- Hardware & Software IT Services

- Global Product Analytics Market

Global Product Analytics Market Size, Share, and Growth Forecast 2026 – 2033

Product Analytics Market by Solution (Product Analytics Platform and Services), Enterprise Size (SMEs and Large Enterprises), Industry (BFSI, Retail & e-Commerce, Travel & Hospitality, Food & Beverages, Healthcare, Energy & Utilities, and Others), and Regional Analysis

Product Analytics Market Size and Share Analysis

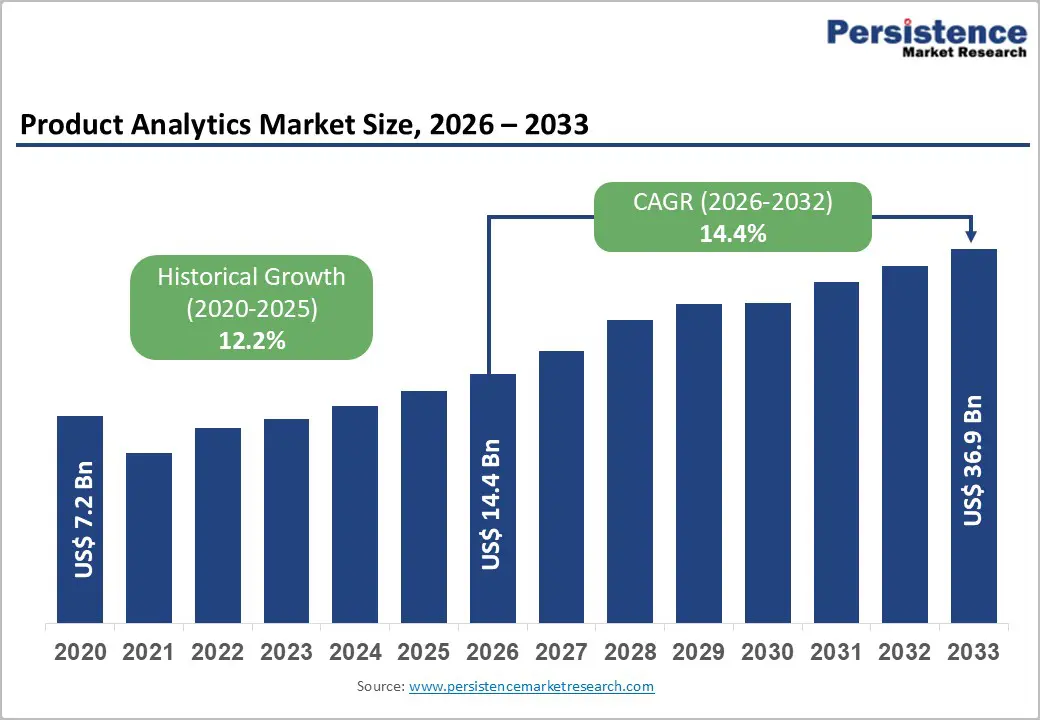

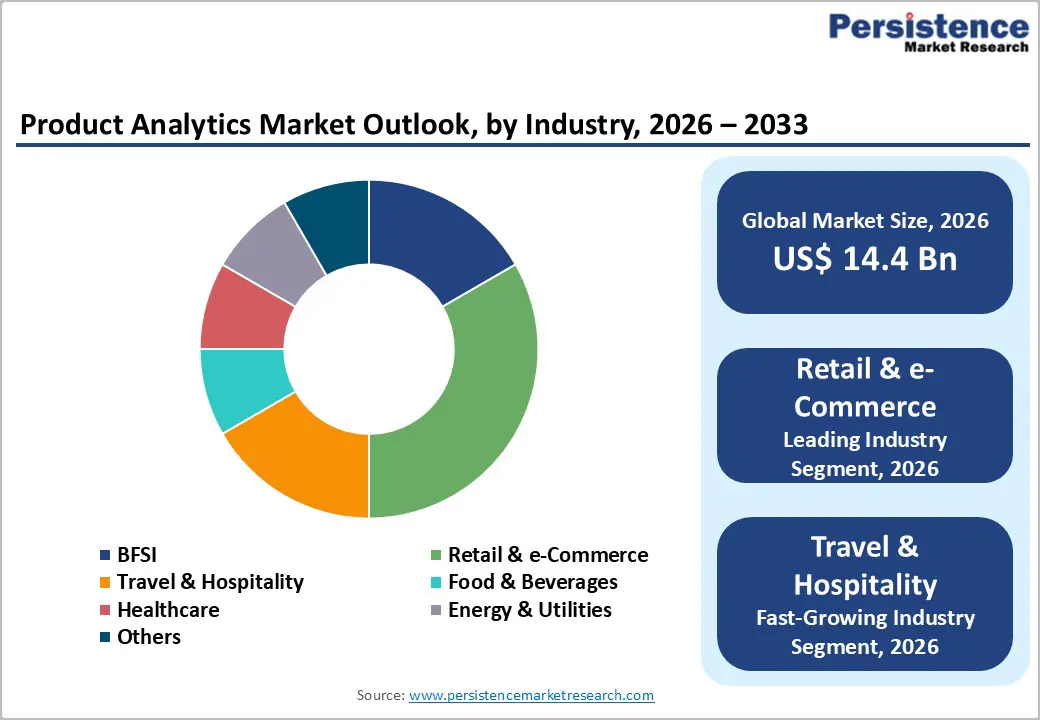

The global Product Analytics Market size was valued at US$ 14.4 Bn in 2026 and is projected to reach US$ 36.9 Bn by 2033, growing at a CAGR of 14.4% between 2026 and 2033.

Market expansion is driven by accelerating cloud analytics adoption with web-based solutions commanding 63.5% market share enabling real-time accessibility and distributed team collaboration, supported by enterprise recognition of data-driven decision-making necessity for competitive advantage and product optimization. Explosive digital transformation initiatives across BFSI, retail, healthcare, and telecommunications sectors requiring advanced analytics capabilities for customer journey optimization and conversion funnel improvement establish critical growth catalyst supporting market acceleration.

