- Biotechnology

- Allogeneic Cell Therapy Market

Allogeneic Cell Therapy Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Allogeneic Cell Therapy Market by Therapy Type (Stem Cell Therapies, Non-stem Cell Therapies), Therapeutic Area (Hematological Disorders, Dermatological Disorders, Oncological Disorders, Neurological Disorders, Others), and Regional Analysis 2026 - 2033

Allogenic Cell Therapy Market Share and Trends Analysis

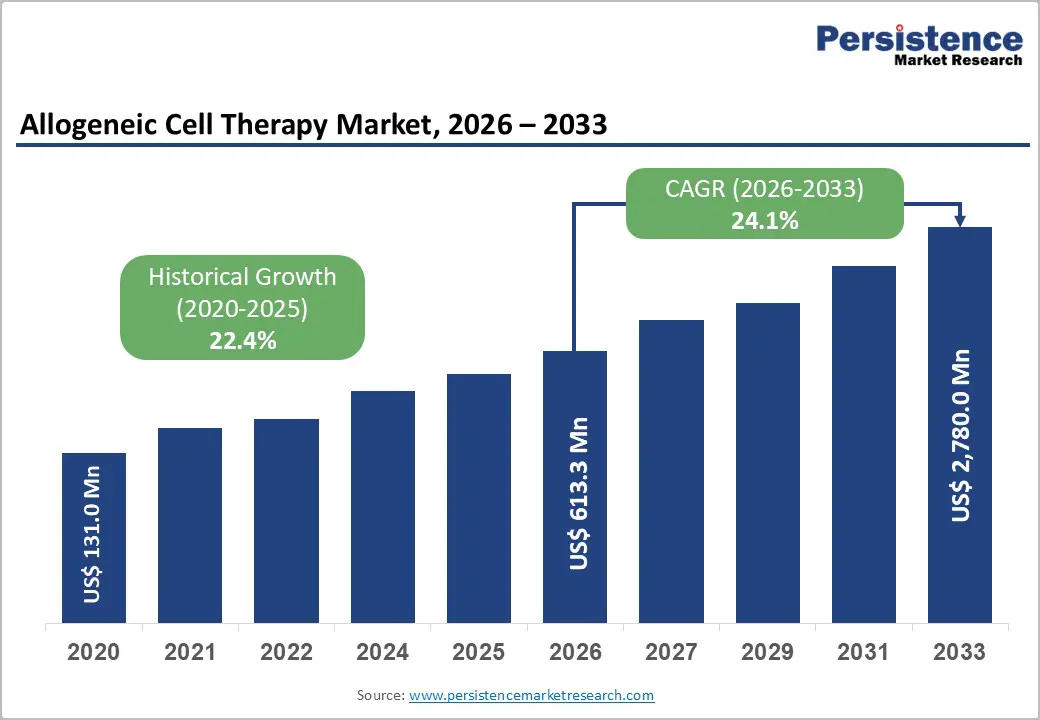

The global allogeneic cell therapy market is projected to grow from US$ 613.3 million in 2026 to US$ 2,780.0 million by 2033, at a CAGR of 17.2% over the forecast period.

The global allogeneic cell therapy market is expanding steadily, driven by digital healthcare, telehealth, and advanced analytics. North America dominates due to robust infrastructure and stringent regulations that ensure quality. The Asia-Pacific region is the fastest-growing region, supported by expanding healthcare facilities, government digital initiatives, rising patient awareness, and increasing investments in software, services, and interoperable manufacturing solutions.

Key Industry Highlights:

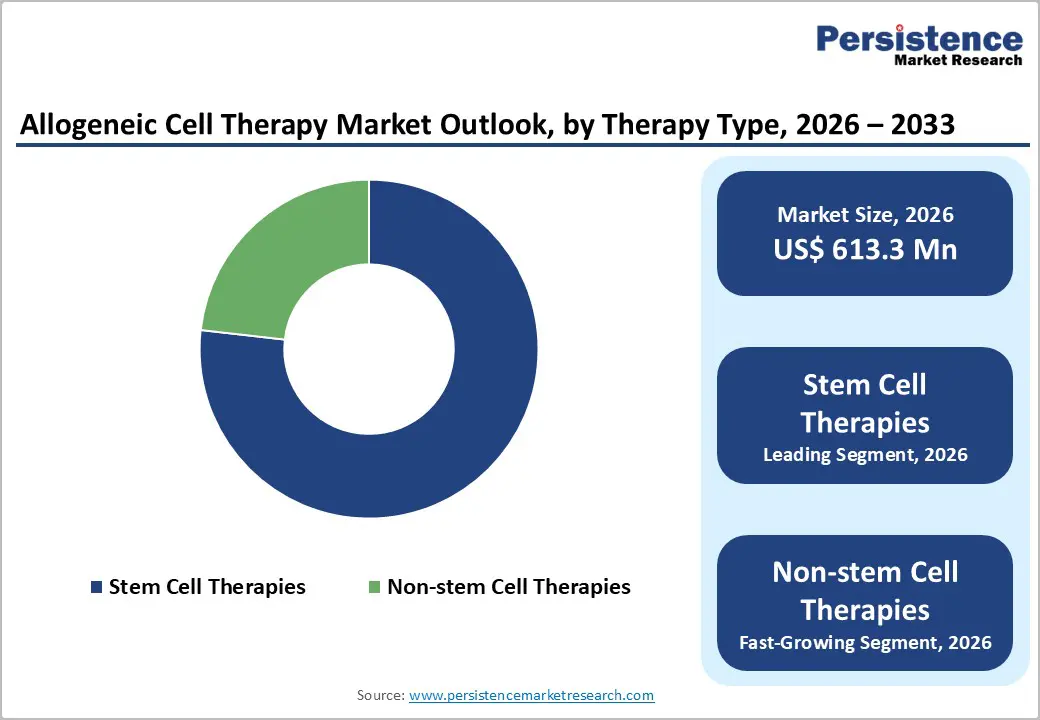

- Dominant Segment: Stem cell therapies are projected to account for 76.8% of the allogeneic cell therapy market in 2025, driven by applications in tissue repair, organ regeneration, and personalized medicine. Their ability to restore damaged tissues, modulate immune responses, and integrate with digital manufacturing and quality monitoring enhances treatment precision and efficacy.

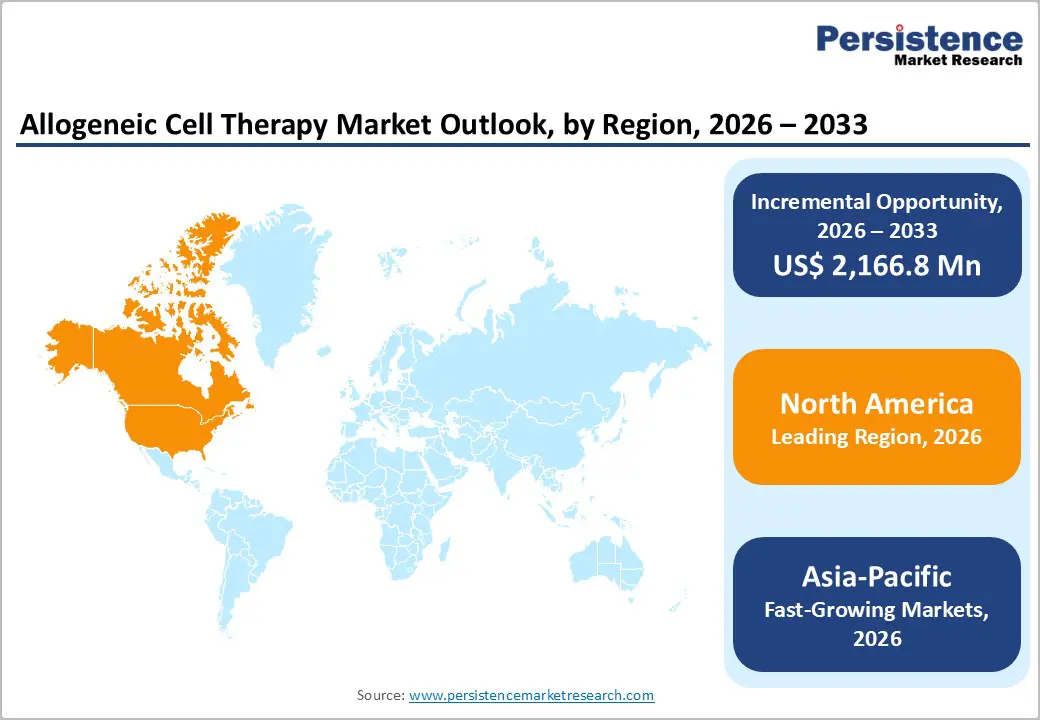

- Dominant Region: North America leads with a 46.0% share in 2025, supported by advanced biotech infrastructure, strong regulatory frameworks, and high adoption of stem cell and gene-based therapies. The Asia-Pacific region is the fastest-growing region, driven by expanding healthcare and biotech facilities, government initiatives, rising R&D investment, and the adoption of scalable regenerative medicine manufacturing solutions.

