- Animal Health

- Canine Stem Cell Therapy Market

Canine Stem Cell Therapy Market Size, Share, Growth, and Regional Forecast, 2025 to 2032

Canine Stem Cell Therapy Market by Product (Allogeneic Stem Cells, Autologous Stem cells), Application (Arthritis, Dysplasia, Tendonitis, Lameness, Others), End-user and Regional Analysis from 2025 to 2032

Canine Stem Cell Therapy Market Share and Trends Analysis

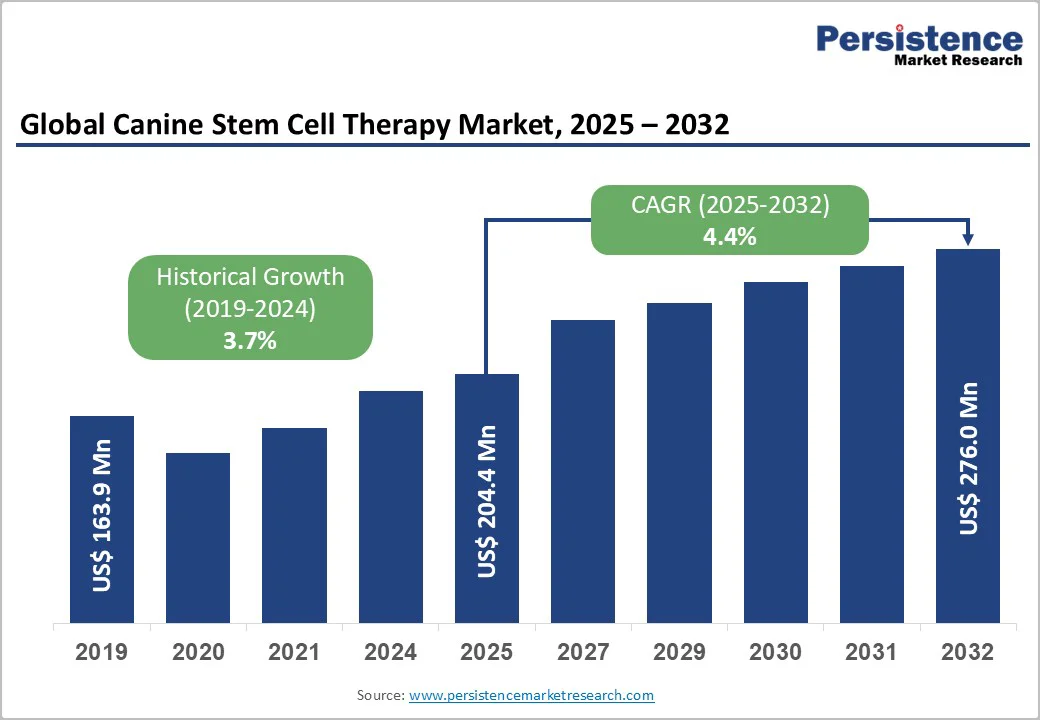

The global canine stem cell therapy market size is valued at US$204.4 million in 2025 and is projected to reach US$276.0 million by 2032, growing at a CAGR of 4.4% between 2025 and 2032. Stem cells are the body’s natural repair system, uniquely capable of self-renewal and transforming into specialized cell types such as muscle, nerve, or blood cells.

This regenerative ability makes them vital for repairing damaged tissues and restoring organ function. Beyond their fundamental biological role, stem cells have become a cornerstone of modern regenerative medicine, offering new hope for treating chronic and degenerative diseases.

Thousands of clinical trials worldwide are actively exploring their therapeutic potential, ranging from orthopedic and neurological disorders to innovative applications in both human and veterinary healthcare.

