- Biotechnology

- Cell Separation Market

Cell Separation Market Size, Trends, Share, Growth, and Regional Forecast, 2026 to 2033

Cell Separation Market by Product (Consumables, Kits and Reagents, Instruments, and Others), Cell Type (Human Cells and Animal Cells), by Method (Centrifugation, Surface Marker, and Filtration), Application (Biomolecule Isolation, Cancer Research, Stem Cell Research, Tissue Regeneration, In Vitro Diagnostics, and Others), End-user, and Regional Analysis from 2026 to 2033

Cell Separation Market Share and Trends Analysis

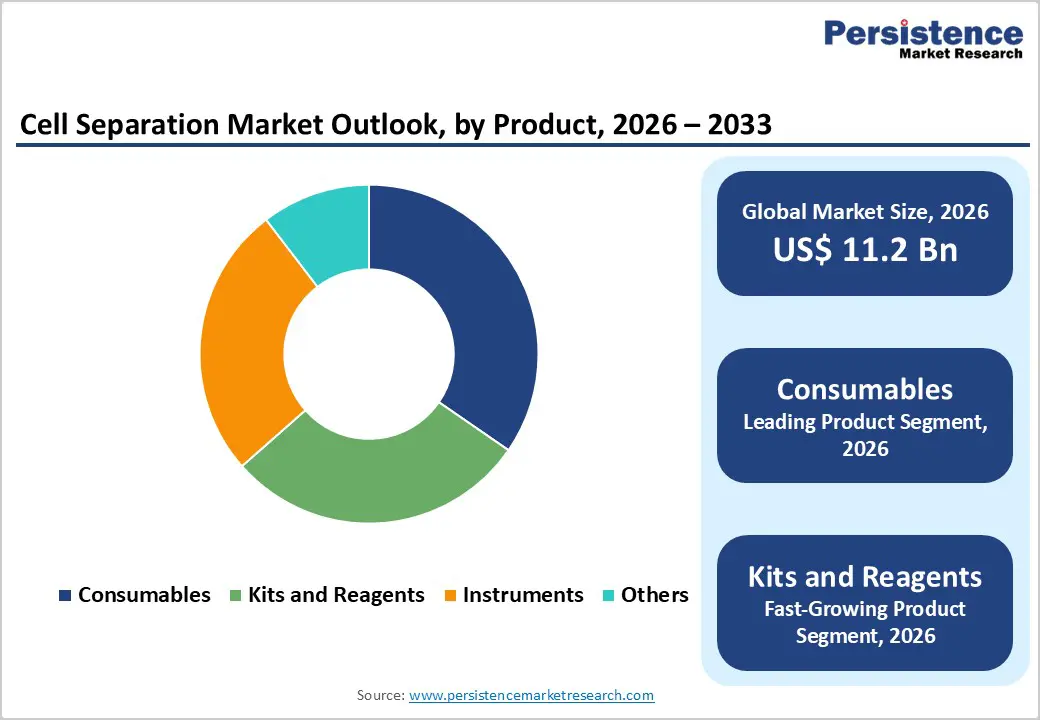

The global cell separation market size is estimated to grow from US$ 11.2 billion in 2026 to US$ 18.4 billion 2033. The market is projected to grow at a CAGR of 5.9% from 2026 to 2033.

Global demand for cell separation technologies is rising steadily, driven by the increasing prevalence of chronic diseases, cancer, autoimmune disorders, infectious diseases, and age-related conditions that require advanced cellular analysis and targeted therapeutic approaches. Growing volumes of clinical diagnostics, oncology testing, translational research, and cell-based therapy development are expanding the user base across hospitals, diagnostic laboratories, academic institutes, and biopharmaceutical manufacturing facilities.

The rapid expansion of cell and gene therapy pipelines is further increasing demand for high-purity, reproducible cell isolation solutions. Rising adoption of precision medicine and immunotherapy is accelerating the use of cell separation in biomarker discovery, immune profiling, and treatment monitoring. Advancements in separation technologies, including surface marker-based methods, automation, closed systems, and microfluidics, are improving accuracy, scalability, and workflow efficiency.

