- Biotechnology

- North America Induced Pluripotent Stem Cells Market

North America Induced Pluripotent Stem Cells Market Size, Share, and Growth Forecast, 2025 - 2032

North America Induced Pluripotent Stem Cells Market By Product Type (Instruments/Devices, Reagents & Kits, Services), Cell Type (Autologous, Allogeneic), Application (Drug Development, Regenerative Medicine, Others), by End-user, and Country Analysis from 2025 - 2032

North America Induced Pluripotent Stem Cells Market Size and Trends Analysis

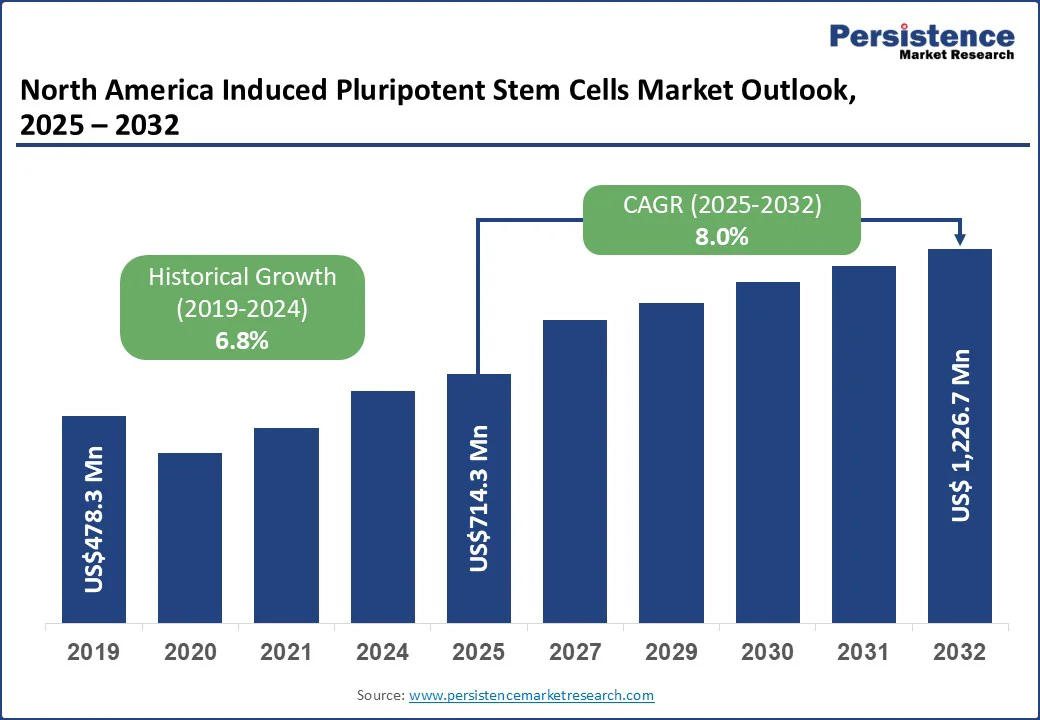

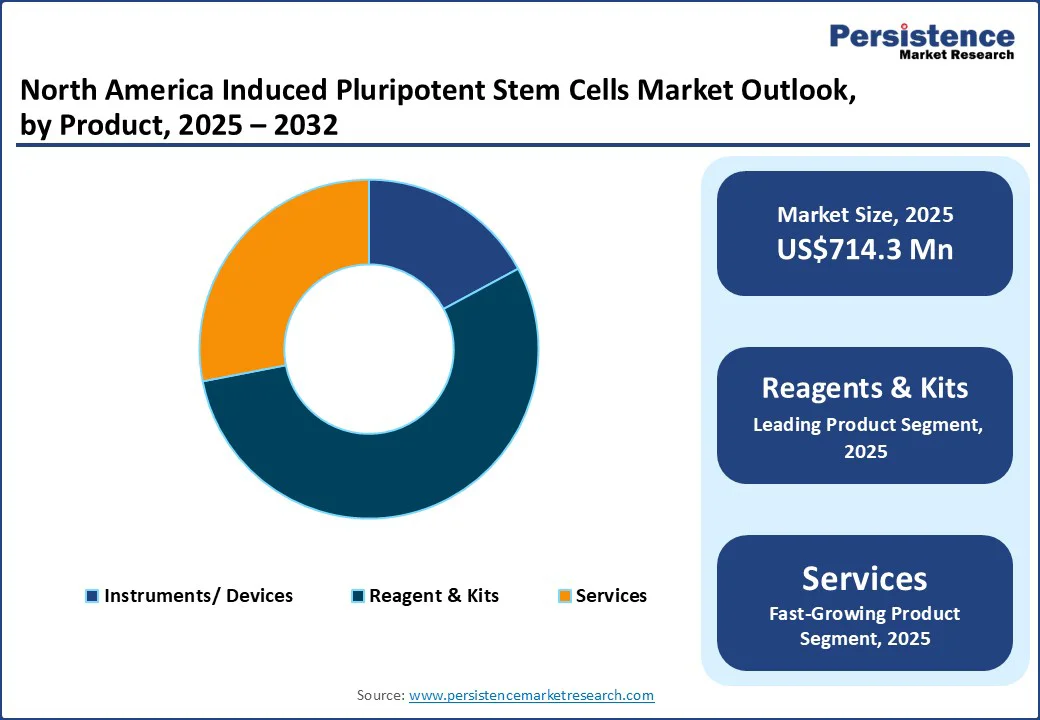

The North America induced pluripotent stem cells market size is likely to be valued at US$714.3 Mn in 2025 and is expected to reach US$1,226.7 Mn by 2032, growing at a CAGR of 8.0% during the forecast period from 2025 to 2032, driven by a strong biotechnology and pharmaceutical sector, particularly in the U.S., which leads in clinical trials, R&D investment, and therapeutic innovation. The region benefits from advanced infrastructure, high healthcare spending, and a growing demand for personalized medicine and regenerative therapies.

Key Industry Highlights

- Leading Country: The U.S. leads the North America induced pluripotent stem cells market, driven by its advanced biotechnology infrastructure, high R&D investments, and strong presence of pharmaceutical and academic institutions.

- Fastest-Growing Product Segment: Consumables & Kits are the fastest-growing product category, due to their essential role in disease modeling, drug testing, and streamlined iPSC production processes.

- Fastest-Growing Application Segment: Drug Development is the most rapidly expanding application area, fueled by demand for personalized therapies and the ability of iPSCs to replicate disease-specific genotypes.

- Investment Plans: The U.S. government, through agencies including the NIH, has committed billions of dollars to stem cell research, including iPSCs, to support regenerative medicine and personalized therapies.

| Key Insights | Details |

|---|---|

|

Induced Pluripotent Stem Cells Market Size (2025E) |

US$714.3 Mn |

|

Market Value Forecast (2032F) |

US$1,226.7 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

8.0% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Shift toward Human-Relevant Preclinical Testing Driving iPSC Adoption in North America

One of the main drivers of the North America induced pluripotent stem cells market, especially the U.S., is the growing focus on human-relevant preclinical testing. Regulatory authorities, including the FDA, are promoting alternative testing approaches that more accurately replicate human biology, reducing dependence on animal models. iPSC-derived cell types such as cardiomyocytes, hepatocytes, and neurons offer high physiological fidelity and can capture patient-specific genetic variations, making them ideal for in vitro toxicology, ADME studies, and disease modeling.

