- Biotechnology

- Regenerative Medicine Market

Regenerative Medicine Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Regenerative Medicine Market by Product Type (Cell-Based Therapies, Gene Therapies, Tissue Engineering, Others), Application (Orthopedics & Musculoskeletal, Oncology, Cardiovascular, Dermatology & Wound Healing, Others), End User (Hospitals & Clinics, Research Institutes & Academic Centers, Pharmaceutical & Biotechnology Companies, Others), and Regional Analysis from 2026 to 2033

Regenerative Medicine Market Share and Trends Analysis

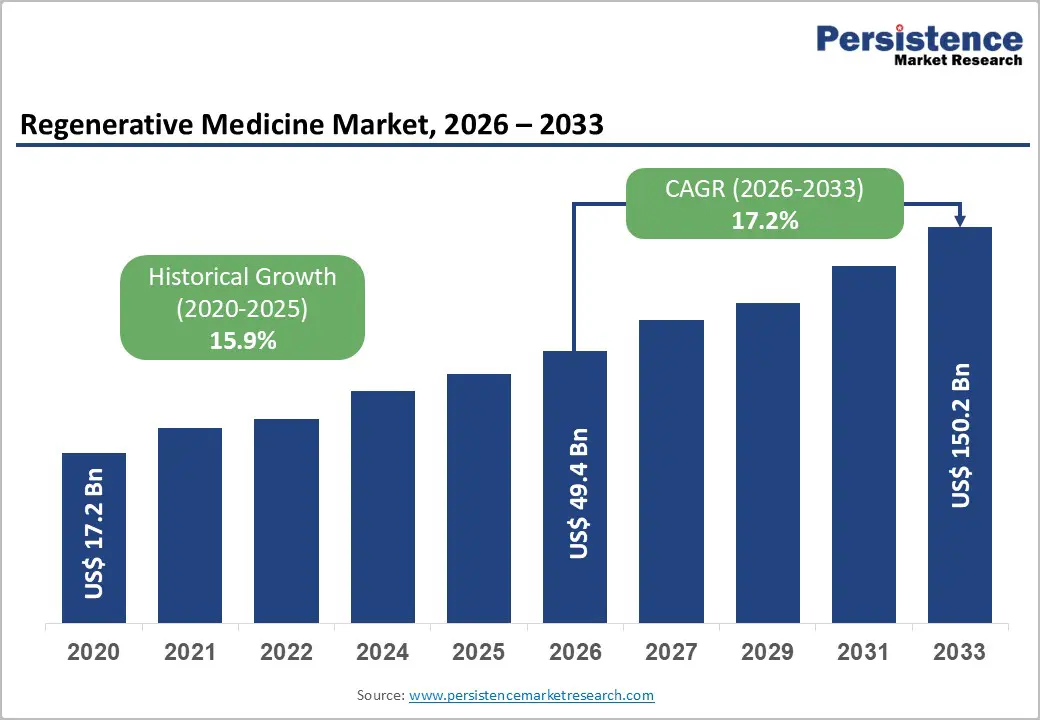

The global regenerative medicine market is projected to grow from US$49.4 billion in 2026 to US$150.2 billion by 2033, at a CAGR of 17.2% over the forecast period.