Key Industry Highlights:

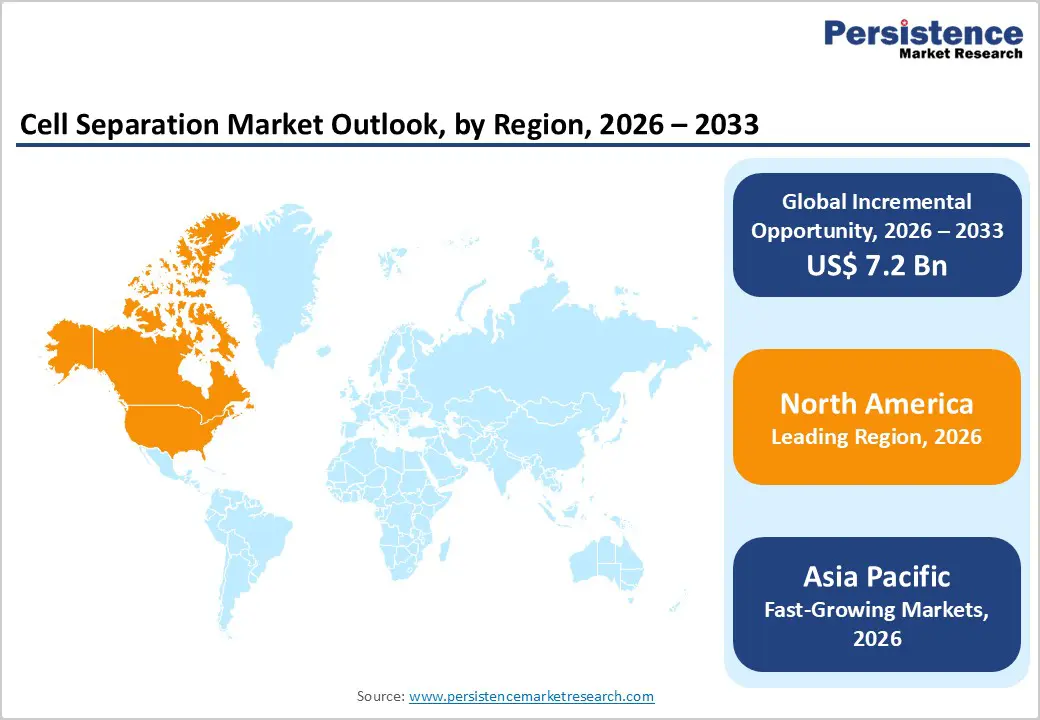

- Leading Region: North America holds the largest market share at 48.5%, supported by advanced research infrastructure, high prevalence of cancer and chronic diseases, strong funding for biomedical research, and early adoption of advanced cell separation technologies.

- Fastest-Growing Region: Asia Pacific is expanding at the fastest pace due to a large research and patient base, rapid growth of biotechnology and pharmaceutical manufacturing, expanding academic research activity, and increasing government investment in life sciences infrastructure.

- Leading Product Segment: Consumables dominate the market due to their recurring usage, essential role in routine cell separation workflows, and widespread adoption across research laboratories, hospitals, and biopharmaceutical production facilities.

- Fastest-Growing Product Segment: Kits and reagents are seeing rapid growth as demand rises for targeted nutritional management in chronic disease care, oncology, metabolic disorders, and home care settings.

- Leading Cell Type Segment: Human cells remain the largest usage segment due to their central role in clinical research, diagnostics, oncology studies, and therapeutic development.

- Fastest-Growing Cell Type Segment: Animal cells are expanding rapidly, driven by extensive use in preclinical research, toxicology studies, and drug discovery applications.

| Key Insights | Details |

|---|---|

| Cell Separation Market Size (2026E) | US$ 11.2 Bn |

| Market Value Forecast (2033F) | US$ 18.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Market Dynamics

Driver - Rising Chronic Disease Burden and Advancements in Cell-Based Research Driving Market Growth

The rising global burden of chronic and life-threatening diseases is a key driver accelerating demand for cell separation technologies. The increasing prevalence of cancer, autoimmune disorders, infectious diseases, cardiovascular conditions, and neurological disorders has significantly expanded the need for advanced cellular analysis, diagnostics, and therapeutic research. Cell separation is critical for isolating specific cell populations for disease profiling, biomarker discovery, immunophenotyping, and treatment monitoring. The growing adoption of cell-based assays in oncology, immunology, and regenerative medicine further reinforces market demand. In clinical settings, cell separation supports applications such as blood component analysis, immune cell characterization, and sample preparation for downstream molecular diagnostics. Additionally, the expansion of cell and gene therapy pipelines is increasing reliance on high-purity cell isolation to ensure safety, efficacy, and regulatory compliance.