Key Industry Highlights

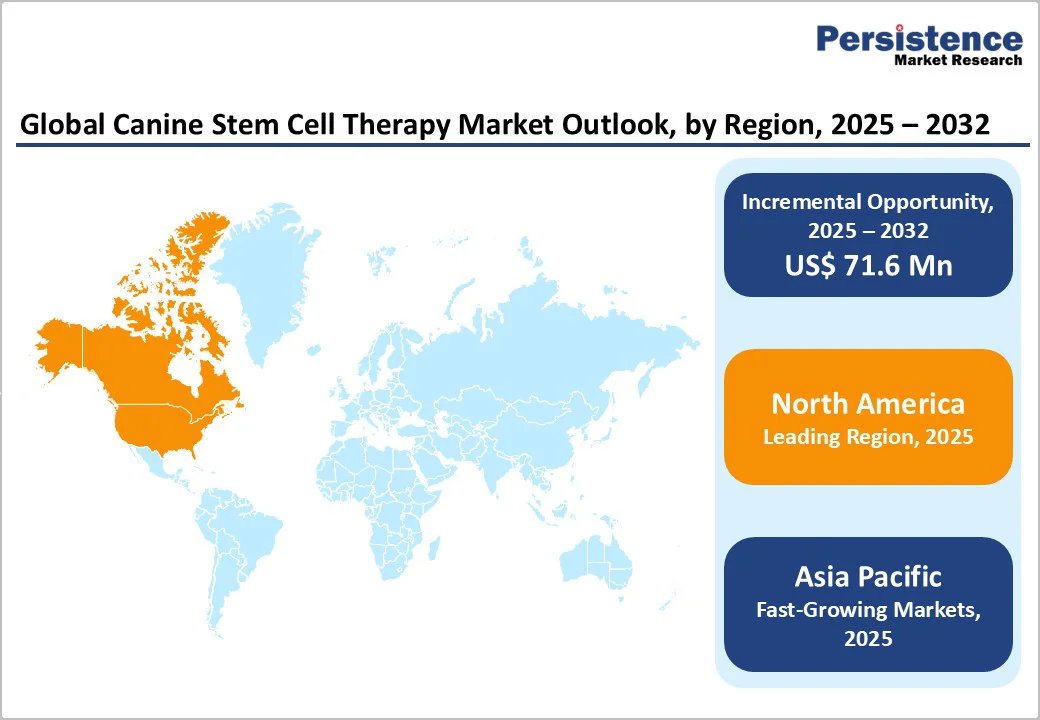

- Leading Region: North America dominates the global market, accounting for 44.2%, driven by strong R&D investment, higher pet healthcare spending, and advanced regulatory and clinical infrastructure.

- Fastest-Growing Region: The Asia Pacific market is expected to grow rapidly with a CAGR of 5.5% in the forecast period, fueled by rising pet ownership, expanding veterinary networks, and emerging biotech startups.

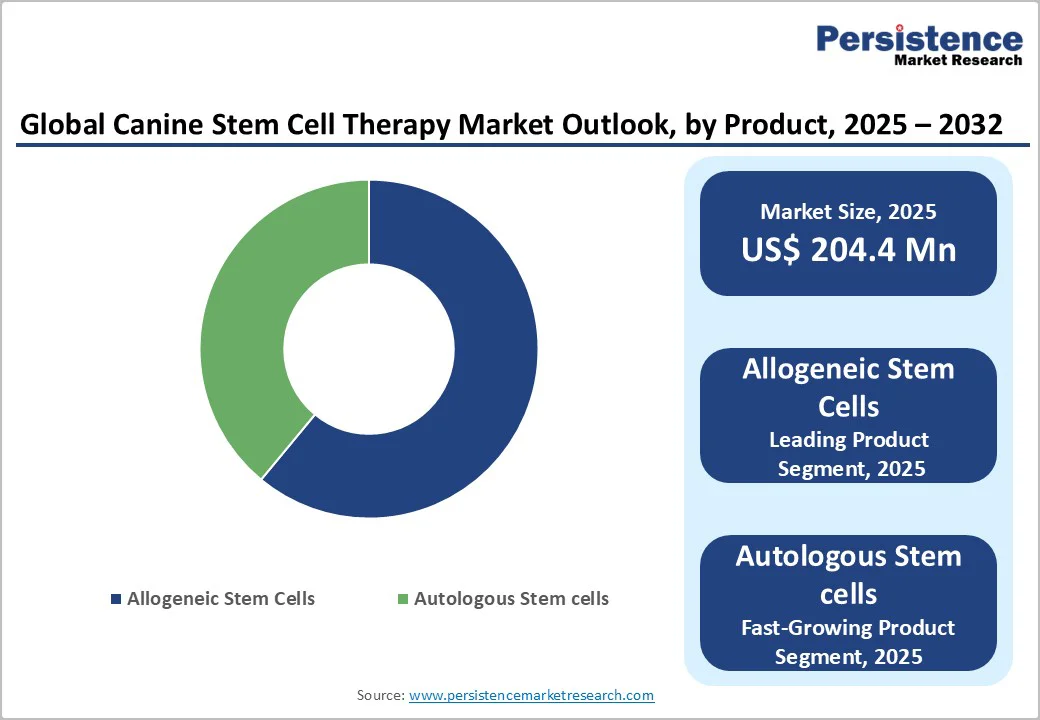

- Leading Product: Allogeneic stem cells lead with 61.2% share, supported by scalability, off-the-shelf availability, and easier logistics versus autologous approaches.

