- Transportation & Logistics

- Bicycle Market

Bicycle Market Size, Share, and Growth Forecast 2026 - 2033

Bicycle Market by Bike Category (Performance/Race, Mountain Bike (MTB)/Trekking, Gravel & Touring, City/Urban, Others (Cargo Bikes)), Bike Type (Muscular/Traditional, Electric), Price Range (Premium (Above US$ 1,000), Mid-range (US$ 500-1,000), Low-range (Below US$ 500)), End Use (Men, Women, Kids), Distribution Channel (Online Retailers, Direct-to-Consumer, Department Stores, Independent Bike Shops), and Regional Analysis, 2026 - 2033

Bicycle Market Size and Trend Analysis

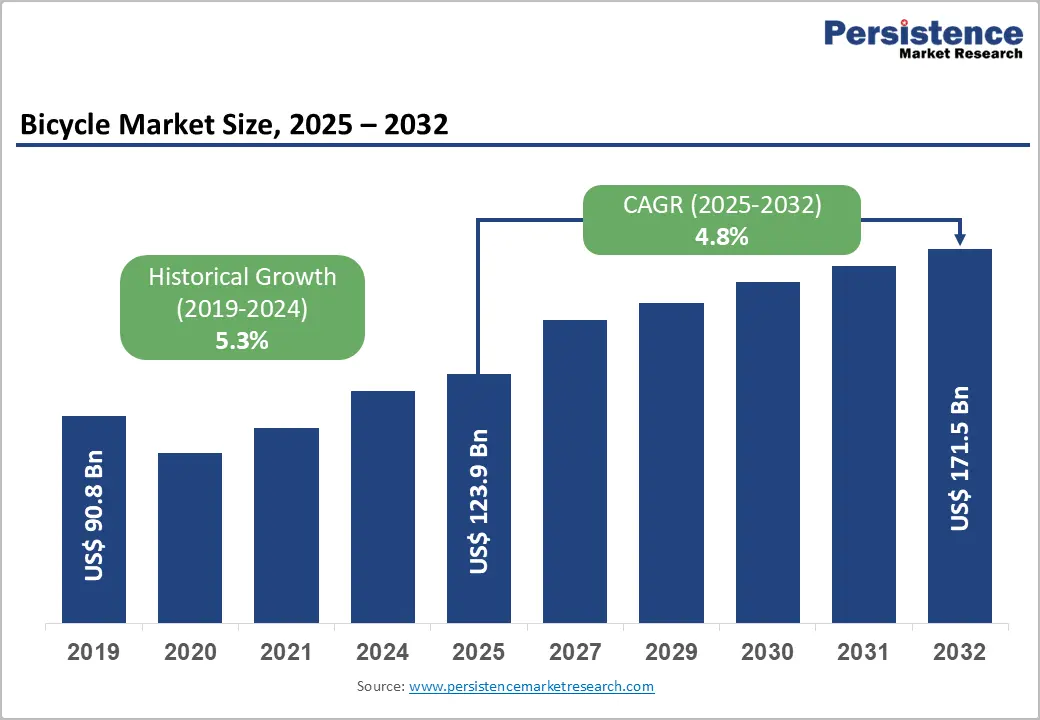

The global bicycle market size is expected to be valued at US$ 137.1 billion in 2026 and projected to reach US$ 185.3 billion by 2033, growing at a CAGR of 4.4% between 2026 and 2033.

This robust growth trajectory is primarily propelled by the convergence of three structural forces: the global pivot toward sustainable urban mobility, rapidly rising health and fitness consciousness among consumers, and accelerating government investment in cycling infrastructure.

The explosive adoption of electric bicycles, particularly across Europe and Asia Pacific, is expanding the addressable consumer base beyond traditional cycling demographics. Supportive policy frameworks, such as the European Union’s Sustainable and Smart Mobility Strategy and India’s FAME-II initiative, are generating durable, policy-backed demand that reinforces long-term market expansion.