Technological advancements in cell separation platforms are further strengthening market growth. Innovations such as magnetic-activated cell sorting, fluorescence-based separation, microfluidics, and automated closed systems are improving accuracy, throughput, and reproducibility. Enhanced reagents, surface marker specificity, and integration with downstream analytical tools are enabling more efficient workflows. These advancements reduce manual handling, contamination risks, and processing time, increasing adoption across research, diagnostic, and biopharmaceutical manufacturing environments. Collectively, the convergence of disease-burden growth and technological innovation continues to drive the sustained expansion of the global cell separation market.

Restraints - High Technology Costs and Operational Complexity Limiting Broader Adoption

The high cost associated with advanced cell separation technologies remains a significant restraint on market growth, particularly in resource-constrained settings. Sophisticated instruments, proprietary consumables, and specialized reagents required for high-precision separation often entail substantial capital and operating expenditures. Automated and surface-marker-based systems, while offering superior performance, command premium prices that can limit adoption among smaller laboratories, academic institutions with restricted funding, and healthcare facilities in emerging markets. In addition, recurring costs related to consumables, maintenance, and calibration further increase total cost of ownership. Limited reimbursement for advanced cellular diagnostics in some regions also constrains hospital-based adoption.

Operational complexity presents another challenge. Cell separation workflows often require skilled personnel, strict adherence to protocols, and controlled laboratory environments to ensure reliable outcomes. Errors in sample handling, marker selection, or processing conditions can compromise cell viability and purity, affecting downstream applications. In clinical and manufacturing settings, stringent regulatory requirements and validation processes lengthen implementation timelines and increase operational burdens. Additionally, variability in biological samples can impact separation efficiency, requiring optimization and repeated testing. These technical and economic barriers may lead some users to rely on conventional or lower-cost alternatives, thereby moderating overall market penetration and constraining the broader adoption of advanced cell separation technologies.

Opportunity - Expansion of Cell and Gene Therapy and Automation, Creating New Growth Avenues

The rapid expansion of cell and gene therapy development represents a major growth opportunity for the global cell separation market. Increasing investment in immunotherapies, stem cell therapies, and regenerative medicine is driving demand for highly efficient, scalable, and reproducible cell isolation solutions. Cell separation is a foundational step in manufacturing therapeutic cell products, requiring high purity, viability, and consistency to meet regulatory standards. As more therapies progress from clinical trials to commercialization, demand for GMP-compliant separation systems and consumables is expected to rise significantly. Growth in personalized medicine further supports this trend, as patient-specific therapies require precise and reliable workflows for cell processing.

Automation and integration of digital technologies present additional opportunities. Adoption of automated, closed-system cell separation platforms is increasing due to their ability to reduce contamination risk, labor dependency, and process variability. Integration with downstream analytical tools, data management systems, and process monitoring technologies supports scalability and compliance, particularly in biopharmaceutical manufacturing. Emerging markets also present untapped potential as governments invest in biotechnology infrastructure, research funding, and local manufacturing capabilities. Expanding academic-industry collaborations and the use of contract research and manufacturing organizations further accelerate technology adoption. Collectively, these trends are creating substantial long-term growth opportunities for cell separation solution providers globally.

Category-wise Analysis

By Product Insights

The consumables segment is projected to dominate the global cell separation market in 2026, accounting for a revenue share of 34.60%. Segment leadership is primarily driven by the recurring use of separation reagents, buffers, beads, columns, and disposable components across routine research and clinical workflows. Consumables are integral to cell separation protocols in academic laboratories, biotechnology and biopharmaceutical companies, diagnostic laboratories, and cell therapy manufacturing facilities. Their high replacement rate, batch-specific usage, and limited reusability ensure consistent demand irrespective of instrument lifecycles. Consumables are widely used across applications such as immunology research, oncology studies, stem cell isolation, and biomolecule extraction. Additionally, standardized consumable kits simplify workflows, reduce handling errors, and improve reproducibility, making them preferred in regulated and high-throughput environments. Growing adoption of automated and closed-system cell separation platforms further supports consumable demand, as many systems require proprietary reagents and disposables. Continuous improvements in reagent purity, separation efficiency, and compatibility with multiple cell types are reinforcing the dominant position of consumables within the global cell separation market.

