- Food Ingredients & Additives

- Global Cranberry Flavor Market

Global Cranberry Flavor Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Cranberry Flavor Market by Flavor (Liquid, Powder, Paste, Concentrate, Others), Application (Food and Beverage, Cosmetics, Pharmaceuticals, Nutraceuticals), End Use (Household, Commercial, Industrial), Distribution Channel (Online Retail, Offline Retail, Direct Sales), and Regional Analysis from 2026 to 2033.

Cranberry Flavor Market Size and Trends Analysis

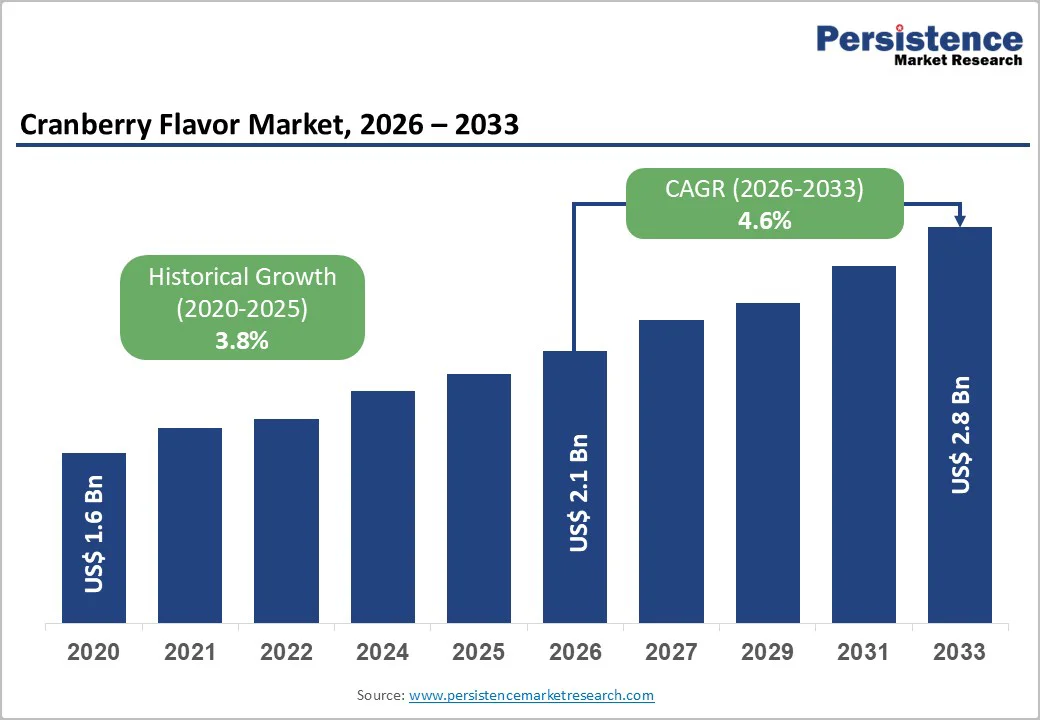

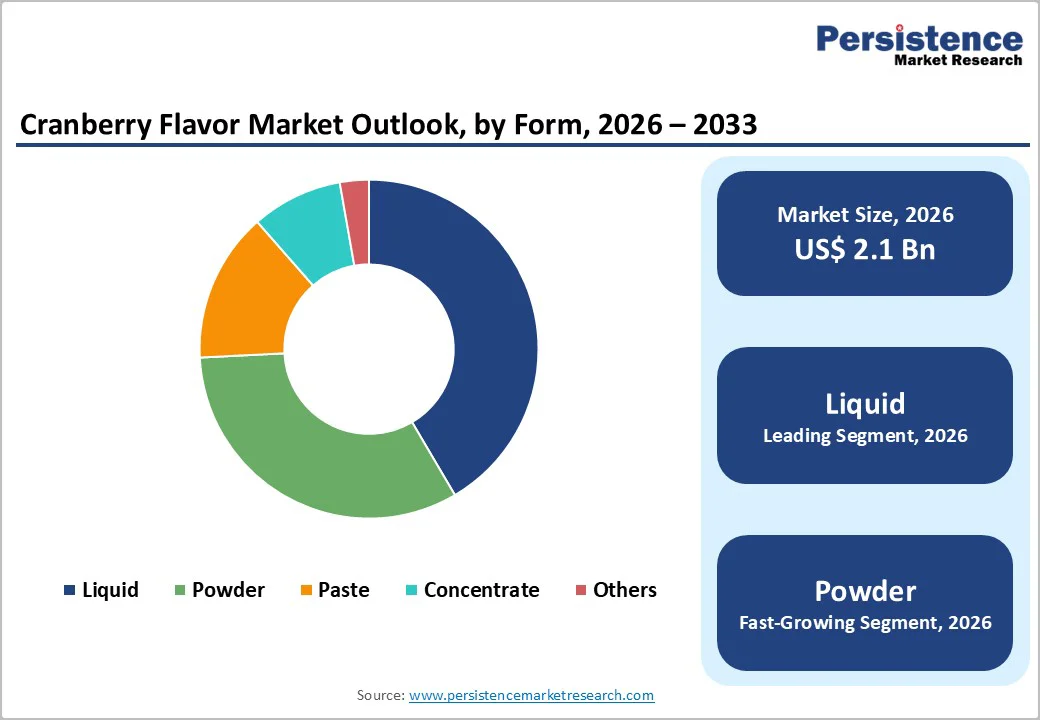

The global Cranberry Flavor Market is estimated to grow from US$ 2.1 Bn in 2026 to US$ 2.8 Bn by 2033. The market is projected to record a CAGR of 4.6% from 2026 to 2033.

