- Food Ingredients & Additives

- Organic Fruits and Vegetables Market

Organic Fruits and Vegetables Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Organic Fruits and Vegetables Market by Fruits (Banana, Apple, Berries), by Vegetables (Leafy Vegetables, Tomato, Potato), by Certification (USDA Organic, EU Organic), by Distribution Channel (Supermarkets/Hypermarkets, Online Retail), and Regional Analysis for 2025 - 2032

Organic Fruits and Vegetables Market Size and Trends

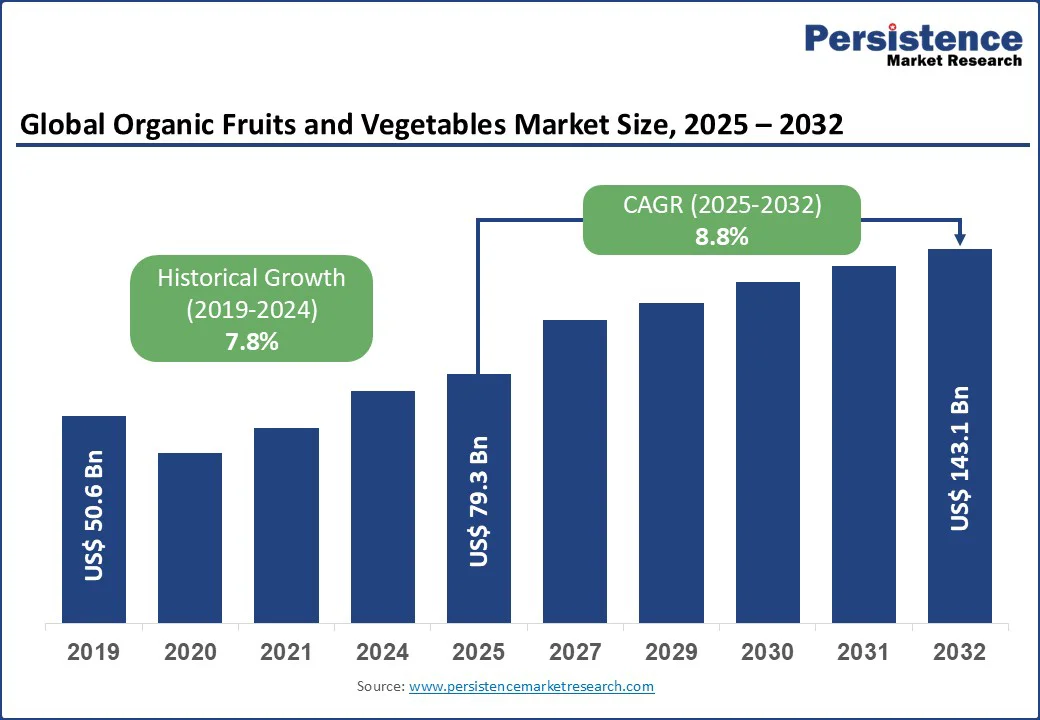

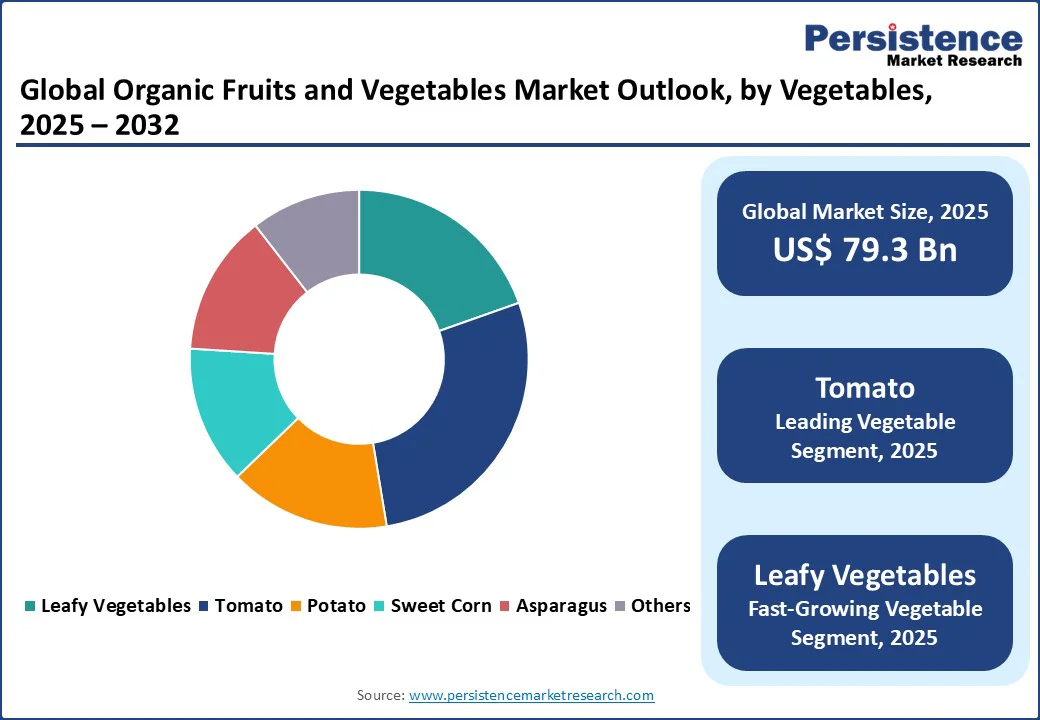

The organic fruits and vegetables market size is likely to be valued at US$ 79.3 Bn in 2025 and is estimated to reach US$ 143.1 Bn in 2032, growing at a CAGR of 8.8% during the forecast period 2025 - 2032; the growth is spurred by Environmental, Social, and Governance (ESG)-focused investments, adoption of regenerative agriculture, and collaborations between growers and retailers.

