- Advanced Materials

- Wood-Based Panel Market

Wood-Based Panel Market Size, Share, and Growth Forecast, 2026 – 2033

Wood-Based Panel Market by Product Type (Medium Density Fiberboard (MDF), High Density Fiberboard (HDF), Others), Application (Furniture, Construction, Packaging), and Regional Analysis for 2026 – 2033

Wood-Based Panel Market Size and Trends Analysis

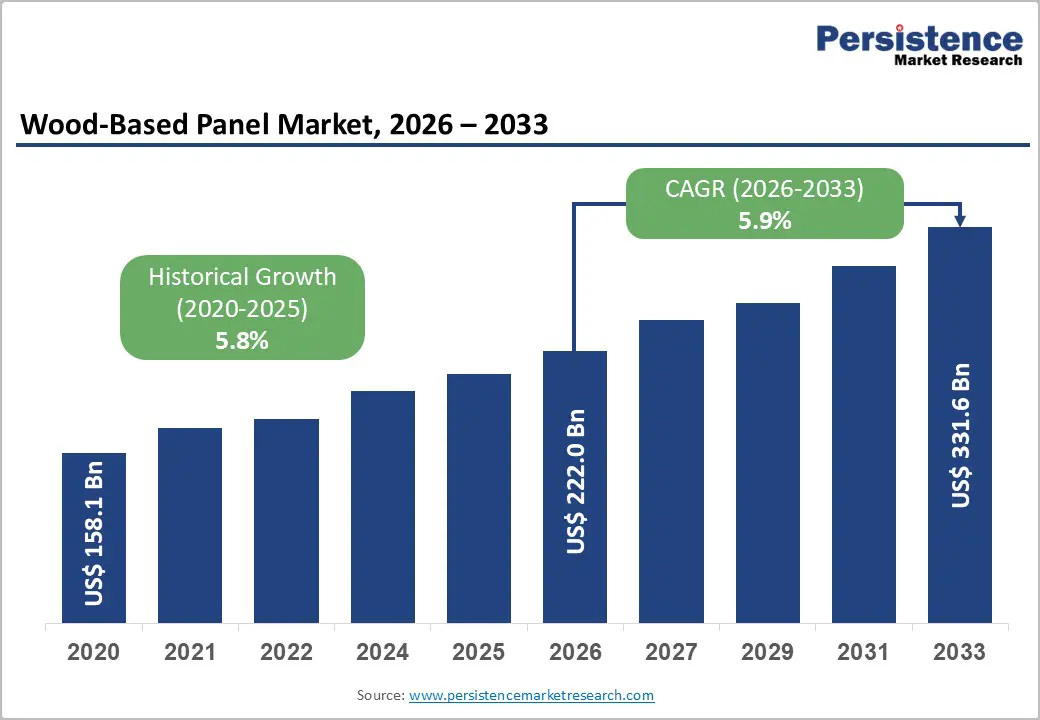

The global wood-based panel market size is likely to be valued at US$222.0 billion in 2026 and is expected to reach US$331.6 billion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033, driven by rapid urbanization and increasing construction activities, particularly in emerging economies, which fuel demand for plywood, MDF, and particleboard in residential and commercial infrastructure.

The rising adoption of cost-effective, lightweight, and sustainable materials in furniture manufacturing is accelerating the use of engineered wood panels as substitutes for solid timber. Expanding packaging applications, coupled with growing consumer and regulatory emphasis on environmentally responsible sourcing, low-emission products, and recycled wood content, further support market penetration. Technological advancements in panel manufacturing, including improved resin systems and enhanced moisture- and fire-resistant properties, are expanding the application scope of wood-based panels across interior and structural uses.

Key Industry Highlights:

