- Electric Mobility

- Electric Boats Market

Electric Boats Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Electric Boats Market by Boat Power (< 5kW, 5-30kW, and >30kW), by Boat Size (< 20ft, 20-50ft, and >50ft), by Power Source (Battery, Solar, and Hybrid and by End-user (Recreational Boats, Commercial Boats and Military & Law Enforcements Boats) and Regional Analysis for 2025 - 2032

Electric Boats Market Share and Trends Analysis

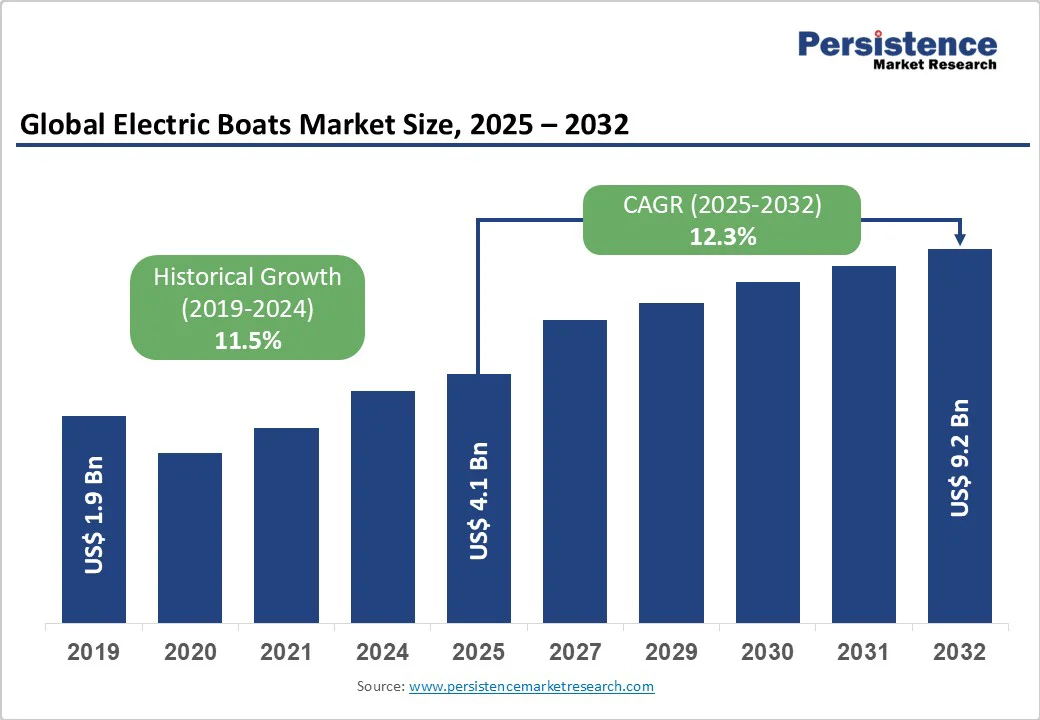

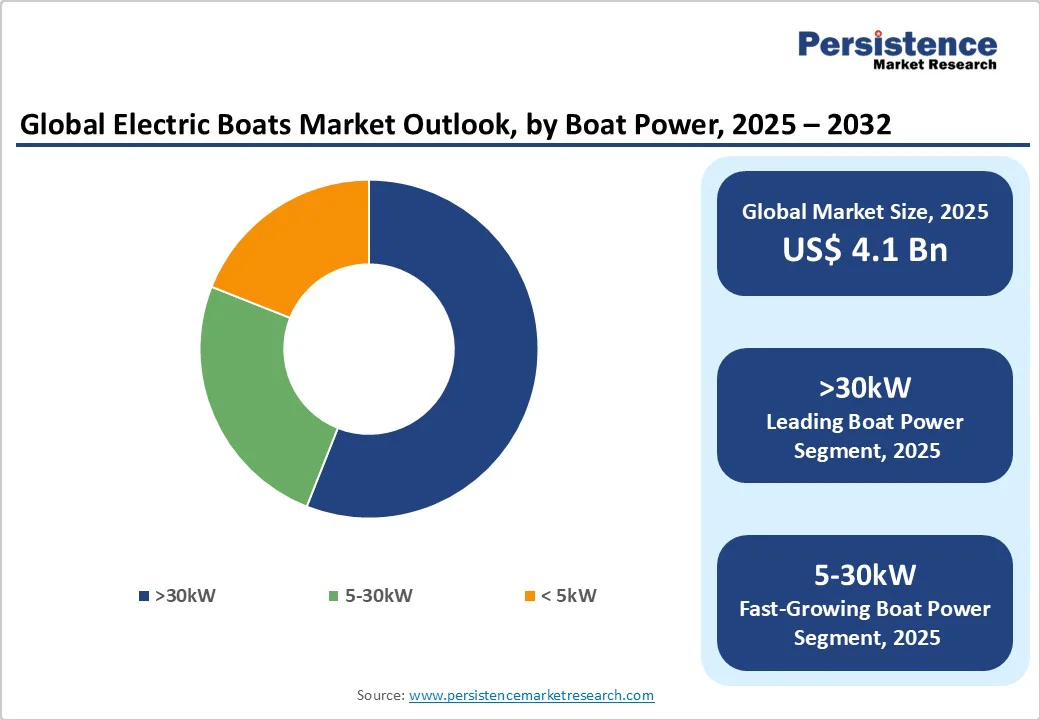

The global electric boats market size is likely to value at US$ 4.1 billion in 2025 and is projected to reach US$ 9.2 billion by 2032, growing at a CAGR of 12.3% between 2025 and 2032.

The Market momentum is driven by stringent environmental regulations, including the International Maritime Organization's carbon reduction strategy and the European Union's Green Deal, targeting climate neutrality by 2050.

