- Automotive Components & Materials

- Automotive Door Panel Market

Automotive Door Panel Market Size, Share, and Growth Forecast, 2025 - 2032

Automotive Door Panel Market by Product Type (Front-hinged doors, Rear-hinged doors, Scissor door and Gullwing doors), Distribution Channel (OEM and Aftermarket), Vehicle Type (Passenger Car, LCV, HCV and Electric Vehicles) and Regional Analysis for 2025 - 2032

Automotive Door Panel Market Size and Trends Analysis

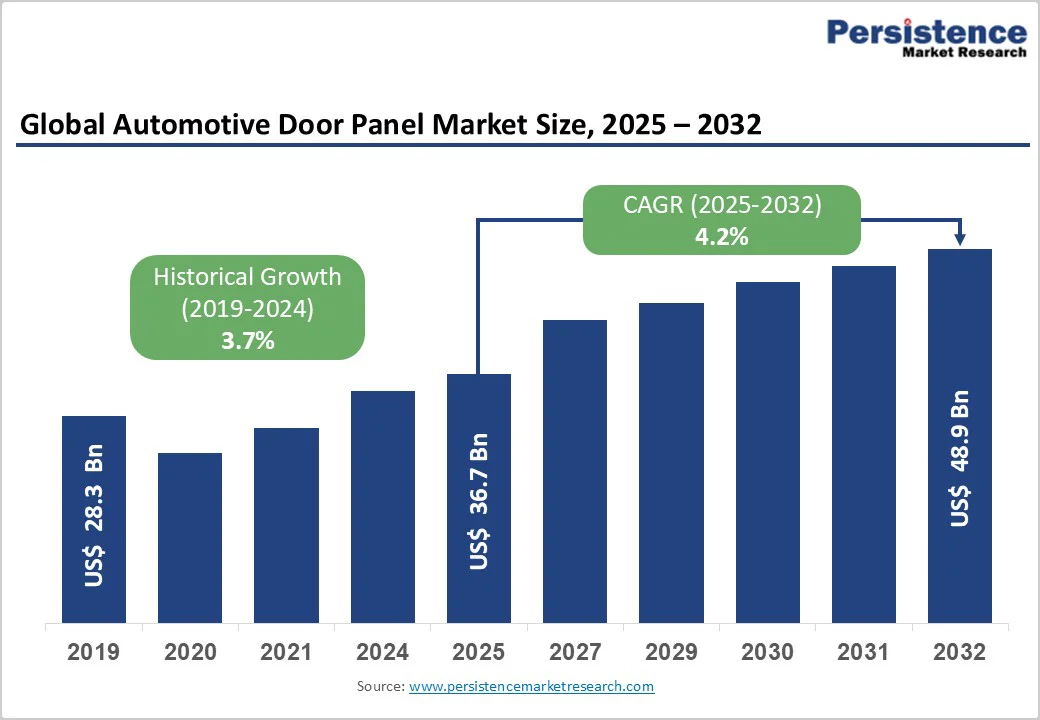

The global automotive door panel market size was valued at US$ 36.7 billion in 2025 and is projected to reach US$ 48.9 billion by 2032, growing at a CAGR of 4.2% between 2025 and 2032.

The increasing global production of vehicles, coupled with heightened consumer demand for advanced interior features, is set to propel the market forward. The industry will also benefit from a growing emphasis on lightweight materials to enhance fuel efficiency, driving innovation in panel design.

Key Industry?Highlights:

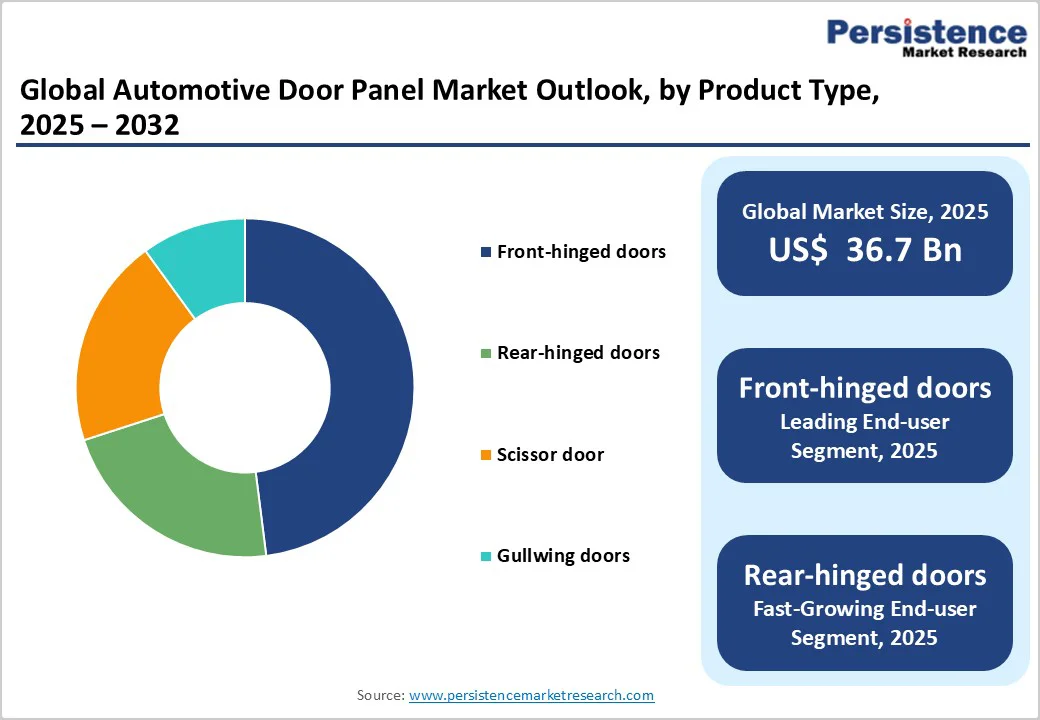

- Product Segments: Front-hinged doors dominate with a 42.8% market share, supported by universal adoption across vehicle platforms, cost-efficient engineering, and established compatibility with global automotive standards. Rear-hinged doors represent the fastest-growing product segment, expanding at 7-10% CAGR, driven by increasing integration in luxury vehicles and emerging demand from autonomous vehicle designs requiring wider cabin access.

- Sales Channel Segments: The OEM channel leads with a 65.4% market share, driven by primary demand from new vehicle production and automaker integration of advanced door systems into factory specifications. The aftermarket segment is the fastest-growing channel at 52% CAGR, supported by an aging global vehicle fleet-over 1 billion units exceeding 12 years driving replacement and retrofit demand.

- Vehicle Type Segments: Passenger cars command a 58.4% share, reflecting the highest production volumes and widespread use of standardized door architectures. Electric vehicles (EVs) are the fastest-growing vehicle segment, expanding at 18% CAGR, driven by adoption of specialized door formats such as gullwing and falcon-wing designs, along with lightweighting requirements intrinsic to EV engineering.

