- Automotive

- Electric Forklift Market

Electric Forklift Market Size, Share, Trends, Growth, Forecasts 2026 - 2033

Electric Forklift Market Product Type (Counterbalanced Forklift, Pallet Truck, Stacker, Reach Truck, Order Picker & Others), Battery Type (Lithium-Ion, Lead Acid, Hydrogen Fuel-Cell), Lift Capacity (Up to 5 Ton, 5.1 to 10 Ton, Above 10 Ton), End-Use Industry (Logistics & Warehousing, Manufacturing, Chemicals & Pharmaceuticals, Food & Beverage, Retail & E-Commerce, Construction, Misc.), and Regional Analysis from 2026 to 2033

Electric Forklift Market Share and Trends Analysis

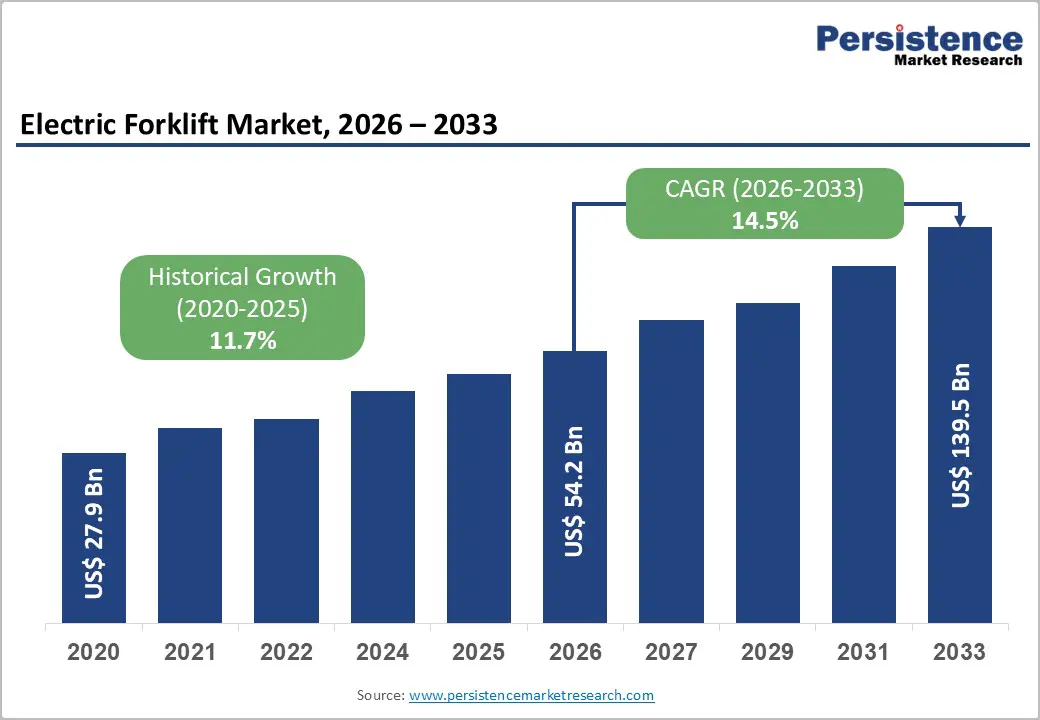

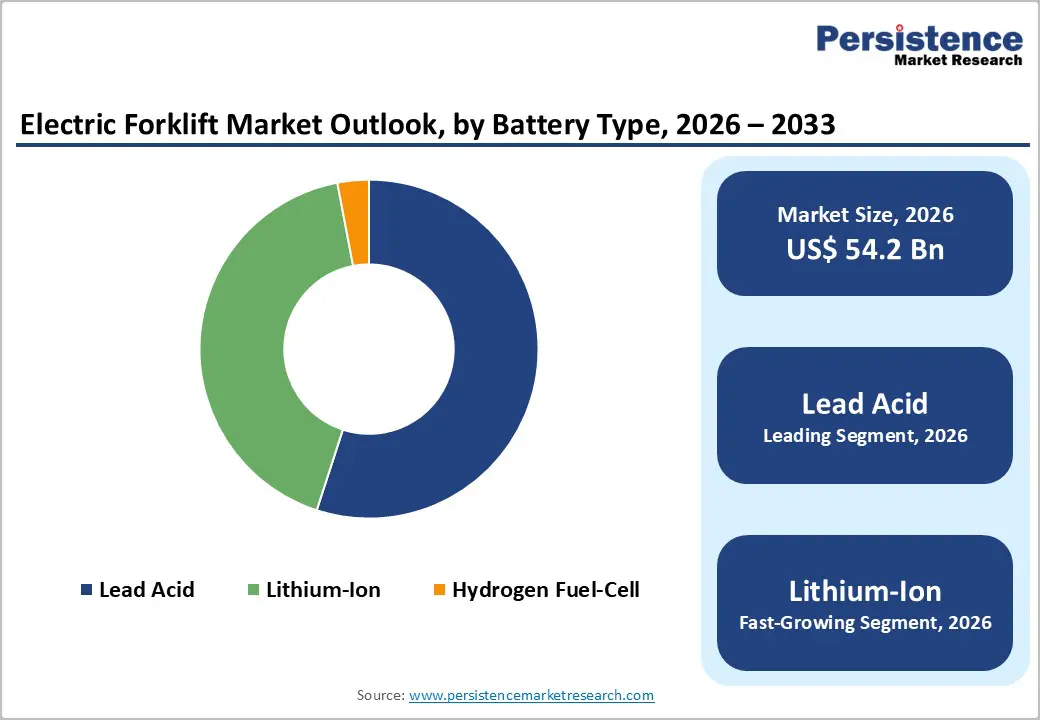

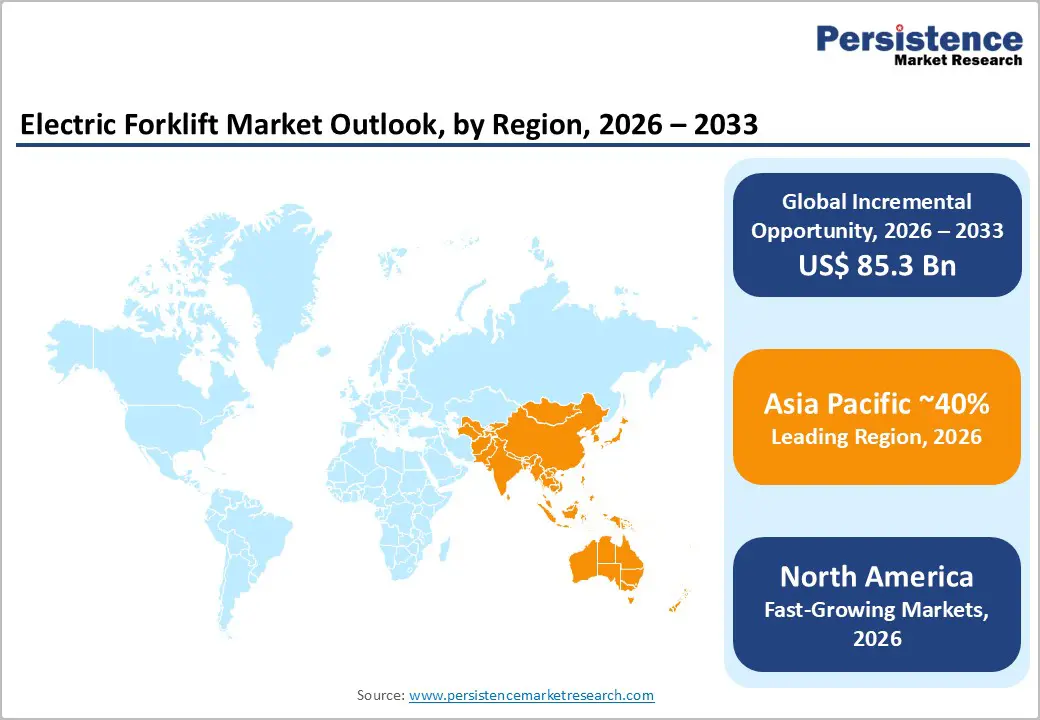

The global electric forklift market size is likely to be valued at US$54.2 billion in 2026 and is projected to reach US$139.5 billion by 2033, growing at a CAGR of 14.46% between 2026 and 2033.