Key Industry Highlights:

- Leading Fruit: Organic bananas hold nearly 27.6% share in 2025, as consumers favor them due to low pesticide exposure and better flavor.

- Dominant Vegetable: Tomatoes, approximately 27.8% of the organic fruits and vegetables market share in 2025, with their rich taste and chemical-free cultivation.

- New Organic Line: In February 2025, a product line featuring organic fruits and vegetables was launched in Sharjah. The organic produce from Gheras, a division of the Sharjah Agricultural and Livestock Production Establishment (EKTIFA) are being grown in the greenhouses of Al Dhaid, where it is ensured they are free from genetic modification.

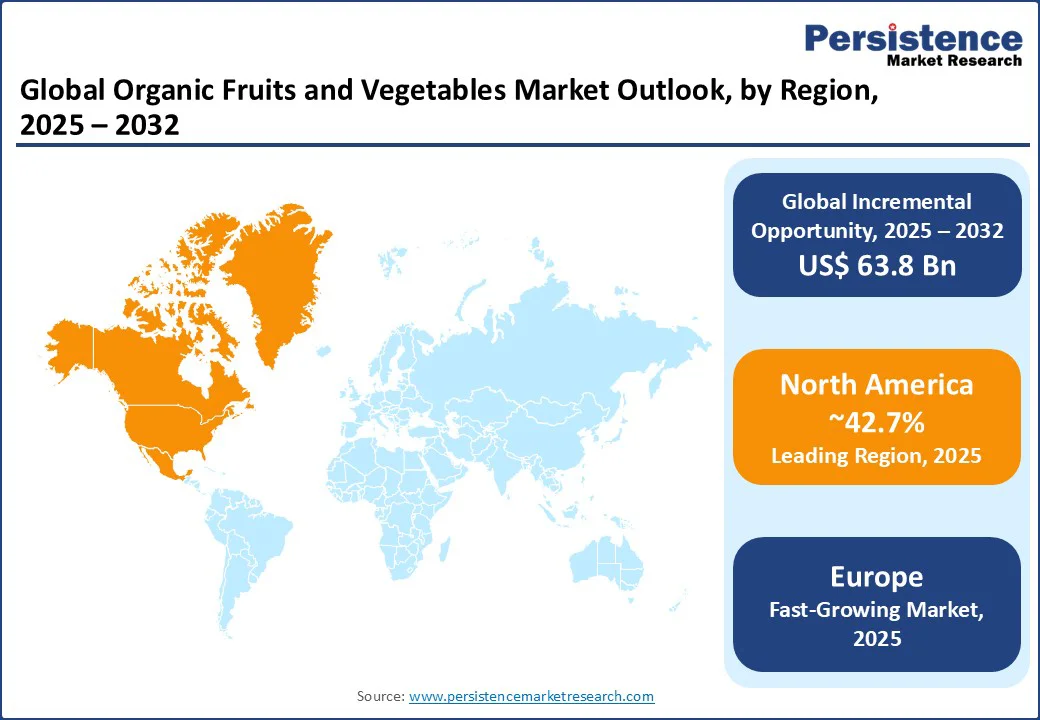

- Leading Region: North America with about 42.7% share in 2025, backed by the expansion of organic-friendly retailers and fast-casual chains.