Key Industry Highlights:

- Dominant Power Segment: The >30kW segment leads with 52.3% market share, reflecting strong adoption for larger applications. Meanwhile, the 5-30kW segment records the fastest growth, signaling a transition from luxury-focused uses to mainstream adoption.

- Leading End-use Application: Recreational boats dominate with 54.3% market share, while the commercial segment grows fastest, driven by regulatory compliance pressures and operational cost advantages.

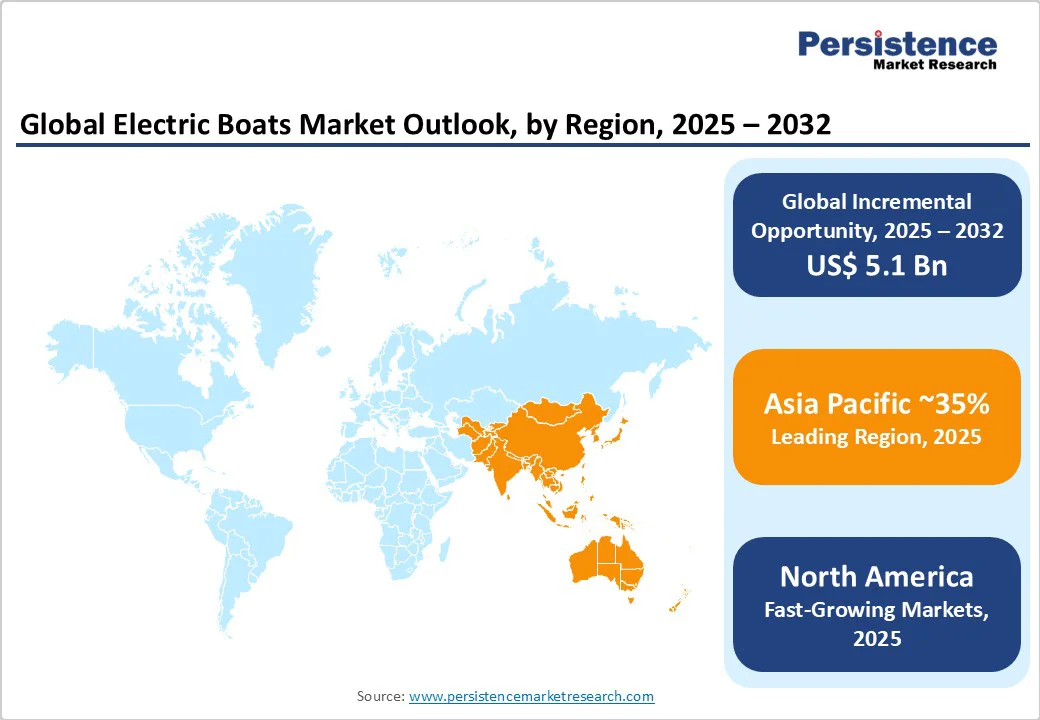

- Fastest-Growing Region: Asia Pacific emerges as the fastest-growing market with 35.2% share, propelled by government support, expanding maritime tourism, and strong regional manufacturing advantages.

