- Processed Food

- Organic Lamb Market

Organic Lamb Market Size, Share, and Growth Forecast 2026 - 2033

Organic Lamb Market by Product Type (Raw, Processed), by End Use (Household, Foodservice/Hospitality, Food Processing), by Sales Channel (Supermarkets/Hypermarkets, Specialty Organic Stores, Convenience Stores, Online Retail, Others), by Regional Analysis, 2026-2033

Organic Lamb Market Size and Trends Analysis

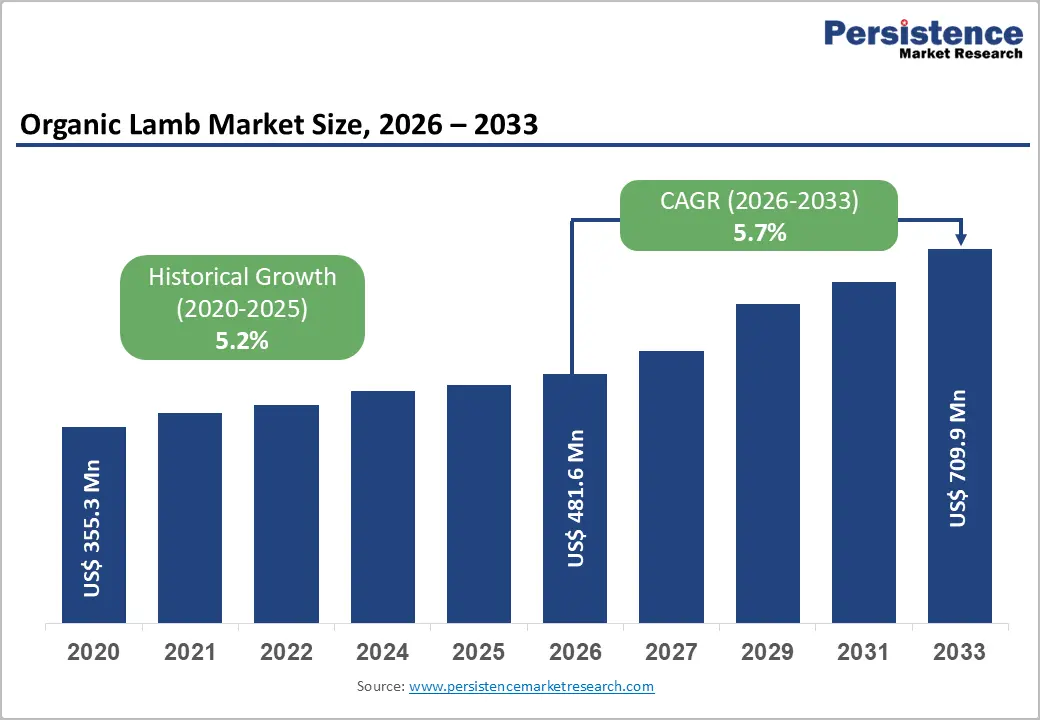

The global Organic Lamb market size is expected to be valued at US$ 481.6 million in 2026 and projected to reach US$ 709.9 million by 2033, growing at a CAGR of 5.7% between 2026 and 2033

The steady ascent of the market is primarily driven by an intensive shift in consumer dietary preferences toward clean-label and ethically sourced proteins. As global health awareness reaches a critical mass, demand for meat produced without synthetic hormones, antibiotics, or chemical pesticides has shifted from a niche trend to a mainstream requirement. Furthermore, the integration of organic livestock within regenerative agriculture frameworks is attracting environmentally conscious demographics, particularly in North America and Europe, who prioritize carbon-neutral and high-welfare farming systems over conventional production methods.

