- Specialty & Fine Chemicals

- Semi-Chemical Wood Pulp Market

Semi-Chemical Wood Pulp Market Size, Share, and Growth Forecast 2026 - 2033

Semi-Chemical Wood Pulp Market By Pulping Process Type (Portable, Handheld, Benchtop), Application (Ground Water, Drinking Water, Wastewater, Aquaculture), Component (Sensors, Software), End-user (Government, Industrial, Others), and Regional Analysis for 2026 - 2033

Semi-Chemical Wood Pulp Market Size and Trends Analysis

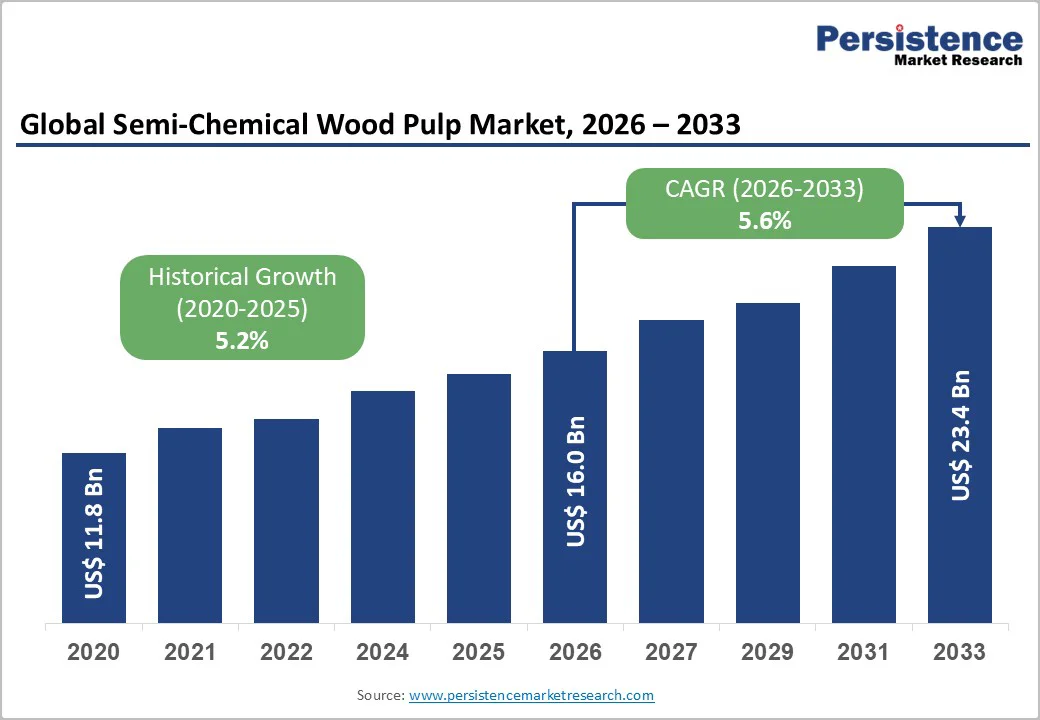

The global semi-chemical wood pulp market size is likely to be valued at US$16.0 billion in 2026. It is expected to reach US$23.4 billion by 2033, growing at a CAGR of 5.6% during the forecast period from 2026 to 2033, driven by rising demand for corrugated packaging, fueled by e-commerce growth and the global shift toward sustainable, fiber-based materials. Its high yield, cost efficiency, and suitability for producing lightweight yet strong containerboard further support market expansion, especially in emerging manufacturing regions.