Market expansion is driven by unprecedented e-commerce growth, with around 2.7 billion online shoppers generating significant sales, accelerating global warehouse automation and logistics investment. Lithium-ion battery advances enable 1-2 hour charging versus 8+ hours for lead-acid, transforming economics. Emission regulations, sustainability mandates, and labor shortages further accelerate automation, positioning electric forklifts as essential infrastructure for resilient supply chain modernization.

Key Industry Highlights:

- Lithium-Ion Technology Dominance: Lithium-ion batteries expand fastest at 16% CAGR, establishing clear trajectory toward market leadership as lead-acid technology (55% current share) declines to 35-40% by 2033 through superior operational economics.

- Counterbalanced Leadership with Pallet Truck Growth: Counterbalanced forklifts maintain 45% market share as product category leader; electric pallet trucks accelerate at 14.6% CAGR, driven by last-mile delivery and micro-fulfillment requirements.

- Food & Beverage Sector Acceleration: The Food & Beverage industry emerges as the fastest-growing end-use segment, with a 15.7% CAGR, driven by cold-chain logistics expansion and e-commerce fulfillment demand for perishable goods.

- Asia-Pacific Market Dominance with India Leadership: Region commands ~40% global market share with China and India driving exceptional growth; India specifically demonstrates 15.2% CAGR through 2035, supported by National Logistics Policy implementation.

- Autonomous Technology and FaaS Model Emergence: Strategic developments, including Jungheinrich-Magazino acquisition and Crown lithium-ion integration, establish autonomous capability and subscription-based equipment access as emerging differentiators, addressing labor shortage constraints.

| Key Insights | Details |

|---|---|

| Electric Forklift Market Size (2026E) | US$ 54.2 billion |

| Market Value Forecast (2033F) | US$ 139.5 billion |

| Projected Growth CAGR (2026 - 2033) | 14.5% |

| Historical Market Growth (2020 - 2025) | 11.7% |

Market Dynamics Analysis

Drivers - Explosive E-Commerce Growth and Warehouse Automation Acceleration

E-commerce market expansion represents the paramount driver of electric forklift demand, with prominent online sales globally in 2024 & projected to grow at a significant pace. This growth fundamentally transforms logistics infrastructure requirements: major e-commerce operators operate 300+ fulfillment centers globally, requiring high-throughput material handling capacity. Industry data indicates approximately 64% of warehouses globally have adopted some form of automation, with penetration exceeding 75% among large distribution networks. Electric forklifts specifically address e-commerce operational demands through improved maneuverability in constrained facility spaces, reduced noise, enabling 24/7 operations in residential-proximate distribution centers, and a superior total cost of ownership due to lower maintenance requirements compared to internal combustion alternatives. Recent warehouse automation market analysis projects a ~15% CAGR, directly correlating with the expansion of electric forklift fleets.

Lithium-Ion Battery Technology Maturation and Operational Superiority

Lithium-ion battery adoption is the fastest-growing market segment, with a 16% CAGR, fundamentally redefining equipment economics and operational capabilities. Advanced lithium-ion systems deliver 1-2 hours of charging time versus 8+ hours for traditional lead-acid batteries, enabling opportunity charging during operator breaks without degrading battery performance, which is critical for continuous warehouse operations. Energy density advantages translate into operational performance gains: lithium-ion-equipped forklifts demonstrate 30-40% fuel cost reductions while supporting extended operating hours from a single charge. Battery lifecycle economics 2,500+ charge cycles for lithium-ion versus 1,000-1,500 for lead-acid establish superior total cost of ownership despite 2-3x higher upfront acquisition costs.

Integrated battery management systems with predictive maintenance capabilities monitor discharge patterns, optimize charging protocols, and extend equipment lifespan by preventing operation outside warranted parameters. Leading manufacturers, including Crown Equipment, have comprehensively integrated lithium-ion systems across their entire product portfolios, establishing accessibility to this technology beyond premium segments.

