- Home Care & Utilities

- Plywood Market

Plywood Market Size, Share, and Growth Forecast, 2026 - 2033

Plywood Market By Plywood Type (Softwood Plywood, Hardwood Plywood, Others), Product (MR, BWR / BWP, Others), Application, Distribution, and Regional Analysis for 2026 - 2033

Plywood Market Size and Trends Analysis

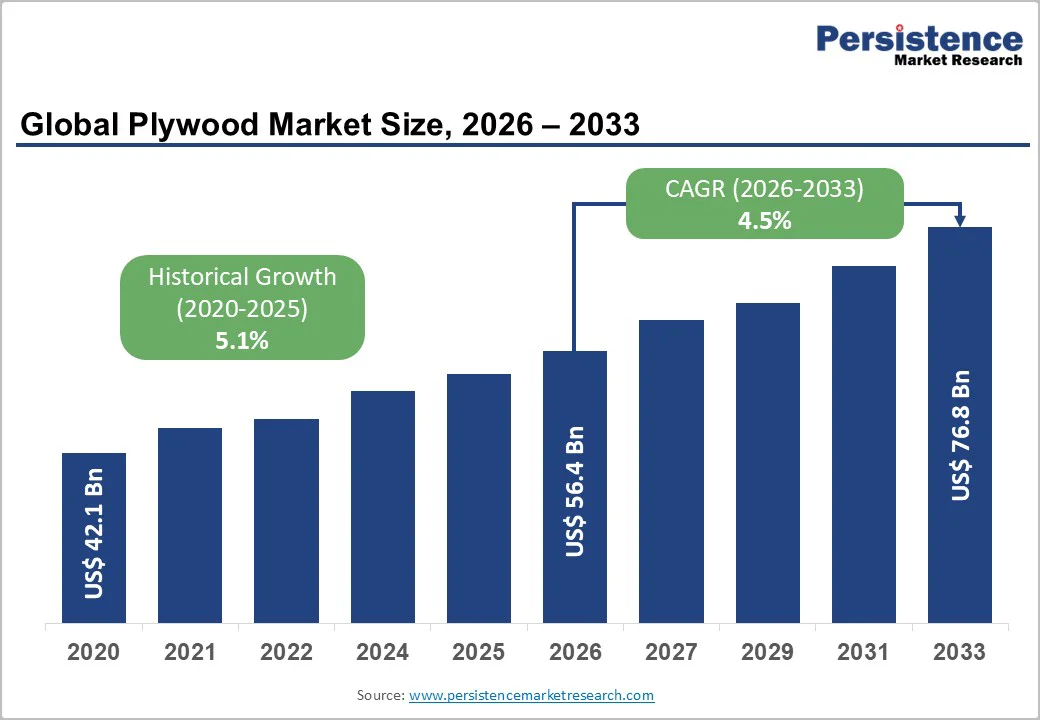

The global plywood market size is likely to be valued at US$56.4 Billion in 2026 and is expected to reach US$76.8 Billion by 2033, growing at a CAGR of 4.5% during the forecast period from 2026 to 2033, driven by rising residential and commercial construction activities, expanding furniture production, and the shift toward engineered wood products in manufacturing applications.

Strengthening regulatory emphasis on sustainable building materials continues to accelerate plywood adoption across major markets. Demand patterns align with long-term urbanization, higher spending on interior renovation, and strengthening supply chain capabilities in emerging Asia.