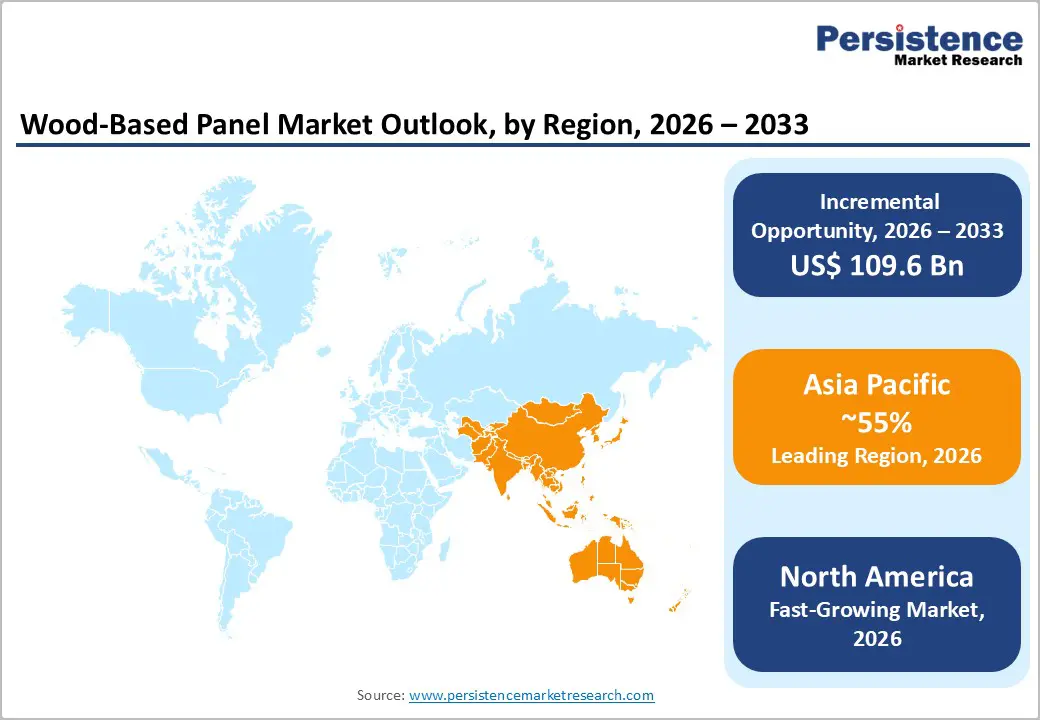

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 55% in 2026, driven by rapid urbanization, strong construction activity, and large-scale manufacturing across China, India, Japan, and ASEAN economies.

- Fastest-growing Region: North America is likely to be the fastest-growing region, supported by strong residential construction activity, renovation demand, and increasing adoption of sustainable and engineered wood products in the U.S. and Canada.

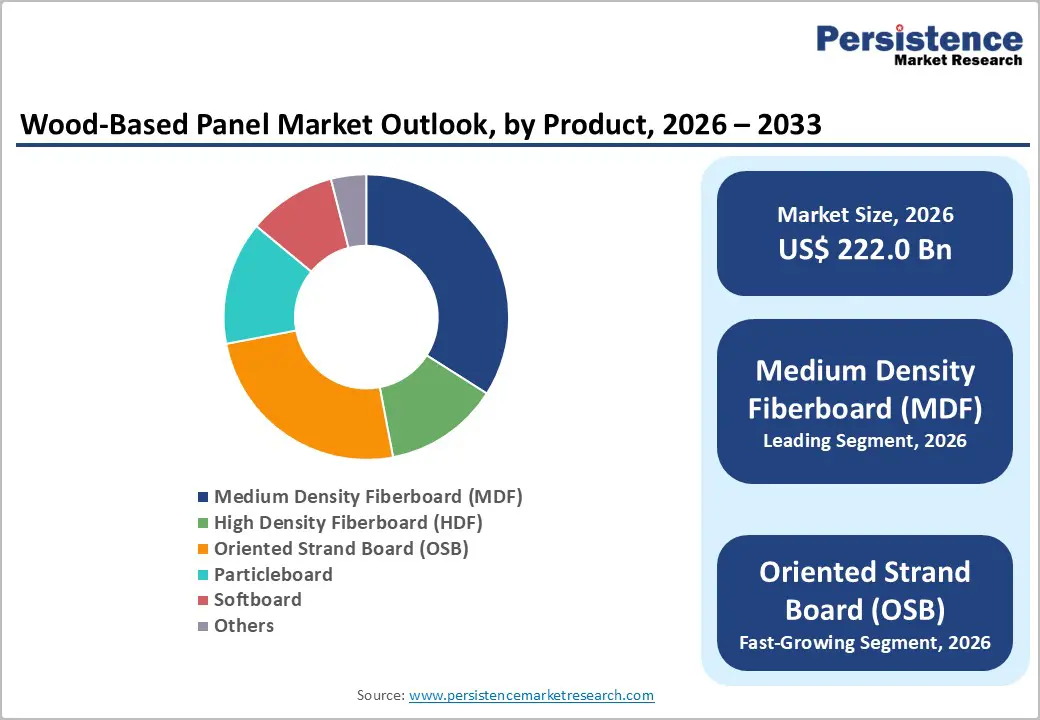

- Leading Product Type: Medium Density Fiberboard (MDF) is projected to represent the leading product type in 2026, accounting for 40% of the revenue share, driven by strong demand in furniture, cabinetry, and interior décor applications.