Key Market Highlights

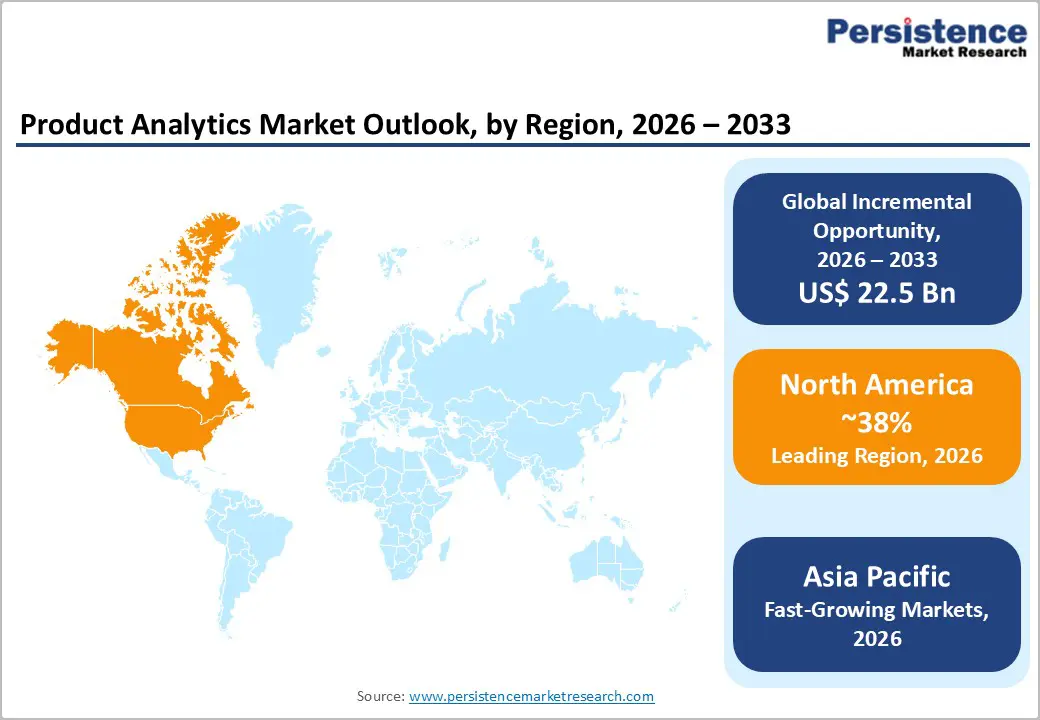

- Leading Region: North America maintains market leadership anchored by United States innovation ecosystem dominance, product-led growth strategy adoption across SaaS companies, substantial enterprise analytics budgets, regulatory clarity supporting cloud adoption, and established market consolidation around tier-one vendors.

- Fastest Growing Region: Asia-Pacific commands fastest expansion driven by China market dominance with manufacturing analytics adoption, India's exceptional 21.8% CAGR fueled by digital commerce explosion, ASEAN mobile-first markets, and government digital transformation initiatives across emerging economies.

- Dominant Industry: Cloud-based product analytics platforms command market dominance with 75% share and 63.5% web-based solution preference, driven by superior scalability, real-time accessibility, rapid deployment, and reduced infrastructure investment requirements enabling distributed team collaboration.

- Fastest Growing Solution: Artificial intelligence and machine learning integration experiencing fastest growth momentum, propelled by automated pattern detection capabilities, predictive modeling advancement, self-service analytics expansion, and natural language processing integration reducing analytical expertise requirements.

- Key Market Opportunity: Vertical-specific analytics platforms expansion with 2,000+ specialized solutions addressing healthcare digital transformation, BFSI compliance automation, retail omnichannel optimization, and government public sector modernization, creating high-margin market segments with premium pricing justification.

| Key Insights | Details |

|---|---|

| Global Product Analytics Market Size (2026E) | US$ 14.4 Bn |

| Market Value Forecast (2033F) | US$ 36.9 Bn |

| Projected Growth CAGR(2026-2033) | 14.4% |

| Historical Market Growth (2020-2025) | 12.2% |

Market Dynamics

Market Growth Drivers

Cloud-Based Analytics Adoption and Real-Time Intelligence Requirement Acceleration