Key Industry Highlights

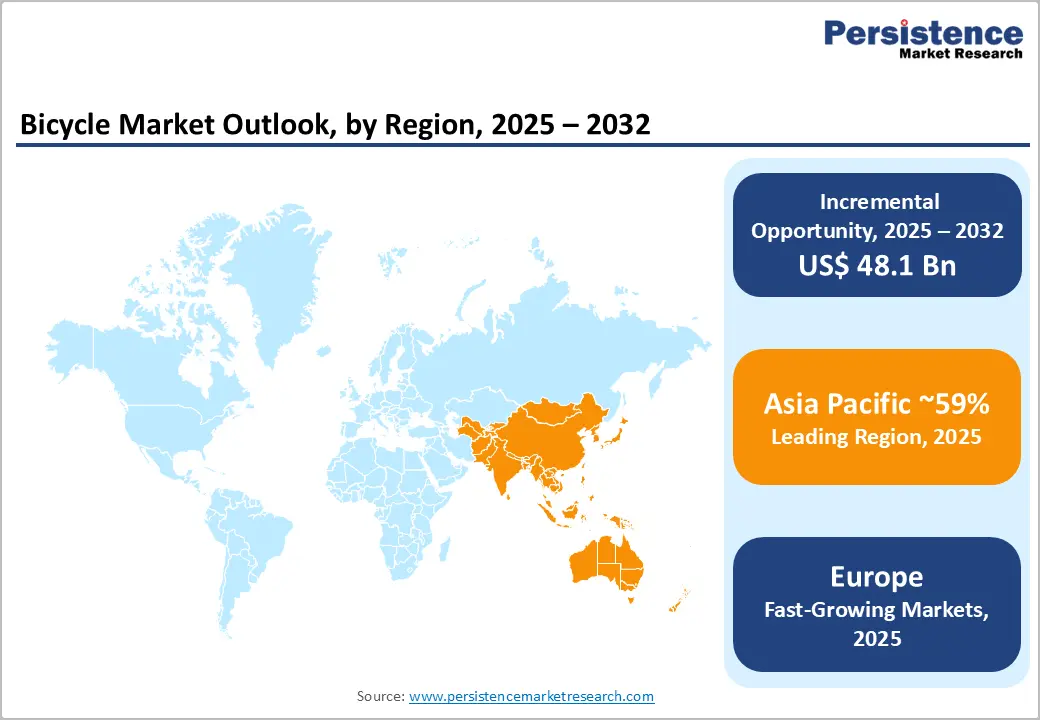

- Leading Segment: Asia Pacific leads the global Bicycle Market with approximately 59% revenue share in 2025, underpinned by China’s manufacturing scale, Japan’s urban cycling maturity, and high-growth demand in India and ASEAN nations, making it the world’s most strategically significant bicycle region for manufacturers and investors.

- Fastest Growing Segment: Asia Pacific is also the fastest-growing bicycle region in the 2026 - 2033 forecast period, fueled by India’s FAME-II e-mobility policies, expanding urban cycling infrastructure investment, and the dynamic proliferation of bicycle sharing programs integrating bicycles into multimodal urban transport ecosystems.

- Dominant Segment: Electric bicycles dominate by bike type with ~66% market share in 2025, driven by battery technology advances, government subsidy programs across Europe and Asia Pacific, and a broadening consumer base, cementing the e-bike segment as the single largest value contributor in the global bicycle industry.