Key Industry Highlights

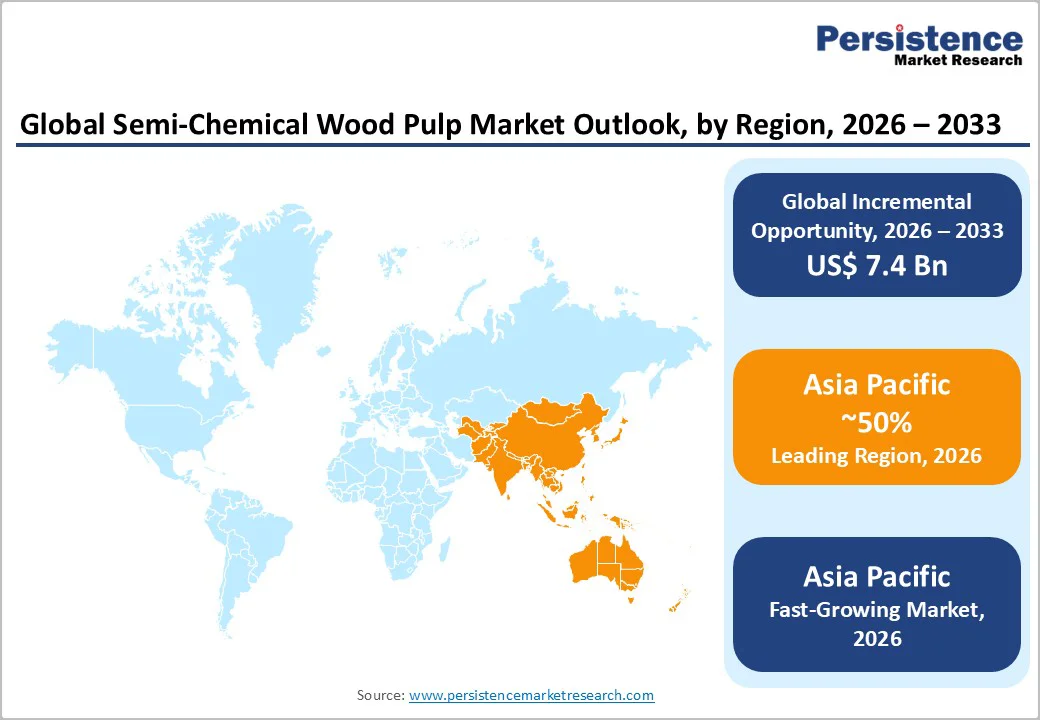

- Leading Region: Asia Pacific to lead the market with around 50% share in 2026, driven by strong manufacturing bases in China, India, and Japan, and rising ASEAN export activity.

- Fastest-growing Region: Asia Pacific is the fastest-growing, driven by rapid urbanization, expanding e-commerce, favorable policies, and growing participation from local and multinational players.

- Leading Pulping Process Type: Neutral Sulfite Semi-Chemical (NSSC) segment, anticipated to capture around 50% share in 2026, supported by its preference as a corrugating medium for high fluting strength.

- Fastest-Growing Pulping Process Type: The kraft segment is likely to be the fastest-growing, driven by rising demand for packaging and linerboard.