- Fastest-growing Region: Europe, owing to strict certification standards and increasing consumer focus on sustainability.

| Key Insights | Details |

|---|---|

| Organic Fruits and Vegetables Market Size (2025E) | US$ 79.3 Bn |

| Market Value Forecast (2032F) | US$ 143.1 Bn |

| Projected Growth (CAGR 2025 to 2032) | 8.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 7.8% |

Market Factors - Growth, Barrier, and Opportunity Analysis

Health and Safety Perceptions among Gen Z and Millennials Spur Demand

Young consumers, especially millennials and Gen Z, are increasingly choosing organic produce not just for taste or trend, but because they see organic food as a health and safety shield. A recent U.S. survey showed that nearly 38% of adults are more likely to eat at restaurants that provide organically produced food, and Gen Z consumers overwhelmingly view the USDA Organic label as essential when dining out.

Fast-casual chains and university dining programs are integrating certified organic ingredients into their standard menus. In its 2022 Impact Report, Sweetgreen revealed having purchased over 5 Mn pounds of organic greens.

It also stated that 65% of its produce suppliers use organic, transitional, or Integrated Pest Management (IPM) practices. Environmental and ethical concerns are further pushing organic demand. Producers in India are capitalizing on this trend by linking organic sourcing with local farmer support.

Rising Expenses and Falling Prices Compel Small Farmers to Exit the Segment

High production costs and low yields are limiting demand for organic fruits and vegetables as they affect both price and supply consistency. Since organic farming avoids synthetic fertilizers and pesticides, yields typically lag behind conventional farming, which makes each unit more expensive to produce. For consumers, this translates into high retail prices, which restricts organic purchases to more affluent or health-conscious buyers instead of the mass market.

The problem is more acute when production costs rise faster than selling prices. In 2024, U.S.-based organic corn growers faced a 20% increase in expenses while market prices fell by 14%, compelling some small farmers to leave the segment.

A similar squeeze applies to fruits and vegetables, where input costs for labor-intensive tasks such as hand weeding or pest control are high. However, retail competition prevents growers from passing on the full cost to consumers.

Institutional Investment in Soil Carbon Sequestration Opens New Revenue Streams

Institutional investors entering the market with a focus on soil carbon sequestration are creating new opportunities for organic fruits and vegetables by tying climate finance directly to farming practices. Instead of relying only on consumer willingness to pay a premium, growers often attract long-term funding by proving that their organic cultivation methods improve soil carbon storage.

This gives small and mid-sized farms a new revenue stream through carbon credits or sustainability-linked financing. For instance, in 2024, SLM Partners in Europe expanded its regenerative organic farmland fund, showcasing both food production and carbon benefits to investors.

The shift is further encouraging large-scale transitions to organic acreage. Farmers who were hesitant to switch due to high upfront costs now see institutional backing as a cushion. The capital allows them to invest in cover crops, composting systems, and agroforestry.

These help improve soil carbon while producing marketable organic fruits and vegetables. In California, a few vineyards and mixed farms have already tapped climate-focused funds to broaden their organic orchards and diversify into organic vegetables.

Category-wise Analysis

Fruits Insights

Based on fruits, the market is segregated into banana, apple, berries, grapes, kiwi, dragon fruit, passion fruit, and others. Among these, organic bananas are estimated to hold approximately 27.6% share in 2025 as they are one of the few fruits where the difference in cultivation practices is visible to consumers.

Conventional bananas are often grown in large monoculture plantations that rely heavily on pesticides due to high pest pressure in tropical climates. Organic bananas are cultivated with crop rotation, natural pest control, and healthy soil practices, which appeal to buyers concerned about chemical residues. Shoppers see bananas as a staple fruit consumed daily, so avoiding pesticide exposure feels more relevant.

Organic berries are poised to exhibit a considerable CAGR in the forthcoming years as they are one of the most pesticide-intensive fruits in conventional farming, and consumers are highly aware of this. Organic berries are often grown in small, soil-rich farms or controlled environments that focus on flavor rather than just yield.

Short shelf life has also worked in favor of organic berries. Retailers want to reduce waste and differentiate their produce aisles. Hence, they invest in supply partnerships with organic berry growers using improved packaging and cold-chain solutions.

Vegetables Insights

By vegetables, the market is divided into leafy vegetables, tomato, potato, sweet corn, asparagus, and others. Out of these, organic tomatoes are likely to account for about 27.8% of share in 2025 as consumers directly notice differences in taste, texture, and aroma compared to conventional ones.

Organic cultivation often emphasizes soil health and slow ripening, which produces tomatoes with strong flavor and natural sweetness. This sensory appeal has made organic tomatoes a favorite in Europe, where retailers such as Coop Switzerland point toward the superior taste of their organic cherry tomatoes to justify premium placement.

Organic leafy vegetables are anticipated to showcase steady growth through 2032 because they are highly perishable and eaten directly with minimal cooking, which makes consumers more sensitive to pesticide residues. Spinach, kale, and lettuce often rank high on lists of pesticide-heavy crops.