Cloud-based product analytics commanding dominant positioning with web-based solutions capturing 63.5% market share establishes primary growth driver through superior accessibility, rapid deployment, and distributed team support capabilities. Enterprise demand for real-time intelligence enabling immediate identification of customer behavior patterns and friction points drives accelerated cloud migration from legacy on-premise systems. Software segment capturing 57.9% market share in 2025 reflects centralized analytical platforms' necessity for consolidating behavioral data and converting to actionable insights supporting performance tracking, cohort analysis, and funnel breakdowns.

Browser-native platform preference eliminating infrastructure complexity combined with seamless integration with cloud environments and digital-first business models establishes compelling adoption case for distributed enterprises globally. Cost optimization through consumption-based pricing models enabling organizations to scale analytics investment proportional to data volume supports accelerating adoption particularly among emerging market enterprises, ensuring sustained growth momentum through forecast period.

Digital Transformation Across Enterprise Sectors and Product-Led Growth Strategy Adoption

Unprecedented digital transformation initiatives across BFSI, retail, healthcare, energy, and telecommunications sectors generating substantial demand for advanced product analytics capabilities to optimize customer journeys, improve conversion funnels, and enhance product lifecycle visibility establishes structural market expansion driver. BFSI sector demand including KYC, AML compliance automation, real-time settlement tracking, and creditworthiness assessment acceleration through AI-driven analytics solutions creates high-value market segment with premium pricing justification.

Retail and e-commerce adoption explosion including omnichannel integration, inventory optimization, and dynamic pricing strategies supported by expansion of digital marketplaces and social commerce platforms drives accelerated analytics solution deployment. Product-led growth strategy adoption across SaaS companies requiring detailed product usage analysis, feature adoption tracking, and retention optimization create dedicated analytics platform demand from fast-growing software organizations. Healthcare digital transformation including telemedicine expansion and electronic health record digitization creating regulatory compliance requirements and data privacy emphasis support healthcare-specific analytics solution adoption, ensuring multi-sector growth sustainability through forecast period.

