- Food Ingredients & Additives

- U.S. and Europe Plant-based Tuna Market

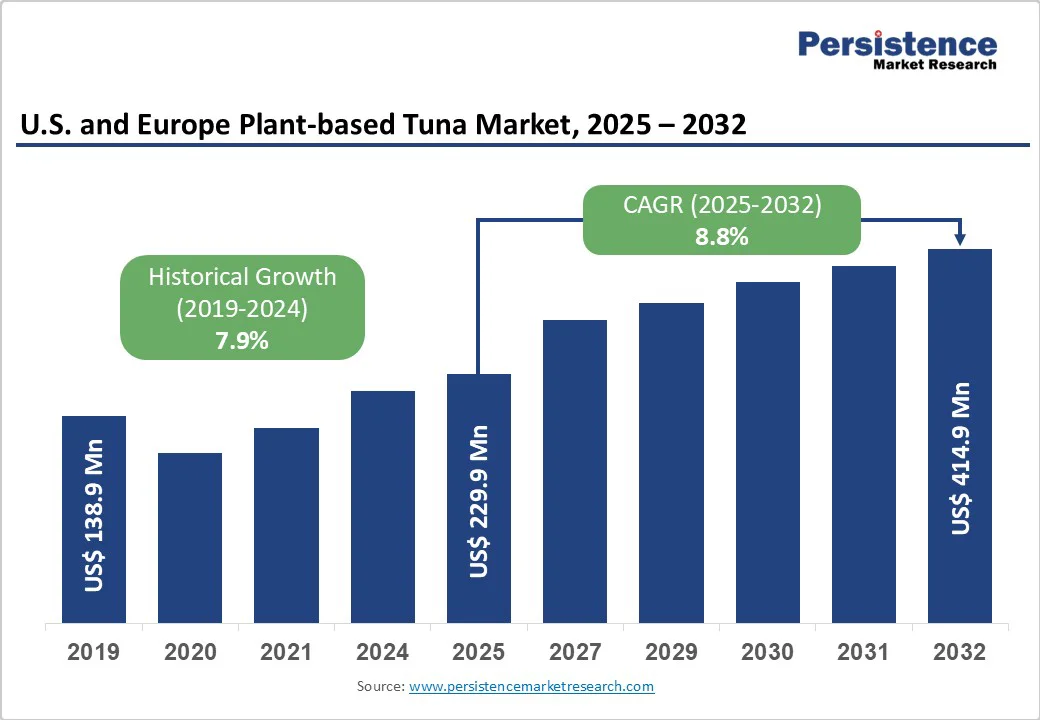

U.S. and Europe Plant-based Tuna Market Size, Share, Growth, and Regional Forecast, 2025 to 2032

U.S. and Europe Plant-based Tuna Market by Source (Soy-based, Pea-based, Wheat-based, Algae-based, Lentil-based, Chickpea-based, Others), Format (Refrigerated, Frozen), Distribution Channel {(Supermarkets/Hypermarkets, Online, Convenience Stores, Specialty Stores, Foodservice (HoReCa)}, and Country Analysis from 2025 to 2032

U.S. and Europe Plant-based Tuna Market Share and Trends Analysis

The U.S. and Europe plant-based tuna Market size is likely to be valued at US$229.9 Mn in 2025 and is projected to reach US$414.9 Mn by 2032, growing at a CAGR of 8.8% during the forecast period from 2025 to 2032.

The U.S. and European plant-based tuna market is growing rapidly, driven by health-conscious, vegan, and flexitarian consumers seeking sustainable seafood alternatives. Product innovations in texture, omega-3 fortification, and eco-friendly packaging boost appeal.

North America leads with a strong retail presence and a high volume of product launches, while Europe is expanding rapidly, supported by sustainability policies, high consumer awareness, and established plant-based seafood brands.

Key Industry Highlights:

- Leading Source Segment: Soy-based, holding approximately 41.3% share in 2025, driven by strong retail availability, cost efficiency, high protein content, and consumer familiarity. Its versatility in flaked, chunk, and spread formats, along with ease of processing and long shelf life, makes it the preferred choice for manufacturers and a trusted option for health- and sustainability-conscious consumers.