- Leading Application: Arthritis dominates, at 43.2%, driven by the high prevalence of osteoarthritis in companion animals and proven clinical improvements from cell therapies.

- Leading End-user: Veterinary hospitals remain dominant, driven by established clinical expertise, access to specialized equipment, and integrated care pathways for advanced treatments.

- Rising adoption of regenerative therapies reflects pet owners’ shift toward advanced, minimally invasive treatments.

- Emerging veterinary biotech startups accelerate innovation and commercial expansion across global markets.

- Academic-industry collaborations strengthen research and clinical translation in veterinary regenerative medicine

| Key Insights | Details |

|---|---|

| Canine Stem Cell Therapy Market Size (2025E) | US$204.4 Million |

| Market Value Forecast (2032F) | US$276.0 Million |

| Projected Growth (CAGR 2025 to 2032) | 4.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.7% |

Market Dynamics

Driver - Advancing Veterinary Innovation and Rising Demand for Regenerative Pet Therapies

The global canine stem cell therapy market is gaining strong momentum, driven by robust clinical evidence, rising investment, and increasing focus on chronic pet diseases. Multiple clinical studies have demonstrated the therapeutic potential of mesenchymal stem cells (MSCs) in managing canine osteoarthritis (OA)-one of the most prevalent degenerative conditions in dogs.

In a study involving 203 dogs with OA, both intra-articular and intravenous allogenic MSC treatments led to significant improvements within 10 weeks, as assessed by veterinary assessments. Another trial with 245 dogs unresponsive to conventional therapies also showed statistically significant improvements across all clinical evaluation periods, reinforcing the efficacy of autologous MSCs.

Similarly, a randomized, blinded, multicenter trial found that 18 dogs treated with adipose-derived stem cells had markedly better lameness, pain, and mobility scores than controls.

On the innovation front, in January 2024, Gallant Therapeutics raised over US$15 million in Series A funding to accelerate its pipeline of off-the-shelf stem cell therapies for pets.

The company is targeting FDA approval for its lead candidate addressing Feline Chronic Gingivostomatitis (FCGS) while also advancing treatments for OA, chronic kidney disease (CKD), and atopic dermatitis (AD). Together, these advancements highlight the market’s shift toward scalable, evidence-backed, and accessible regenerative solutions in veterinary care.

Restraints - High Costs, Limited Data, and Regulatory Gaps Hampering Market Expansion

The global canine stem cell therapy market continues to face several key restraints despite growing research interest and clinical promise. The high cost of stem cell therapy remains a primary barrier, limiting accessibility for average pet owners and restricting wider adoption in general veterinary practice.

Additionally, the short shelf life and complex storage requirements of live cell products add significant logistical challenges, especially in maintaining viability during transport and administration.

Scientific limitations further constrain progress. Studies have highlighted the lack of standardized protocols, variable treatment outcomes, and insufficient long-term safety data, making it difficult to establish consistent therapeutic benchmarks. Regulatory oversight also varies widely across countries, leading to uncertainty regarding quality control, ethical sourcing, and product approval processes.

Experts from veterinary research bodies emphasize that translation from laboratory success to consistent clinical efficacy in pets has been slower than anticipated. Many veterinarians remain cautious due to these knowledge gaps, limited training, and the need for stronger evidence-based guidelines.

As a result, despite encouraging advances in regenerative medicine, the combination of high cost, regulatory ambiguity, and limited scalability continues to restrain the global canine stem cell therapy market’s growth potential.

Opportunity - Expanding Scope of Regenerative and Cellular Therapies in Animal Health

The global canine stem cell therapy market presents significant growth opportunities, driven by the rising demand for alternative treatments in conditions where conventional therapies have limited success. Mesenchymal stem cells (MSCs) have emerged as a key innovation in regenerative veterinary medicine, offering the ability to repair and regenerate damaged tissues.