Market Restraints

High Technical Implementation Complexity and Analytical Skill Shortage Challenges

Product analytics platform implementation requiring specialized technical expertise for data integration, workflow automation, and infrastructure provisioning creates significant adoption barriers particularly for resource-constrained organizations lacking internal analytics capabilities. Critical shortage of data scientists and analytics professionals with expertise in advanced analytics, machine learning, and data interpretation limits organizations' ability to derive maximum value from deployed analytics platforms, reducing return on investment and adoption momentum. Complex integration requirements with existing enterprise systems including legacy databases, CRM platforms, and data warehouses extend implementation timelines and increase total cost of ownership offsetting platform licensing savings.

Data Privacy, Cybersecurity Risks, and Regulatory Compliance Complexity

Heightened cybersecurity concerns and stringent data privacy regulations including GDPR, HIPAA, and regional compliance requirements create additional implementation layers increasing solution complexity and cost particularly in regulated industries. Risk of unauthorized data access combined with data residency requirements limiting cloud deployment options force organizations toward on-premise solutions with reduced scalability and operational efficiency limiting market expansion velocity.

Market Opportunities

Vertical-Specific Analytics Platforms and Industry-Tailored Solutions Expansion

Emergence of more than 2,000 vertical-specific analytics platforms addressing unique industry requirements creates exceptional growth opportunity for specialized solution providers serving niche market segments with deep industry expertise. BFSI segment requiring specialized compliance automation, risk assessment, and fraud detection capabilities establishing high-value market opportunity with premium pricing justification for tailored solutions addressing sector-specific regulatory mandates. Healthcare industry analytics platforms emphasizing HIPAA compliance, patient privacy protection, and telemedicine integration create dedicated market segment with exceptional growth potential supported by accelerating digital health transformation and expansion of remote patient monitoring.

Retail omnichannel analytics solutions integrating point-of-sale, inventory, marketplace, and customer touchpoint data into unified decision-support platforms establish fastest-growing application segment driven by explosive e-commerce expansion and dynamic pricing adoption. Government and public sector analytics adoption driven by digital government initiatives, open data mandates, and citizen engagement optimization create emerging market opportunity, establishing multi-segment expansion opportunity through forecast period.

Artificial Intelligence and Machine Learning Integration Driving Next-Generation Product Innovation

Integration of advanced artificial intelligence and machine learning capabilities including automated pattern detection, predictive modeling, and natural language processing into product analytics platforms creates differentiation opportunity enabling organizations to derive deeper insights with minimal analytical expertise requirements. Predictive analytics capability expansion enabling organizations to forecast customer churn, identify growth opportunities, and optimize resource allocation creates premium product positioning justifying higher pricing strategies for AI-enabled platforms. Self-service analytics and low-code/no-code platforms eliminating requirement for specialized technical expertise expand addressable market to non-technical business users and SME organizations with limited IT resources.

Automated anomaly detection and real-time alerting systems identifying critical product issues and customer behavior shifts instantly enable rapid response and proactive product optimization establishing compelling business case for next-generation analytics solutions. Mobile-first analytics and edge computing integration supporting real-time analysis of IoT sensor data and mobile application performance create emerging market opportunity for next-generation platform providers, establishing sustained innovation-driven growth through forecast period.

Category-wise Insights

Solution Analysis

Cloud-based product analytics platforms command dominant market position with estimated 75% share driven by superior scalability, real-time accessibility, and reduced infrastructure investment requirements compared to on-premise alternatives. Web-based solutions capturing 63.5% market share in 2025 reflect universal preference for browser-native platforms eliminating complex installation and maintenance burden. Software platforms comprising 57.9% market share demonstrate overwhelming enterprise preference for centralized analytical systems consolidating behavioral data and providing actionable insights over fragmented, point-solution approaches.

Rapid deployment capability enabling organizations to activate analytics within weeks rather than months supports accelerated time-to-value and faster return on investment justification. Seamless integration with cloud-native applications and microservices architectures combined with API-first design principles establish cloud solutions as de facto standard for digital-first organizations globally, ensuring sustained cloud dominance throughout forecast period.