By Application Insights

The biomolecule isolation segment is projected to dominate the global cell separation market in 2026, accounting for 29.70% of revenue. This leadership is driven by the widespread use of cell separation technologies in isolating DNA, RNA, proteins, and other cellular components for downstream molecular analysis. Biomolecule isolation is a foundational step in genomics, proteomics, transcriptomics, and biomarker discovery, supporting applications across academic research, pharmaceutical R&D, and clinical diagnostics. Increasing investment in precision medicine, oncology research, and infectious disease studies is significantly expanding demand for high-purity biomolecule extraction. Cell separation enables enrichment of target cell populations, improving sensitivity and accuracy in molecular assays. The rising adoption of next-generation sequencing, single-cell analysis, and advanced omics platforms further reinforces the importance of efficient cell separation in biomolecule workflows. Additionally, growth in translational research and companion diagnostics is increasing reliance on standardized and reproducible isolation techniques, solidifying biomolecule isolation as the largest application segment within the cell separation market.

By End-user Insights

The hospital segment is projected to dominate the global cell separation market in 2026, accounting for 24.90% of revenue. Hospitals serve as major demand centers due to their role in diagnostic testing, oncology treatment, hematology, and emerging cell-based therapeutic procedures. Cell separation technologies are increasingly used in hospital laboratories for applications including blood component separation, immune cell analysis, cancer diagnostics, and cell preparation for downstream testing. Large patient volumes, centralized laboratory infrastructure, and availability of trained clinical personnel support sustained utilization. Hospitals are also at the forefront of adopting advanced diagnostic workflows, including flow cytometry-based cell sorting and surface marker-based separation techniques. While academic institutes and biopharmaceutical companies contribute significantly to research-driven demand, hospitals maintain leadership due to their integration of diagnostic and therapeutic services. Continued investments in hospital laboratory modernization, precision diagnostics, and translational medicine programs are expected to reinforce hospital dominance within the global cell separation market.

Region-wise Insights

North America Cell Separation Market Trends

The North American cell separation market is expected to dominate globally, with a 48.5% value share in 2026, led primarily by the United States. The region benefits from a highly advanced life sciences ecosystem, strong biotechnology and biopharmaceutical presence, and widespread adoption of advanced research and diagnostic technologies. High levels of funding for biomedical research, cancer studies, and cell-based therapies are driving sustained demand for cell separation solutions across academic institutions, hospitals, and industry laboratories.

North America demonstrates strong adoption of automated, high-throughput, and surface-marker-based separation technologies, supported by well-established laboratory infrastructure and a skilled workforce. The presence of leading market players, robust clinical trial activity, and ongoing innovation in cell therapy and immuno-oncology further strengthen the region's leadership. Additionally, favorable regulatory frameworks and early adoption of precision medicine approaches are accelerating the integration of cell separation into routine workflows. Growth in translational research and hospital-based diagnostics continues to reinforce North America’s dominant position in the global market.

Europe Cell Separation Market Trends

The European cell separation market is expected to grow steadily, supported by strong academic research networks, expanding biopharmaceutical manufacturing, and an increasing focus on advanced diagnostics. Countries such as Germany, the U.K., France, Italy, and the Nordic nations are key contributors owing to well-developed research infrastructure and public health care systems. European laboratories emphasize standardized workflows, quality assurance, and regulatory compliance, supporting consistent adoption of cell separation technologies. The rising prevalence of cancer and immune-related disorders is increasing demand for cell-based research and diagnostic applications.

The region shows growing utilization of surface marker-based and filtration-based separation methods aligned with precision medicine initiatives. Expansion of cell and gene therapy research, supported by government and EU-level funding programs, is further driving market growth. Additionally, increasing collaboration between academic institutions and biopharmaceutical companies is accelerating technology transfer and adoption. Despite pricing pressures within public healthcare systems, sustained investments in research, diagnostics, and advanced therapies are expected to support long-term market expansion across Europe.