Their versatility, being easily derived from various tissues and capable of differentiating into multiple cell types, makes MSCs a highly adaptable therapeutic tool for a broad range of canine diseases.

Therapies based on MSCs are increasingly being explored for spinal cord injuries, chronic wounds, and skin and ocular diseases, with encouraging clinical outcomes. Although the effectiveness of MSC-based therapies can vary depending on numerous biological and procedural factors, ongoing research continues to expand understanding and optimize treatment protocols.

A major opportunity lies in integrating advanced cellular platforms. For example, in November 2023, a pioneering clinical trial was launched at Colorado State University (CSU) to test CAR T-cell therapy in dogs with solid tumors.

This novel immunotherapy, successful in human leukemia and lymphoma cases, is being adapted for canine oncology, marking a new frontier in precision veterinary medicine. Together, these advancements underscore vast untapped potential for next-generation cell and gene-based therapies in animal health.

Category-wise Analysis

By Product: Allogeneic Stem Cells Dominate Owing to Scalability, Accessibility, and Simplified Clinical Use

Allogeneic stem cells are expected to capture a leading 61.2% share of the global canine stem cell therapy market by 2025. Their dominance is driven by the ease of large-scale production, immediate availability, and standardized quality compared to autologous cells.

Unlike patient-derived cells that require individualized processing, allogeneic stem cells can be stored and administered “off the shelf,” reducing turnaround time and costs. This scalability supports broader clinical adoption, enabling veterinarians to deliver consistent, high-quality regenerative treatments across diverse patient populations.

By Application: Arthritis Lead Due to High Prevalence and Proven Therapeutic Response to Regenerative Treatments

Arthritis is projected to dominate the global canine stem cell therapy market in 2025, accounting for around 43.2% of the total share. The growing incidence of osteoarthritis among aging dogs, affecting millions globally, has created strong demand for effective, non-surgical interventions.

Stem cell therapy offers pain relief, improved mobility, and cartilage regeneration, showing measurable success in clinical trials. As pet owners increasingly seek long-term, minimally invasive solutions to chronic joint pain, arthritis remains the most widely targeted condition in veterinary regenerative medicine.

By End-user: Veterinary Hospitals Lead Owing to Specialized Infrastructure and Integrated Regenerative Treatment Capabilities

Veterinary hospitals are expected to maintain dominance in the canine stem cell therapy market, holding approximately 54.1% share by 2025. Their leadership stems from access to advanced facilities, skilled specialists, and the ability to manage complex regenerative procedures safely.

These hospitals serve as primary centers for clinical trials, stem cell processing coordination, and post-treatment care. Additionally, increasing collaborations between hospitals and biotechnology firms are strengthening in-house expertise, ensuring higher treatment success rates and patient satisfaction. This integrated care ecosystem continues to position veterinary hospitals as key drivers of market adoption.

Regional Insights

North America Canine Stem Cell Therapy Market Trends

By 2025, North America is projected to command around 44.2% of the global canine stem cell therapy market, driven by rising pet healthcare spending and the growing prevalence of osteoarthritis in dogs. In the U.S. alone, nearly 14 million adult dogs suffer from osteoarthritis, making it one of the most common and concerning pet health issues.

Additionally, about 90% of cats over 12 years old show X-ray signs of osteoarthritis, underscoring the expanding need for advanced regenerative treatments.

In February 2024, VetStem, Inc., a leader in regenerative veterinary medicine, marked a milestone by processing over 16,000 patient samples and delivering 38,000 stem cell treatments across North America. Meanwhile, innovation continues to accelerate. In July 2025, Gallant, a U.S.-based startup founded by Aaron Hirschhorn, raised $18 million to develop the first FDA-approved, off-the-shelf stem cell therapy for pets, with approval expected in early 2026.

Similarly, in October 2025, The Jackson Laboratory acquired the New York Stem Cell Foundation, strengthening research capabilities and fostering translational breakthroughs in stem cell and AI-based therapies. Together, these developments highlight North America’s strong ecosystem of funding, research, and innovation, driving rapid adoption of stem cell-based solutions in veterinary care.