- Leading Application: The construction segment is anticipated to be the leading application, accounting for over 45% of revenue in 2026, supported by the extensive use of wood-based panels in residential and commercial building activities.

| Key Insights | Details |

|---|---|

| Wood-Based Panel Market Size (2026E) | US$222.0 Bn |

| Market Value Forecast (2033F) | US$331.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Construction and Urbanization Activities

Expanding urban populations are increasing the demand for residential housing, commercial buildings, and public infrastructure, directly boosting consumption of engineered wood products such as MDF, particleboard, OSB, and plywood. Governments in the Asia Pacific, the Middle East, and parts of Latin America are investing heavily in affordable housing programs, smart cities, and large-scale infrastructure projects, which require cost-effective, lightweight, and easy-to-install building materials.

Wood-based panels are widely used in flooring, wall panels, roofing, partitions, and interior fittings due to their dimensional stability and design flexibility. Urban redevelopment and renovation activities in mature markets such as North America and Europe support steady demand, as wood panels are preferred for retrofitting, remodeling, and interior upgrades in residential and commercial spaces.

Urbanization also encourages the adoption of modern construction practices, including prefabrication, modular housing, and sustainable building designs, all of which favor the use of wood-based panels. Engineered panels such as OSB and MDF enable faster construction timelines, reduced labor costs, and more efficient material use than traditional solid-wood or concrete-based solutions. The growing emphasis on green buildings and energy-efficient structures further strengthens demand, as wood-based panels offer lower carbon footprints and compatibility with environmentally responsible construction standards. Increasing urban lifestyles drive demand for aesthetically appealing interiors, leading to greater use of decorative panels in apartments, offices, retail spaces, and hospitality projects.

Tightening Emission and Environmental Regulations

Stringent limits on formaldehyde and volatile organic compound (VOC) emissions, enforced through standards such as CARB Phase II, EPA TSCA Title VI, and European E1/E0 norms, require panel producers to invest heavily in advanced resin technologies, emission-control systems, and continuous product testing. Smaller and mid-sized manufacturers often face challenges in upgrading facilities and sourcing compliant raw materials, which can limit their competitiveness and slow capacity expansion. Regulations governing sustainable forestry and legal timber sourcing impose stricter documentation and certification requirements, adding operational burdens across the supply chain.

Environmental regulations also create market entry barriers and regional inconsistencies that restrain overall growth. In emerging economies, uneven enforcement of emission standards can disrupt trade flows, as non-compliant products face restrictions in export-oriented markets. Manufacturers supplying multiple regions must adapt to varying regulatory frameworks, which increases administrative costs and complicates product standardization.

The transition to low-emission or bio-based adhesives may temporarily affect product performance characteristics, requiring additional research and development investment. While regulations promote sustainability in the long term, the short-term impact includes increased capital expenditures and operational complexity, which may discourage new entrants and slow the adoption of innovation.

Technological Advancements and Recycled Content Integration

Innovations such as continuous press technology, advanced resin formulations, and precision-controlled drying and pressing systems have improved panel strength, surface quality, and dimensional stability. These developments enable manufacturers to produce high-performance MDF, particleboard, and OSB tailored for specific end-use applications, including moisture-resistant, fire-retardant, and load-bearing panels. Automation and digital monitoring systems optimize production efficiency, reduce material waste, and lower energy consumption. Advancements in surface finishing, including digital printing and lamination technologies, allow producers to offer visually appealing and customizable panels for furniture and interior design.

The integration of recycled wood content represents another major opportunity, aligning the wood-based panel industry with circular economy principles. Increasing use of post-consumer and post-industrial wood waste reduces reliance on virgin timber, lowers raw material costs, and supports sustainability goals demanded by regulators and consumers. Technological progress in sorting, cleaning, and processing recycled fibers has significantly improved the quality and consistency of recycled-content panels, making them suitable for furniture, construction, and packaging applications. Manufacturers incorporating higher recycled content can achieve environmental certifications and appeal to green building projects, expanding market reach.

Category-wise Analysis

Product Type Insights

Medium-density fiberboard (MDF) is expected to lead the wood-based panel market, accounting for approximately 40% of revenue in 2026, driven by its superior surface smoothness, uniform density, and high adaptability across furniture and interior design applications. MDF is widely preferred for cabinetry, wardrobes, wall panels, doors, and decorative components, as it supports precision cutting, edge profiling, and surface finishing, including laminates, veneers, and digital printing. Manufacturers continue to invest in advanced pressing and finishing technologies to enhance durability, moisture resistance, and aesthetic appeal, expanding MDF’s applicability across residential and commercial interiors. For example, EGGER Group offers high-quality MDF boards with decorative finishes tailored for modern furniture and interior solutions across Europe and Asia.