Market Restraints

High Capital Equipment Costs and Lithium-Ion Price Sensitivity

Lithium-ion equipped electric forklifts command a premium pricing 2-3x higher than lead-acid alternative systems, creating capital constraint barriers for small and medium-sized enterprises and emerging market contractors. Equipment acquisition costs for advanced lithium-ion forklifts range US$25,000-60,000 depending on lift capacity and specialization, substantially exceeding traditional lead-acid counterparts priced US$15,000-30,000. This pricing differential disproportionately impacts emerging market adoption despite a strong operational case, as financing infrastructure in developing regions remains underdeveloped relative to capital equipment requirements. Lead-acid battery technology dominance, maintaining 55% market share, reflects this cost sensitivity, particularly among price-conscious contractors prioritizing upfront capital minimization over long-term operational economics. Charging infrastructure investment requirements constitute hidden capital costs that limit smaller contractor participation; centralized charging station networks require US$10,000-20,000 per charging point, creating coordination challenges absent in fuel-based systems.

Technology Transition Complexity and Supply Chain Constraints

The market transition from mature lead-acid battery technology to emerging lithium-ion systems faces organizational inertia and operational complexity barriers. Contractor training requirements, equipment compatibility assessment, and charging infrastructure reconfiguration create implementation friction, delaying adoption decisions. Lithium-ion battery supply constraints originating from raw material (lithium, cobalt) sourcing concentration and manufacturing capacity limitations restrict equipment production velocity, particularly in emerging markets with limited direct battery manufacturing capacity. Post-pandemic supply chain disruptions have disproportionately affected specialized component sourcing for advanced battery management systems and thermal regulation equipment, extending equipment lead times 3-6 months beyond historical norms.

Opportunity - Autonomous Forklift Technology and Fleet-as-a-Service Models

Autonomous forklift systems integrating LiDAR sensors, artificial intelligence navigation, and collision-avoidance technologies represent a high-impact opportunity addressing acute labor shortages in developed markets. Leading manufacturers such as Toyota Industries and Jungheinrich are actively deploying autonomous-ready fleets across manufacturing plants and logistics hubs. Hangcha Group has validated industrial-scale adoption by deploying over 7,000 autonomous guided vehicles for customers, including P&G, BMW, and JD.com. Parallelly, Fleet-as-a-Service subscription models are disrupting ownership economics, enabling contractors to access advanced equipment without capital expenditure. This shift accelerates technology penetration, improves fleet utilization, and stabilizes cash flows. Collectively, autonomous deployment and subscription-led access models are expected to generate an incremental US$15-20 billion in revenue through 2033, fundamentally reshaping electric forklift commercialization strategies globally and the industry structure.

Hydrogen Fuel-Cell and Alternative Energy Technologies

Hydrogen fuel-cell forklifts represent an emerging alternative that addresses rapid refueling needs in high-intensity operations, delivering performance between that of lead-acid and lithium-ion systems. Currently accounting for an estimated 2-3% market penetration, this technology could expand to 10-15% by 2033 as hydrogen infrastructure investment accelerates and unit costs decline through scale. Fuel-cell systems offer consistent power output, minimal downtime, and superior performance in cold environments. Market opportunity sizing conservatively estimates a US$3-5 billion addressable segment by 2033, with strongest suitability in cold-chain logistics, food distribution centers, ports, and specialty material handling applications requiring extended operating hours, fast refueling cycles, and predictable energy performance across multi-shift industrial environments supporting decarbonization objectives, operational resilience, workforce productivity, and long-term adoption across global supply chains worldwide.

Category-wise ANALYSIS

Product Type Insights

Counterbalanced forklifts command 45% market share, establishing clear product category dominance driven by versatility across diverse material handling applications and cost-effectiveness relative to specialized equipment. These standardized platforms accommodate variable lift heights, load configurations, and attachment options, enabling deployment across construction, manufacturing, and logistics environments. Market leadership reflects manufacturer investment concentration: leading suppliers including Toyota Industries, KION Group, and Crown Equipment maintain comprehensive counterbalanced product portfolios spanning 2-ton to 30+ ton lift capacity.