Key Industry Highlights

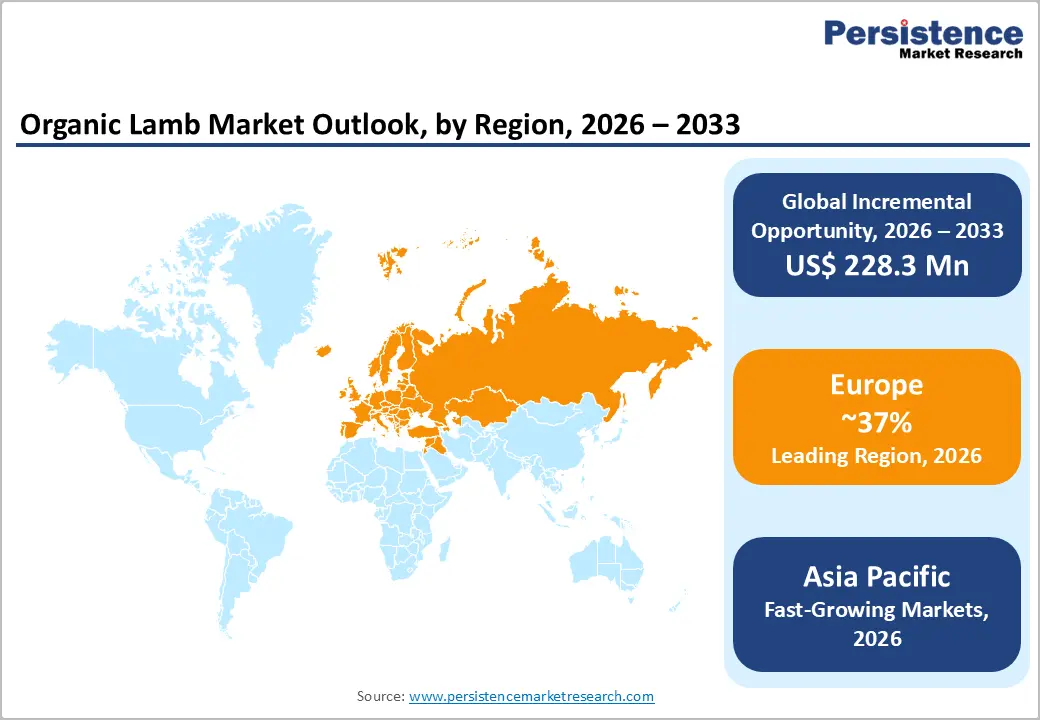

- Leading Region: Europe, accounting for ~37% market share, supported by strong organic farming subsidies under the EU Common Agricultural Policy, high consumer trust in organic certification, and deep-rooted lamb consumption across households and foodservice.

- Fastest-Growing Region: Asia Pacific, propelled by rising middle-class income, food safety concerns, premium protein demand in Tier-1 cities, and increasing imports of certified organic lamb from Australia and New Zealand.

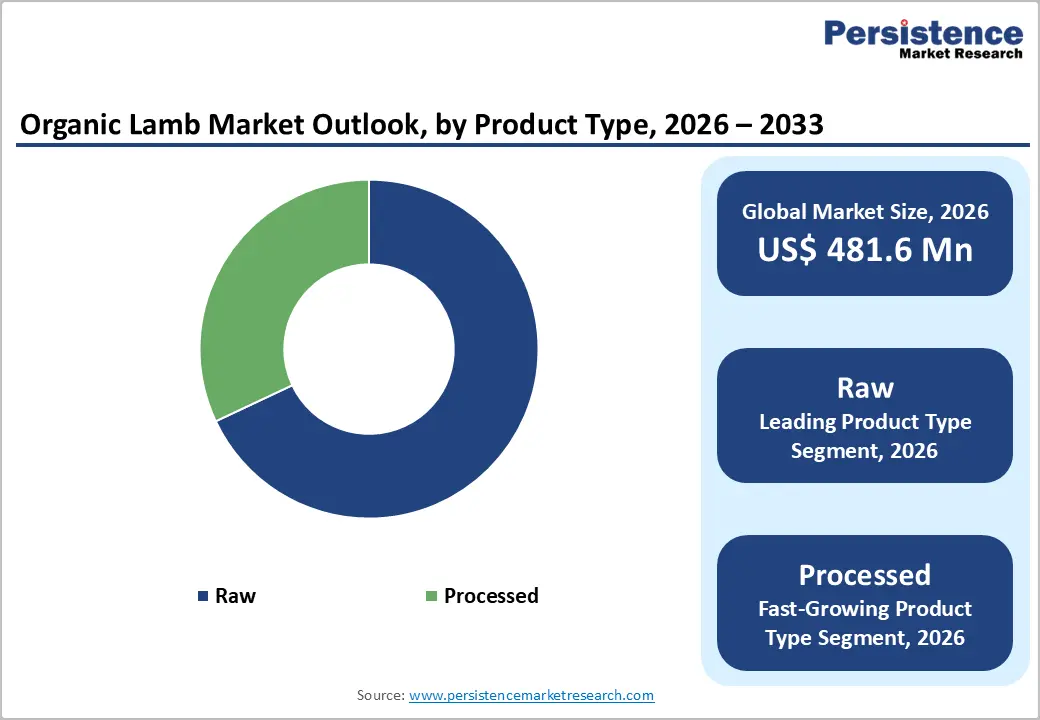

- Fastest-Growing Product Type Segment: Processed & Value-Added Organic Lamb, driven by demand for ready-to-cook formats such as sausages, marinated cuts, and burgers that align with urban lifestyles without compromising organic integrity.

- Market Drivers: Rising health consciousness and clean-label demand are accelerating organic lamb adoption as consumers actively avoid antibiotics, synthetic hormones, and chemically treated feed while prioritizing nutrient-dense, grass-fed animal proteins.

