- Smart Packaging

- Unbleached Softwood Kraft Pulp Market

Unbleached Softwood Kraft Pulp Market Size, Share, and Growth Forecast, 2026 - 2033

Unbleached Softwood Kraft Pulp Market by Product Type (Northern Unbleached Softwood Kraft, Southern Unbleached Softwood Kraft, Others), Application, End-use Industry, and Regional Analysis for 2026 - 2033

Unbleached Softwood Kraft Pulp Market Size and Trends Analysis

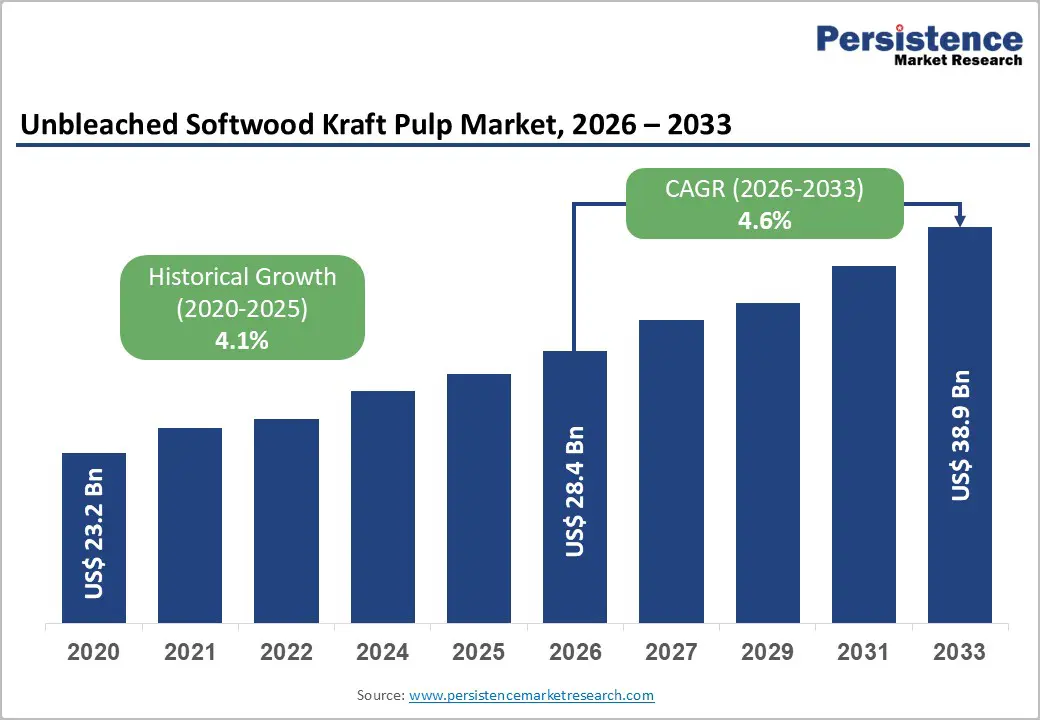

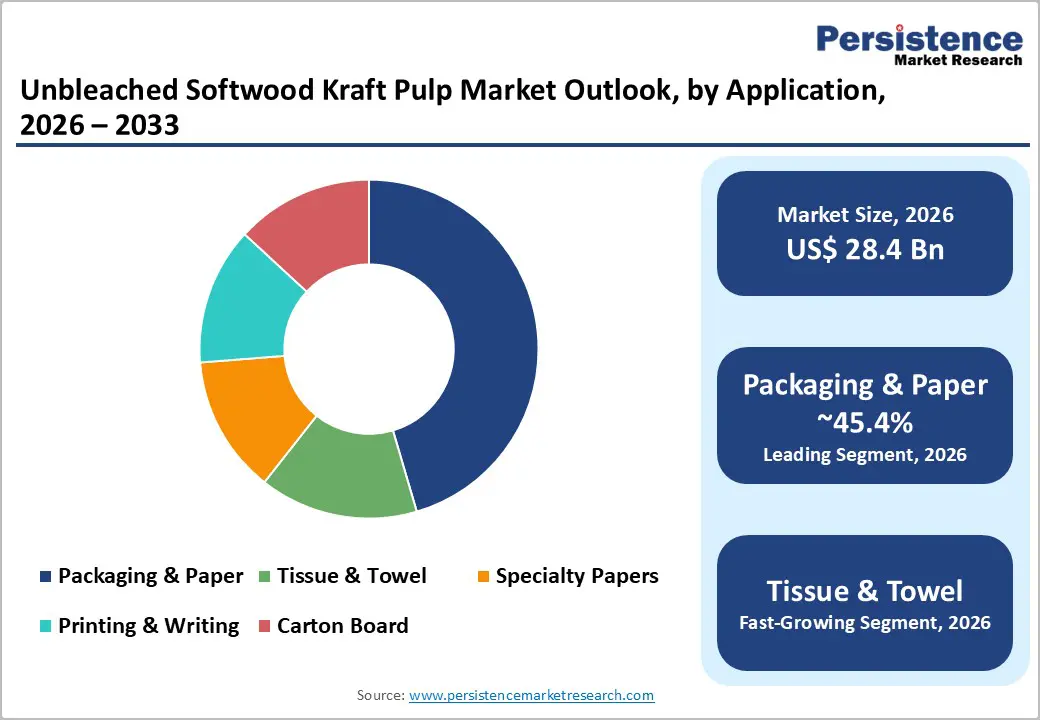

The global unbleached softwood kraft pulp market size is likely to be valued at US$28.4 billion in 2026 and is expected to reach US$38.9 billion by 2033, growing at a CAGR of 4.6% during the forecast period from 2026 to 2033, driven by the rising demand for fiber-based packaging, sustained growth in tissue and hygiene end-uses, and capacity rationalization among major pulp producers, which continues to support market pulp pricing.

