphasis on lightweighting to enhance fuel and EV efficiency. Germany is considered the dominant producer and consumer of WPCs, serving as the epicenter of compounding and machinery capabilities.

The market in Europe is fragmented among domestic players such as Kosche, Tecnaro, Beologic, NOVO-TECH, and JELU-WERK. Various companies are competing through research and development into innovative WPC formulations, premium certifications, and acquisitions. Despite long-term durability benefits, fiber reinforced plastic composite materials such as WPCs in Europe still face hurdles due to high upfront costs and susceptibility to moisture and UV-related degradation. Ongoing research activities hence aim to enhance hydrophobicity and UV resilience.

Asia Pacific Wood Plastics Composites Market Trends

Increasing interest in sustainable materials across both residential and commercial sectors is a key factor pushing growth in Asia Pacific. Polyethylene-based WPCs remain the dominant formulation, but polypropylene-based composites are witnessing steady growth, mainly where high performance at low cost is required. Construction remains the key application, but significant momentum exists in consumer goods, packaging, industrial, and automotive due to the multitiered industrial growth and eco-conscious policies.

Foreign investment and joint venture activities are notable across Asia Pacific. Various manufacturers from Europe and North America are extending their production in this region through local facilities and partnerships to capitalize on cost advantages and regional demand. Japan and South Korea are expected to embrace WPCs, especially in automotive interiors. Companies in these countries are likely to tap into lightweighting trends to enhance fuel efficiency and comply with regulatory standards.

Competitive Landscape

The global wood plastics composites market exhibits a moderately consolidated competitive structure at the premium segment level, where a cohort of established North American and European manufacturers including Trex Company, Inc., The AZEK Company Inc. (TimberTech®), UFP Industries, Inc., Fiberon, LLC, and CertainTeed, LLC hold significant brand equity, channel relationships, and proprietary material science capabilities. At the commodity and regional product tier, however, the market remains fragmented, particularly across Asia Pacific, where a large base of Chinese and Indian manufacturers competes primarily on price. Market leaders are differentiating through vertically integrated recycling programs, proprietary extrusion technologies, fire-rated and regulatory-compliant product innovations, and aggressive capacity expansion investments

Key Developments:

- In April 2025, Century introduced its premium quality product called louvers made from wood plastic composite. It marked a significant step toward enhancing the market for functional and aesthetic interior and exterior solutions in India.

- In April 2025, Biesse India announced the launch of its new Material Hubs in six cities worldwide, namely, Toronto, Sydney, Porto, Lyon, and Osaka. This strategy marked a milestone in the company’s journey to transform its value proposition in an ever-changing world.

Companies Covered in Wood Plastics Composites Market

- CertainTeed, LLC

- Guangzhou Kindwood Co. Ltd.

- TAMKO Building Products LLC

- Oakio Plastic Wood Building Materials Co. Ltd.

- JELU-WERK J. Ehrler GmbH & Co. KG

- The AZEK Company Inc. (TimberTech)

- Hardy Smith Designs Private Limited

- Beologic

- FKuR Kunststoff GmbH

- Fiberon, LLC

- RENOLIT SE

- PolyPlank AB

- UFP Industries, Inc.

- Trex Company, Inc.

- Other Key Players

Frequently Asked Questions

The global wood plastics composites market is valued at US$ 12.7 Bn in 2026 and is projected to reach US$ 19.7 Bn by 2033, expanding at a CAGR of 6.5% over the forecast period.

The primary demand drivers include the global construction industry's adoption of sustainable, low-maintenance building materials aligned with green certification frameworks such as LEED and BREEAM, rapid urbanization in Asia Pacific, and the automotive sector's integration of WPC for lightweighting in electric vehicle platforms, where PP-wood composites deliver approximately 30% part-mass reduction per component.

The Polyethylene (PE) segment is the market leader, accounting for approximately 66% of total revenue share. Its dominance is supported by easy extrusion processability, compatibility with up to 60% wood flour loading without viscosity complications, competitive raw material pricing, and broad application versatility spanning decking, flooring, furniture, wall cladding, and automotive interior components.

North America, led by the United States, holds a dominant regional position driven by strong residential construction activity, high consumer spending on outdoor living products, stringent fire compliance codes such as the California WUI standards, and major manufacturing capacity investments by Trex Company, Inc. (US$ 400 million Arkansas facility) and UFP Industries, Inc. (US$ 250 million expansion plan).

The leading companies in the global Wood Plastics Composites Market include Trex Company, Inc., The AZEK Company Inc. (TimberTech®), UFP Industries, Inc. (Deckorators®), Fiberon, LLC, CertainTeed, LLC, RENOLIT SE, TAMKO Building Products LLC, PolyPlank AB, JELU-WERK J. Ehrler GmbH & Co. KG, FKuR Kunststoff GmbH, Beologic, Guangzhou Kindwood Co. Ltd., and Oakio Plastic Wood Building Materials Co. Ltd., among others.