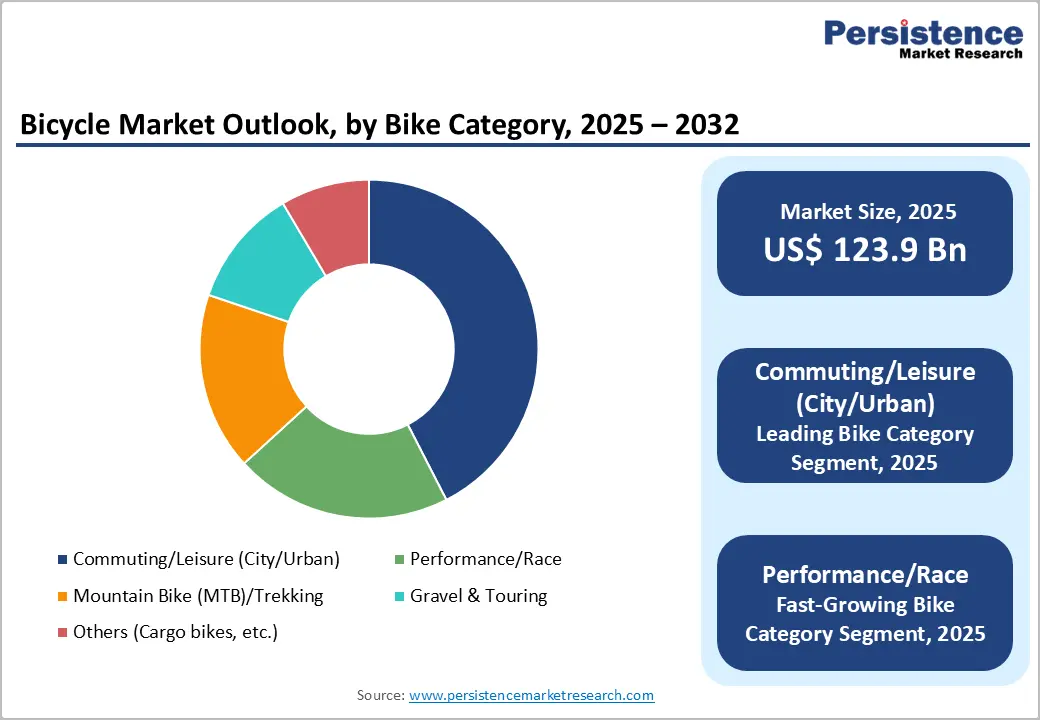

- Fastest Growing Segment: Gravel & Touring is the fastest-growing bike category in the 2026 - 2033 forecast period, propelled by surging global interest in bikepacking, multi-surface adventure cycling, and endurance sports tourism, attracting a new generation of versatile cyclists demanding performance bikes capable of both on-road and off-road exploration.

- Key Opportunity: Direct-to-Consumer distribution is the highest-growth channel opportunity, as demonstrated by Canyon Bicycles GmbH’s scalable DTC model; companies investing in digital commerce platforms, virtual fitting tools, subscription maintenance services, and community engagement strategies are positioned to capture significant margin improvement and long-term brand equity.

| Key Insights | Details |

|---|---|

| Bicycle Market Size (2026E) | US$ 137.1 Billion |

| Market Value Forecast (2033F) | US$ 185.3 Billion |

| Projected Growth CAGR (2026 - 2033) | 4.4% |

| Historical Market Growth (2020 - 2025) | 5.5% |

Market Dynamics

Drivers - Government-Led Urban Mobility Reforms and Infrastructure Investment

Government-mandated urban mobility reforms represent a foundational catalyst for sustained bicycle demand globally. The European Union’s Sustainable and Smart Mobility Strategy commits member states to doubling cycling modal share by 2030, with dedicated funding streams for protected cycling infrastructure. In the United States, the Infrastructure Investment and Jobs Act (2021) allocated over US$ 1 billion specifically toward pedestrian and bicycle pathway development. Municipal governments are actively redesigning urban streetscapes to prioritize non-motorized transport; Paris alone has expanded its cycling network by over 1,000 km through the landmark “Paris en Selle” program. These macro policy tailwinds directly amplify demand for city/urban bicycles and create complementary downstream growth across the Bicycle Apparel Market, as commuter cyclists invest in safety equipment, helmets, and performance-oriented clothing that drive incremental category expansion.

Driver 2: Surge in Health-Conscious and Recreational Cycling Participation

Rising global awareness of preventable chronic disease is fundamentally reshaping consumer behavior in favor of active transport and recreational cycling. The World Health Organization (WHO) identifies physical inactivity among the top four leading risk factors for global mortality, motivating millions of urban residents toward cycling as both exercise and daily commuting. Post-pandemic behavioral shifts have entrenched cycling as a habitual routine across Europe, North America, and Asia Pacific, with many first-time pandemic cyclists becoming permanent enthusiasts. The European Cyclists’ Federation (ECF) documented cycling participation increases of 20-30% across multiple EU member states during the pandemic period, with a significant proportion of new riders sustaining the habit thereafter. Growing investment in organized cycling events, sports tourism, cycling apps, and wearable performance tracking further cements recreational cycling as a mainstream wellness activity supporting durable long-term demand.