Key Industry Highlights

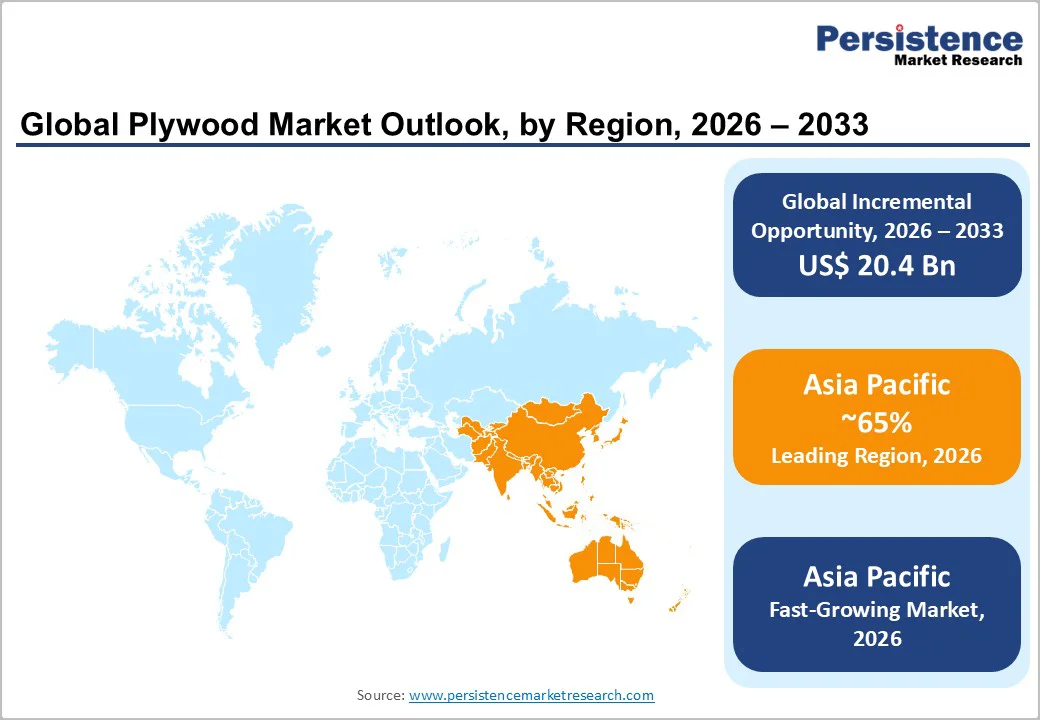

- Leading Region: Asia Pacific accounts for over 65% of global plywood volume, driven by strong manufacturing capacity and great domestic demand.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, supported by housing programs, retail furniture demand, and sector formalization.

- Investment Plans: Major producers across the Asia Pacific are implementing large-scale capacity expansions, automation upgrades, and new veneer-milling lines, contributing to notable multi-year capital spending growth.

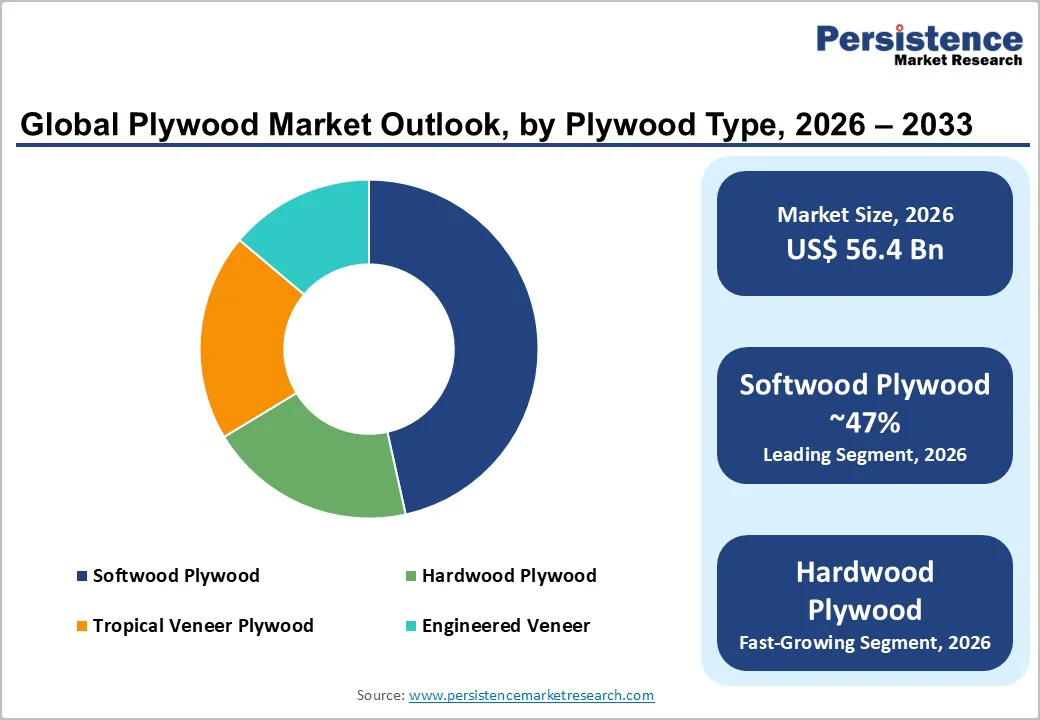

- Dominant Product Type: Softwood plywood remains the largest segment, expected to hold 47% of the market share, driven by strong consumption in structural construction, flooring substrates, exterior sheathing, concrete formwork, pallets, and industrial packaging.