Rising e-commerce packaging demand and stricter packaging regulations in developed markets are driving a shift toward higher-strength softwood pulp grades. On the supply side, capacity realignments, constrained log availability, and tightening environmental compliance are intensifying price volatility and shaping long-term investment decisions across the pulp and paper value chain.

Key Industry Highlights

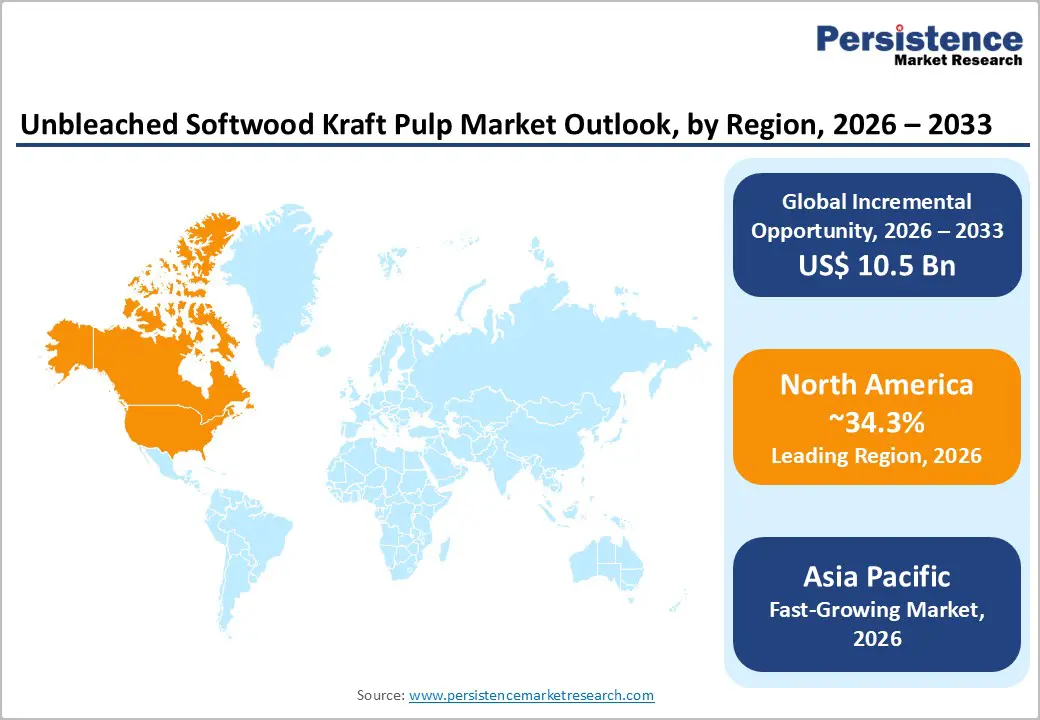

- Leading Region: North America is projected to account for approximately 34.3% of global market value in 2026, supported by extensive softwood fiber availability, integrated pulp and packaging infrastructure, and long-term supply contracts with major packaging and tissue producers.