Asia Pacific Cell Separation Market Trends

The Asia Pacific cell separation market is expected to register a relatively higher CAGR of around 7.9% between 2026 and 2033, driven by the rapid expansion of healthcare and research infrastructure across the region. Countries including China, India, Japan, South Korea, and Southeast Asian nations are witnessing increasing investment in biotechnology, pharmaceutical manufacturing, and academic research. The rising incidence of cancer, infectious diseases, and chronic conditions is driving demand for advanced diagnostic and research tools, including cell separation technologies.

Government initiatives supporting life sciences research, laboratory modernization, and domestic biopharmaceutical production are accelerating market adoption. The growth of private hospitals, contract research organizations, and clinical laboratories is improving accessibility to advanced cell separation platforms. Increasing awareness among researchers and clinicians, along with improving the affordability of consumables and instruments, is further supporting uptake. The expansion of cell therapy research and precision medicine initiatives is expected to sustain strong long-term growth in the Asia-Pacific cell separation market.

Market Competitive Landscape

The global cell separation market is highly competitive, with strong participation from companies such as Thermo Fisher Scientific, Inc., BD, Danaher, Terumo Corp., and STEMCELL Technologies Inc. These players leverage broad cell separation and analysis portfolios, strong relationships with academic research institutes, biotechnology and biopharmaceutical companies, advanced manufacturing capabilities, and extensive global distribution networks.

Competitive strategies focus on expanding application-specific cell separation solutions, enhancing accuracy, purity, and scalability of separation technologies, and supporting research and clinical workflows across cell therapy, oncology, and regenerative medicine. Continuous product innovation, clinical and research validation, user training initiatives, and geographic expansion into emerging markets continue to intensify competition and drive market evolution.

Key Developments:

- In September 2025, Cayman Chemical, a global provider of life science research tools, and Akadeum Life Sciences, a leader in buoyancy-based cell separation technology, announced a distribution partnership aimed at expanding access to Akadeum’s next-generation cell isolation solutions for cell and gene therapy development.

- In January 2025, Akadeum Life Sciences® reported strong outcomes from its early access program for the Alerion™ Microbubble Cell Separation System, validating the platform as a high-capacity, rapid, and gentle cell isolation solution. The program demonstrated exceptional performance and robust customer support, driving multiple purchase requests and creating a two-to-three-week demonstration waitlist. These results highlight Alerion™’s potential to significantly accelerate process efficiency and scalability in cell therapy manufacturing.

- In October 2023, Akadeum Life Sciences, a global leader in buoyancy-based cell separation technology, announced a preview of its Alerion™ cell separation system. The platform is designed as a closed system for isolating T cells from leukopaks using Akadeum’s proprietary Buoyancy Activated Cell Sorting (BACS) microbubble technology. The system is expected to accelerate separation workflows, enhance cell recovery, automate multiple manual steps, improve processing consistency, reduce user-related variability, and minimize cell stress and exhaustion during isolation.

Companies Covered in Cell Separation Market

- Thermo Fisher Scientific, Inc.

- BD

- Danaher

- Terumo Corp.

- STEMCELL Technologies Inc.

- Bio-Rad Laboratories, Inc.

- Merck KGaA

- Agilent Technologies, Inc.

- Corning Inc.

- Akadeum Life Sciences

- Miltenyi Biotec

- Others

Frequently Asked Questions

The global cell separation market is projected to be valued at US$ 11.2 Bn in 2026.

The global cell separation market is driven by the increasing prevalence of chronic diseases requiring cell-based therapies and diagnostics, rising R&D investment in biotechnology and pharmaceutical sectors, growing demand for personalized medicine and immunotherapy, and continuous technological advancements in cell separation methods that improve efficiency and accuracy.

The global cell separation market is poised to witness a CAGR of 5.9% between 2026 and 2033.

Significant opportunities exist in emerging markets with expanding biotech infrastructure and in the development of automated, AI-integrated cell separation technologies.

Thermo Fisher Scientific, Inc., BD, Danaher, Terumo Corp., and STEMCELL Technologies Inc. are some of the key players in the cell separation market.