- Leading Application: Construction and sheathing applications represent the largest segment, accounting for approximately 46% of market share in 2026, due to load-bearing performance, screw-holding capacity, dimensional stability, and easy machinability.

| Key Insights | Details |

|---|---|

| Plywood Market Size (2026E) | US$56.4 Bn |

| Market Value Forecast (2033F) | US$76.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Global Construction Activity

Rapid increases in residential and commercial construction expenditure continue to strengthen plywood demand, particularly in structural applications, interior finishing, and modular housing. According to global construction indicators published by international economic bodies, worldwide construction output is expected to expand, driven by sustained investment in housing, infrastructure modernization, and population migration toward urban centers.

The demand for durable, cost-efficient, and versatile building materials positions plywood as a preferred choice for flooring, roofing, sheathing, and wall systems. The widespread presence of small and medium-scale contractors further reinforces volume consumption, supporting stable long-term demand growth.

Growth of the Furniture and Interior Products Industry

The global furniture market continues to expand due to rising disposable incomes, increased homeownership rates, and heightened consumer interest in home interiors. Industry data shows that furniture production output across Asia Pacific and North America has steadily risen over the past decade, supported by lifestyle upgrades and greater emphasis on household aesthetics.

Plywood is widely used for cabinetry, shelves, partitions, and decorative panels because of its strength, dimensional stability, and workability. Manufacturers increasingly prefer plywood over solid wood due to cost benefits and enhanced design flexibility. These factors collectively enhance plywood consumption across both mass-market and premium furniture categories.

Rising Adoption of Engineered Wood for Sustainability Compliance

Regulatory authorities in key markets have intensified their focus on reducing carbon emissions, encouraging the use of engineered wood materials that minimize waste and support circular-economy objectives. Plywood, which optimizes timber utilization through layer-based construction, aligns with environmental certification standards related to renewable sourcing and responsible forest management.

International sustainability programs continue to promote engineered panels as alternatives to non-renewable materials. Growing alignment between construction regulations and green-building frameworks encourages broader adoption of plywood in infrastructure and urban development projects, improving overall market penetration.

Barrier Analysis - Volatility in Timber Supply and Price Fluctuations

Irregularities in log availability and fluctuating timber prices pose challenges for plywood producers, particularly those dependent on imported sources. Variations in forest yield, regulatory restrictions on logging, and transportation disruptions create cost unpredictability across the value chain.

Producers operating on thin margins are especially vulnerable to spikes in raw-material costs, which can reduce profitability and limit expansion capacity. Higher procurement expenses also impact downstream product pricing, affecting competitiveness in cost-sensitive applications.

Growing Competition from Alternative Engineered Wood Products

The increasing availability of substitutes, such as medium-density fiberboard, oriented strandboard, and particleboard, creates a competitive environment for plywood manufacturers. These materials offer varying benefits, including lower cost, lighter weight, and improved surface uniformity, attracting demand in furniture and interior solutions.

Continuous product development in the broader engineered-wood ecosystem intensifies the challenge for plywood producers to differentiate their offerings. Price-sensitive industries, such as low-cost furniture manufacturing, are particularly inclined toward alternative products, restraining plywood’s growth in some application segments.

Opportunity Analysis - Expansion of Green Buildings and Certified Wood Products

Global adoption of green building standards continues to accelerate, creating favorable conditions for certified plywood products that meet low-emission and sustainability criteria. Governments increasingly integrate energy-efficient and eco-friendly construction standards into public infrastructure development, presenting substantial procurement opportunities. Certified plywood for interior panels, acoustic systems, and modular construction components has significant market potential.

Rapid Urbanization and Affordable Housing Programs

Large-scale housing initiatives across Asia Pacific, Africa, South America, and parts of the Middle East offer long-term opportunities for plywood manufacturers. Demand growth is linked to economic development, rising populations, and infrastructure expansion.

Governments continue to allocate funding for affordable housing programs, creating a substantial volume requirement for cost-efficient and durable building materials. Plywood’s adaptability and function in roofing, wall systems, and interior finishing position it well to benefit from new construction activities.

Technological Advancements in Plywood Manufacturing

Automation, improved adhesives, digital quality control, and environmental compliance systems are transforming plywood manufacturing capabilities. Modern production lines allow enhanced durability, improved bonding performance, and customized product variants targeting high-end furniture, marine, and structural applications.

Innovations in veneer processing and surface finishing also support new market opportunities in decorative interiors. Manufacturers adopting advanced production technologies can access higher-margin segments and strengthen competitive differentiation.