- Growth Indicators: Growth is propelled by rising demand for cell and gene therapies, increasing biopharmaceutical investments, technological advances in tissue engineering, and the need for effective, personalized regenerative treatments.

- Market Opportunity: Key opportunities include next-generation gene and stem cell therapies, oncology and rare disease applications, scalable manufacturing platforms, AI-enabled therapy optimization, integration with personalized medicine pipelines, and rapid expansion in emerging biotech regions.

| Key Insights | Details |

|---|---|

| Allogeneic Cell Therapy Market Size (2026E) | US$ 613.3 Mn |

| Market Value Forecast (2033F) | US$ 2,780.0 Mn |

| Projected Growth (CAGR 2026 to 2033) | 24.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 22.4% |

Market Dynamics

Driver: Rising Demand for Cell and Gene Therapies

The clinical research landscape shows a consistent rise in cell and gene therapy development globally, with public clinical trial databases indicating thousands of active gene and cell therapy studies (including mesenchymal stromal cell trials and gene therapy trials listed internationally) that have substantially increased over the past decade. For example, one public repository lists 879 distinct gene therapy trials registered from 2011-2021 alone, indicating expanding pipeline activity and therapeutic interest. This rising clinical activity aligns with broader public health trends targeting chronic, genetic, and life-threatening conditions, which are leading causes of morbidity worldwide and are increasingly being addressed through advanced biological modalities. Growth in the underlying therapeutic landscape directly bolsters demand for scalable allogeneic approaches, which can serve multiple patients without individualized manufacturing.

Restraints: High Cost and Complex Manufacturing Challenges

A principal restraint on advanced therapies such as allogeneic cell products is the significant manufacturing complexity and cost structure, documented in scientific and policy analyses. Regulatory and health science literature notes that R&D costs for bringing a new cell or gene therapy to approval can exceed USD 1.9 billion per asset, driven by complex clinical development stages and high attrition risk during trials.

Furthermore, public academic reviews indicate that the manufacturing and quality-control processes for cell and gene therapies are highly specialized, requiring stringent Good Manufacturing Practices, extensive analytical testing, and infrastructure that is not uniformly available globally. These factors elevate operational costs and limit broad production scalability, particularly in settings without established biomanufacturing ecosystems.

Opportunity: Expansion of Next-Generation Gene and Stem Cell Therapies in Emerging Regions

Public data show that both scientific activity and infrastructure development for advanced therapies are expanding in emerging regions. Regulatory registries reflect increasing trial activity and a broader geographic footprint for cell and gene therapy research beyond traditional leaders in North America and Europe. For instance, China’s share of global cell therapy pipelines has grown substantially in recent years, indicating robust regional engagement in advanced biological sciences. Additionally, public investments in stem cell research institutes and regenerative medicine platforms, such as dedicated government research institutes in India focusing on cell therapies, illustrate growing regional capacity and policy support for innovation. These developments create opportunities to align allogeneic cell therapy production with emerging scientific ecosystems, enabling more accessible clinical applications and localized manufacturing solutions.

Category-wise Analysis

By Therapy Type Insights

Stem cell therapies occupies 76.8% share of the global market in 2025, because they constitute a substantial portion of clinical research and therapeutic application in regenerative medicine. Public clinical data show that stem cells represent about 36 percent of current cell therapy clinical trials worldwide, used across at least ten major disease categories including hematological disorders and tissue regeneration, indicating deep clinical interest and broad applicability. Stem cells such as hematopoietic and mesenchymal stem cells can differentiate into multiple cell types and help rebuild or support damaged tissues, giving them unique value in treating complex diseases like blood cancers, autoimmune disorders, and organ failure. Additionally, government trials and regulatory approvals for stem cell-based allogeneic products (e.g., mesenchymal cell therapies for graft-versus-host disease) demonstrate clinical feasibility and institutional support for these approaches.

By Therapeutic Area, Hematological Disorders demand, due to high prevalence, proven efficacy, and research focus

Hematological disorders dominate the allogeneic cell therapy market due to their high prevalence, well-defined biology, and proven responsiveness to cell-based interventions. Allogeneic hematopoietic stem cell transplants have long been standard treatments for conditions such as leukemia, lymphoma, and bone marrow failure. For instance, acute myeloid leukemia (AML) accounts for nearly one-third of adult leukemia cases in the U.S., with allogeneic stem cell transplantation significantly improving five-year survival compared to chemotherapy alone.

Clinical trial data and public registries indicate that most cell therapy research focuses on hematologic malignancies, owing to the accessibility of blood and bone marrow cells, measurable endpoints, and established protocols. This combination of disease burden, efficacy, and research focus ensures hematological disorders remain the leading therapeutic area in the allogeneic cell therapy market.