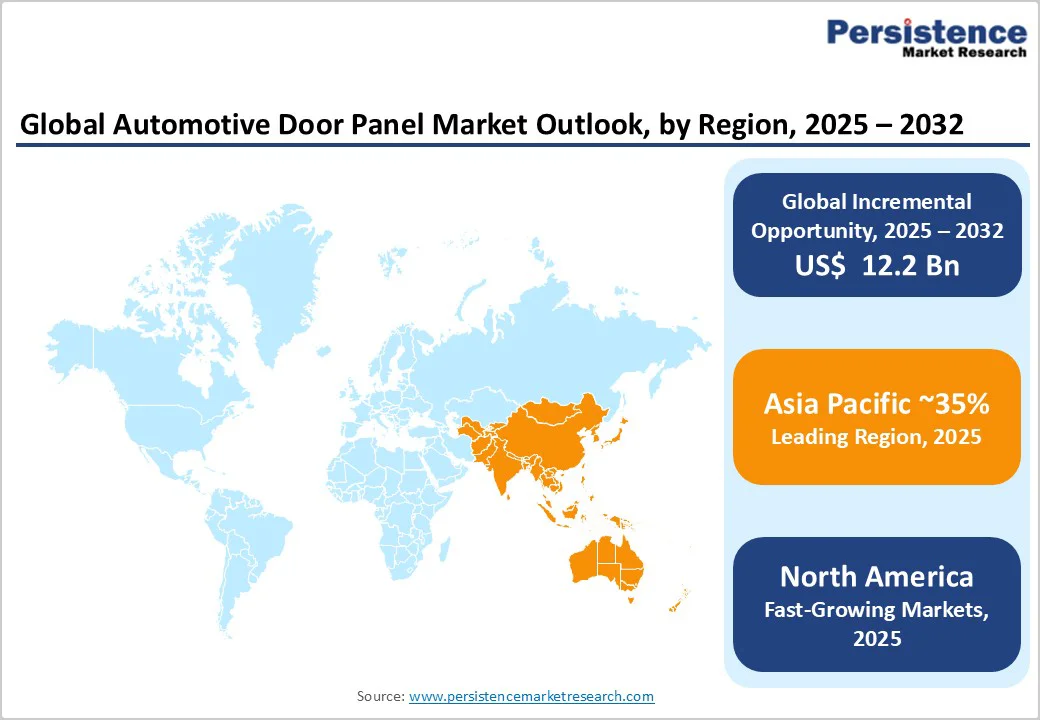

- Regional Leaders: Asia-Pacific leads the global market with a 35% share, growing at 8.2% CAGR, anchored by China’s dominant manufacturing base (accounting for 42% of regional demand) and India’s rapid expansion (6% CAGR). North America captures 25% of global share with a 4.8% CAGR, while Europe holds 22% share, growing at 4.5% CAGR, supported by continuous platform modernization and premium vehicle production strength.

| Key Insights | Details |

|---|---|

| Automotive Door Panel Market Size (2025E) | US$ 36.7 Bn |

| Market Value Forecast (2032F) | US$ 48.9 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.7% |

Market Dynamics

Drivers - Rise in Vehicle Production and Sales

One of the key drivers shaping the automotive door panel market is the sustained growth in global vehicle production and sales. The rising demand for automobiles, including passenger cars and commercial vehicles, directly influences the demand for door panels. As automotive manufacturers increase their production capacities to meet consumer needs, the requirement for door panels grows proportionally.

This driver is particularly significant in emerging economies where a burgeoning middle class and urbanization contribute to a higher demand for vehicles. The expanding automotive market, driven by economic growth and increased disposable income, creates a favorable environment for the automotive door panel market to thrive, fostering innovation and competition among manufacturers to meet the escalating demand.

In addition, another critical driver steering the automotive door panel market is the industry's increasing emphasis on lightweight materials to enhance overall vehicle fuel efficiency.

As regulatory standards for fuel economy become more stringent globally, automotive manufacturers are seeking ways to reduce the weight of vehicles without compromising safety and structural integrity. Lightweight materials in door panels, such as advanced plastics and composites, play a pivotal role in achieving this objective.

The adoption of these materials not only contributes to fuel efficiency but also aligns with broader industry trends toward sustainability. As automakers strive to meet environmental regulations and consumer preferences for eco-friendly vehicles, the integration of lightweight materials in door panels becomes a strategic imperative, driving technological advancements in the automotive door panel market.

Restraint - Technological Advancements, and Innovation

Technological advancements play a pivotal role in shaping the performance of the automotive door panel market. Continuous innovation in materials, manufacturing processes, and design significantly influences the market dynamics.

Advanced materials, such as lightweight composites and smart materials with enhanced durability and safety features, contribute to the overall improvement of door panel performance. Innovations in manufacturing technologies, including efficient production methods and automation, can impact production costs and lead times, influencing the competitiveness of market players.

Additionally, the integration of smart features within door panels, such as touch-sensitive controls, integrated sensors, and connectivity options, aligns with the growing trend of connected vehicles.

As consumer preferences evolve and automotive manufacturers seek to differentiate their products, the pace of technological innovation becomes a key factor influencing the market performance of automotive door panels, driving both product development and market competition.

Stringent Regulatory Standards

One significant challenge facing the automotive door panel market is the adherence to stringent regulatory standards. Regulatory bodies worldwide are increasingly imposing strict guidelines related to vehicle safety, emissions, and materials used in manufacturing.

Compliance with these regulations poses a challenge for door panel manufacturers as they must ensure that the materials and designs meet safety standards without compromising on aesthetics and functionality.

Stricter emissions regulations especially may drive the need for lighter materials, impacting the traditional choices for door panel manufacturing. Navigating the complex landscape of evolving regulatory requirements requires continuous adaptation and investment in research and development to meet or exceed standards.