- Dominant Power Source: Battery technology holds an 80.3% share, underscoring its maturity and reliability, whereas hybrid systems show the fastest growth, reflecting demand for operational flexibility and longer ranges.

- Key Developments: Strategic funding surpassed USD 200 million during 2024 - 2025, with significant investments in Arc Boats, Candela, and Echandia to accelerate global expansion and innovation.

- Emerging Opportunity: Commercial vessel electrification is gaining momentum through government mandates, creating substantial growth prospects in ferry services, water taxis, and harbor craft applications.

Market Dynamics

Driver - Stringent Environmental Regulations and Government Mandates

Environmental regulations serve as the primary catalyst for electric boat market expansion, with governments worldwide implementing aggressive emission reduction targets that mandate cleaner marine propulsion systems.

The International Maritime Organization's 2020 sulfur cap and subsequent greenhouse gas reduction initiatives compel vessel operators to adopt electric alternatives to traditional combustion engines. The European Union's Green Deal, targeting climate neutrality by 2050, creates legally binding requirements that accelerate electric boat deployment across commercial and recreational segments.

In the Asia Pacific, China's Ministry of Transport's strategic guidelines for inland waterway transportation until 2050 emphasize decarbonization initiatives that boost regional market adoption. Government incentives and subsidies further amplify this trend, with numerous countries offering financial support for electric marine vehicle purchases and charging infrastructure development, creating favorable economics for early adopters.

Advanced Battery Technology and Performance Improvements

Revolutionary advancements in lithium-ion battery technology fundamentally enhance electric boat viability, extending operational range, reducing charging times, and improving overall vessel performance. Modern electric boats achieve three times the battery storage capacity of Tesla Model Y vehicles, delivering 500-horsepower performance with ranges exceeding 50 nautical miles at cruising speeds. Innovations in liquid-cooled battery systems and modular designs enable scaling according to vessel power requirements, while solid-state battery development promises even greater energy density improvements.

Battery management systems now integrate with smart propulsion technologies, offering real-time performance monitoring, predictive maintenance capabilities, and over-the-air software updates that enhance user experience and operational efficiency. Industry partnerships, such as the EUR 12 million European Commission-backed 'Current Direct' project, demonstrate collaborative efforts to reduce battery-electric propulsion system costs while developing innovative Energy-as-a-Service platforms.

Restraint - High Initial Purchase Costs and Premium Pricing

Electric boats command significant price premiums compared to traditional gas-powered vessels, creating substantial barriers to widespread market adoption. Entry-level electric models typically start above USD 100,000, while high-performance boats exceed several hundred thousand dollars, representing 50% cost premiums over comparable combustion-engine alternatives. The Arc One luxury cruiser exemplifies this challenge at USD 300,000, significantly higher than traditional powerboats with similar specifications.

Premium pricing stems from expensive lithium-ion battery systems, specialized electric propulsion components, and limited manufacturing scale economies that prevent cost reduction benefits. Small and medium-sized operators face particular challenges accessing capital for electric vessel investments, especially in regions lacking government incentives or financing support programs.

Inadequate Charging Infrastructure and Range Limitations

Limited charging infrastructure represents a critical constraint on electric boat market growth, restricting operational flexibility and creating range anxiety among potential users. Unlike conventional boats that can refuel at widely available fuel stations, electric boats require dedicated charging facilities that remain sparse across popular boating destinations and marina networks.

Insufficient charging station availability leads to congestion and potential delays when multiple electric boat owners attempt to access the same charging points, particularly during peak boating seasons. Extended charging times compared to rapid fuel refilling further compound infrastructure limitations, requiring planning for longer excursions and reducing spontaneous boating opportunities.

Market Opportunities

Integration of Renewable Energy Sources and Solar Systems

Solar-electric boat technology creates substantial growth opportunities by enabling battery charging through renewable energy sources that align with global sustainability trends. Solar panels installed on boat decks or charging stations can harness abundant solar energy, while wind turbines and hydroelectric power offer additional renewable charging options. Recent product launches demonstrate market traction, including Navalt's introduction of India's fastest solar-electric boat, the Barracuda, featuring twin 50 kW motors and 6 kW solar panels.

Solar-electric boats deliver significant operational cost advantages, with users able to recover initial investments within four to five years through reduced fuel expenses and minimal maintenance requirements.

