- Agrochemicals

- Wood Tar Market

Wood Tar Market Size, Share, and Growth Forecast, 2026 – 2033

Wood Tar Market by Product Type (Resinous Tars, Hardwood Tars, Others), Production Technology (Destructive Distillation, Pyrolysis, Other Advanced Methods), Application (Construction Coatings, Ship Coatings, Animal Husbandry, Others), and Regional Analysis for 2026-2033

Wood Tar Market Share and Trends Analysis

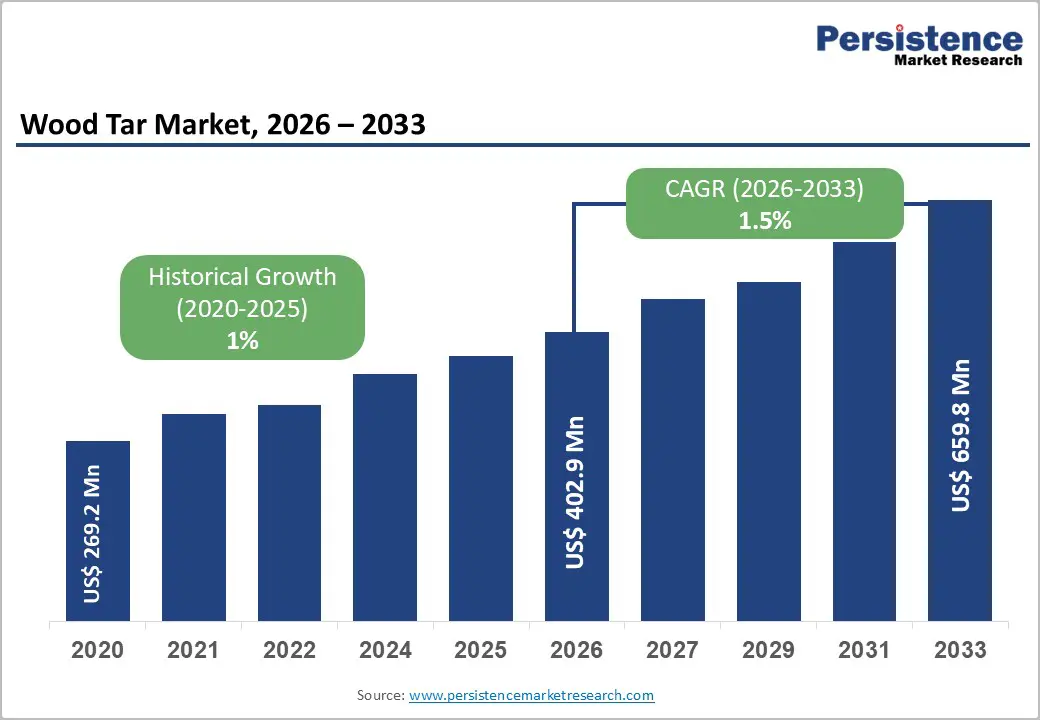

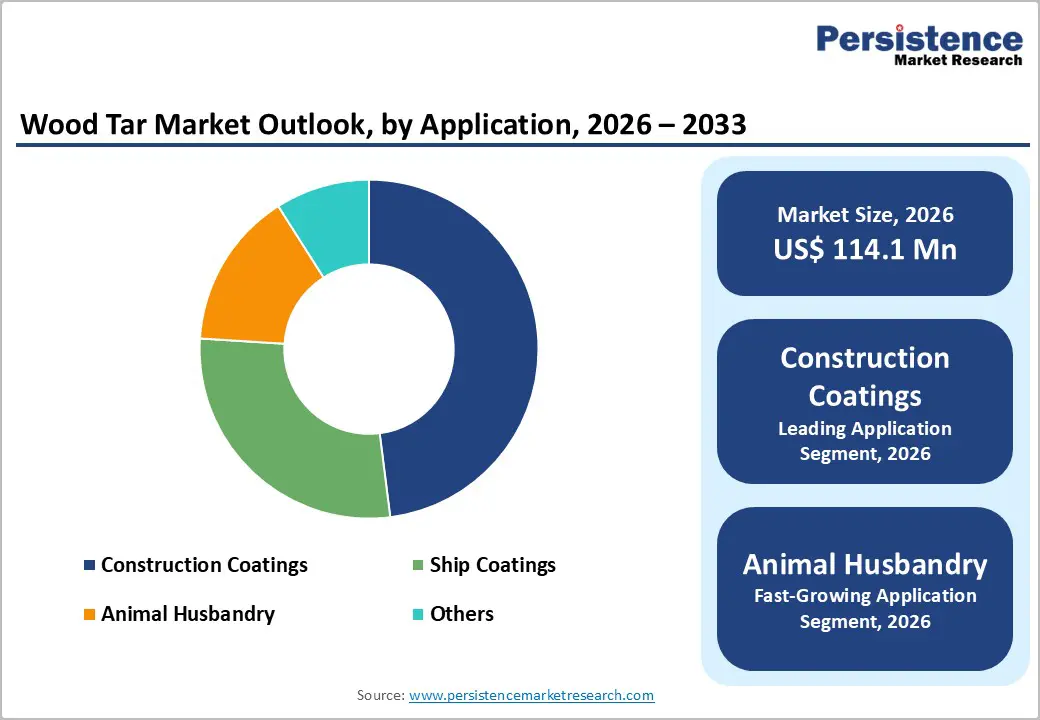

The global wood tar market size is likely to be valued at US$ 114.1 million in 2026, and is projected to reach US$ 126.6 million by 2033, growing at a CAGR of 1.5% during the forecast period 2026−2033.

Growth is primarily driven by rising awareness of industrial applications in construction and animal husbandry, increased integration into eco-friendly coatings, and broader acceptance in traditional medicine and healthcare sectors. The demographic shift toward urbanized regions with increasing demand for protective and durable coatings contributes to market expansion. Technological adoption in production processes, such as pyrolysis and advanced distillation methods, enhances extraction efficiency and product consistency, fostering