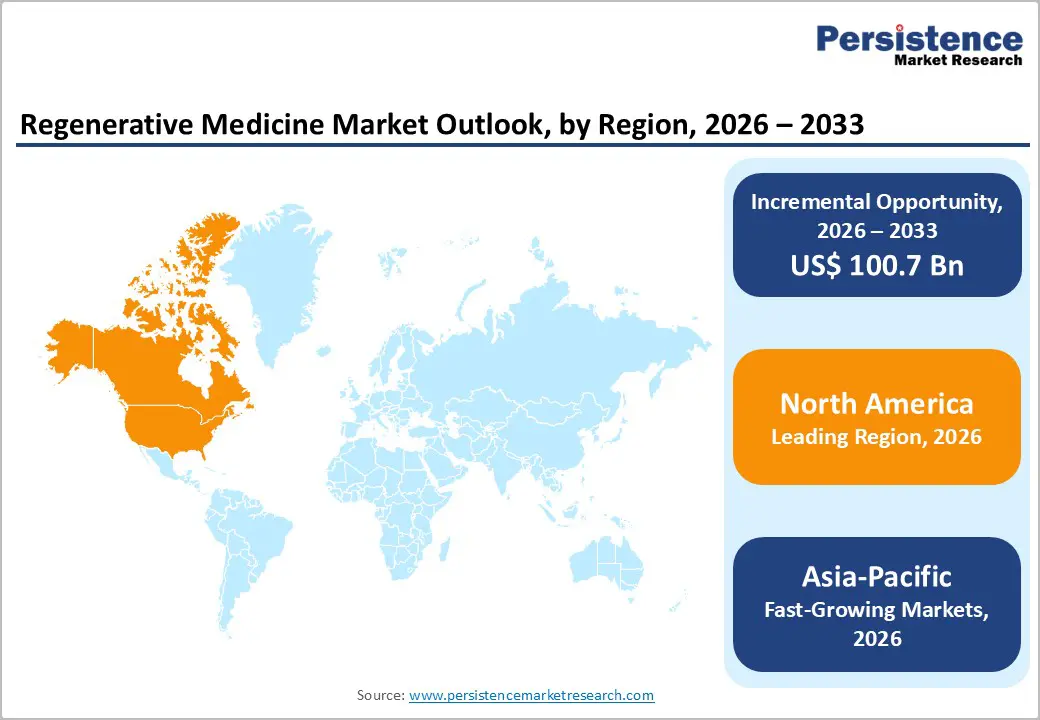

The regenerative medicine market is growing steadily, fueled by digital healthcare, telehealth, and analytics. North America leads with robust infrastructure and stringent regulations ensuring quality production. Asia-Pacific is the fastest-growing region, driven by expanding healthcare facilities, government digital initiatives, rising patient awareness, and increased investments in software, services, and interoperable manufacturing solutions.

Key Industry Highlights:

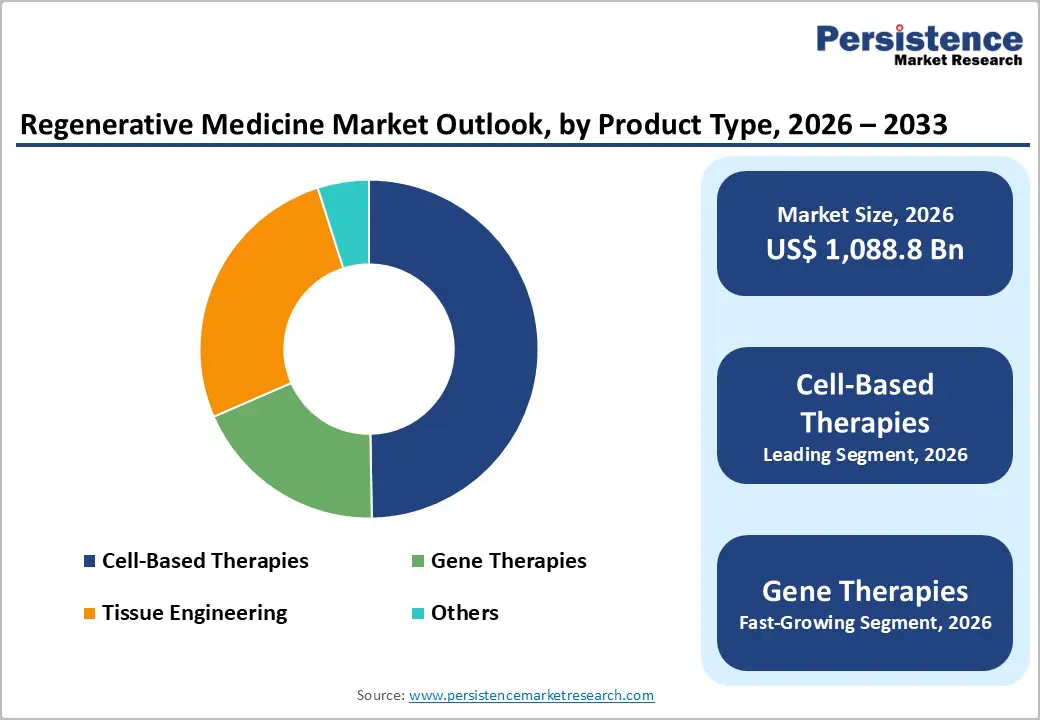

- Dominant Product: Cell therapies are projected to dominate the Regenerative Medicine Market in 2025 with 49.7% share, driven by their use in tissue repair, organ regeneration, and personalized medicine. Their ability to restore damaged tissues, modulate immune responses, and integrate with digital manufacturing and quality monitoring enhances treatment efficacy and precision.

- Dominant Region: North America leads with a 43.5% share in 2025, supported by advanced biotech infrastructure, strong regulatory frameworks, and high adoption of stem cell and gene-based therapies. Asia-Pacific is the fastest-growing region, driven by expanding healthcare and biotech facilities, government initiatives, rising R&D investment, and adoption of scalable regenerative medicine manufacturing solutions.

- Growth Indicators: Growth is propelled by rising demand for cell and gene therapies, increasing biopharmaceutical investments, technological advances in tissue engineering, and the need for effective, personalized regenerative treatments.

- Opportunity: Key opportunities include next-generation gene and stem cell therapies, oncology and rare disease applications, scalable manufacturing platforms, AI-enabled therapy optimization, integration with personalized medicine pipelines, and rapid expansion in emerging biotech regions.

| Key Insights | Details |

|---|---|

| Regenerative Medicine Market Size (2026E) | US$ 49.4 Bn |

| Market Value Forecast (2033F) | US$ 150.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 17.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 15.9% |

Market Dynamics

Driver: Advances in tissue engineering and biomaterials

Advances in tissue engineering and biomaterials are central to regenerative medicine, enabling the creation of functional biological substitutes that restore or enhance damaged tissues. Tissue engineering integrates living cells with scaffolds and biological signals to form constructs that mimic natural tissues, such as skin, cartilage, and bone. Government-supported research programs, such as those funded by the National Institute of Dental and Craniofacial Research (NIDCR), emphasize engineering biocompatible scaffolds and smart materials that support growth and integration with native tissues, thereby steering translational research toward clinical applications. This interdisciplinary work combines biology, chemistry, materials science, and engineering to advance regenerative approaches.

Biomaterials have evolved from passive supports to active agents that interact with cells and tissue microenvironments to promote regeneration. Scientific literature highlights the development of regenerative biomaterials, including hydrogels, polymers, and bioactive matrices that facilitate the repair of bone, cartilage, cardiovascular tissues, and wounds by enhancing cell adhesion and tissue induction. These innovations expand regenerative capabilities beyond conventional grafts and implants, reducing reliance on donor tissues and improving clinical outcomes. Federal agencies such as the National Institute of Standards and Technology (NIST) are also developing measurement standards to ensure consistency and quality in engineered constructs, thereby accelerating the field’s maturation and adoption.

Restraints: Limited availability of skilled professionals and specialized facilities

The regenerative medicine field depends on highly specialized expertise in biology, cell culture, manufacturing, and quality assurance, but workforce shortages persist. A U.S. Government Accountability Office (GAO) report highlights current shortages of laboratory and biomanufacturing technicians, data scientists, and other trained personnel necessary to advance regenerative and advanced therapies, noting that education programs at community and technical college levels are insufficient to meet current and future needs. Stakeholders also emphasize the absence of a nationally recognized curriculum covering essential interdisciplinary skills. These gaps limit research throughput, slow clinical development timelines, and constrain production capacity across the sector.