- Fastest-growing Distribution Channel Segment: Online Retail, driven by rising e-commerce adoption, direct-to-consumer subscriptions, and expanding digital grocery platforms in both North America and Europe.

- Market Scalability: Texture & Omega-3 Fortification, focusing on flaked and chunk formats, supported by consumer demand for nutrient-enriched alternatives, cross-border R&D in taste and mouthfeel, and multi-million-dollar investments by leading plant-based seafood brands.

- Leading Format: Refrigerated plant-based tuna, holding over 61.8% revenue share driven by strong brand recognition, widespread supermarket and specialty store availability, and consumer preference for fresh, ready-to-eat alternatives.

| Key Insights | Details |

|---|---|

| U.S. and Europe Plant-based Tuna Market Size (2025E) | US$ 229.9 Mn |

| Market Value Forecast (2032F) | US$414.9 Mn |

| Projected Growth (CAGR 2025 to 2032) | 8.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 7.9% |

Market Dynamics

Driver - Growing Adoption of Vegan, Vegetarian, and Flexitarian Lifestyles

The growing adoption of vegan, vegetarian, and flexitarian lifestyles in the U.S. and Europe is significantly driving the plant-based tuna market. In Germany, over 8 million individuals identify as vegetarians, and approximately 1.58 million as vegans. Additionally, more than half of the population considers themselves flexitarians, opting to reduce meat consumption.

In the U.S., approximately 5% of the population identifies as vegetarian, with a growing inclination toward plant-based diets. Flexitarianism is gaining traction, with many individuals reducing meat intake without fully eliminating it. Concerns about health, environmental awareness, and ethical considerations drive this shift in dietary preferences. As consumers increasingly seek sustainable and health-conscious alternatives, the demand for plant-based tuna continues to rise, influencing market dynamics and product offerings.

Restraints - Regulatory and Labeling Restrictions

Regulatory and labeling restrictions pose significant challenges to the plant-based tuna market in both the U.S. and Europe. In the U.S., the Food and Drug Administration (FDA) requires that plant-based products clearly identify their plant origin. For instance, a product labeled as “plant-based tuna” must specify its plant source, such as “pea protein-based tuna,” to avoid misleading consumers.

Similarly, the European Union has proposed legislation to ban the use of meat-related terms, such as “steak” and “burger,” for plant-based products, aiming to prevent consumer confusion. This move has faced criticism from environmental groups and retailers who argue that such restrictions could hinder the growth of plant-based alternatives. These regulatory measures highlight the need for clear and accurate labeling to ensure consumer trust and market expansion.

Despite advancements in food technology, many plant-based tuna products still struggle to replicate the flaky texture and umami flavor of traditional tuna. This discrepancy can lead to consumer dissatisfaction and reluctance to adopt these alternatives. As the plant-based seafood market continues to grow, addressing these sensory challenges through innovation and improved formulations will be essential for enhancing consumer acceptance and expanding market reach.

Opportunity - Advancements in Sensory Experience

Enhancing the sensory attributes such as taste, texture, and appearance of plant-based tuna presents a significant opportunity in the U.S. and European markets. Consumer acceptance studies indicate that taste is the most crucial factor influencing the purchase of alternative seafood products. In the U.S., texture closely follows taste in importance for both plant-based and cultivated seafood.

Recent innovations have led to products that closely mimic the sensory profile of traditional tuna. For instance, Solina's NEXTERA® vegan tuna has been evaluated by trained panelists and found to have similar flakiness, chewiness, and fibrous texture to conventional tuna, while being less bitter and acidic.

These advancements suggest that focusing on sensory optimization can enhance consumer acceptance and drive market growth. As the plant-based seafood sector continues to evolve, ingredient innovation plays a pivotal role in meeting consumer expectations and expanding market share.

Category-wise Analysis

By Source, Soy-based Dominates the Plant-based Tuna Market

Soy-based ingredients dominate the plant-based tuna market due to their high protein content, versatility, and cost-effectiveness. Soy provides all essential amino acids, making it a complete plant protein suitable for replicating the nutritional profile of conventional tuna.