- Opportunities: Expansion of processed and convenience-focused organic lamb offerings using clean-label preservation, modified atmosphere packaging, and e-commerce–ready formats to unlock higher margins and repeat household consumption.

- Key Developments: In May 2025, Lidl US launched its private-label fresh meat line “Butcher’s Specialty,” entering organic and premium proteins. In March 2025, Danish Crown A/S partnered with certified organic sheep farmers in Northern Europe to scale standardized organic lamb exports to Asia.

| Key Insights | Details |

|---|---|

| Organic Lamb Market Size (2026E) | US$ 481.6 Mn |

| Market Value Forecast (2033F) | US$ 709.9 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.2% |

Market Dynamics

Driver – Rising Consumer Health Consciousness and Clean Label Demand

The foremost driver of the global organic lamb market is the accelerating consumer pivot toward health-centric food choices. Modern shoppers are increasingly scrutinizing food labels, seeking transparency regarding the origin and processing of their meat. According to the Organic Trade Association (OTA), a significant portion of the growth in organic meat categories is linked to the perceived health benefits of consuming livestock raised on 100% organic feed. Organic lamb is rich in Omega-3 fatty acids and Conjugated Linoleic Acid (CLA), which are often found in higher concentrations in grass-fed, organic livestock compared to grain-fed conventional counterparts. This nutritional profile, combined with the absolute absence of growth-promoting hormones and prophylactic antibiotics, positions organic lamb as a premium health food. Consequently, households are increasingly willing to pay a premium for products that mitigate the risk of antibiotic resistance and chemical ingestion.

Restraints – Prohibitively High Production and Certification Costs

The primary barrier to widespread adoption of organic lamb is the significant cost differential compared to conventional meat. Organic sheep farming requires USDA Organic or equivalent international certifications, which involve rigorous audits and annual fees. More importantly, the cost of organic-certified feed can be 30% to 50% higher than conventional grain. Additionally, organic standards prohibit the use of synthetic fertilizers in pastures, often resulting in lower stocking densities and slower animal growth rates. Data from Australian Organic Ltd suggests that these factors culminate in production costs that are substantially higher, which are inevitably passed on to consumers. In price-sensitive markets or during periods of economic volatility, this high price point limits the addressable market mainly to high-income households, hindering the sector's volume growth.

Opportunity – Surging Demand for Processed and Ready-to-Cook Organic Solutions

A significant opportunity lies in the diversification of organic lamb into the processed and Value-Added segments. As urban lifestyles become more fast-paced, consumers are seeking convenience without compromising their commitment to organic standards. There is a burgeoning market for organic lamb sausages, pre-marinated lamb chops, and organic lamb burgers. Companies like Hormel Foods Corporation, through its Applegate brand, have already demonstrated the success of organic processed meats. Developing a wider variety of "heat-and-eat" organic lamb meals can capture a larger share of the Household segment. Statistics indicate that the processed meat sector is evolving rapidly, with a growing interest in clean-label preservatives and Nitrite-free formulations. By leveraging innovative packaging technologies like Modified Atmosphere Packaging (MAP), producers can extend the shelf life of these processed products, making them more viable for global distribution and e-commerce retail.

Category-wise Analysis

Product Type Analysis

The Raw lamb segment is the dominant force in the Organic Lamb Market, accounting for a commanding 69% market share in 2025. This dominance is rooted in the traditional consumer preference for fresh, chilled, or frozen cuts that allow for home preparation and culinary customization. Primary cuts such as lamb racks, shanks, and legs are highly sought after in both the Household and Foodservice sectors. The high market share of raw lamb is supported by the consumer's desire for the "purest" form of the product, free from any additives or processing steps. Organizations like the Agriculture and Horticulture Development Board (AHDB) note that while processed options are rising, the core of the market remains centered on fresh, high-quality meat. The transparency of a raw cut allows consumers to inspect the marbling and color, which are key indicators of quality in organic, grass-fed livestock.

Sales Channel Analysis

Supermarkets/Hypermarkets represent the leading sales channel for the Organic Lamb Market, providing the most significant volume of sales in 2025. This is due to the aggressive expansion of organic sections within major retail chains like Whole Foods Market, Tesco, and Carrefour. These retailers offer the convenience of one-stop shopping and the ability to easily compare prices and labels. However, Online Retail is emerging as the fastest-growing channel. The shift is supported by the growing reliability of refrigerated delivery services and consumers' desire for specialized products that may not be available in local stores. Data suggests that online sales of organic meat have increased by over 16% year over year in certain regions, as consumers value the detailed product information and traceability reports typically provided by digital platforms, which enhance trust in organic certification.