Survey data from industry sources further underscore workforce constraints: a cited analysis indicates that the proportion of laboratories unable to hire experienced technical and production staff increased from 28.1% in 2018 to 35% in 2023, with persistent deficits in manufacturing, analytical development, and quality control roles. Companies report multiple open positions and lengthy recruitment timelines of two to three months to fill specialized roles, indicating ongoing hiring challenges. Without expansion of targeted training programs and specialized facilities, regenerative medicine developers may struggle to scale production, hindering commercialization and broader patient access to advanced therapies.

Opportunity: Development of next-generation stem cell and gene therapies

Next-generation stem cell and gene therapies present a major opportunity in regenerative medicine by shifting treatment paradigms from symptom management to potential cures for chronic and genetic disorders. Government and clinical trial databases show a growing pipeline of cellular and genetic approaches: as of April 2024, there were 1,751 active global regenerative medicine clinical trials, including 442 cell therapy and 586 gene therapy trials, indicating extensive research activity and translational momentum. These trials span diverse conditions, including cardiovascular and neurological diseases and rare diseases, underscoring broad therapeutic potential. Regulatory bodies like the U.S. Food and Drug Administration (FDA) have approved multiple cell and gene therapies, affirming progress from research to clinical practice.

Recent regulatory milestones further illustrate this opportunity. In late 2025, the FDA approved Waskyra (etuvetidigene autotemcel), a gene therapy for Wiskott-Aldrich syndrome, significantly reducing the incidence of severe infections and bleeding in treated patients. Additionally, England’s NHS approved exa-cel, a CRISPR-based gene-edited stem cell therapy, which delivered functional cures in approximately 96.6% of trial participants with sickle cell disease. These approvals demonstrate increasing regulatory flexibility and clinical validation of advanced therapies, accelerating adoption and patient access. Collectively, this substantiates substantial growth potential and opportunities for innovation in next-generation regenerative treatments.

Category-wise Analysis

By Product Type, Cell-Based Therapies Dominate the Regenerative Medicine Market

Cell-Based Therapies account for 49.7% of the global market in 2025 because they address fundamental mechanisms of tissue repair and functional restoration, and this is reflected in clinical research and regulatory activity. According to peer-reviewed data, there are more than 1,700 active clinical trials worldwide investigating cell therapies, spanning stem cells, T cells, and other therapeutic cell types, indicating broad scientific and clinical engagement. Many of these trials focus on hematopoietic and mesenchymal stem cells for the treatment of blood disorders, degenerative diseases, and immunomodulation, underscoring their central role in regenerative medicine. Additionally, regulatory bodies like the U.S. Food and Drug Administration (FDA) have approved numerous cell-based products, including CAR-T cell therapies and stem cell products listed on the FDA’s approved cellular and gene therapy products page validating the clinical relevance and translational success of cell therapies relative to other modalities.

By Application, orthopedics and musculoskeletal demand is driven by high prevalence of musculoskeletal disorders and stem cell therapy-based on therapy adoption

Orthopedics and musculoskeletal applications dominate the regenerative medicine market because musculoskeletal conditions affect a vast global population and present high unmet clinical needs that regenerative approaches can address. According to the World Health Organization, about 1.71 billion people worldwide live with musculoskeletal conditions such as osteoarthritis, fractures, and back pain, making these disorders a leading contributor to disability and functional impairment. Regenerative techniques like stem cell therapy, scaffold-based tissue engineering, and Orthobiologics are increasingly used to promote healing of bone, cartilage, ligaments, and tendons, offering alternatives to conventional surgery and prosthetics. Government-supported research programs, such as the NIH’s Musculoskeletal Tissue Engineering and Regenerative Medicine Program, further underscore the focus on healing and restoring function in musculoskeletal tissues, highlighting sustained scientific and clinical investment in this application area.