Restraints - High Purchase Cost of Premium and Electric Bicycles

The elevated price point of premium and electric bicycles constitutes a significant barrier to broad-based adoption, particularly across price-sensitive markets in Latin America, Sub-Saharan Africa, and parts of Southeast Asia. Quality e-bikes typically retail between US$ 1,500 and US$ 10,000, substantially exceeding the financial capacity of large consumer segments in developing economies. Even within mid-income markets, the total cost of bicycle ownership, encompassing safety gear, replacement components from the Bicycle Tires Market, and routine servicing, adds meaningful financial friction. This affordability gap bifurcates the global market, concentrating premium revenue growth among high-income demographics in North America and Western Europe while limiting volume growth in emerging regions, thereby constraining overall market penetration depth and slowing adoption velocity in high-population, high-potential geographies.

Insufficient Cycling Infrastructure in Emerging and Developing Markets

The absence of safe, dedicated cycling infrastructure remains a primary impediment to bicycle adoption across many emerging markets. The International Transport Forum (ITF) has consistently identified the lack of protected cycling lanes as the leading behavioral barrier preventing potential cyclists from committing to bicycle commuting. In high-population markets such as India, Brazil, and Indonesia, a substantial majority of arterial roads lack segregated bicycle pathways, exposing riders to significant traffic safety risks. Inadequate secure parking facilities, poor road surface conditions, and limited public awareness campaigns collectively deter adoption among women, elderly users, and families considering bicycles for their children. This infrastructure deficit restricts market development in demographically large nations with strong underlying demand potential, creating a structural ceiling on volume growth and urban cycling adoption rates.

Opportunities - E-Bike Market Expansion Backed by Policy Incentives and Technological Innovation

The surging e-bike market presents the most transformative and immediate growth opportunity for bicycle industry participants in the forecast period. Electric bicycles are redefining urban mobility economics, with the European Commission estimating that e-bikes could displace up to 10% of total car journeys within European urban environments by 2030. Government incentive architectures are accelerating consumer uptake: Germany’s environmental bonus programs, France’s “Bonus Vélo” scheme, and the Netherlands’ employer bicycle tax benefit framework have collectively driven e-bike sales to record highs. In Asia Pacific, India’s FAME-II policy and China’s deeply integrated two-wheeler electrification supply chain create manufacturing and distribution advantages at scale. Industry participants investing in next-generation lightweight battery systems, mid-drive motor efficiency, integrated smart connectivity, and affordable entry-level e-bike variants are best positioned to capture disproportionate revenue share from this high-velocity segment.

Direct-to-Consumer Digital Commerce and Fleet Supply for Shared Mobility Networks

The maturation of direct-to-consumer (DTC) digital commerce channels and the explosive growth of urban shared mobility infrastructure collectively create a dual-track revenue opportunity for forward-looking bicycle companies. Canyon Bicycles GmbH has demonstrated through its DTC-only global business model that online-first bicycle retailing can achieve premium brand positioning and scalable international revenue without reliance on traditional dealer networks. The burgeoning Bicycle Sharing Market and the broader micro-mobility market are generating significant B2B fleet procurement demand from municipalities, corporate campuses, and mobility-as-a-service (MaaS) operators. Companies investing in proprietary digital experience platforms, virtual bike-fitting technology, community-led content marketing, and subscription-based maintenance programs can structurally improve customer lifetime value while building resilient brand ecosystems that attract and retain high-value, digitally native cycling enthusiasts.

Category-wise Analysis

Bike Category Insights

The City/Urban segment commands a dominant position within the global bicycle market by bike category, accounting for approximately 37% of total market share in 2025. This sustained leadership is directly tied to accelerating global urbanization, the United Nations projects that 68% of the world’s population will reside in urban areas by 2050, which amplifies demand for practical, ergonomically optimized commuting solutions. City/urban bicycles, engineered with upright riding geometry, integrated lighting systems, mudguards, and rear cargo racks, have become the preferred last-mile connectivity vehicle across densely populated metropolitan areas in Europe, East Asia, and North America. Government-mandated low-emission zones in cities such as Amsterdam, Copenhagen, London, and Paris are compelling commuters to substitute motor vehicles with bicycles, establishing urban cycling as a structural megatrend that will sustain this segment’s market leadership throughout the forecast horizon.