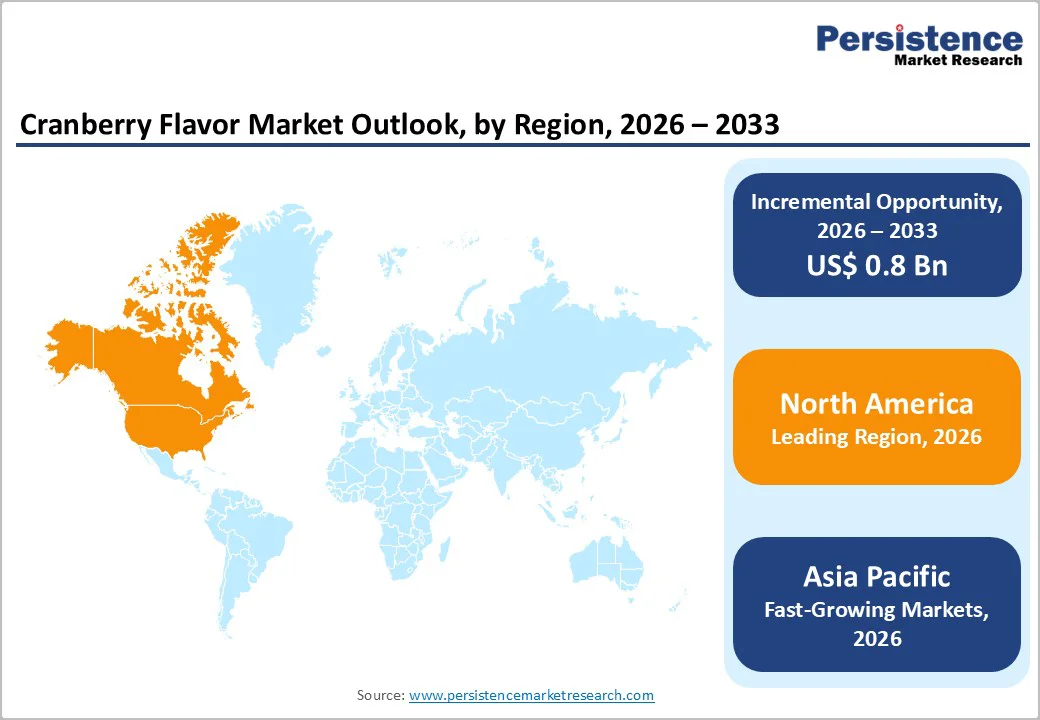

The cranberry flavor market is growing steadily, driven by increasing health awareness, rising demand for functional foods and beverages, and expanding use in nutraceuticals and dietary supplements. North America leads the market due to strong consumer familiarity, established distribution channels, and high adoption of cranberry-flavored products. Meanwhile, the Asia-Pacific region is experiencing the fastest growth, driven by a health-conscious population, expanding e-commerce penetration, and greater availability of innovative cranberry-based flavors and functional ingredients across food, beverage, and supplement applications.

Key Industry Highlights

- Dominant Segment: Liquid cranberry flavors lead the market in 2025 with 41.5% share, driven by their versatility in beverages, sauces, and functional foods, ease of formulation, and widespread consumer acceptance. They are extensively used across food, beverage, nutraceutical, and supplement applications, making them a preferred choice among cranberry flavor formats.

- Dominant Region: North America holds 40.6% share in 2025, supported by strong consumer familiarity with cranberry flavors, established distribution channels, and high adoption in food and beverage products. Europe follows, while Asia-Pacific is the fastest-growing region, driven by rising health awareness, expanding e-commerce, and greater availability of innovative cranberry-based flavors.

- Market Drivers: Growth is fueled by an increasing health-conscious population, demand for functional ingredients, the incorporation of cranberry flavors into foods, beverages, and supplements, and a preference for natural, convenient, and plant-based flavor solutions.

- Market Opportunity: Key opportunities include development of clean-label and plant-based cranberry flavors, functional blends targeting health benefits, expansion into emerging markets, growth in online retail channels, and innovation in flavor, formulation, and application across food, beverages, nutraceuticals, and dietary supplements.

| Key Insights | Details |

|---|---|

| Global Cranberry Flavor Market Size (2026E) | US$ 2.1 Bn |

| Market Value Forecast (2033F) | US$ 2.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.8% |

Market Dynamics