Regional Insights

North America Regenerative Medicine Market Trends

North America dominates the regenerative medicine market with 43.5% share in 2025, because it combines robust research infrastructure, favorable regulatory support, and a high concentration of clinical activity. As of late 2023, North America accounted for the largest portion of global regenerative medicine clinical trials, with around 980 active trials, more than any other region, demonstrating scientific leadership and early access to innovative therapies. Countries in the region, especially the United States and Canada, benefit from strong federal research funding, university-industry collaboration, and dedicated institutions that accelerate translational science. Additionally, regulatory frameworks like the U.S. Food and Drug Administration’s Regenerative Medicine Advanced Therapy (RMAT) designation streamline the development and review of promising cell and gene therapies for serious conditions, enhancing commercial viability and adoption.

Europe Regenerative Medicine Market Trends

Europe is an important region in the regenerative medicine market because it combines strong public funding, collaborative research networks, and supportive regulatory frameworks that drive innovation and clinical adoption. The European Medicines Agency (EMA) has approved over 25 Advanced Therapy Medicinal Products (ATMPs), including cell and gene therapies showing regulatory commitment to advanced treatments. Governments and EU programmes, such as Horizon Europe, fund bio-printing and biomaterials research to accelerate the clinical translation of regenerative solutions. European countries host a dense ecosystem of biotech firms and academic centres, particularly in Germany, the United Kingdom, France, Spain, and Italy, enhancing R&D output and cross-sector partnerships. Demographic pressures from an ageing population and high chronic disease prevalence further sustain demand for regenerative therapies.

Asia-Pacific Regenerative Medicine Market Trends

The Asia-Pacific region is the fastest-growing region in the regenerative medicine market, driven by rapidly expanding clinical research, supportive government initiatives, and demographic pressures. More than 500 active clinical trials involving stem cells were underway in Japan, China, and South Korea in 2023, indicating strong translational research momentum and regional innovation capacity. Governments in the region are actively shaping favorable regulatory environments, for example, Japan’s Regenerative Medicine Act accelerates clinical development of cell therapies, while other nations streamline pathways for advanced biotherapeutics. Demographic data from the United Nations Department of Economic and Social Affairs show the Asia-Pacific elderly population (aged 60+) exceeding 700 million, driving demand for regenerative solutions to treat chronic, age-related conditions and expanding market potential.

Competitive Landscape

Leading regenerative medicine companies prioritize advanced cell and gene therapy technologies, scalable manufacturing, and regulatory compliance. Investments focus on process optimization, AI-enabled design, and high-throughput testing to ensure reproducibility and efficacy. Collaborations with biotech, academia, and regulators, alongside strict quality control and supply chain integration, accelerate adoption of stem cell, gene, and tissue-engineered therapies globally.

Key Industry Developments:

- In January 2026, Novartis announced that its investigational therapy ianalumab had received Breakthrough Therapy designation from the U.S. Food and Drug Administration (FDA) for the treatment of Sjögren’s disease, a chronic autoimmune disorder with significant unmet medical need.

- In November 2024, Roche entered into a definitive agreement to acquire Poseida Therapeutics, including its portfolio of cell therapy candidates and related platform technologies.

Companies Covered in Regenerative Medicine Market

- Pfizer, Inc.

- Novartis AG

- F. Hoffmann-La Roche Ltd.

- Bayer AG

- AstraZeneca plc

- GlaxoSmithKline (GSK)

- Merck KGaA

- Abbott

- Integra LifeSciences Corp.

- Vericel Corp.

- Cook Biotech, Inc.

- Astellas Pharma, Inc.

- Others

Frequently Asked Questions

The global regenerative medicine market is projected to be valued at US$ 49.4 Bn in 2026.

Rising demand for cell and gene therapies, technological advances, ageing population, and supportive regulations drive growth.

The global regenerative medicine market is poised to witness a CAGR of 17.2% between 2026 and 2033.

Next-generation stem cell and gene therapies, rare disease applications, AI optimization, and emerging market expansion.

Pfizer, Inc., Novartis AG, F. Hoffmann-La Roche Ltd., Bayer AG, AstraZeneca plc, GlaxoSmithKline (GSK).