Bike Type Insights

Electric bicycles have established decisive dominance in the global bicycle market by bike type, capturing approximately 66% of total market share in 2025. This commanding position reflects the superior utility value proposition that e-bikes deliver, enabling extended commuting ranges, effortless navigation of hilly terrain, and reduced physical exertion, which effectively broadens the cycling demographic to include older adults, less physically active consumers, and longer-distance commuters. The e-bike market has been transformed by continuous innovation in mid-drive motor systems, wireless gear-shifting integration, and smart battery management, substantially enhancing performance and reliability. Confederation of the European Bicycle Industry (CONEBI) data confirms that electric bicycles have accounted for the majority of total bicycle sales by value in leading EU markets, including Germany, Netherlands, and Belgium, since 2021, underscoring electric’s structural, long-term supremacy across the global bicycle landscape.

Price Range Insights

The premium price segment, encompassing bicycles priced above US$ 1,000, dominates the global bicycle market by revenue contribution, holding approximately 64% of total market share in 2025. This disproportionate value share is a direct consequence of the significantly higher average selling prices commanded by premium bicycles, which include high-specification e-bikes, carbon-fiber road racing bikes, and elite mountain bicycles, relative to mid-range and entry-level alternatives. The segment’s leadership is further reinforced by a growing cohort of affluent lifestyle cyclists in North America and Western Europe who regard premium bicycles as both performance instruments and status expressions. Brands such as Specialized Bicycle Components, Inc., Trek Bicycle Corporation, BMC Switzerland AG, and Cicli Pinarello S.p.A. have methodically curated premium portfolios incorporating aerodynamic engineering, proprietary component integration, and concierge-level fitting services to sustain loyalty among high-value clientele.

End-user Insights

The men’s end-use segment leads the global bicycle market, representing approximately 57% of total market share in 2025. Male consumers constitute the core buyer base across the performance/race, mountain biking, and gravel touring categories, driven by historically higher participation rates in competitive cycling, endurance sports, and adventure riding. The Union Cycliste Internationale (UCI), the sport’s global governing body, consistently reports that men represent the majority of registered competitive cyclists worldwide, reflecting broader patterns of gendered sports participation that ripple through consumer purchasing behavior. However, the gender gap is progressively narrowing as institutional investment in women’s cycling competitions increases visibility and participation. Brands including Trek Bicycle Corporation and Specialized Bicycle Components, Inc. have significantly expanded dedicated women’s lines. Simultaneously, the Kids segment is demonstrating the strongest growth momentum in the forecast period, driven by parental emphasis on childhood health, active outdoor lifestyles, and school cycling promotion programs.

Distribution Channel Insights

Independent Bike Shops (IBS) retain clear channel leadership in bicycle distribution, accounting for approximately 45% of total channel share in 2025. Their market dominance is underpinned by the irreplaceable value of specialist expertise, personalized professional fitting services, in-store test ride experiences, and ongoing after-sales maintenance, factors that are particularly critical for consumers purchasing mid-range and premium bicycles requiring technical guidance. The National Bicycle Dealers Association (NBDA) in the United States has consistently documented that consumer confidence in specialist retail guidance remains a primary determinant of channel preference, especially for first-time premium buyers and technically engaged cyclists. While Independent Bike Shops maintain the highest share, the Direct-to-Consumer channel is the fastest-growing distribution model, as leading brands invest in sophisticated proprietary e-commerce platforms, digital configuration tools, and home delivery services to capture margin improvement and cultivate direct, data-rich consumer relationships.

Regional Insights

North America Bicycle Market Trends and Insights

The United States anchors North American bicycle demand, supported by a deeply entrenched culture of recreational trail cycling, competitive racing, and expanding urban commuter cycling adoption. The Outdoor Industry Association (OIA) has estimated that cycling generates over US$ 6 billion in annual retail sales activity in the U.S., reflecting the sector’s significant economic weight. Federal investment under the Infrastructure Investment and Jobs Act continues to fund multi-use trail expansions and protected urban cycling lanes across major metropolitan areas, structurally supporting long-term demand. Canada contributes meaningfully to regional performance, with year-round cycling gaining notable traction in progressive cities including Vancouver, Montreal, and Ottawa.

North America remains a global nucleus for cycling innovation. Specialized Bicycle Components, Inc. and Trek Bicycle Corporation, both headquartered in the region, consistently advance product development in carbon-fiber fabrication, electric drivetrains, and AI-integrated performance technologies. The rising popularity of gravel cycling and bikepacking is creating a new, rapidly scaling consumer segment. Simultaneously, the expanding bicycle sharing market in cities such as New York, Chicago, and San Francisco is catalyzing entry-level demand among urban residents seeking sustainable last-mile connectivity solutions integrated with broader public transit networks.