Electric pallet trucks expand at 14.6% CAGR, driven by e-commerce order fulfillment requirements enabling single-operator management of high-volume, lower-weight package handling. These pedestrian-controlled units address last-mile distribution challenges, particularly in urban fulfillment networks prioritizing space efficiency and noise reduction. Crown's July 2025 WJ 50 Series launch 1,500kg capacity, lightweight design targeting micro-fulfillment centers exemplifies product evolution matching emerging warehouse architecture requirements.

Battery Type Insights

Lead-acid technology maintains 55% market share despite lithium-ion growth, reflecting cost competitiveness and widespread contractor familiarity. This mature technology segment serves price-sensitive contractors and equipment rental companies prioritizing capital preservation over operational optimization. However, market share erosion accelerates as lithium-ion costs decline through manufacturing scale; lead-acid is projected to decline to 35-40% by 2033.

Lithium-ion systems expand at 16% CAGR, establishing clear trajectory toward market leadership by 2033. Superior performance characteristics (1-2 hour charging, 2,500+ cycles, 30-40% energy cost reduction) are driving adoption acceleration across premium and mid-market segments. OEM integration across entire product portfolios, particularly Crown Equipment's comprehensive V-Force system deployment across the complete forklift lineup, is democratizing technology accessibility, removing premium positioning barriers.

Lift Capacity Insights

Equipment under 5-ton capacity commands 46% market share, reflecting e-commerce fulfillment dominance that prioritizes high-velocity, moderate-weight unit handling across warehouses. This segment achieves the highest shipment volumes through rental, leasing, and subscription models, lowering upfront capital barriers and enabling rapid adoption by third-party logistics providers, retailers, and contractors. Its scalability, maneuverability, and compatibility with lithium-ion batteries reinforce demand in urban distribution centers and last-mile logistics operations globally, supporting consistent replacement cycles and predictable utilization rates in mature markets today.

The 5.1-10 ton segment expands at a 14.7% CAGR, driven by hybrid warehouse operations combining e-commerce fast-pick activity with manufacturing goods receiving requiring intermediate lift capacity. This category balances versatility and specialization, enabling efficient handling of pallets, machinery, and components across logistics hubs and industrial facilities, supporting mixed-use deployment strategies.

Industry Insights

Logistics and warehousing establishments account for 36% of electric forklift demand, reflecting e-commerce infrastructure dominance and rising global investment in third-party logistics automation. This sector records the highest equipment utilization intensity, continuous multi-shift operations, and rapid fleet renewal cycles. Strong corporate sustainability commitments and indoor zero-emission requirements accelerate adoption of lithium-ion and automated forklifts, enabling productivity gains, lower operating costs, and real-time fleet optimization through telematics, reinforcing the segment’s leadership in technology uptake and long-term replacement demand worldwide across modern global distribution networks.

Food and beverage expands at a 15.7% CAGR, driven by growth in cold-chain logistics supporting perishable distribution, pharmaceutical temperature-controlled handling, and specialty food e-commerce fulfillment. These applications demand specialized forklifts with thermal management and corrosion-resistant materials, enabling premium pricing, higher margins, regulatory compliance, and long-term contracts within refrigerated warehouses and facilities globally.

Regional Insights

North America Electric Forklift Market Trends

North America commands approximately 22-24% of global electric forklift market value while demonstrating 14.4% CAGR accelerating growth despite mature market maturity. The United States market drives regional growth through e-commerce logistics infrastructure concentration (Amazon operates 175+ fulfillment centers across North America), manufacturing automation adoption, and regulatory environmental mandates. Canadian market contribution remains modest at 8-10% of regional value, concentrated in manufacturing-intensive regions of Ontario and Quebec. North America's regulatory framework emphasizes workplace safety and environmental emissions reduction, establishing a competitive advantage for manufacturers offering advanced safety features and zero-emission alternatives. California state regulations specifically restrict internal combustion engine equipment in regulated logistics facilities, creating a structured market advantage for electric alternatives. OSHA standards establish baseline safety requirements driving continuous manufacturer equipment redesign, particularly regarding operational visibility, collision avoidance, and ergonomic load management.