Hence, buyers see organic certification as a safe choice. This is evident in families with children, who often consume these greens in salads or smoothies. Retailers and foodservice chains are strengthening this trend by prominently featuring organic leafy greens in ready-to-eat salad mixes and meal kits.

Regional Insights

North America Organic Fruits and Vegetables Market Trends- Retail Giants Expand Private Label Organic Aisles to Provide Affordability

In 2025, North America is predicted to account for nearly 42.7% of share as the market is moving toward consolidation. Large growers and distributors are taking control of supply chains to ensure year-round availability. Companies such as NatureSweet are broadening their greenhouse and controlled-environment farming operations. These strategies enable them to deliver consistent organic produce even in off-season months.

In 2022, the U.S. Department of Agriculture (USDA) launched its Organic Transition Initiative with a funding of US$ 300 Mn. It was aimed at countering the earlier 11% decline in certified farmland and ensuring steady domestic production.

Walmart and Costco in the U.S. organic fruits and vegetables market have expanded their organic fresh produce aisles, often under private labels, making organic more affordable for mainstream shoppers. Similarly, Whole Foods is doubling down on exclusivity by promoting branded organic items with storytelling around farm origins and sustainability.

Europe Organic Fruits and Vegetables Market Trends- Regenerative Agriculture Initiatives Improve Credibility

In Europe, organic fruits and vegetables are influenced by strict regulations and consumer expectations around authenticity. Certification standards are tighter than in many other regions, and buyers actively look for EU organic logos as proof of credibility.

It has created an environment where small and mid-sized farms can compete with well-established players by highlighting regional specialties such as Tuscan tomatoes or Andalusian oranges grown under organic methods.

Germany-based discounters such as Lidl and Aldi have broadened their organic fresh produce assortments at affordable prices. This has made organic a mainstream option rather than just a premium category.

On the other hand, premium retailers such as Marks & Spencer and Carrefour are focusing on branded and provenance-based organics, often underlining local farm partnerships to differentiate from mass-market chains. In 2024, for instance, Carrefour launched initiatives linking organic vegetables to regenerative agriculture.

Asia Pacific Organic Fruits and Vegetables Market Trends- Distrust in Conventional Farming Propels Organized Organic Farms

Increasing demand from urban areas and concerns over food safety are creating new opportunities in Asia Pacific. China and India have seen rising middle-class consumption of organic produce. It is attributed to distrust in conventional farming practices that rely heavily on chemical pesticides.

This has created space for organized organic farms and direct-to-consumer delivery apps such as India’s Farmizen and China’s Meicai. These market trust and freshness as their most important selling points.

Retailers and e-commerce platforms are also heavily involved. Alibaba’s Freshippo in China and Japan’s Aeon stores have dedicated organic sections. These have made organic fruits and vegetables easily accessible to urban shoppers.

In India, BigBasket and Reliance Smart Bazaar now feature organic ranges, often sourced from certified local cooperatives. These platforms are blending convenience with transparency, propelling small farmers to adopt certification and traceability to remain competitive.

Competitive Landscape

The organic fruits and vegetables market is characterized by several large global players and small local growers. Big brands such as Driscoll’s are broadening their premium organic lines and buying regional farms to secure year-round supply and better control over quality.

This allows them to stand out in categories such as berries, where branding and taste-based differentiation create loyalty among consumers. Retailers are adding their own competition through private-label organic ranges. A few companies are further using coatings such as Apeel to expand shelf life and reduce waste, enabling imports to compete with local seasonal produce.

Key Industry Developments

- In September 2025, Farmland LP and Stemilt Growers declared a joint venture to broaden organic apple and cherry production in Washington’s Columbia Basin. Farmland LP aims to guide organic transition and land management, while Stemilt will serve as farm manager and post-harvest lead.

- In June 2025, Freshway Produce announced its participation in the upcoming Organic Produce Summit. The company planned to officially launch its new Organic Line and exhibit a wide portfolio of premium exotic fruits.

Companies Covered in Organic Fruits and Vegetables Market

- Amy's Kitchen

- General Mills Inc.

- The Hain Celestial Group

- Fresh Del Monte Produce Inc.

- Driscoll's, Inc.

- Dole Food Company, Inc.

- Organic Valley

- SunOpta, Inc.

- Danone S.A.

- Conagra Brands

- Healthy Buddha

- Mission Produce Inc.

- Others

Frequently Asked Questions

The organic fruits and vegetables market is projected to reach US$ 79.3 Bn in 2025.

Rising health consciousness and increasing food safety concerns are the key market drivers.

The organic fruits and vegetables market is poised to witness a CAGR of 8.8% from 2025 to 2032.

ESG-linked investments and retailer-exclusive supply contracts are the key market opportunities.

Amy's Kitchen, General Mills Inc., and The Hain Celestial Group are a few key market players.