Enterprise Size Analysis

Large enterprises command estimated 75% market share through comprehensive platform requirements, complex integration needs, and substantial analytics budgets supporting premium solution purchasing from established market leaders. SME adoption accelerating at faster growth rates particularly in cloud-based deployment driven by reduced implementation complexity and consumption-based pricing models eliminating prohibitive upfront capital investment.

SME preference for ease-of-setup solutions including auto-capture capabilities eliminating engineering resource requirements establishes specialized market segment for simplified, user-friendly product analytics platforms enabling rapid adoption without technical expertise. Large enterprise emphasis on custom implementation, enterprise support, and complex security requirements creates premium market segment supporting higher pricing and service-driven differentiation strategies for tier-one solution providers, ensuring both segments growth sustainability throughout forecast period.

Industry Analysis

Retail and e-commerce commanding estimated 40% market share as largest industry adopter driven by omnichannel integration requirements, inventory optimization needs, and conversion rate improvement focus. Healthcare industry experiencing fastest growth trajectory with CAGR exceeding 20% driven by telemedicine expansion, electronic health record digitization, and remote patient monitoring advancement creating substantial analytics demand for patient engagement optimization.

BFSI sector capturing 25% market share with premium pricing justification through compliance automation emphasis, risk management requirements, and creditworthiness assessment acceleration leveraging AI-driven analytics solutions. Travel and hospitality segment growing 18% CAGR driven by post-pandemic recovery, customer journey optimization, and personalization strategy emphasis. Energy and utilities sector adoption accelerating with 15% CAGR driven by smart grid optimization, demand forecasting, and IoT sensor data integration for operational efficiency improvement, establishing multi-industry growth diversification throughout forecast period.

Regional Insights

North America Product Analytics Trends

North America maintains developed market maturity with United States commanding regional leadership through strong innovation ecosystem, mature SaaS industry, and early product-led growth strategy adoption. Product-led growth focus driving demand for advanced analytics platforms enabling feature adoption tracking, user engagement optimization, and retention improvement across SaaS companies and digital-first organizations. Regulatory clarity regarding data privacy compliance supporting accelerated cloud analytics adoption with enterprises confident in platform security and GDPR/CCPA compliance capabilities.

Substantial enterprise technology budgets supporting premium analytics platform adoption with organizations prioritizing real-time intelligence and predictive analytics capabilities for competitive differentiation. Mature market characteristics including high platform standardization, established vendor relationships, and preference for established market leaders like Mixpanel, Amplitude, and Heap driving consolidation around proven solutions.

Europe Product Analytics Trends

Europe represents advanced developed market with Germany and United Kingdom commanding regional leadership through established enterprise software ecosystem and stringent data protection standards. GDPR compliance requirements establishing institutional mandate for data privacy-first analytics solutions with organizations requiring transparent data handling and user consent mechanisms within product analytics platforms. Premium product adoption preference reflecting quality-conscious enterprises valuing security, compliance, and reliability over lowest-cost alternatives.

EU regulatory emphasis on data protection and individual privacy rights driving innovation in privacy-preserving analytics technologies and anonymization capabilities within product analytics platforms. Enterprise preference for established European and global tier-one vendors with proven compliance track records supporting market consolidation around IBM, Google, Oracle, and Salesforce solutions, establishing stable, mature market growth trajectory through forecast period.

Asia Pacific Product Analytics Trends

Asia-Pacific commands fastest regional growth at 21.0% CAGR driven by China establishing market dominance with USD 4,882 million projected by 2033 and India experiencing exceptional 21.8% CAGR fueled by rapid digital commerce expansion and cloud adoption acceleration. China's massive manufacturing base leveraging analytics for supply chain optimization with over 60% of large manufacturers integrating advanced analytics solutions supporting Industry 4.0 transformation. India's extraordinary growth momentum reflecting booming population, rapid urbanization, and government digital transformation initiatives creating substantial analytics demand from emerging e-commerce platforms and startups.

Japan maintaining quality-focused, premium market segment with 20.3% CAGR driven by specialized manufacturing analytics and automotive industry focus. ASEAN region emerging as fastest-expanding segment with digital commerce explosion, mobile-first markets, and government smart city initiatives creating substantial analytics demand from cost-sensitive organizations seeking affordable cloud-based solutions, establishing sustained Asia-Pacific expansion momentum through forecast period.