Category-wise Analysis

Product Type Insights

Softwood plywood is likely to be the largest segment, and is expected to hold about 47% of the market in 2026, driven by strong use in structural construction, flooring substrates, exterior sheathing, concrete formwork, pallets, and industrial packaging. Large integrated forest-product companies and sawmills provide a consistent veneer supply, ensuring panel strength, uniformity, and compliance with building-code requirements.

This structural reliability continues to support softwood plywood’s preference across residential framing, roofing assemblies, and infrastructure projects. Its dominance is further reinforced by mature distribution networks serving construction merchants, building-material retailers, and OEM buyers, making softwood plywood the default choice for a wide range of structural and semi-structural applications.

Hardwood plywood is projected to be the fastest-growing segment, especially in revenue terms, supported by rising demand in furniture manufacturing, architectural interiors, premium fit-outs, and export-oriented joinery. Consumers in Asia, Europe, and higher-income markets increasingly value aesthetics, surface consistency, and premium finishes, favoring hardwood veneer panels.

Strong growth is seen in decorative, fire-retardant, and certified specialty plywood, where producers with secured veneer sourcing in Southeast Asia and West Africa achieve notable margin advantages. Manufacturers investing in calibrated sanding, integrated finishing lines, pre-lamination, and digital surface treatments are well-positioned to capture accelerating demand from furniture OEMs, interior contractors, and project-driven commercial segments.

Application Insights

The construction and sheathing application segment is anticipated to be the largest segment, accounting for roughly 46% of market share in 2026. This category covers building sheathing, roofing substrates, subfloors, structural bracing, concrete formwork, scaffolding platforms, and on-site structural frameworks.

Plywood’s strength-to-weight ratio, screw-holding capability, dimensional stability, and ease of machining make it a preferred material across residential, commercial, and infrastructure projects. Rapid urbanization, rising housing starts, and steady commercial renovation cycles continue to sustain demand.

Public-sector investment in bridges, transit facilities, civic buildings, and industrial expansion further supports consistent procurement cycles for panel manufacturers. Strong distribution networks serving contractors and building-material suppliers reinforce the segment’s dominance, making construction the most resilient and highest-volume demand base.

Furniture and interior applications represent the fastest-growing segment, driven by rising demand for decorative panels, moisture-resistant grades, and premium engineered surfaces. Growth in middle-income households, renovation activity, and preference for high-quality finishes are boosting demand for calibrated and aesthetically enhanced plywood.

Producers capable of consistent veneer matching, advanced surface finishing, and reliable OEM supply gain a competitive edge. Expanding adoption of modular kitchens, wardrobes, and custom interior solutions further accelerates demand, positioning this segment among the most lucrative and rapidly evolving categories.

Regional Insights

North America Plywood Market Trends - Renovation-Led Demand & Sustainability-Certified Panel Adoption

North America is a high-value plywood market supported by a mature construction sector and high per-capita use of engineered wood products. The U.S. drives regional demand, propelled by steady housing starts, recurring home-renovation cycles, and consistent non-residential construction.

Institutional spending, infrastructure modernization, and commercial upgrades provide stability and reduce volatility. Canada adds strength through abundant softwood resources and an active panel-processing industry that serves both domestic needs and U.S. markets.

Regional growth is further reinforced by renovation activity tied to aging housing stock, sustainability-focused procurement favoring FSC- and PEFC-certified panels, and the expanding use of modular and off-site construction, especially in multi-family housing. These forces support higher-value product categories and help suppliers manage cyclical exposure.

Regulation strongly shapes market access, with certification requirements, timber-legality rules, and building-code compliance influencing competitiveness. LEED-aligned procurement and legality verification increasingly determine eligibility for public and private projects. Trade measures, including tariffs and anti-dumping actions, periodically alter the balance between imports and domestic production, affecting pricing and supply.

Investment priorities center on automation, advanced surface finishing, and expanded capacity for fire-retardant and marine-grade plywood. Manufacturers are also strengthening traceability and carbon accounting to meet evolving sustainability standards. Recent industry activity includes selective mill rationalization, strategic acquisitions, and heightened emphasis on certified, performance-oriented panel grades.

Europe Plywood Market Trends - High-Spec Certified Panels Driven by Strict Standards & Renovation Programs

Europe is a high-value plywood market defined by stringent certification requirements, rigorous emissions and fire-safety standards, and a strong emphasis on sustainability.

Although total consumption is smaller than in Asia, the region commands higher average selling prices due to extensive use of certified, specialty, and high-performance panels. Recent EU trade actions, including investigations and provisional duties on imported plywood, have reshaped import patterns and strengthened the competitive positioning of domestic and intra-EU suppliers.