provider confidence and consumer trust. Strengthened healthcare infrastructure in emerging economies supports uptake in veterinary and therapeutic applications. Regulatory recognition of natural product applications further facilitates commercialization and cross-sector utilization. Investment in scalable production facilities and supply-chain optimization allows manufacturers to expand regional presence, reinforcing market stability.

Key Industry Highlights

- Fastest-growing Application: Animal husbandry is anticipated to be the fastest-growing segment through 2033, propelled by the antiseptic and therapeutic benefits of wood tar for livestock.

- Leading Application: Construction coatings are likely to lead with about 48% in 2026, fueled by durability, water resistance, regulatory compliance and reliable procurement of wood tar.

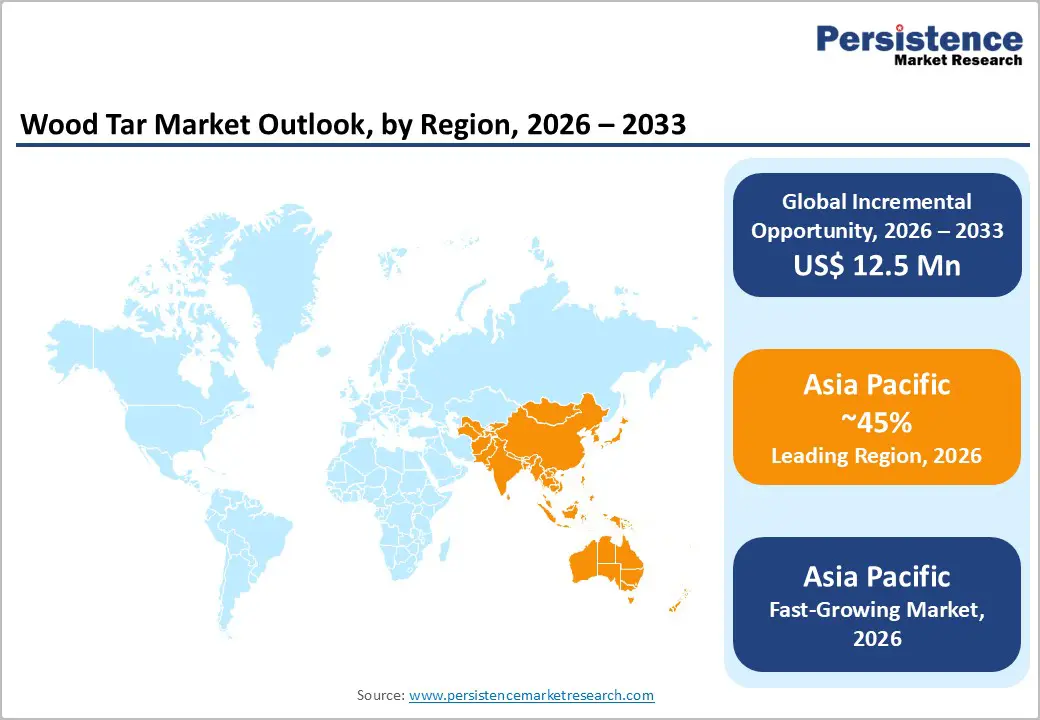

- Dominant Region: Asia Pacific is expected to dominate with 41% of the market share in 2026, driven by extensive use of wood tar in construction, maritime, and agriculture.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, supported by the expanding use of wood tar in animal husbandry and sustainable agriculture practices.