Emerging Market Expansion and Maritime Tourism Growth

Asia Pacific and emerging markets present exceptional growth opportunities driven by maritime tourism recovery, urbanization trends, and government infrastructure investments. India's marine electric vehicle market demonstrates this potential, growing from USD 186.50 million in 2024 to projected USD 427.47 million by 2033. Government initiatives such as India's Sagarmala Project emphasize port modernization and sustainability, creating demand for electric ferries and commercial vessels.

Maritime tourism sector recovery post-pandemic accelerates demand for sustainable boating experiences, with environmentally sensitive destinations and marine protected areas increasingly favoring electric boats for quiet, emission-free operations. Urban waterway transportation development, particularly in coastal Asian cities tackling pollution through green port initiatives, creates substantial commercial vessel electrification opportunities.

Category-wise Analysis

Boat Power Analysis

The >30kW segment dominates the electric boats market with 52.3% market share, reflecting strong demand for high-performance vessels capable of supporting luxury yachts, commercial ferries, and larger recreational boats.

This segment's leadership stems from commercial vessel electrification requirements and premium recreational boat demand, where power output directly correlates with performance capabilities and operational range. Professional operators in ferry services, water taxis, and commercial fishing prioritize higher power ratings to maintain competitive operational schedules and payload capacities comparable to traditional vessels.

The 5-30kW segment represents the fastest-growing category, driven by its optimal balance of performance, affordability, and charging infrastructure compatibility. This segment benefits from renewable energy charging capabilities, particularly solar power integration that reduces operational costs while extending practical range.

The 5-30kW category encompasses popular vessel types including leisure boats, fishing boats, and smaller commercial applications that serve diverse market needs while remaining accessible to broader consumer segments.

Boat Size Analysis

The <20ft segment commands 56.3% market share, reflecting the dominance of smaller recreational vessels, personal watercraft, and urban water taxi applications. Smaller boats benefit from lower battery requirements, reduced infrastructure demands, and greater operational flexibility in congested waterways and marina facilities. This segment particularly thrives in urban environments where shorter trips, frequent charging opportunities, and noise reduction requirements favor electric propulsion systems.

The 20-50ft segment emerges as the fastest-growing category, capturing demand from affluent recreational users and commercial operators seeking premium electric alternatives. This segment represents the sweet spot for luxury electric boats, offering sufficient space for advanced battery systems, comfortable amenities, and performance capabilities that rival traditional powerboats.

Commercial applications in this size range include water taxis, tour boats, and specialty vessels where electric propulsion provides competitive advantages in noise-sensitive environments and emission-controlled zones.

Power Source Analysis

Battery-powered systems dominate with 80.3% market share, reflecting mature lithium-ion technology, established supply chains, and proven performance in marine applications. Battery dominance stems from technological reliability, declining costs, and comprehensive charging infrastructure development that supports widespread adoption across recreational and commercial segments. Advanced battery management systems now offer sophisticated features including real-time monitoring, predictive maintenance, and integration with vessel control systems.

Hybrid systems represent the fastest-growing power source category, offering operational flexibility that addresses range limitations and charging infrastructure constraints. Hybrid propulsion combines electric motors with conventional engines, enabling extended range capabilities while maintaining zero-emission operation in sensitive environments. Major manufacturers like Brunswick Corporation and Groupe Beneteau actively invest in hybrid technologies, recognizing market demand for versatile propulsion solutions that bridge the transition from conventional to full-electric systems.

End-use Analysis

Recreational boats dominate with 54.3% market share, driven by environmentally conscious consumers seeking quieter, cleaner boating experiences. Recreational segment growth reflects premium market willingness to pay for advanced technology, enhanced user experience, and environmental sustainability benefits. High-profile manufacturers like Arc Boats successfully target affluent recreational users with luxury electric vessels featuring advanced technology and superior performance.

Commercial boats represent the fastest-growing end-use segment, propelled by regulatory compliance requirements, operational cost advantages, and government electrification mandates. Commercial applications include ferries, water taxis, harbor craft, and offshore support vessels where electric propulsion delivers immediate environmental and economic benefits. Public transportation electrification receives substantial government support, with funding programs and regulatory incentives accelerating commercial vessel conversion to electric systems.

Regional Market Insights

North America Electric Boats Market Trends

North America maintains market leadership with approximately 35% global market share, driven by robust recreational boating culture, advanced technology infrastructure, and supportive regulatory frameworks. The United States leads regional development with companies like Arc Boats, Pure Watercraft, and Tesla-inspired startups driving innovation in premium electric vessels.