The Oriented Strand Board (OSB) segment is likely to be the fastest-growing in 2026, driven by rising adoption in structural construction applications. OSB is increasingly used in roofing, flooring, wall sheathing, and load-bearing components due to its strength, dimensional stability, and cost advantages over traditional plywood. Growth is particularly strong in North America and Europe, where modular housing, prefabricated buildings, and sustainable construction practices are gaining traction. OSB’s compliance with green building standards and its efficient material use further enhance its appeal. For example, Louisiana-Pacific Corporation (LP) has expanded its OSB product portfolio to support residential construction and engineered structural solutions.

Application Insights

The construction segment is projected to lead the market, capturing around 45% of the revenue share in 2026, supported by the extensive use of panels in residential, commercial, and infrastructure development. Wood-based panels such as MDF, OSB, and particleboard are widely used for flooring systems, wall partitions, roofing, formwork, and interior fittings due to their lightweight nature, ease of installation, and cost efficiency. Rapid urbanization, housing demand, and infrastructure expansion across the Asia Pacific, North America, and Europe continue to fuel consumption. Renovation and remodeling activities in mature markets are boosting demand for engineered wood panels. For instance, West Fraser Timber Co. supplies OSB and other structural panels widely used in North American residential construction.

The furniture segment is likely to be the fastest-growing application in 2026, driven by rising demand for modular, ready-to-assemble, and space-efficient furniture solutions. MDF and particleboard dominate this segment due to their machinability, affordability, and compatibility with modern furniture designs. Growth is supported by urban lifestyles, increasing disposable incomes, and the expansion of e-commerce furniture platforms, which favor lightweight and standardized panel-based products. The growing demand for interior customization and aesthetically finished furniture is also driving the rapid adoption of these materials. For instance, IKEA extensively uses MDF and particleboard in its flat-pack furniture collections to balance cost-efficiency and design versatility.

Regional Insights

North America Wood-Based Panel Market Trends

North America is likely to be the fastest-growing region in 2026, driven by strong residential construction and renovation activity, the high adoption of engineered wood products such as OSB and MDF, stringent environmental standards that encourage low-emission panels, and continued investments by major manufacturers in advanced, sustainable production technologies. Demand for structural panels such as Oriented Strand Board (OSB) and plywood remains strong, driven by new housing starts and remodeling activity across the U.S. and Canada. Sustainability has become a central theme, with builders and developers increasingly specifying low-emission and eco-certified panels to comply with stringent environmental standards and green building programs.

The North American wood-based panel market is being shaped by strategic capacity expansions and increased technological investments by leading industry players. Companies are streamlining supply chains and modernizing manufacturing facilities to enhance operational efficiency, lower emissions, and improve product performance. For instance, Georgia-Pacific LLC has invested substantially in its OSB and engineered wood panel operations to address rising demand from the construction sector while supporting sustainability objectives.

These initiatives include adopting advanced pressing technologies and optimizing resin formulations to minimize environmental impact. The growth of e-commerce and direct-to-consumer furniture sales is driving higher demand for medium-density fiberboard (MDF) and particleboard, particularly for use in modular and panelized furniture components.

Europe Wood-Based Panel Market Trends

Europe is likely to be a significant market in 2026, due to strict environmental regulations and strong adoption of sustainable and low-emission panels. European regulations, such as stringent formaldehyde emission limits and strong forest certification requirements, have pushed manufacturers to adopt low-emission resins and responsibly sourced raw materials. This focus aligns with broader environmental goals under the EU Green Deal and circular-economy initiatives, which prioritize recyclable and bio-based materials in construction and furniture applications. Consumer preferences in Europe are increasingly shifting toward eco-friendly and premium aesthetic panels, driving demand for decorative MDF, HDF, and specialty boards designed for interior applications.

The strategic positioning of major producers to enhance competitiveness and meet evolving customer needs. Companies are leveraging advanced automation, energy-efficient processes, and agile supply chains to maintain quality and cost advantages. For example, EGGER Group has expanded its range of sustainable panel offerings, including recycled-content MDF and decorative surfaces tailored for high-end furniture and interior design segments, reinforcing its presence across key European markets. Cross-border trade within Europe supports availability and price stability, while Eastern Europe is emerging as a growth region driven by expanding construction activity and improved manufacturing infrastructure.