Europe Electric Forklift Market Trends

Europe maintains approximately 26% of the global electric forklift market value, reflecting mature market infrastructure combined with aggressive sustainability mandates. Germany, United Kingdom, France, and Spain collectively represent around 70% of European market value, with Germany demonstrating highest per-capita electric equipment adoption driven by Industry 4.0 manufacturing initiative and strict environmental regulations. Germany specifically exhibits an 8.7% CAGR through 2035, supported by automation requirements in automotive and electronics manufacturing. European Union environmental directives establish continent-wide standards that prioritize zero-emission material handling in indoor logistics environments, directly incentivizing the adoption of electric equipment. CE certification requirements establish quality benchmarks that exceed typical global standards, supporting premium equipment positioning for compliant manufacturers. Germany's leadership in smart factory integration creates an advanced customer base valuing autonomous capabilities, telematics integration, and predictive maintenance features unavailable in cost-competitive markets.

Asia-Pacific

Asia-Pacific establishes overwhelming market dominance with approximately 40% global market share while demonstrating the strongest growth momentum driven by manufacturing expansion, e-commerce acceleration, and logistics infrastructure modernization. China alone commands 30.2% of the Asia-Pacific share, with manufacturing automation investment targeting 350+ million square feet of new warehouse capacity by 2030. India demonstrates a remarkable 15.2% CAGR, driven by the implementation of the National Logistics Policy, which supports the development of 700+ million square feet of warehouse infrastructure through 2033. Japan's mature market reflects sophisticated automation adoption, addressing demographic labor constraints and manufacturing export requirements. Asia-Pacific hosts approximately 50-55% of global electric forklift manufacturing capacity, establishing structural cost leadership through labor efficiency and vertical integration. India's manufacturing expansion through the Make in India program and government equipment leasing initiatives creates emerging competitive alternatives to established Japanese and European suppliers.

Competitive Landscape

Market leaders adopt differentiated strategies shaped by geography and product focus. Japanese OEMs emphasize technology leadership and manufacturing quality, supporting premium positioning in developed markets. European manufacturers prioritize sustainability credentials and autonomous capability to meet regulatory demands. Emerging players compete on value and proximity. Industry models increasingly feature Fleet-as-a-Service, autonomous integration, telematics platforms, and battery-swapping infrastructure, expanding revenue beyond sales.

Companies Covered in Electric Forklift Market

- Toyota Industries Corporation

- KION Group

- Jungheinrich AG

- Crown Equipment Corporation

- Mitsubishi Logisnext Co., Ltd.

- Hyster-Yale Materials Handling, Inc.

- Hyundai Material Handling

- Hangcha Group Co., Ltd.

- Godrej & Boyce Manufacturing Company

- Komatsu Ltd.

- Clark Material Handling Company

- Nissan Forklift

- Yale Materials Handling

- Doosan Industrial Vehicle

- Anhui Heli Co., Ltd.

Frequently Asked Questions

The global Electric Forklift Market was valued at US$27.9 Billion in 2020, reached US$54.2 Billion in 2026, and is projected to reach US$139.5 Billion by 2033.

Explosive e-commerce growth, fast-charging lithium-ion batteries, zero-emission regulations, ESG mandates, labor shortages, and Industry 4.0-enabled automation are the primary forces accelerating electric forklift adoption.

The Electric Forklift Market is projected to grow at a CAGR of 14.5% between 2026 and 2033.

Major opportunities lie in India’s logistics expansion, autonomous forklifts, hydrogen fuel-cell systems, cold-chain logistics, and Fleet-as-a-Service models, collectively creating multi-billion-dollar growth avenues by 2033.

The market is led by Toyota Industries, KION Group, Jungheinrich, Crown Equipment, Mitsubishi Logisnext, Hyster-Yale, Hyundai, Hangcha, Godrej & Boyce, Komatsu, and Anhui Heli, supported by strong automation and lithium-ion technology portfolios.