California emerges as a critical innovation hub, hosting major manufacturers and early adopters who demonstrate market viability for luxury electric boats.

Regulatory support accelerates market expansion through state-level emission standards, marina electrification incentives, and clean transportation funding programs. The region benefits from established venture capital networks that provide substantial funding for electric boat startups, with Arc Boats raising over USD 100 million in total funding.

North American manufacturers focus on high-performance recreational vessels, targeting affluent consumers willing to pay premium prices for cutting-edge technology and environmental benefits. Strategic partnerships with technology companies leverage automotive electric vehicle expertise to accelerate marine propulsion development.

Europe Electric Boats Market Trends

Europe represents the second largest regional market, with strong environmental regulations, government support programs, and established maritime manufacturing expertise driving sustained growth. The European Union's Green Deal creates comprehensive regulatory framework mandating emission reductions that accelerate electric boat adoption across commercial and recreational segments. Germany, France, and the United Kingdom lead regional development through supportive policies, infrastructure investments, and domestic manufacturer capabilities.

Norwegian and Swedish companies pioneer advanced electric boat technology, with manufacturers like Silent Yachts and X Shore developing innovative solar-electric vessels that demonstrate European leadership in sustainable marine solutions.

Government incentive programs provide substantial financial support for electric boat purchases, charging infrastructure development, and research funding that accelerates technology advancement. European manufacturers emphasize luxury yacht electrification, targeting high-value segments where environmental benefits justify premium pricing.

Asia Pacific Electric Boats Market Trends

Asia Pacific emerges as the fastest-growing regional market, driven by rapid economic development, government electrification initiatives, and flourishing maritime tourism industry. China leads regional growth through strategic government guidelines for inland waterway transportation, substantial infrastructure investments, and domestic manufacturing capabilities. The region benefits from abundant renewable energy resources that support solar-electric boat development and sustainable charging solutions.

Maritime tourism growth across Southeast Asian countries creates substantial demand for electric boats in environmentally sensitive destinations where quiet, emission-free operation provides competitive advantages. Government support programs accelerate adoption through purchase incentives, infrastructure funding, and regulatory frameworks favoring clean transportation technologies. India represents significant growth potential with marine electric vehicle market expanding at 8.93% CAGR, supported by government initiatives like the Sagarmala Project.

Competitive Landscape

The global electric boats market demonstrates moderate fragmentation with numerous specialized manufacturers competing alongside established marine industry players entering the electrification space.

Leading companies maintain estimated market shares ranging from 5-15% individually, with no single player dominating the global market due to diverse applications, regional preferences, and technology specializations. Market concentration increases in premium segments where companies such as Arc Boats, Silent Yachts, and Candela command higher market shares through advanced technology and brand positioning.

Key Developments:

- In May 2025, Australian boatbuilder Incat launched Hull 096, the world’s largest battery-powered ship at 130 meters, designed for ferry service between Buenos Aires and Uruguay. Capable of carrying 2,100 passengers and 225 vehicles, it marks a milestone in sustainable electric shipping technology.

- In February 2025, Vision Marine Technologies deepened its partnership with Electrified Marina, a leading 100% electric watercraft dealer. This collaboration aims to expand adoption of Vision Marine's E-Motion electric propulsion technology, boosting the availability of high-performance electric boats on the East Coast.

Companies Covered in Electric Boats Market

- FRAUSCHER BOOTSWERFT GmbH & Co KG

- Duffy Electric Boat Company

- RAND Boats ApS

- Lillebror Marine

- Vision Marine Technologies

- Quadrofoil d.o.o.

- NAVAL DC B.V.

- LTSMARINE

- Symphony Boat Company,

- Ruban Bleu

- Nautique

- Correct Craft

- Other Market Players

Frequently Asked Questions

The Electric Boats market is estimated to be valued at US$ 4.1 Bn in 2025.

The key demand driver for the Electric Boats market is the global push toward sustainable and zero-emission maritime transportation.

In 2025, the Asia Pacific region will dominate the market with an exceeding 35% revenue share in the global Electric Boats market.

Among the Power Segment Type, 30kW segment holds the highest preference, capturing beyond 52.3% of the market revenue share in 2025, surpassing other Power Segment Type.

The key players in the Electric Boats market are Duffy Electric Boat Company, RAND Boats ApS, Lillebror Marine, Vision Marine Technologies and Quadrofoil.