The challenge lies in striking a balance between compliance and innovation, ensuring that door panels not only meet regulatory criteria but also align with consumer expectations and market trends.

Opportunities - Integration of Advanced Features

An opportunity for increasing revenue in the automotive door panel market lies in the integration of advanced features. The evolving demands of consumers for enhanced comfort, convenience, and connectivity pave the way for incorporating innovative technologies within door panels. Manufacturers can explore the integration of touch-sensitive controls, ambient lighting, and smart sensors that enhance user experience and contribute to the overall appeal of the vehicle's interior.

By offering door panels with advanced features, companies can differentiate their products in the market, potentially commanding premium pricing and capturing a segment of consumers seeking technologically sophisticated automotive interiors. This avenue not only caters to current consumer trends but also positions manufacturers strategically in an increasingly competitive landscape.

Moreover, another lucrative opportunity in the automotive door panel market is the rising trend of customization and personalization. Consumers increasingly seek vehicles that reflect their individual style and preferences. Door panels, being a prominent part of a vehicle's interior, offer a canvas for customization. Manufacturers can capitalize on this trend by providing a range of customizable options, including materials, colors, textures, and design elements.

Offering personalized door panels allows manufacturers to tap into niche markets and cater to diverse consumer tastes. This not only enhances customer satisfaction but can also open up avenues for premium pricing models, contributing to increased revenue. Embracing customization trends aligns with the broader shift towards providing unique and tailored automotive experiences, presenting a compelling opportunity for growth in the automotive door panel market.

Category-wise Analysis

Product Type Insights

Front-hinged doors command 42.8% market share due to their universal use in automotive architecture, mature manufacturing ecosystem, and cost-effective production supporting widespread adoption across passenger and commercial vehicles.

Their dominance is reinforced by proven durability, regulatory standardization, and consumer familiarity, with over 90% of global vehicles still relying on this traditional design. Established supply chains and high-volume production enable competitive pricing of $400-700 per unit, while strong aftermarket compatibility ensures long-term demand.

Rear-hinged doors are the fastest-growing segment at around 7% CAGR, driven by rising luxury vehicle integration, superior cabin accessibility for autonomous vehicle concepts, and specialized commercial applications requiring enhanced side entry. Their use in premium sedans, mobile service vehicles, and future AV interiors supports accelerating adoption.

Distribution Channel Insights

The OEM segment commands 65.4% market share, driven by consistent demand from new vehicle production, which ensures predictable volumes and long-term supplier commitments.

Major automakers such as Toyota, Volkswagen, GM, Ford, Stellantis, Hyundai, and Geely source door panels across diverse vehicle lineups, aligning demand directly with global production output. OEM requirements for just-in-time delivery, stringent quality standards, and lifecycle support create strong supplier integration, technology collaboration, and premium pricing opportunities.

The aftermarket segment is growing at 5.6% CAGR, supported by the aging global vehicle fleet, accident-related replacement needs, and rising customization trends. With over 1 billion vehicles in operation and average ages of 12 years in mature markets, the replacement of worn or damaged door panels is a continuous driver.

Vehicle Type Insights

Passenger cars hold 58.4% market share, supported by annual production volumes exceeding 70 million units and long-standing OEM supplier relationships.

Mainstream sedans, SUVs, and crossovers-accounting for over 80% of passenger vehicle output drive consistent door panel demand, while luxury brands such as BMW, Mercedes-Benz, Audi, and Porsche push higher-value specifications through premium materials and advanced designs. A strong customization ecosystem further boosts demand through interior upgrades and personalization services.

Electric vehicles represent the fastest-growing segment at roughly 18% CAGR, driven by EV production projected to reach 39 million units by 2030 and the need for specialized door architectures such as gullwing and falcon-wing systems. EV manufacturers increasingly adopt lightweight composites and thermoplastics to improve efficiency, establishing distinct design and material requirements compared to traditional ICE vehicles.

Regional Insights and Trends

North America Automotive Door Panel Market Share Insights

North America generates approximately US$10.2 billion market value in 2025 representing 30% global market share growing at 4.8% CAGR through 2032, driven by high vehicle production volumes, light truck and SUV market dominance, and robust aftermarket supporting aging vehicle fleet.