| Report Attribute | Details |

|---|---|

|

Wood Tar Market Size (2026E) |

US$ 114.1 Mn |

|

Market Value Forecast (2033F) |

US$ 126.6 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

1.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Demand for Eco-Friendly Coating

The rising demand for eco?friendly coatings drives growth as regulatory frameworks and corporate sourcing policies shift focus from traditional solvent?based finishes to sustainable alternatives that reduce environmental impact and align with broader sustainability targets. Governments and industry standards in North America, Europe, and Asia are increasingly restricting emissions of volatile organic compounds (VOCs) and other hazardous substances, prompting buyers to adopt low?emission, water?based, and bio?based coatings that support healthier indoor environments and compliance with green building criteria.

Corporate environmental, social, & governance (ESG) commitments along with growing consumer awareness are influencing purchasing decisions across industries. In construction, industrial manufacturing, and furniture sectors, buyers increasingly consider environmental impact when defining product specifications. Products that enhance indoor air quality and comply with green building certifications such as Leadership in Energy and Environmental Design (LEED) or Building Research Establishment Environmental Assessment Method (BREEAM) are gaining preference. This shift supports stronger long?term contracts and allows premium pricing for sustainable coatings, encouraging further investment in eco?friendly technologies.

Supply Chain and Raw Material Constraints

Supply chain and raw material constraints significantly impact the availability and pricing stability of wood tar. The production of wood tar relies on consistent access to specific timber types, often sourced from controlled forests or regions with seasonal harvesting cycles. Transportation bottlenecks, regulatory restrictions on logging, and geopolitical factors can disrupt the flow of raw materials, leading to fluctuating supply levels. Variations in timber quality and yield further complicate production planning, requiring manufacturers to adjust processes and incur higher operational costs to maintain consistent output standards.

The reliance on limited and geographically concentrated sources exposes the industry to external shocks, such as natural disasters, labor shortages, or policy changes, which can abruptly reduce raw material availability. As production is highly dependent on these inputs, any disruption in the upstream supply chain translates into increased lead times and elevated costs throughout the production cycle. Companies face challenges in scaling operations efficiently while maintaining product quality, resulting in competitive pressure and potential margin compression.

Product Innovation and Application Diversification

Product innovation drives wood tar market growth through the development of novel formulations and enhanced quality, enabling penetration into new industrial and consumer segments. Modern industries demand multifunctional materials that improve performance, durability, and sustainability. By introducing advanced variants with specific properties, such as high purity or targeted chemical composition, manufacturers can cater to specialized requirements in pharmaceuticals, cosmetics, and chemical processing. This strategic approach strengthens brand positioning, differentiates offerings from generic alternatives, and enhances customer loyalty. Innovation in production techniques also reduces costs, optimizes resource efficiency, and ensures compliance with emerging environmental and regulatory standards, creating long-term operational advantages.

Application diversification expands utilization across multiple sectors, mitigating dependency on traditional end uses. Emerging sectors seek natural and sustainable solutions, creating opportunities for integration into products such as adhesives, protective coatings, and bio-based materials. Companies that explore unconventional applications can access untapped revenue streams and establish partnerships with industries adopting green and renewable technologies. Diversification supports resilience against market fluctuations, as demand shifts across sectors with varying economic cycles.

Category-wise Analysis

Product Type Insights

Resinous tars are anticipated to secure around 42% of the wood tar market share in 2026, reflecting established demand in industrial coatings and ship protection. The segment benefits from proven durability, water resistance, and chemical stability, supporting adoption in high-volume applications such as maritime coatings and protective construction layers. Industrial users favor resinous tars for consistent performance under regulatory compliance and environmental standards. Accessibility and integration with existing coating systems reinforce supplier and consumer confidence. Their high reliability encourages widespread use, particularly among enterprises focused on preventive maintenance and product longevity. Innovation in formulation, including hybrid resinous blends, sustains demand and strengthens market share.