Region-wise Insights

North America Organic Lamb Market Trends and Insights

The North America market is characterized by a mature regulatory environment and a high degree of consumer awareness regarding organic standards. The United States leads the region, supported by the rigorous USDA National Organic Program (NOP), which ensures that all products labeled as organic meet strict federal guidelines. In recent years, demand for grass-fed and pasture-raised organic lamb has surged, reflecting broader interest in sustainable agriculture.

Innovations in the region are heavily focused on the innovation ecosystem, with companies like Tyson Foods, Inc. and Hormel Foods Corporation expanding their organic portfolios to include more convenient, portion-controlled options. The rise of regenerative organic certifications is a key trend, with consumers increasingly looking for products that not only avoid chemicals but also actively improve soil health. This has led to a collaborative effort between farmers and retailers to enhance supply chain transparency through QR codes and digital labels.

Europe Organic Lamb Market Trends and Insights

Europe is the global leader in the Organic Lamb Market, holding a 37% market share in 2025. The region's dominance is underpinned by a long-standing culture of organic farming and strong government support through the Common Agricultural Policy (CAP). Countries like Germany, France, and the U.K. have robust domestic production and highly sophisticated distribution networks. The European Union’s commitment to increasing organic farmland to 25% by 2030 has provided a stable framework for market growth.

Regulatory harmonization across the EU enables seamless trade and consistent labeling, thereby building consumer trust. In the U.K., the Soil Association reports that lamb is a preferred organic red meat due to its natural suitability for traditional grazing landscapes. Furthermore, European consumers are increasingly opting for organic lamb in the Foodservice sector, as sustainability becomes a core pillar of corporate social responsibility for restaurant chains and catering companies across the continent.

Asia Pacific Organic Lamb Market Trends and Insights

The Asia Pacific region is the fastest-growing market for organic lamb, driven by the rapid expansion of the middle class in China, India, and ASEAN countries. Increasing disposable income and a heightened focus on food safety following various conventional meat scandals have steered consumers toward certified organic imports. Australia and New Zealand are the primary suppliers to this region, leveraging their reputation for "clean and green" production.

In China, the demand for premium organic proteins is surging in Tier-1 cities, where health-conscious consumers are willing to pay significant premiums for imported organic lamb. The region also benefits from a growing manufacturing advantage in terms of processed organic meat products, with local players investing in advanced processing facilities. As e-commerce continues to dominate the retail landscape in Asia, the availability of organic lamb through platforms like Alibaba and JD.com is expected to catalyze further market penetration.

Market Competitive Landscape

Market Structure Analysis The Organic Lamb Market is currently fragmented, characterized by a mix of large-scale meat processors and numerous small-to-medium-sized specialized organic farms. Global leaders like Tyson Foods, Inc. and Danish Crown A/S are increasingly consolidating their positions through the acquisition of niche organic brands to capitalize on the high-growth potential. Key strategies include heavy investment in Research and Development (R&D) to improve meat quality and shelf life, as well as the adoption of blockchain technology for enhanced traceability. Differentiation is primarily achieved through stringent adherence to animal welfare standards and the use of unique, heritage breeds. Emerging business models are focusing on Direct-to-Consumer (DTC) delivery and subscription boxes, which allow producers to build stronger brand loyalty and gather direct consumer feedback.

Key Developments:

- In May 2025, Lidl US announced the launch of its first private-label fresh meat range under the brand Butcher’s Specialty, marking a strategic expansion of its protein portfolio.

- In March 2025, Development (Danish Crown A/S) Danish Crown A/S entered into a strategic partnership with a group of certified organic sheep farmers in Northern Europe. The collaboration aims to standardize organic processing methods and increase the export volume of organic lamb to Asia.

Companies Covered in Organic Lamb Market

- Tyson Foods, Inc.

- Hormel Foods Corporation

- Danish Crown A/S

- Pick’s Organic Farm

- Saltbush Livestock Pty Ltd

- Windy N Ranch

- Mallow Farm & Cottage

- Neat Meat

- Minerva Foods S.A.

- Dawn Meats

- Others

Frequently Asked Questions

The global Organic Lamb Market is expected to be valued at approximately US$ 481.6 million in 2026, following a steady growth trajectory driven by the rising demand for premium, chemical-free meat products.

The demand is primarily driven by increasing consumer health consciousness, a shift toward clean-label foods, and heightened awareness of animal welfare and environmental sustainability in livestock production.

Europe is the leading region, accounting for an estimated 37% market share in 2025, supported by robust regulatory frameworks such as the EU Farm to Fork Strategy and a strong culture of organic consumption.

A significant opportunity exists in the development of Processed and Ready-to-Cook organic lamb products, as well as expanding into Online Retail channels to capture the growing segment of tech-savvy, time-poor consumers.

Major companies include Tyson Foods, Inc., Hormel Foods Corporation, Danish Crown A/S, and specialized producers like Pick’s Organic Farm and Saltbush Livestock Pty Ltd.