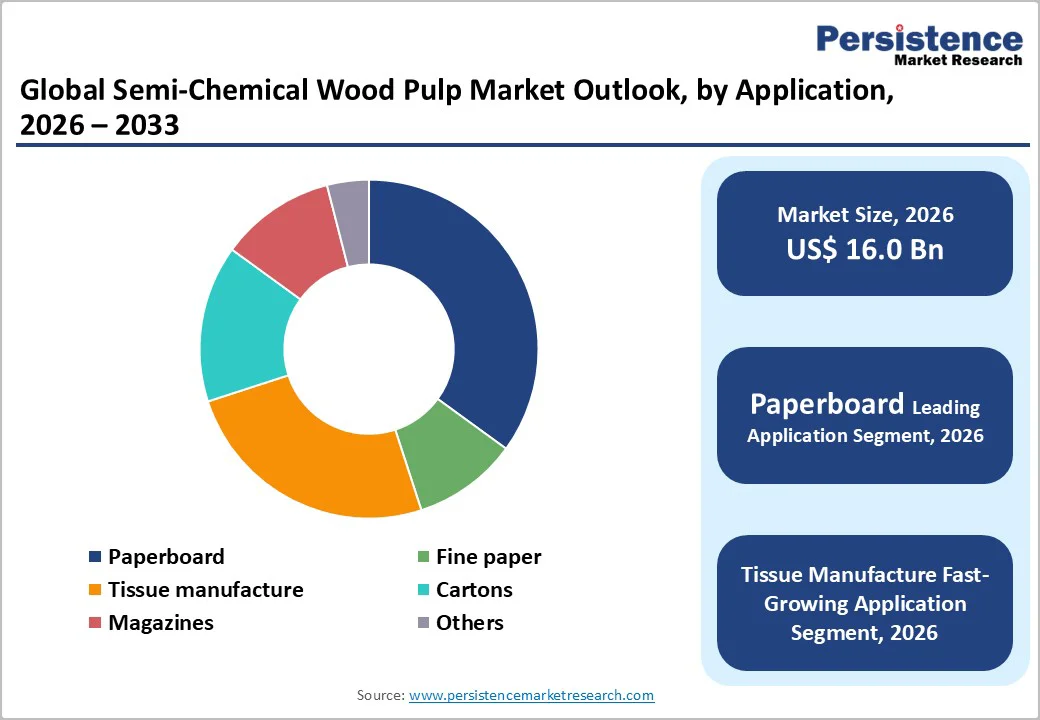

- Leading Application: The paperboard segment is expected to lead the market with over 26.8% market share in 2026, propelled by its essential role in cartons and high-stiffness packaging formats.

- Fastest-growing Application: The tissue manufacturing segment is likely to be the fastest-growing, driven by surging hygiene demand and the adoption of sustainable fibers.

- Leading End-user Type: The packaging segment is expected to lead the market, with about 70% share in 2026, driven by expanding logistics networks and demand for corrugated boxes.

| Key Insights | Details |

|---|---|

|

Semi-Chemical Wood Pulp Market Size (2026E) |

US$16.0 Bn |

|

Market Value Forecast (2033F) |

US$23.4 Bn |

|

Projected Growth CAGR (2026-2033) |

5.6% |

|

Historical Market Growth (2020-2025) |

5.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Packaging Demand

The growing global demand for packaging materials is a major driver of the semi-chemical wood pulp market, particularly as industries shift toward stronger, lightweight, and cost-efficient substrates for corrugated boxes and paperboard products. Semi-chemical pulps, especially NSSC, offer the ideal balance of strength, stiffness, and high yield, making them the preferred choice for fluting and medium used in containerboard. This demand is driven by the rapid growth of e-commerce, which needs durable packaging for long-distance and multi-stage handling.

The shift toward sustainable, fiber-based packaging solutions is accelerating the use of semi-chemical pulps, as regulators and brands push to reduce dependence on plastic. The pulp’s compatibility with recycled fibers and its suitability for lightweight packaging formats make it attractive for producers aiming to cut material costs while maintaining performance. Rapid urbanization, rising retail activity, and the growth of quick-commerce are increasing demand for fiber-based packaging, strengthening the role of semi-chemical pulp in the packaging value chain.

Supply Chain Constraints

Supply chain constraints are a significant restraint in the semi-chemical wood pulp market, disrupting the steady availability of raw materials and affecting production stability. Fluctuating timber supply, transportation bottlenecks, and rising energy and chemical costs often lead to inconsistent pulp output and higher operating expenses for mills. These challenges are intensified by regional wood shortages, forcing APAC and Europe to rely on imported chips or alternative fibers, which increases lead times and procurement risks.

Global logistics disruptions, such as port congestion, container shortages, and longer shipping cycles, create delays in delivering pulp to packaging and paper producers. Environmental regulations on harvesting and effluent treatment also slow down production expansions, further tightening supply. For downstream industries that depend on steady pulp quality for corrugated boxes, tissue, and paperboard, these constraints can cause cost volatility and limit production flexibility.

Technological and Sustainability Advancements in Transforming Semi-Chemical Pulp Production

Mills increasingly adopt cleaner, smarter, and more efficient production methods. With global pressure to reduce carbon footprints and comply with stricter environmental regulations, producers are turning to advanced technologies such as energy-efficient digesters, improved heat recovery systems, and closed-loop chemical cycles. These innovations minimize waste, cut energy consumption, and enhance overall pulp yield, making semi-chemical processes more cost-effective while maintaining the strength properties required for packaging applications.

Digitalization is reshaping pulp operations through AI-driven process control, real-time fiber quality monitoring, and automated chemical dosing. These tools increase operational precision, reduce variability, and optimize resource utilization. The combination of green production technologies and digital automation strengthens the competitiveness of semi-chemical pulp manufacturers, especially in APAC and Europe, where sustainability commitments are rapidly expanding.