- Fastest-growing Region: Asia Pacific, projected to grow at the highest regional CAGR through 2033, driven by expanding packaging demand, rising tissue consumption, and increasing reliance on imported long-fiber pulp across China, India, and Southeast Asia.

- Investment Plans: Ongoing investments are focused on mill modernization, energy-efficiency upgrades, and capacity optimization, particularly in North America and Europe, while export-oriented producers are increasing logistics, port infrastructure, and regional distribution investments to serve Asia Pacific demand.

- Dominant Product Type: Northern Unbleached Softwood Kraft (NBSK) is anticipated to hold approximately 57.3% of revenue share in 2026, owing to its superior strength properties and widespread use in packaging and premium paper applications.

- Leading Application: Packaging and paper applications are estimated to represent around 45.4% of the revenue share in 2026, driven by sustained growth in corrugated packaging, e-commerce logistics, and fiber-based packaging substitution initiatives.

| Key Insights | Details |

|---|---|

| Unbleached Softwood Kraft Pulp Market Size (2026E) | US$28.4 Bn |

| Market Value Forecast (2033F) | US$38.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Surge in Packaging Demand from E-Commerce and Sustainable Packaging

Packaging demand represents the single largest growth driver for unbleached softwood kraft pulp, primarily due to the material’s superior tensile strength, stiffness, and recyclability. Expansion of e-commerce has increased demand for corrugated containerboard and high-performance protective packaging. Packaging applications account for roughly one-third to two-fifths of global pulp and paper consumption, with a heavy reliance on softwood-rich linerboard to meet performance requirements. Regulatory and corporate sustainability initiatives are accelerating the replacement of plastic packaging with paper-based alternatives in transit and single-use applications. This structural shift is creating a multi-year volume tailwind for unbleached softwood kraft pulp, particularly in strength-critical packaging grades.

Hygiene and Tissue Consumption Growth

Urbanization, rising disposable incomes, and improved hygiene awareness across Asia, Latin America, and parts of Africa are driving steady growth in tissue, towel, and specialty hygiene products. These products require long-fiber pulp components to provide strength, bulk, and durability, leading manufacturers to blend unbleached softwood kraft with hardwood or fluff pulp. Capacity expansions and long-term supply partnerships announced in recent years indicate confidence in sustained tissue demand growth. As tissue consumption tends to be less cyclical than printing and writing paper, this segment provides a stabilizing influence on pulp demand, supporting higher capacity utilization and pricing resilience for unbleached softwood kraft producers.

Environmental Regulations and Circularity Preferences

Regulatory pressure, particularly in Europe and North America, is encouraging recyclable, mono-material packaging solutions while restricting certain plastics and chemical additives in food contact applications. New packaging regulations emphasize recyclability, waste reduction, and circular material use, incentivizing higher fiber content in packaging designs. Unbleached softwood kraft pulp is widely used in strength layers of recyclable packaging formats, positioning it favorably under these frameworks. While compliance increases capital and operating costs for pulp mills, the net market impact remains positive, as regulatory alignment continues to redirect demand toward fiber-based materials and strengthens long-term demand visibility for unbleached softwood pulp.

Barrier Analysis - Raw Material Supply Constraints and Cost Volatility

Softwood pulp production depends on geographically concentrated fiber resources, including boreal forests in North America and Scandinavia and plantation softwoods in select regions. Seasonal harvesting limitations, wildfire risks, and log export controls periodically tighten fiber availability and raise input costs. Since 2022, freight and energy price volatility has further increased delivered pulp costs, compressing margins for producers unable to fully pass costs downstream. Where fiber supply becomes constrained, mills may curtail operating rates, reducing spot availability and contributing to short-term price volatility across global markets.