Hardwood tars are expected to be the fastest-growing segment during the 2026–2033 forecast period, propelled by rising interest in natural and traditional applications. They offer distinct bioactive properties valued in animal husbandry, veterinary therapeutics, and specialty ointments. Provider preference for natural ingredients, combined with cultural acceptance in emerging markets, drives adoption. Expansion of digital commerce enables broader retail penetration, making hardwood tar accessible to small-scale agricultural operators. Formulation innovations, including odor reduction and viscosity control, further enhance usability.

Production Technology Insights

Destructive distillation extracts are poised to dominate with a forecasted revenue share of over 55% in 2026, powered by widespread industrial familiarity and cost-efficient processing. Controlled high-temperature pyrolysis within sealed environments ensures consistent yield and product quality. Industrial operators favor this technology due to reliability, regulatory acceptance, and alignment with environmental emission standards. Consumer trust in established production methods supports adoption across construction, maritime, and agricultural applications. Operational scalability allows manufacturers to meet demand efficiently, while automated process controls minimize contamination risks and enhance overall safety.

Pyrolysis is estimated to be the fastest-growing segment from 2026 to 2033, fueled by increasing interest in advanced and energy-efficient production methods. This method enables precise control over chemical composition, supporting specialty applications in veterinary and healthcare industries. Emerging markets are adopting pyrolysis for modular plant deployment, facilitating regional manufacturing without extensive infrastructure. Regulatory agencies recognize pyrolysis as environmentally compatible due to lower emission profiles, driving expansion. Digital monitoring systems and quality assurance protocols strengthen consumer confidence and encourage broader adoption, creating a growth trajectory above traditional methods

Application Insights

Construction coatings are likely to be the dominant application segment, with a projected 48% of the wood tar market revenue share in 2026 due to durability, water resistance, and regulatory compliance. Industrial operators prefer wood tar-based coatings for roofing, wood preservation, and concrete protection. Provider recommendations and historical performance reinforce adoption. The segment benefits from stable industrial procurement channels and proven long-term efficacy, supporting steady demand. Integration with eco-friendly building initiatives enhances strategic appeal and aligns with sustainability objectives.

Animal husbandry is anticipated to be the fastest-growing application segment from 2026 to 2033, driven by increasing recognition of wood tar's antiseptic and therapeutic properties in livestock care. Veterinary practitioners and farm operators increasingly adopt wood tar for hoof treatment, wound care, and hygiene maintenance. Accessibility through specialized distributors and online channels supports small- and medium-scale adoption. Technological improvements in formulation, including reduced odor and improved consistency, further facilitate uptake. Growing emphasis on preventive animal health and sustainable agriculture practices underpins rapid segment growth.

Regional Insights

North America Wood Tar Market Trends

The North America market is predicted to exhibit steady growth driven by stable demand from well-established industrial and commercial applications rather than rapid diversification. Construction coatings, marine protection, and wood preservation continue to represent core consumption areas, supported by ongoing infrastructure maintenance, renovation activities, and long asset life-cycle management practices. Industrial operators prioritize performance consistency, regulatory compliance, and durability, leading to continued reliance on materials with proven operational histories. Mature manufacturing capabilities and standardized production processes ensure uniform quality and predictable supply, reinforcing long-term procurement agreements.

Market growth here is reinforced by gradual expansion into niche and specialty uses, including selective agricultural treatments and customized industrial coatings, where natural and durable materials fit sustainability-oriented procurement strategies. Technological improvements in processing efficiency, emission control, and quality monitoring enhance cost control and operational reliability without altering demand fundamentals. Well-established distribution networks and consolidated supplier bases reduce supply volatility and support consistent market access. Investment patterns favor incremental capacity optimization rather than large-scale expansion, reflecting disciplined capital allocation.

Europe Wood Tar Market Trends

Europe holds a significant position in the market for wood tar supported by strong alignment between industrial demand and sustainability-focused regulatory frameworks. Construction restoration, heritage preservation, and maritime maintenance represent core application areas, where long-term durability, moisture resistance, and material authenticity influence procurement decisions. Industrial buyers prioritize consistent quality, traceable sourcing, and compliance with stringent environmental standards, reinforcing reliance on established production practices. Renovation-led construction activity sustains demand, as refurbishment projects favor materials with proven performance in legacy structures.