Europe Canine Stem Cell Therapy Market Trends

By 2025, Europe is expected to account for around 26.1% of the global canine stem cell therapy market, supported by a growing companion animal population, robust veterinary infrastructure, and rising adoption of novel biotherapeutics.

Governments across the region are promoting veterinary health initiatives and research collaborations to advance ethical and evidence-based use of regenerative therapies.

The AO VET-ARI Collaborative Research Grants program exemplifies this progress, focusing on training grants for young investigators, structured mentorship, and innovative surgical courses that reinforce best practices in preclinical animal research. AO VET also serves as a key resource in ensuring the most ethical use of animals in research across Europe.

A major milestone came in January 2023, when TVM launched DogStem, the first licensed stem cell treatment for canine osteoarthritis (OA) in Europe. Designed for mild to severe OA, DogStem delivers lasting efficacy of over 12 months following a single injection, eliminating the need for surgical harvesting under general anesthesia.

This ready-to-use innovation has widened access to regenerative care in veterinary practices that previously faced procedural and licensing barriers. Together, such regulatory backing, ethical research frameworks, and groundbreaking product launches continue to position Europe as a leading hub for veterinary stem cell innovation.

Asia Pacific Canine Stem Cell Therapy Market Trends

The Asia-Pacific canine stem cell therapy market is experiencing robust growth and is projected to grow at a CAGR of 5.5% over the forecast period. Growth is being fueled by the emergence of veterinary biotechnology startups, the expansion of clinical infrastructure, and rising awareness of regenerative medicine’s benefits among veterinarians and pet owners alike.

Countries such as Japan, South Korea, China, and Australia are leading innovation in animal health research, with increasing investments in veterinary R&D and biotherapeutic development. Local startups are driving the commercialization of stem cell-based therapies for conditions such as osteoarthritis and ligament injuries, offering more affordable and accessible alternatives to traditional treatments.

Meanwhile, the rapid expansion of veterinary service networks-including specialty clinics and animal rehabilitation centers-has made advanced treatments more widely available across urban centers.

Additionally, growing pet ownership rates, particularly in India and Southeast Asia, coupled with rising disposable incomes, are strengthening market demand. Supportive government programs promoting animal welfare and research collaborations between academia and industry are also enhancing innovation pipelines.

Together, these trends underscore Asia Pacific’s increasing role as a dynamic growth hub for canine regenerative therapies, driven by innovation, accessibility, and a shifting cultural emphasis toward advanced pet healthcare.

Competitive Landscape

The global canine stem cell therapy market is moderately competitive with companies focusing on product innovation, clinical validation, and partnerships with veterinary hospitals to expand access. Emerging biotech firms in Asia-Pacific are also intensifying regional competition through cost-effective solutions.

Key Industry Developments:

- In October 2025, PetGeneX, in partnership with Thailand’s National Innovation Agency (NIA), launched the nation’s first stem cell bank for pets, offering ISO-certified collection and preservation services to support long-term regenerative healthcare and enhance pets’ lifespan and well-being.

- In June 2024, the FDA approved clinical trials at Cornell University Hospital for Animals (CUHA) to study stem cell therapy for musculoskeletal and neurological disorders in dogs and horse.

Companies Covered in Canine Stem Cell Therapy Market

- VetStem, Inc.

- Ardent Animal Health, LLC

- Aratana Therapeutics, Inc.

- Boehringer Ingelheim International GmbH

- Zoetis Inc.

- StemcellX

- Cell Therapy Sciences

- Magellan Stem Cells

- VetCell Therapeutics Ltd.

- Vetherapy

- AniCell Biotech

- Medrego.com

- Gallant

- Biobest Laboratories Ltd

- Hilltop Bio

- Animacel d.o.o.

Frequently Asked Questions

The global canine stem cell therapy market is valued at US$ 204.4 Million in 2025.

Rising pet healthcare spending, growing osteoarthritis prevalence, and increasing adoption of regenerative therapies drive market growth.

The global market is poised to witness a CAGR of 4.4% between 2025 and 2032.

Expansion of allogeneic and off-the-shelf stem cell therapies for chronic and orthopedic conditions present major growth opportunities.

Major players in the global are Boehringer Ingelheim International GmbH, Zoetis Inc., StemcellX, Cell Therapy Sciences, VetStem, Inc., and others.