Capital Intensity and Environmental Compliance Costs

Although unbleached pulp avoids some bleaching-related expenses, mills still require significant investment in wastewater treatment, emissions control, and chemical management systems. Stricter environmental reviews and monitoring requirements increase compliance costs and raise breakeven thresholds for new projects. Retrofitting legacy mills or constructing compliant greenfield facilities involves long permitting timelines and high capital outlays, which can delay capacity additions. These structural barriers limit the pace of low-cost supply expansion and elevate project risk, particularly for new or smaller market entrants.

Opportunity Analysis - Premium, Value-Added Specialty Unbleached Grades

Producers have opportunities to improve margins through specialty unbleached grades designed for high-performance packaging, reinforced corrugating medium, and industrial applications. These grades offer enhanced strength, surface properties, or functional performance and command price premiums relative to commodity pulp. Although specialty volumes are smaller, they deliver higher value and foster long-term supply relationships with converters. Over the next five years, differentiated specialty grades could represent an incremental 3-6% revenue opportunity for producers that invest in process optimization, technical service capabilities, and collaborative product development.

Emerging Markets and Regional Conversions

Asia Pacific, particularly India and Southeast Asia, continues to exhibit rapid growth in paper and packaging demand driven by industrialization and rising per-capita consumption. Local converters increasingly import long-fibre pulp to blend with hardwood fibres to meet strength requirements. Strategic investments in regional capacity, logistics infrastructure, or long-term supply agreements can capture this incremental demand. Over the medium term, targeted expansion in high-growth markets could support a 6-10% uplift in export volumes for globally active pulp producers.

Category-wise Analysis

Product Type Insights

Northern Unbleached Softwood Kraft (NBSK) is anticipated to represent the dominant product category, accounting for approximately 57.3% of the revenue share. The segment’s leadership is underpinned by its superior fiber morphology, which delivers high tensile strength, tear resistance, and bonding performance, critical properties for linerboard, multi-ply packaging, and reinforced paper grades. NBSK is widely used as the strength-enhancing component in blends with hardwood pulp, particularly in packaging and premium tissue applications.

Large-scale, capital-intensive production facilities in Canada and Scandinavia form the backbone of global NBSK supply, benefiting from sustainably managed boreal forests and established export logistics. These regions supply major packaging and tissue manufacturers across North America, Europe, and Asia. The geographic concentration of NBSK capacity makes the market sensitive to operational disruptions such as mill maintenance shutdowns, fiber shortages, or regulatory constraints. As a result, changes in NBSK availability often translate quickly into global price movements and influence annual and multi-year contract negotiations between pulp producers and paper manufacturers.

Southern Unbleached Softwood Kraft (SBSK) and plantation-based softwood pulp are likely to represent the fastest-growing product segment, supported by lower delivered wood costs, faster tree growth cycles, and proximity to expanding end-use markets. Mills utilizing plantation pine benefit from a predictable fiber supply, shorter rotation periods, and competitive operating cost structures compared with traditional northern producers.

These advantages have encouraged capacity expansion in regions with plantation forestry models, improving global supply diversity. SBSK is increasingly adopted in packaging, tissue, and specialty paper blends, particularly where cost optimization is a priority without materially compromising strength performance. Capacity additions in plantation-based regions have outpaced those in mature northern markets, enhancing supply flexibility and moderating long-term price volatility. This shift is intensifying competition and narrowing cost differentials between producers, prompting northern suppliers to prioritize process efficiency, product differentiation, and higher-value specialty grades to protect margins and maintain market relevance.

Application Insights

Packaging and paper applications are estimated to lead, accounting for the largest revenue share of approximately 45.4% in 2026. Long fibers derived from softwood pulp are essential for producing linerboard and corrugated medium used in shipping cartons, protective packaging, and industrial packaging solutions. These fibers provide the compression strength, durability, and stacking performance required for modern logistics and distribution systems.

Growth in e-commerce, omnichannel retail, and sustainability-driven packaging redesign continues to increase containerboard production globally. Brand owners and converters are also redesigning packaging to reduce plastic content and improve recyclability, which often increases reliance on long-fiber pulp for strength reinforcement. In response, long-term supply agreements between pulp producers and packaging converters have become more prevalent, improving supply security and enabling better planning across the value chain. This application segment remains a core demand anchor for unbleached softwood kraft pulp producers.