The United States dominates regional market with 78-82% North American share through automotive production exceeding 10 million vehicles annually, extensive SUV and light truck production requiring specialized door panel designs for oversized vehicles, and well-established aftermarket distribution networks.

Light truck segment commanding 80% U.S. production preference drives specialized door panel requirements for crew-cab configurations and premium interior appointments supporting higher-value component specifications. Luxury vehicle concentration including premium sedans and performance vehicles, supports material innovation adoption with carbon fiber and advanced composite penetration exceeding 15-20% in premium segments.

Europe Automotive Door Panel Market Insight

Europe is emerging as a dominating region in the automotive door panel market due to its status as a technological advancements and innovation hub. European countries are at the forefront of developing and implementing cutting-edge automotive technologies. The region's emphasis on research and development fosters innovation in door panel materials, manufacturing processes, and integrated smart features.

Automotive manufacturers in Europe leverage this technological prowess to produce door panels that align with the latest industry trends, attracting both domestic and international demand. The continuous pursuit of innovation positions Europe as a leader in developing sophisticated door panel solutions, contributing to the region's dominance in the global market.

Asia Pacific Automotive Door Panel Market Trends

Asia Pacific represents a dominant region at approximately 35% of global market share with an estimated market value of US$18.7 billion by 2025, driven by automotive manufacturing leadership, emerging market vehicle ownership expansion, and EV adoption acceleration.

Asia Pacific presents significant opportunities for manufacturers in the automotive door panel market due to the rapid growth of the automotive industry in the region. With increasing urbanization, rising disposable incomes, and a growing middle class, there is a surge in demand for vehicles.

The heightened demand directly translates to a need for automotive components, including door panels. Manufacturers establish strong partnerships with regional automakers and capitalize on the expanding market to secure a substantial share in the growing automotive industry of Asia Pacific.

Competitive Landscape

Prominent organizations, including Grupo Antolin, Faurecia, Magna International, Brose Fahrzeugteile, are at the vanguard of this sector, competitive intelligence in the automotive door panel market involves a comprehensive analysis of key industry players, their market share, product portfolios, and strategic initiatives.

Manufacturers keenly observe competitors to understand market trends, technological advancements, and pricing strategies. Insights into the competitive landscape enable companies to identify opportunities for differentiation and innovation.

Monitoring competitors' supply chain dynamics and production efficiency also plays a crucial role in maintaining a competitive edge. Analysing customer preferences and anticipating market shifts based on competitors' actions allows companies to proactively adjust their strategies.

Key Industry Developments

- In April 2024, Plastic Omnium and Brose announced their partnership to manufacture and market new side-door systems for vehicles. The goal of this partnership is to bring cylinder-shaped door designs, which include both plastic and metal elements, into the automotive manufacturing industry. Plastic Omnium will apply its know-how on body panels, crash optimization, and external vehicle structures system engineering.

- In September 2023, Technology company Continental will present its Curved Ultrawide Display at CES September 2023. "Ultrawide" refers to a width of 1.29 meters, curving from one A-pillar to the other. The 47.5-inch TFT display is illuminated by more than 3,000 LEDs on a 7,680 by 660- pixel active area.

Companies Covered in Automotive Door Panel Market

- Grupo Antolin

- Faurecia

- Magna International

- Brose Fahrzeugteile

- Yanfeng Automotive Interiors

- Toyoda Gosei Co., Ltd.

- Draexlmaier Group

- Kasai Kogyo Co., Ltd.

- Hayashi Telempu Co., Ltd.

- Johnson Controls International plc

- Other Market Players

Frequently Asked Questions

The Automotive Door Panel market is estimated to be valued at US$ 36.7 Bn in 2025.

The key demand driver for the Automotive Door Panel market is the global surge in vehicle production and the shift toward premium, lightweight, and technologically advanced interiors.

In 2025, the Asia Pacific region will dominate the market with an exceeding 35% revenue share in the global Automotive Door Panel market.

Among the Product Type, Front-hinged doors hold the highest preference, capturing beyond 42.8% of the market revenue share in 2025, surpassing other Product Type.

The key players in the Automotive Door Panel market are Grupo Antolin, Faurecia, Magna International and Brose Fahrzeugteile.