Competitive Landscape for the Product Analytics Market

The product analytics market exhibits moderate consolidation dominated by tier-one global technology companies including IBM, Google, Oracle, and Salesforce commanding substantial enterprise market share through comprehensive platform portfolios, established customer relationships, and enterprise support capabilities. Specialized analytics platforms including Mixpanel, Amplitude, Heap, and Fullstory establishing competitive positions through superior user experience, ease-of-setup, and domain specialization particularly in e-commerce and SaaS segments. Vertical-specific solution providers capturing niche market segments with deep industry expertise serving healthcare, BFSI, and retail verticals with compliance-first, industry-tailored platforms. R&D-driven competition emphasizing AI/ML integration, real-time capabilities, and mobile-first architectures creating continuous innovation cycle supporting sustained market dynamism.

Key Market Developments

- In March 2025, Salesforce expanded its product analytics capabilities within Tableau by introducing real-time embedded analytics powered by AI-driven insights, enabling enterprises to unify customer, product, and behavioral data across digital touchpoints and accelerate data-informed product optimization decisions at scale.

- In September 2024, Amplitude launched its next-generation AI Copilot for product analytics, allowing product teams to generate automated insights, predictive user behavior analysis, and natural-language queries, significantly reducing analysis time and improving decision velocity for digital product development.

- In June 2024, Mixpanel announced major enhancements to its enterprise product analytics suite, including advanced data governance, privacy-first analytics, and deeper cloud data warehouse integrations, addressing growing regulatory compliance requirements and enterprise-scale analytics adoption globally.

Companies Covered in Global Product Analytics Market

- IBM Corporation

- Oracle

- Salesforce

- Mixpanel

- Piwik

- Heap

- Pendo

- Amplitude

- Risk Edge Solution

- Latent View

- Plytix

- Fullstory Inc.

- Indicative Inc.

- Hevo Data Inc.

Frequently Asked Questions

The global Product Analytics Market is projected to reach US$ 36.9 billion by 2032, expanding from US$ 14.4 billion in 2025 at a CAGR of 14.4%, driven by cloud analytics adoption acceleration, digital transformation across enterprises, AI/ML integration, Asia-Pacific growth leadership, and industry-specific solution expansion.

Market demand growth is driven by multiple converging factors including cloud-based solutions commanding 63.5% market share with web-based platform preference, digital transformation initiatives across BFSI, retail, healthcare, and telecommunications sectors, product-led growth strategy adoption across SaaS companies, real-time intelligence necessity for competitive advantage, AI/ML integration enabling automated pattern detection, and vertical-specific analytics platform emergence addressing industry-unique regulatory requirements.

Cloud-based product analytics platforms command market leadership with estimated 65-75% market share, driven by superior scalability, real-time accessibility, rapid deployment capability, reduced infrastructure investment requirements, seamless integration with cloud-native applications, and distributed team collaboration support compared to on-premise alternatives.

North America maintains market leadership anchored by United States innovation ecosystem dominance, product-led growth strategy pioneer position, substantial enterprise analytics budgets, regulatory clarity supporting cloud adoption, and established market consolidation around tier-one vendors including IBM, Google, Oracle, and Salesforce.

Major market opportunities include vertical-specific analytics platform expansion with 2,000+ specialized solutions serving healthcare, BFSI, and retail sectors; AI/ML integration enabling next-generation predictive analytics; self-service and low-code platform expansion reducing analytical expertise requirements; Asia-Pacific explosive growth particularly India's 21.8% CAGR; and government and public sector modernization creating emerging market opportunities.

Leading market players include Mixpanel excelling in core analytics and predictive capabilities; Amplitude commanding data visualization and engagement features; Fullstory establishing session replay and behavioral insights leadership; Heap specializing in auto-capture and ease-of-setup; and enterprise leaders IBM, Google, Oracle, and Salesforce dominating large-scale enterprise deployments with comprehensive platform portfolios and established customer ecosystems.