Pharmaceutical companies are increasingly adopting iPSC-based platforms in early-stage drug development to detect toxicity early, improve candidate selection, and lower late-stage failure rates. Additionally, the EPA’s plan to eliminate animal testing by 2035 further reinforces demand for scalable, standardized, and quality-assured iPSC products and services, including off-the-shelf assay-ready cell lines and custom differentiation solutions. This shift has led to rising adoption of commercial iPSC solutions by CROs and pharma R&D units across the region.

High Cost of Custom iPSC Products Restricts Adoption among Smaller Research and Academic Institutions

The growing complexity of highly specialized iPSC workflows, such as making patient-specific cells, detailed quality checks, and creating custom assays, has pushed up the cost of iPSC products and services. This creates limitations, particularly for small labs, universities, and early-stage biotech companies that often work with limited budgets.

For example, creating a research-grade iPSC line can cost between US$10,000 and 25,000 and take up to six to nine months, while clinical-grade lines are even more expensive. Owing to these high prices, many groups avoid large-scale or exploratory studies, even though demand is rising for ready-to-use cell lines and advanced custom differentiation services. In the U.S., core facilities often charge more than US$4,800 just to make a few iPSC lines, and extra fees apply for testing or expansion. These costs pose a big entry barrier for smaller groups and slow down the growth of iPSC-based research in North America.

Academic-Industry Partnerships and CRO Expansion Driving iPSC Commercialization in North America

The rapid expansion of contract research organizations (CROs) and a robust academic research ecosystem in North America provide a substantial growth opportunity for the induced pluripotent stem cell (iPSC) market. Biotech and pharmaceutical companies increasingly outsource iPSC-based disease modeling, cell line development, and early-phase trials to CROs, enabling accelerated research without the need for heavy infrastructure investments.

At the same time, leading academic institutions and hospitals actively collaborate with industry partners to translate basic research into commercially viable therapies and drug testing platforms. The U.S. National Institutes of Health (NIH), the world’s largest public biomedical research funder, distributes over US$31 Bn annually across more than 2,500 institutions, supporting innovations in iPSC technology. These collaborations foster standardized protocols, assay-ready cell lines, and scalable differentiation platforms, driving wider adoption in preclinical research, drug discovery, and regenerative medicine applications, and positioning North America as a global hub for iPSC commercialization.