Germany and the U.K. remain the leading consumers of high-specification plywood for furniture manufacturing, interior fit-outs, and construction. France and Spain also demonstrate solid demand driven by renovation cycles, residential upgrades, and commercial building activity. Germany’s large furniture and interior solutions industry further supports stable consumption of quality-certified plywood.

Key growth drivers include strong renovation activity supported by energy-efficiency and retrofit programs, green procurement standards favoring sustainably sourced plywood, and continued commercial construction, particularly in office refurbishments, education facilities, and hospitality upgrades.

Investments across Europe focus on automation, advanced adhesive systems to meet emissions limits, and expanded production of fire-rated and marine-grade plywood. Exporters serving the EU increasingly prioritize traceability, legality assurance, and comprehensive documentation to maintain compliance and market access.

Asia Pacific Plywood Market Trends - Global Volume Hub Powered by Urbanization & Large-Scale Production Capacity

Asia Pacific is expected to account for more than 65% of global plywood volume in 2026, making it the leading region in both production and consumption. China, India, Indonesia, and major ASEAN countries anchor global capacity, supported by cost competitiveness, abundant labor, access to veneer materials, and large domestic markets that enable economies of scale.

China remains a dominant producer and consumer, with evolving environmental regulations and sourcing requirements reshaping production costs and supply-chain practices.

India is one of the fastest-growing markets, driven by rapid formalization of the plywood sector, capacity expansion by leading domestic manufacturers, strong, affordable-housing demand, rising retail furniture nsumption, and substantial government infrastructure investment.

Export-oriented producers in Indonesia, Malaysia, and Gabon continue to supply significant volumes of veneer and logs, influencing global pricing through plantation expansion and regulatory adjustments.

Regional growth is further fueled by urbanization, growing middle-class furniture demand, expansion of organized retail, and large housing initiatives across emerging economies. Asia Pacific also benefits from increasing export orientation in standardized plywood and veneer grades.

Investment momentum remains strong, with India adding capacity, manufacturers upgrading veneer-milling technologies, and producers expanding marine and fire-retardant panel output. Companies are also improving adhesives, emissions compliance, and traceability systems to meet tightening global standards and strengthen higher-value export competitiveness.

Competitive Landscape

The global plywood market features a top-heavy structure dominated by large integrated forest-products corporations alongside highly fragmented regional markets. Major players control timber, veneer, and panel operations, capturing substantial value, while regional manufacturers thrive on raw material proximity and strong distributor networks. This dual model drives price competition in commodity grades but supports premium niches for certified or specialty panels.

Leading firms emphasize vertical integration, sustainability certification, and value-added products, leveraging scale and logistics for institutional contracts. Emerging competitors differentiate through niche grades, localized distribution, and export-driven opportunities.

Key Industry Developments

- In January 2025, Paged Plywood introduced RockPly, a novel plywood variant using rock-fiber reinforcement, which reportedly offers roughly twice the strength of traditional plywood along with improved thermal resistance and lower weight.

- In July 2025, Plyneer Industry Pvt. Ltd. launched a premium plywood line under the name Plyneer Club, a fire-retardant and waterproof plywood that the company is backing with a “100 Test Challenge” (100 real-world stress tests), aiming to ensure long-term durability and structural integrity.

Companies Covered in Plywood Market

- Georgia-Pacific

- Weyerhaeuser

- Boise Cascade

- Roseburg

- UPM

- Sveza

- Metsä Wood

- West Fraser

- Canfor

- Greenply Industries

- Century Plyboards

- Kitply Industries

- Samling Group

- Austral Plywoods

- PotlatchDeltic

- Tolko Industries

- Kronospan

- Evergreen Plywood

- Joubert Group

- Richmond Plywood Corporation

Frequently Asked Questions

The global plywood market size is estimated to reach US$56.4 Billion in 2026.

By 2033, the plywood market is projected to reach US$76.8 Billion.

Major trends include growing demand for certified and sustainably sourced plywood, increasing adoption of fire-retardant and marine-grade panels, expansion of modular construction, investment in automated manufacturing lines, and strengthening regulatory requirements for emissions, timber legality, and traceability.

Softwood plywood remains the dominant type due to its structural strength, availability, and extensive use in construction.

The plywood market is expected to expand at a CAGR of 4.5% between 2026 and 2033.

Leading companies include Georgia-Pacific, Weyerhaeuser, Boise Cascade, Roseburg, and UPM.