Tissue and towel applications are likely to be the fastest-growing end-use segment for selected unbleached softwood pulp blends. Demand growth is driven by population expansion, urbanization, rising hygiene standards, and increased per-capita consumption of tissue products across both developed and emerging economies. Softwood pulp is used in tissue formulations to enhance tensile strength, bulk, and runnability, particularly in premium and multi-ply products.

Tissue manufacturers increasingly rely on market pulp rather than an integrated fiber supply to ensure consistent quality and operational flexibility. Compared with printing and writing paper, tissue demand exhibits lower cyclicality and stronger resilience during economic downturns, making it an attractive and stable outlet for pulp producers. Ongoing investments in tissue capacity, particularly in Asia Pacific and Latin America, are expected to sustain incremental demand for long-fiber pulp over the medium to long term.

Regional Insights

North America Unbleached Softwood Kraft Pulp Market Trends - Integrated Packaging Demand and Certified Supply Strength

North America is projected to account for approximately 34.3% of the global unbleached softwood kraft pulp market share in 2026, supported by abundant softwood fiber availability, highly integrated pulp and paper infrastructure, and long-established trade linkages. The U.S. dominates regional consumption, driven by a large packaging, containerboard, and converting base, while Canada remains a critical exporter of long-fiber pulp to Asia and Europe.

Major North American producers operate vertically integrated systems that link pulp production with downstream packaging and paper manufacturing, providing resilience against demand fluctuations. The U.S. packaging sector continues to anchor demand, particularly through corrugated packaging used in e-commerce, food distribution, and industrial logistics. Large packaging companies such as International Paper, WestRock, and Packaging Corporation of America rely heavily on long-fiber pulp for linerboard strength and durability.

Strategic capacity optimization initiatives undertaken by these firms in recent years, including mill conversions away from declining printing paper toward packaging grades, have reinforced steady pulp offtake. In parallel, Canadian producers such as Canfor Pulp and Resolute Forest Products play a pivotal role in supplying northern bleached softwood kraft pulp to export markets, benefiting from well-developed port infrastructure and long-term supply contracts. Regulatory frameworks across the U.S. and Canada impose stringent environmental compliance requirements related to emissions, wastewater discharge, and sustainable forestry management.

While these standards increase capital and operating costs, they also strengthen the region’s reputation for certified, traceable, and sustainably sourced pulp, which is increasingly valued by global buyers. Recent investment activity has focused on mill modernization, energy efficiency upgrades, and bioenergy integration, allowing producers to reduce operating costs while meeting regulatory obligations. For buyers, North America remains a preferred sourcing region due to consistent quality, supply reliability, and contract transparency, particularly for strength-critical applications.

Europe Unbleached Softwood Kraft Pulp Market Trends - Circular Economy Policy and Nordic Export Leadership

Europe functions as both a major consumption hub and a globally significant export base for unbleached softwood kraft pulp, underpinned by advanced manufacturing capabilities and strong regulatory alignment across member states. Demand is concentrated in Germany, the U.K., France, and Spain, where packaging, consumer goods, and tissue manufacturing form the backbone of pulp consumption. At the same time, Nordic countries, particularly Sweden and Finland, anchor regional production, leveraging vast managed forests and highly efficient mill operations.

European demand dynamics are strongly influenced by packaging reform policies and circular economy directives, which promote recyclable, fiber-based materials and discourage non-recyclable plastics. These regulatory shifts have accelerated the adoption of paper-based packaging in food service, retail, and consumer goods. Leading producers such as Stora Enso and UPM have responded by repositioning their pulp portfolios toward packaging and specialty paper applications, while investing in traceability systems and eco-design solutions that align with brand-owner sustainability commitments.

In tissue and hygiene products, European converters continue to rely on high-quality softwood pulp for strength layers, particularly in premium and private-label brands. Investments across the region emphasize recycled fiber integration alongside virgin softwood pulp, rather than full substitution, preserving demand for long fibers. Compliance with evolving environmental and sourcing regulations has become a competitive differentiator; producers that meet strict certification and disclosure requirements gain preferential access to long-term contracts with multinational consumer goods companies. As a result, Europe remains a stable but regulation-driven market, where innovation, sustainability performance, and supply transparency increasingly determine competitive positioning.