Asia Pacific Wood-Based Panel Market Trends

The Asia Pacific region is anticipated to be the leading region, accounting for 55% of the market share in 2026, driven by robust urbanization, infrastructure development, and rising residential construction across key economies such as China, India, Japan, and ASEAN nations. Rapid economic growth and rising disposable incomes are fueling strong demand for housing and commercial real estate, which, in turn, is driving consumption of engineered wood products, including MDF, particleboard, plywood, and OSB.

Urban population growth intensifies demand for affordable yet aesthetically pleasing interiors, increasing the use of decorative panels in furniture, cabinetry, and retail spaces. The adoption of prefabricated and modular building systems is gaining traction, as these methods offer cost efficiencies and faster completion timelines for large-scale projects.

Industry players in the Asia Pacific region are actively expanding production capacity and investing in technological advancements to maintain competitiveness and cater to diverse market requirements. For example, Arauco has strengthened its footprint by establishing integrated manufacturing facilities that optimize supply chains and support the production of high quality MDF and particleboard tailored for both domestic and export markets. These facilities leverage modern continuous-press technologies and resin systems to improve panel performance while reducing environmental impact. Demand from furniture manufacturers and real estate developers continues to grow in India and Southeast Asia, where wood-based panels are increasingly chosen for their versatility, cost-effectiveness, and ease of installation.

Competitive Landscape

The global wood-based panel market exhibits a moderately fragmented structure, driven by a mix of large multinational corporations and strong regional players that collectively shape competitive dynamics through production scale, geographic reach, and product diversity.

Established companies benefit from extensive manufacturing assets, integrated supply chains, and broad product portfolios spanning MDF, HDF, OSB, particleboard, and softboard to serve diverse end-use segments such as construction, furniture, and packaging. The landscape features both global leaders and regional specialists competing for share, with ongoing capacity expansions, technology upgrades, and sustainability initiatives influencing strategic priorities across the industry.

With key leaders including Kronospan, Arauco, West Fraser Timber Co. Ltd., and EGGER Group, the competitive field is defined by efforts to enhance efficiency, product quality, and environmental performance across the value chain. These players compete through strategic investments in advanced manufacturing technologies, expanded distribution networks, and sustainability credentials that align with emerging regulatory and consumer expectations for low-emission and recycled content panels. Competitive differentiation also arises through mergers and acquisitions, partnerships, and targeted product development aimed at meeting evolving market needs while navigating raw material fluctuations and environmental compliance requirements.

Key Industry Developments:

- In October 2025, Daiken introduced its groundbreaking DIO woodcore, a laminated wood panel designed for flooring, modular housing, and recreational vehicles. Developed over seven years since 2018, the DIO woodcore delivers superior performance at a reduced cost, positioning it as a competitive domestic alternative to imported materials in both local and international markets. Backed by US$10 million in provincial funding, Daiken is set to enhance production capabilities, boost productivity, and scale operations. This strategic initiative will safeguard 128 existing jobs and generate 10 new roles. Additionally, the US$70 million investment is poised to invigorate the local forest sector by creating demand for underutilized wood, directly benefiting 28 regional businesses.

- In April 2025, as part of its strategic initiative, the BIS Quality Control Order (QCO) made BIS certification and ISI marking mandatory for all MDF, particle board, block board, plywood, shuttering plywood, and other panel-based materials. This move triggered a surge in import orders, particularly affecting plywood imports from Russia, which had been favored in the Indian market for its refined finish and compatibility with advanced furniture production machinery.

Companies Covered in Wood-Based Panel Market

- Ainsworth Lumber Co. Ltd.

- Arauco

- Boise Cascade Company

- EGGER Group

- Georgia-Pacific LLC (Koch Industries)

- Kronospan

- Louisiana-Pacific Corporation (LP)

- Norbord Inc.

- Panels & Furniture Group (PFM Group)

- Pfleiderer Group S.A.

- Roseburg Forest Products

- Swiss Krono Group

- U.S. Lumber Group LLC

- West Fraser Timber Co. Ltd.

Frequently Asked Questions

The global wood-based panel market is projected to reach US$222.0 billion in 2026.

Rising construction and urbanization, growing demand for furniture and interior applications, and increasing adoption of sustainable and cost-effective engineered wood products.

The wood-based panel market is expected to grow at a CAGR of 5.9% from 2026 to 2033.

Technological advancements in manufacturing, integration of recycled content, growing demand for sustainable and low-emission panels, expansion in modular and prefabricated construction, and increasing adoption in furniture and interior applications.

Ainsworth Lumber Co. Ltd., Arauco, Boise Cascade Company, and EGGER Group are the leading players.