Driver – Demand for Functional Foods & Beverages

Consumer demand for functional foods and beverages, defined as products that provide health benefits beyond basic nutrition, is a major driver of the Cranberry Flavor Market. In the United States, about 64% of adults consumed fortified or functional food and drink products in 2024, with consumption patterns showing that nearly 46% of households include functional foods in weekly grocery purchases. Cranberry flavors are increasingly used in juices, smoothies, and gummy supplements that align with this trend because cranberries contain antioxidants, vitamins, and plant compounds associated with health benefits such as immune support and gut health. This broad adoption of functional products correlates with the integration of cranberry flavor into beverages and supplements for health-oriented consumers.

Cranberry ingredients themselves have documented nutritional properties that support the appeal of cranberry-flavored functional products. For example, cranberries are rich in vitamin C and phytonutrients, contributing to antioxidant activity that may support various aspects of health. While the U.S. Food and Drug Administration notes that scientific evidence is limited and inconsistent for some health claims, it has recognized that daily consumption of certain cranberry juice beverages may help reduce recurrent urinary tract infections in healthy women. Growing public awareness of these potential benefits, along with broader health trends favoring antioxidant and immune-supporting ingredients, reinforces demand for cranberry-flavored functional foods and beverages.

Restraints – Seasonal and Supply Chain Constraints

The cranberry crop is inherently seasonal, with harvests concentrated in the autumn months (typically late September through early November) in major producing regions such as Wisconsin and Massachusetts, which together account for a large share of U.S. cranberry output. Outside this narrow harvest window, fresh berries are scarce because cranberries are highly perishable, complicating year-round supply stability. This seasonal dependency means processors of cranberry flavors and extracts must rely on stored, frozen, or concentrated inventories for much of the year, which can increase costs and complicate inventory management when supply is limited.