Category-wise Analysis

Pulping Process Type Insights

The Neutral Sulfite Semi-Chemical (NSSC) segment is anticipated to lead the global market, capturing over 50% of the total revenue share in 2026, due to its unique balance of high yield, strength, and cost efficiency. NSSC is particularly favored for manufacturing corrugating medium because it offers excellent fluting strength, crush resistance, and dimensional stability properties essential for containerboard used in global packaging and logistics networks. For example, corrugators across APAC and North America continue adopting NSSC-based corrugating medium lines to scale production for FMCG and e-commerce packaging, leveraging NSSC’s high yield to reduce overall fiber costs. Its mildly cooked process and high yield help mills optimize fiber use while maintaining bulk and stiffness, making it ideal for large-scale packaging production across major regions.

Kraft pulping is emerging as the fastest-growing category, driven by rising global demand for linerboard and high-performance packaging materials that can withstand heavy loads, long-distance shipping, and multi-stage handling. This growth is closely linked to the acceleration of e-commerce, cross-border trade, and export-oriented manufacturing, which require stronger corrugated structures, for which Kraft pulp offers superior tensile strength and durability. E.g., the increasing investment by integrated pulp-and-paper mills to expand unbleached Kraft linerboard capacity, specifically to supply heavier, export-grade corrugated boxes for parcel logistics and long-haul freight. These trends position Kraft pulping as a crucial enabler for advanced packaging performance and global supply-chain resilience.

Application Insights

The paperboard segment is projected to lead the market, capturing over 26.8% share in 2026, driven by its essential role in producing cartons, containerboard, and folding boxboard used across e-commerce, food packaging, FMCG, and industrial logistics. Semi-chemical pulps, particularly NSSC, are widely used in paperboard manufacturing because they provide the balance of stiffness, bulk, and structural integrity needed to withstand stacking, compression, and transport stress.

The tissue manufacturing segment is likely to be the fastest-growing category, driven by rising hygiene awareness, rapid urbanization, and expanding consumer spending, particularly in APAC markets such as India, China, and Southeast Asia. The demand for tissue products, including facial tissues, toilet paper, kitchen towels, and napkins, has increased significantly as households, institutions, and commercial facilities prioritize hygiene and convenience. Semi-chemical pulp plays an important role in tissue production due to its ability to enhance bulk, softness, and absorbency while maintaining cost efficiency for high-volume manufacturers. For example, several APAC tissue mills have incorporated higher proportions of semi-chemical pulp to boost absorbency and bulk in value and mid-tier tissue products, supporting large-scale production growth across emerging markets.

End-user Insights

The packaging segment is expected to lead the market, accounting for around 70% of total revenue in 2026, driven by the global expansion of corrugated boxes, cartons, and containerboard used across e-commerce, retail, food delivery, electronics, and logistics. Semi-chemical pulps, especially NSSC, offer the fluting strength, stiffness, and durability needed to produce high-performance packaging that can withstand compression, vibration, and multi-stage handling during transportation. As global supply chains grow more complex and shipping volumes increase, demand for reliable, fiber-based packaging continues to surge across APAC, North America, and Europe.

The paper and pulp industry is experiencing rapid growth, driven by rising demand for fine paper, specialty grades, magazines, and recyclable fiber-based materials. As global sustainability efforts intensify, many manufacturers are shifting toward eco-friendly, renewable pulp sources to meet regulatory and consumer expectations. Semi-chemical pulp supports this transition by offering high yield, fiber flexibility, and compatibility with recycled streams, making it ideal for producing papers that require adequate bulk, printability, and smoothness.

Regional Insights

North America Semi-Chemical Wood Pulp Market Trends

North America has long been a mature, stable market for semi-chemical wood pulp, supported by a well-developed packaging and paper industry with robust demand for containerboard, cartons, specialty papers, and packaging materials. The region has seen renewed interest in semi-chemical pulp as brands and converters emphasize sustainability and recycled-content packaging. This shift reflects a growing preference among North American consumers and businesses for biodegradable, recyclable fiber-based packaging over plastics.

A defining trend in the region is the shift toward sustainable and eco-friendly packaging, with semi-chemical pulp playing a central role in reducing reliance on plastics. North American mills are integrating digital process controls, automated monitoring, and optimized chemical use to improve yield and reduce waste. Converters are increasingly focusing on lightweight containerboard, while maintaining stiffness and strength, to meet packaging efficiency needs.