In Europe, soy is widely cultivated and incorporated into processed plant-based foods, with organizations such as the European Soy Association reporting that millions of tons of soy are used annually in food products (europeansoy.org). In the U.S., the USDA notes that soy protein is a major ingredient in vegetarian and vegan products, widely accepted by consumers for taste and texture (usda.gov). Its long shelf life and adaptability in flaked or chunk formats further reinforce its leading position, supporting market growth driven by health- and sustainability-conscious consumers.

By Format, Refrigerated is Gaining Traction due to Freshness, Taste, Texture, and Convenience.

Refrigerated food leads with a 61.8% share in 2025, due to its superior taste, texture, and consumer familiarity. The preference for refrigerated formats aligns with the broader trend in plant-based foods, where fresh, chilled products are favored over frozen or shelf-stable options. The desire for products that closely mimic the sensory qualities of traditional seafood encourages the use of refrigeration techniques.

For instance, in the U.S., the plant-based food sector has witnessed significant growth, with refrigerated plant-based products leading in terms of sales and consumer acceptance. Similarly, in Europe, refrigerated plant-based seafood alternatives are gaining popularity, supported by the region's strong retail infrastructure and consumer demand for fresh, sustainable food options. This trend underscores the importance of the refrigerated format in meeting consumer expectations and driving market growth.

Country Insights

Germany Plant-based Tuna Market Trends

Germany is a leading market for plant-based seafood in Europe, driven by a growing consumer shift towards sustainable and health-conscious diets. Approximately 10% of Germans identify as plant-based eaters, including vegetarians and vegans, with an additional 30% adopting a flexitarian lifestyle. This shift is influencing food choices, including a preference for plant-based tuna alternatives.

Soy-based products currently lead the market due to their high protein content, versatility, and ability to mimic the texture of traditional tuna, while pea-based alternatives are emerging as a fast-growing segment. Germany’s strong retail infrastructure, eco-conscious consumers, and government initiatives promoting sustainable diets further bolster market expansion. The combination of consumer demand and policy support positions Germany as a key player.

Competitive Landscape

The U.S. and Europe Plant-based Tuna Market are expanding as companies focus on innovations in taste, texture, omega-3 fortification, and sustainable packaging. Leading brands improve product quality and nutrition, while emerging players cater to niche segments such as organic, gluten-free, and low-sodium options.

Strategic partnerships with seafood brands, collaborations with foodservice providers, and increased presence across retail and e-commerce channels strengthen competitiveness, driving broader consumer adoption and repeat purchase across both regions.

Key Industry Developments:

- In September 2025, Schouten Europe unveiled a new plant-based tuna product aimed at foodservice and ready-meal applications across Europe. The launch focused on providing a sustainable alternative to conventional tuna, catering to the increasing consumer demand for plant-based seafood options.

- In July 2024, Ahimsa Companies acquired the Good Catch production facility from Gathered Foods. This acquisition strengthens Ahimsa’s manufacturing capabilities and expands its production capacity for plant-based seafood products, enabling broader distribution and meeting growing consumer demand for sustainable, plant-based tuna alternatives.

Companies Covered in U.S. and Europe Plant-based Tuna Market

- Good Catch Foods

- Ocean Hugger Foods

- Sophie’s Kitchen

- Loma Linda (Atlantic Natural Foods)

- The Plant Based Seafood Co.

- Nestlé (Garden Gourmet / Vuna)

- Hooked Foods

- Schouten Europe B.V.

- Vgarden

- Vegan Zeastar

- Prime Roots

- Tofuna Fysh

- Unfished

- Others

Frequently Asked Questions

U.S. and Europe Plant-based Tuna Market is likely to value at US$ 229.9 Mn in 2025.

Health consciousness, vegan/flexitarian diets, sustainability concerns, taste innovations, fortified products, and expanding retail and e-commerce channels drive market growth.

U.S. and Europe Plant-based tuna market is poised to witness a CAGR of 8.8% between 2025 and 2032.

Enhancing taste and texture, fortified products, organic and low-sodium options, café collaborations, strategic partnerships, and expanding retail and e-commerce channels.

Major players in the U.S. and Europe plant-based tuna market include Good Catch Foods, Ocean Hugger Foods, Sophie’s Kitchen, Loma Linda (Atlantic Natural Foods), The Plant Based Seafood Co., Nestlé (Garden Gourmet / Vuna) and others.