Regional Insights

North America Allogeneic Cell Therapy Market Trends

North America dominates the allogeneic cell therapy market with 46.0% share in 2025, due to its advanced clinical research infrastructure, high concentration of biotech firms, and supportive regulatory environment. Public data indicate that North America accounts for roughly half of global cell and gene therapy clinical trials, with over 1,200 active trials reported, reflecting deep engagement in both early- and late-stage development. The United States, in particular, benefits from accelerated regulatory pathways such as the FDA’s RMAT and Fast Track designations, which encourage innovation and speed product approvals. Substantial government and private funding further support discovery, manufacturing scale-up, and commercialization, reinforcing the region’s leadership in allogeneic cell therapy development and adoption.

Europe Allogeneic Cell Therapy Market Trends

Europe plays a pivotal role in the allogeneic cell therapy market due to its cohesive regulatory framework and strong public research institutions. The European Medicines Agency’s Advanced Therapy Medicinal Products (ATMP) regulation provides a centralized pathway for advanced therapies, enabling approvals across EU member states and supporting harmonized clinical development. Key European countries such as Germany, the United Kingdom, and France host robust clinical research networks and benefit from substantial public funding for regenerative medicine, fostering innovation and translational research. An aging population and rising prevalence of chronic diseases further enhance the demand for cell-based therapies. These structural strengths position Europe as the second-largest regional market with growing adoption of allogeneic treatments.

Asia-Pacific Allogeneic Cell Therapy Market Trends

The Asia-Pacific region is the fastest-growing market for allogeneic cell therapy, driven by expanding healthcare infrastructure, rising disease prevalence, and government initiatives supporting biotechnology development. Countries such as China, Japan, South Korea, and India are investing heavily in research capabilities and clinical trial capacity, contributing to a rapid increase in advanced therapy activity. Public data highlight that Asia-Pacific accounts for a significant proportion of global stem cell and regenerative medicine trials, reflecting its expanding scientific ecosystem and patient access improvements. Large populations facing chronic and hematological disorders create substantial demand for innovative treatments, while supportive policies and cost-competitive environments attract both local and international investment, accelerating regional growth.

Competitive Landscape

Leading allogeneic cell therapy companies focus on advanced cell and gene technologies, scalable manufacturing, and regulatory compliance. Investments target process optimization, AI-enabled design, and high-throughput testing for consistent efficacy. Collaborations with biotech, academia, and regulators, combined with strict quality control and integrated supply chains, drive global adoption of stem cell, gene, and tissue-engineered therapies.

Key Industry Developments:

- In January 2026, ImmunityBio’s Allogeneic CD19 Cell Therapy Showed Durable Complete Response Beyond 15 Months. ImmunityBio’s off-the-shelf allogeneic CD19 chimeric antigen receptor natural killer (CAR-NK) cell therapy achieved durable complete responses in patients with Waldenström’s non-Hodgkin lymphoma, with one patient maintaining remission for over 15 months after treatment cessation.

Companies Covered in Allogeneic Cell Therapy Market

- SSM Cardinal Glennon Children's Medical Center

- Cleveland Cord Blood Center

- Duke University School of Medicine

- New York Blood Center

- Clinimmune Labs, University of Colorado Cord Blood Bank

- MD Anderson Cord Blood Bank

- LifeSouth Community Blood Centers, Inc.

- Bloodworks Northwest

- JCR Pharmaceuticals Co., Ltd.

- Sumitomo Pharma Co., Ltd.

- Atara Biotherapeutics

- Mallinckrodt Pharmaceuticals

- Tego Science Inc

- Takeda Pharmaceutical Company Limited

- STEMPEUTICS RESEARCH PVT LTD

- Biosolution Co., Ltd.

- MEDIPOST Co., Ltd.

- Others

Frequently Asked Questions

The global allogeneic cell therapy market is projected to be valued at US$ 613.3 Mn in 2026.

Rising demand for cell and gene therapies, technological advances, and growing biopharmaceutical investments drive growth.

The global allogeneic cell therapy market is poised to witness a CAGR of 24.1% between 2026 and 2033.

Next-generation gene and stem cell therapies, oncology applications, scalable manufacturing, AI optimization, and emerging region expansion.

SSM Cardinal Glennon Children's Medical Center, Cleveland Cord Blood Center, Duke University School of Medicine, New York Blood Center, Clinimmune Labs, University of Colorado Cord Blood Bank, MD Anderson Cord Blood Bank.