Europe Semi-Chemical Wood Pulp Market Trends

Europe represents a robust market for semi-chemical wood pulp, due to mature demand and a strong focus on sustainable, fiber-based packaging solutions. Semi-chemical pulps, particularly NSSC, are widely used for containerboard, corrugated medium, and high-stiffness paperboard due to their fluting strength, bulk, and durability. The region’s packaging and paper industry is increasingly shifting from plastic to recyclable fiber-based materials, driven by circular economy initiatives and consumer preference for eco-friendly products.

European mills benefit from established forestry supply chains and advanced production infrastructure, enabling consistent pulp quality and reliable delivery to converters. Environmental responsibility is a key focus, leading producers to adopt energy-efficient cooking processes, closed-loop chemical recovery, and advanced effluent treatment systems, ensuring compliance with strict regional regulations while supporting sustainable operations. Mills are integrating digital process control, automated monitoring, and improved chemical management to enhance yield and reduce waste.

Asia Pacific Semi-Chemical Wood Pulp Market Trends

Asia Pacific is likely to be the leading region in the semi-chemical wood pulp market, accounting for approximately 50% in 2026, driven by high demand for packaging, paperboard, and tissue products across rapidly urbanizing countries. Semi-chemical pulps, especially NSSC, are widely adopted for containerboard and corrugated medium due to their fluting strength, bulk, and durability. The region’s robust e-commerce growth, expanding retail sectors, and rising consumer goods production significantly increase packaging consumption, directly boosting pulp demand.

Growing investments toward eco-friendly and recyclable packaging, as brands and consumers increasingly prefer sustainable fiber-based materials over plastics. Technological advancements, including automated process control, fiber optimization, and digital monitoring, are improving production efficiency and consistency. Tissue manufacturing and high-strength paperboard production are growing rapidly, driven by hygiene awareness, urbanization, and industrial packaging needs.

Competitive Landscape

The global semi-chemical wood pulp market exhibits a moderately fragmented structure, driven by a mix of large multinational corporations and regionally strong pulp producers operating alongside smaller, specialized mills. With key leaders including International Paper, JK Paper Ltd., Andritz, Arkhangelsk PPM, WestRock Company, and Stora Enso Oyj, these companies have built extensive production capacities and global distribution networks that span pulp production to downstream packaging and paperboard applications.

These players compete through a combination of strategies: adopting advanced pulping technologies, focusing on sustainability and eco-compliant production, and optimizing supply chains to ensure cost-effective raw material sourcing and consistent pulp quality. They also diversify their product portfolios, offering unbleached and high-strength grades for packaging, containerboard, and specialty paper, and often integrate vertically, extending from fiber sourcing down to packaging product supply.

Key Industry Developments:

- In May 2024, ANDRITZ launched its Metris Digital Twin Platform to improve operational control in wood pulp mills, while Valmet introduced an advanced process control system to optimize pulping yield, highlighting the industry's shift toward AI and digital technologies for efficiency and sustainability.

- In November 2025, Shandong Huatai Paper launched a new 700,000-tonne chemical pulp line, signaling continued investment in China’s pulp production infrastructure.

Companies Covered in Semi-Chemical Wood Pulp Market

- International Paper Company

- Stora Enso Oyj

- UPM-Kymmene Corporation

- Nippon Paper Industries Co., Ltd.

- Sappi Limited

- Mondi Group

- Oji Holdings Corporation

- Smurfit Kappa Group

- WestRock Company

- Domtar Corporation

- Georgia-Pacific LLC

- Nine Dragons Paper (Holdings) Limited

- Resolute Forest Products Inc.

- Canfor Corporation

- Mercer International Inc.

- Suzano S.A.

- CMPC Celulosa S.A.

- Metsa Group

- Holmen AB

Frequently Asked Questions

The semi-chemical wood pulp market is valued at US$16.0 billion in 2026 and expected to reach US$23.4 billion by 2033, reflecting robust growth.

Key drivers include rising demand for packaging, paperboard, and tissue products fueled by e-commerce growth, urbanization, and sustainability trends.

The packaging segment leads the market with about 70% share, strengthened by expanding logistics networks and demand for corrugated boxes.

Asia Pacific leads the market with around 50% share, driven by strong manufacturing bases in China, India, and Japan, and rising ASEAN export activity.

The adoption of sustainable and eco-friendly packaging solutions is supported by technological innovations and increasing demand for recyclable fiber-based materials.