Asia Pacific Unbleached Softwood Kraft Pulp Market Trends-Import Dependence and Packaging-Led Demand Growth

Asia Pacific is the fastest-growing regional market for unbleached softwood kraft pulp, driven by rapid industrialization, expanding middle-class populations, and structural growth in packaging and hygiene consumption. China, India, Japan, and Southeast Asian economies are central to regional demand growth, supported by rising e-commerce activity, urbanization, and increased per-capita paper and tissue use.

Unlike North America and Europe, the region has limited domestic softwood resources, resulting in a heavy dependence on imported long-fiber pulp. China remains the largest importer of softwood kraft pulp in the region, with domestic paper and packaging manufacturers relying on imported fiber to meet strength requirements for containerboard and high-performance packaging. Large Chinese packaging and tissue producers source long-fiber pulp from North America, Europe, and Latin America to blend with locally available hardwood pulp. India represents a rapidly emerging demand center, where growth in consumer goods, food packaging, and hygiene products is driving incremental pulp imports.

Regional tissue manufacturers are expanding capacity to serve rising domestic consumption, reinforcing demand for market pulp rather than an integrated fiber supply. Export-oriented producers have increasingly prioritized Asia Pacific through long-term supply agreements, logistics investments, and regional sales offices. Plantation-based producers in the Southern Hemisphere have also strengthened their presence, benefiting from shorter shipping distances and competitive cost structures. While regulatory diversity across Asia introduces compliance complexity, the region’s growth fundamentals remain compelling. Strategic investments in port infrastructure, distribution partnerships, and customer integration are becoming critical for suppliers seeking to capture sustained long-term demand in Asia Pacific’s evolving pulp and paper ecosystem.

Competitive Landscape

The global unbleached softwood kraft market is moderately concentrated, dominated by large integrated producers with global export capabilities. Competitive advantage is derived from secure fiber supply, scale, logistics efficiency, and sustainability compliance. While new plantation-based producers increase cost competition, premium long-fiber grades remain oligopolistic.

Recent strategic activity includes downstream integration into tissue products, portfolio rationalization through asset divestments, and operational realignments to improve margin performance. Joint ventures, capacity adjustments, and technology partnerships continue to reshape global supply and demand dynamics.

Leading players prioritize vertical integration, operational efficiency, premium product development, and sustainability investments. Long-term offtake agreements and logistics optimization are key margin protection strategies, while new entrants focus on cost leadership through plantation-based feedstock.

Key Industry Developments

- In July 2025, Suzano S.A. introduced innovative fiber treatment technologies for unbleached softwood kraft pulp at its Imperatriz mill in Brazil, enhancing tensile strength by 15% for export markets in Asia-Pacific while aligning with global sustainability certifications.

- In June 2025, Stora Enso launched a high-quality unbleached kraft pulp grade, UKP Nova E, specifically engineered for demanding electrical insulation paper applications such as transformer boards, cable papers, and battery separator papers, reinforcing its expanded UKP portfolio and sustainable product offering.

Companies Covered in Unbleached Softwood Kraft Pulp Market

- Suzano S.A.

- International Paper

- Stora Enso

- UPM

- West Fraser Timber Co.

- Metsä Group

- Sappi Limited

- Oji Holdings Corporation

- Nippon Paper Industries

- Mondi Group

- CMPC Group

- Mercer International

- Asia Pulp & Paper (APP)

- Nine Dragons Paper

- Resolute Forest Products

- Canfor Corporation

- Domtar Corporation

- Arauco

Frequently Asked Questions

The global softwood kraft pulp market is estimated to be valued at US$28.4 billion in 2026.

By 2033, the softwood kraft pulp market is projected to reach US$38.9 billion, reflecting sustained demand from packaging and tissue applications.

Key trends include rising demand for fiber-based and recyclable packaging, increasing use of long-fiber pulp in e-commerce and corrugated packaging, capacity optimization and modernization among major producers, and growing import demand from Asia Pacific for strength-enhancing pulp blends.

Northern Unbleached Softwood Kraft (NBSK) is the leading product segment, accounting for approximately 57.3% of global long-fiber market pulp volumes, driven by its superior strength and performance characteristics.

The softwood kraft pulp market is expected to grow at a CAGR of 4.6% between 2026 and 2033.

Major players include Suzano S.A., International Paper, Stora Enso, UPM, and West Fraser Timber Co.