Category-wise Analysis

Product Type Insights

In the North America induced pluripotent stem cells market, reagents and kits represent the largest product segment, driven by their widespread use in stem cell reprogramming, differentiation, expansion, and cryopreservation. Academic institutes, biotechnology firms, and pharmaceutical companies rely heavily on standardized reagents and ready-to-use kits to streamline workflows, ensure reproducibility, and minimize the time required for complex iPSC experiments.

The growing adoption of iPSC platforms for drug discovery, toxicity screening, and disease modeling further strengthens demand for high-quality, assay-ready kits. Moreover, increasing research funding in the U.S. from agencies such as the National Institutes of Health (NIH) supports broader adoption across both basic and translational research. As CROs and pharma R&D centers continue expanding iPSC applications, the reagents and kits category is expected to maintain its dominance, reinforcing North America’s leadership in iPSC commercialization.

Cell Type Insights

The allogeneic cell type segment holds the leading share in the induced pluripotent stem cells (iPSC) market, supported by its scalability, cost-effectiveness, and its suitability for standardized therapeutic applications. Unlike autologous approaches, which require patient-specific processing, allogeneic iPSCs can be generated in bulk, stored, and distributed as off-the-shelf cell therapies, reducing turnaround times and overall expenses. This makes them particularly attractive for regenerative medicine, oncology, and cardiovascular research, where timely access to high-quality cells is critical.

In North America, strong research infrastructure and supportive funding drive advancements in allogeneic platforms, with multiple biotech firms focusing on creating iPSC-derived allogeneic cell banks. The ability to serve a broader patient population while ensuring consistent quality positions the allogeneic segment as the dominant driver of commercial iPSC applications.

Country Insights

U.S. Induced Pluripotent Stem Cells Market Trends

Over recent years, traditional drug toxicity screening faced challenges due to limited access to human samples, relying heavily on immortalized cell lines or animal models. The advent of iPSC technology has transformed this landscape by providing a consistent supply of functional human cells for preclinical drug screening. iPSCs enable patient-specific disease modeling, ushering in a “micromedicine” era that allows researchers to study disease progression at an individual level and identify optimal therapeutic interventions for each patient.

Simultaneously, iPSC platforms support “macromedicine”, enabling high-throughput analyses of drug toxicity and efficacy across patient cohorts using differentiated functional cells, such as iPSC-derived cardiomyocytes. Another emerging trend is patient stratification, where iPSCs help identify biomarkers in drug responders, improving clinical trial success rates by selecting patients most likely to benefit. Collectively, these trends highlight how iPSC technology is reshaping preclinical and clinical research in the U.S., reducing development costs, mitigating risk, and accelerating both personalized and population-level therapies.

Competitive Landscape

The North America iPSC market is shaped by continuous innovation and strategic collaborations. Leading companies such as FUJIFILM Cellular Dynamics, Thermo Fisher Scientific Inc., Lonza, and Sartorius AG are pushing the boundaries of stem cell therapies. Pharmaceutical and biotech firms hold a dominant share, while academic institutions are increasingly contributing to research. The market is further influenced by mergers, licensing agreements, and the development of clinical-grade iPSCs, reinforcing the region’s strong position in regenerative medicine.

Key Industry Developments

- In April 2025, Thermo Fisher Scientific launched its Advanced Therapies Collaboration Center in Greater San Diego to accelerate the development of cell therapies.

- In April 2025, Hitachi, in collaboration with the CiRA Foundation of Kyoto University, plans to launch a demonstration project at the Yanai Facility for my iPS Cell Therapy. The initiative focuses on developing enclosed automated culture systems to reduce manufacturing costs for iPS cell-based therapies.

- In September 2024, FUJIFILM Cellular Dynamics, a prominent global developer and manufacturer of human induced pluripotent stem cells (iPSCs), announced the worldwide commercial launch of its human iPSC-derived iCell® Sensory Neurons. These neurons are designed to support scientists working in neuroscience research, novel pain drug discovery, and neurotoxicity side effect analysis.

Companies Covered in North America Induced Pluripotent Stem Cells Market

- FUJIFILM Holdings Corporation (Cellular Dynamics)

- Thermo Fisher Scientific, Inc.

- Hitachi Ltd.

- Lonza

- Terumo Corporation

- Miltenyi Biotec

- Takara Bio Inc.

- Sartorius AG

- Merck KGaA

- Horizon Discovery Group plc.

- Cell Applications, Inc

Frequently Asked Questions

The North America induced pluripotent stem cells market is projected to be valued at US$714.3 Mn in 2025.

Growing demand for personalized medicine, advancements in regenerative therapies, and increased R&D funding drive market growth in North America.

The North America induced pluripotent stem cells market is poised to witness a CAGR of 8.0% between 2025 and 2032.

Expansion in disease modeling, drug discovery, and cell therapy applications, along with rising collaborations between biotech firms and research institutions, present major growth opportunities.

Major players in the North America induced pluripotent stem cells market are FUJIFILM Holdings Corporation (Cellular Dynamics), Thermo Fisher Scientific Inc., Lonza, and Sartorius AG.