Seasonal production also makes the supply chain sensitive to weather variability that directly affects crop yields and quality. For example, USDA forecasts show that cranberry production in key U.S. states such as Wisconsin and Massachusetts can fluctuate year-over-year due to drought, heat stress, or drought conditions, with some states recording production declines of up to 22 percent in recent seasons. These fluctuations in raw material availability propagate through the supply chain, leading to volatility in input costs for cranberry flavor manufacturers and periodic shortages that challenge consistent product delivery to food, beverage, and nutraceutical customers.

Opportunity – Growth in Plant-Based and Clean-Label Products

Consumer preference for plant?based and clean?label products presents a significant opportunity for the Cranberry Flavor Market because these trends align with increasing demand for natural, minimally processed ingredients. In the United States, 71% of Americans say they are familiar with plant-based products, and 86% report they are likely to purchase them in the next three months, indicating strong mainstream acceptance of plant-based foods and natural sources. This growing interest in plant-derived products reflects broader shifts toward diets perceived as healthier and more sustainable. Integrating cranberry flavor into plant-based foods and beverages supports this demand, enhancing product appeal and capturing consumers seeking natural, health-oriented ingredients.

Clean-label preferences further bolster this opportunity for cranberry flavors because consumers increasingly equate clean labels with health and transparency. Nearly half of global consumers purchased more fresh, unprocessed foods in the past year, and about 30% are reducing processed foods and limiting artificial additives, indicating a strong shift toward simpler and more recognizable ingredients. Cranberry flavor, derived from a natural fruit source, meets clean-label expectations and can be marketed to consumers seeking to avoid artificial flavors and additives. As food and beverage companies respond to these preferences by reformulating products with clean-label ingredients, incorporating cranberry flavor into such offerings is an avenue to meet consumer expectations and expand market share.

Category-wise Analysis

By Form, Liquid Dominates the Cranberry Flavor Market

Liquid form occupies 41.5% share of the global market in 2025, because most cranberry flavor applications are in beverages, which are consumed primarily in liquid form. Data from the U.S. Department of Agriculture show that fruit juices, smoothies, and flavored waters are integral to daily diets, with adults consuming approximately one?third of a serving of fruit juice per day on average, highlighting the high baseline demand for liquid products. Liquid flavors dissolve uniformly in water-based systems, ensuring consistent taste and aroma without clumping or uneven distribution, which is critical for large-scale beverage production. This ease of formulation, combined with strong consumer preference for ready-to-drink juices, flavored waters, and functional beverages, makes liquid cranberry flavors the dominant form in the market, supporting both industrial efficiency and consumer acceptance.

By Application, Food and Beverages is gaining traction due to high consumption of juices, drinks, and snacks

The Food and Beverage segment dominates the Cranberry Flavor Market because cranberry flavor is most frequently used in consumer products such as juices, flavored waters, and snacks, which represent a large share of daily intake worldwide. According to USDA dietary data, fruit juice consumption contributes meaningfully to U.S. diets, with adults consuming roughly one-third of a serving of fruit juice per day on average, underscoring the importance of juice products to consumers. Additionally, data from the National Health and Nutrition Examination Survey show that over 60% of U.S. adults drink flavored beverages regularly, reflecting broad demand for flavored drinks. Because cranberry flavor is especially suited to juice and beverage profiles and is also incorporated into sauces, confections, and dairy products, food and beverage applications account for the largest share of cranberry flavor use.

Regional Insights

North America Cranberry Flavor Market Trends

North America dominates the Cranberry Flavor Market with 40.6% share in 2025, because it is the largest producer and consumer of cranberries, supplying the raw material base that supports extensive flavor production and processing. The United States and Canada together account for the vast majority of global cranberry output, with the U.S. alone harvesting approximately 368,000 metric tons in 2023, and North America producing over 75% of the world's cranberries. Cranberry products — especially juices, sauces, and processed forms — are deeply embedded in North American consumption patterns, with Americans consuming roughly 400 million pounds of cranberries per year, most of which is processed for beverages and other products. The strong production infrastructure, abundant raw materials, and high regional consumption translate directly into greater demand for cranberry flavors in food and beverage applications, reinforcing North America’s leading position.