The market in Europe also benefits from advanced processing technologies, mature quality certification systems, and integrated cross-border supply networks that enable efficient distribution across diverse end-use sectors. Continuous formulation refinement improves performance characteristics while aligning with emission controls and environmental compliance requirements. Technical expertise accumulated through long-standing industrial use supports conservative but consistent adoption patterns, particularly among professional contractors and public-sector entities. Investment activity focuses on process optimization, emission reduction, and quality assurance rather than aggressive capacity expansion, reinforcing market stability. Structured procurement policies and standardized specifications enhance supplier credibility and long-term contracts.

Asia Pacific Wood Tar Market Trends

By 2026, Asia Pacific is expected to lead with an estimated 41% of the wood tar market share, supported by strong industrial utilization across construction coatings, maritime protection, and agricultural preservation applications. Large-scale infrastructure development sustains steady demand for durable and water-resistant coating solutions, while long-standing use in ship protection reinforces volume consumption. Cost-efficient production structures, supported by proximity to forestry resources and established processing capabilities, enhance supply stability and pricing competitiveness. Industrial operators rely on consistent quality and compatibility with existing coating systems, strengthening repeat procurement. Regulatory alignment with sustainability and environmentally acceptable materials further improves adoption among commercial buyers.

Asia Pacific is forecasted to be the fastest-growing market for wood tar between 2026 and 2033, stimulated by expanding use in animal husbandry, veterinary therapeutics, and other bioactive applications. Rising focus on preventive livestock health and sustainable agricultural practices accelerates adoption among farm operators and veterinary practitioners. Growth of digital commerce platforms improves accessibility for small- and medium-scale users, enabling penetration beyond traditional industrial buyers. Product innovation focused on odor reduction, controlled viscosity, and improved handling characteristics enhances suitability for diversified applications. Modular and flexible production setups allow rapid capacity expansion and localized manufacturing, supporting responsiveness to regional demand.

Competitive Landscape

The global wood tar market exhibits a moderately fragmented structure, with leading participants accounting for an estimated 45% of total demand. Key players such as Auson, Xinzhongxing Biomass, Kemet Skandian Group, Verdi Life, and Fusheng Carbon operate alongside several regional manufacturers, creating a balanced competitive environment. Market presence is shaped by a combination of established suppliers and specialized producers that focus on production efficiency, controlled processing, and application-specific solutions. Competitive positioning emphasizes consistency of quality, regulatory compliance, and alignment with sustainability requirements across industrial and agricultural applications.

These key players are strengthening their positioning through targeted strategies centered on formulation refinement, process optimization, and sustainability-aligned production rather than aggressive consolidation. Innovation efforts concentrate on niche development, particularly in high-value veterinary formulations and industrial coating applications, where performance reliability and environmental acceptance influence purchasing decisions. Regional manufacturing proximity and customized product offerings enable responsiveness to localized demand patterns and regulatory frameworks. Investment priorities include quality assurance, emission management, and operational reliability to enhance differentiation in a competitive landscape.

Key Industry Developments

- In January 2026, OzoneBio, a Calgary-based green chemistry startup, began working to convert wood waste and nutshells into wood tar. This is then further processed to produce bio-adipic acid, a key ingredient for plastics such as nylon and polyurethane, through a first-of-its-kind process that cuts up to 97% of emissions versus petroleum methods.?

- In September 2025, scientists from Shenyang Agricultural University proposed converting bio-tar, extracted from wood, crop residue, and other organic waste, into high-value bio-carbon through controlled polymerization of its oxygen-rich compounds.? This advanced material outperforms standard biochar for applications such as water purification, supercapacitor electrodes, sustainable catalysts, and low-emission fuels.

Companies Covered in Wood Tar Market

- Auson

- Xinzhongxing Biomass

- Kemet Skandian Group

- Verdi Life

- Fusheng Carbon

- Albert Kerbl

- S.P.S. BV

- Shuanghui Active Carbon

- Bashles

- Lacq

- Eco Oil

Frequently Asked Questions

The global wood tar market is projected to reach US$ 114.1 million in 2026.

Increasing demand for eco-friendly protective coatings, sustained use in construction and maritime applications, and expanding adoption of bio-based materials in animal husbandry supported by regulatory acceptance are driving the market.

The market is poised to witness a CAGR of 1.5% from 2026 to 2033.

Key market opportunities arise from the development of advanced and hybrid wood tar formulations, and widening application scope across sustainable construction, maritime coatings, and animal husbandry.

Some of the key market players include Auson, Xinzhongxing Biomass, Kemet Skandian Group, Verdi Life, Fusheng Carbon, and Albert Kerbl.