Europe Cranberry Flavor Market Trends

Europe is an important region in the Cranberry Flavor Market because cranberry consumption and related product demand are rising across multiple countries, reflecting broader shifts toward health-oriented foods and beverages. In 2024, combined blueberry and cranberry consumption in Europe reached approximately 266,000?tons, increasing by about 12?percent year?over?year, and the total market value for these berries in the region rose to around USD?2?billion, demonstrating substantial usage of cranberry and similar fruit products in European diets. European consumers increasingly seek fruit-based flavors in juices, functional beverages, and snacks, and imports of cranberries into the EU grew significantly in early 2025, with dried cranberry imports up 11.5%, indicating expanding interest in cranberry products and flavors. These consumption trends support strong demand for cranberry flavor applications across food and beverage categories in Europe.

Asia-Pacific Cranberry Flavor Market Trends

Asia Pacific is the fastest-growing region in the Cranberry Flavor Market, driven by rising health awareness, urbanization, and growing consumption of functional foods and beverages. Governments in the region report rising fruit and juice intake; for example, per capita fruit consumption in China reached approximately 33 kg annually in 2023, reflecting the growing incorporation of fruit into daily diets. Additionally, juice consumption across Asia-Pacific countries is steadily increasing, with more consumers choosing nutrient-rich, antioxidant-containing beverages. Rapid urbanization and the expansion of modern retail and e-commerce platforms make cranberry-flavored products more accessible. Combined, these factors — growing health consciousness, higher disposable income, and improved product availability — are driving strong adoption of cranberry flavors in beverages, snacks, and functional food applications throughout the region.

Market Competitive Landscape

Leading companies in the Cranberry Flavor Market prioritize innovation, safety, and consumer-friendly products to enhance flavor, texture, and functionality. Through R&D, they ensure palatability, nutrient stability, and convenience, while partnerships with healthcare experts build credibility. These initiatives increase consumer adoption, satisfaction, and daily usage, driving growth and fostering innovation across the global cranberry flavor industry.

Key Industry Developments:

- In September 2025, Ocean Spray® Ingredients showcased its latest innovations and “Cran-tastic” concepts at its Cranberry Café during IBIE 2025. The company presented a variety of creative applications for cranberry ingredients, highlighting new flavors, formulations, and functional uses tailored for the baking and foodservice industries.

- In June 2025, Ocean Spray launched a range of new Craisins® Dried Cranberries flavors aimed at summer snacking. The company introduced these bold, fruit-forward varieties to cater to consumers seeking convenient, flavorful, and portable snack options during the summer season.

Companies Covered in Global Cranberry Flavor Market

- Ocean Spray Cranberries

- Decas Cranberry Products

- Givaudan

- Kerry Group

- Symrise

- Sensient Technologies

- Northland Cranberries

- Tropicana Products

- Firmenich

- Cranberry Acres

- Fruit d'Or

- Harvest Fruit

- Wiberg

- Bogh Engineering

- The J.M. Smucker Company

- Others

Frequently Asked Questions

The global Cranberry Flavor Market is projected to be valued at US$ 2.1 Bn in 2026.

Rising health awareness, functional foods demand, beverage consumption, nutraceutical use, and natural ingredient preference drive growth.

The global Cranberry Flavor Market is poised to witness a CAGR of 4.6% between 2026 and 2033.

Plant-based products, clean-label trends, functional blends, emerging markets, e-commerce growth, flavor innovation, and formulation improvements.

Ocean Spray Cranberries, Decas Cranberry Products, Givaudan, Kerry Group, Symrise, Sensient Technologies.