Europe Bicycle Market Trends and Insights

Europe represents the world’s most institutionally supported and structurally mature cycling market, characterized by robust demand across electric, performance, and urban bicycle categories. Germany leads continental performance, with the Zweirad-Industrie-Verband (ZIV) reporting annual e-bike unit sales consistently exceeding two million, establishing it as Europe’s largest e-bike market by volume. The Netherlands and Denmark sustain the world’s highest per-capita cycling rates, underwritten by decades of dedicated infrastructure investment and urban planning centered on cycling. France and Spain are accelerating adoption through national subsidy programs, with cities such as Barcelona, Seville, and Lyon emerging as European cycling model cities.

The European Green Deal and the EU Urban Mobility Framework are driving regulatory harmonization across member states, mandating cycling infrastructure as a core component of national decarbonization strategies. The United Kingdom continues to pursue ambitious cycling expansion targets through its Cycling and Walking Investment Strategy (CWIS). Demand for premium e-bikes, gravel bicycles, and performance road bikes remains particularly strong across Western Europe, creating significant opportunities for brands operating in both the core bicycle segment and adjacent categories, including the growing Bicycle Apparel Market, as rising cycling participation drives parallel accessories demand.

Asia Pacific Bicycle Market Trends and Insights

Asia Pacific commands both the largest and fastest-growing regional position in the global bicycle market, accounting for approximately 59% of worldwide revenue share in 2025. China anchors this dominance as both the world’s foremost bicycle manufacturing nation and an immense domestic consumer market, with its mature two-wheeler electrification ecosystem sustaining extraordinary e-bike production and sales volumes. Japan represents a sophisticated, high-quality urban cycling market characterized by strong commuter cycling traditions, government-supported cycle path development, and growing recreational participation. India is rapidly emerging as a high-growth frontier, energized by the FAME-II policy, expanding fitness culture among the urban middle class, and the substantial domestic manufacturing capability of Hero Cycles Limited.

ASEAN nations including Vietnam, Indonesia, Thailand, and Malaysia are experiencing accelerating bicycle demand, driven by demographic youth bulges, urbanization-fueled traffic congestion, and expanding municipal bicycle sharing programs in cities such as Bangkok, Jakarta, and Ho Chi Minh City. Asia Pacific’s structural manufacturing advantages, anchored in concentrated supply ecosystems in China, Taiwan, and India, provide global cost competitiveness, positioning the region as the dual engine of worldwide bicycle supply and consumption growth through 2033.

Competitive Landscape

The global bicycle market exhibits a moderately fragmented structure, characterized by the presence of multinational manufacturers, vertically integrated original design manufacturers, and niche premium brands. Leading players leverage strong supply chain integration, global distribution networks, and continuous investment in product innovation, particularly in electric drivetrains, lightweight materials, and smart connectivity features to maintain competitive advantage.

Competition is increasingly shaped by evolving business strategies such as direct-to-consumer sales models, which enhance margins and customer engagement, and vertical integration into proprietary components to improve cost control and differentiation. Companies are also focusing on expanding their presence in the fast-growing e-bike segment through partnerships, acquisitions, and technology development. Additionally, collaborations with urban mobility platforms and participation in shared mobility ecosystems are emerging as key strategies to tap into institutional demand and generate recurring revenue streams.

Key Developments:

- February 2026: Haro launched two new carbon mountain bike models, the Daley and Greer, featuring lightweight carbon frames, multiple build options with SRAM and Shimano drivetrains, and enhanced performance while retaining proven suspension platforms and geometry.

- September 2025: Liv Cycling introduced the Tempt E+ line of e-bikes, featuring women-specific design, ALUXX aluminum frames, 100mm suspension, and SyncDrive motors with 430Wh batteries, targeting versatile use across commuting and trail riding with integrated smart connectivity features.

- January 2025: Aoki Mobility launched a new range of electric bicycles aimed at promoting sustainable urban transport, featuring lightweight designs, extended battery range, and smart connectivity features to cater to growing demand for eco-friendly and last-mile mobility solutions in India.

Companies Covered in Bicycle Market

- Shimano Inc.

- Pon Holding B.V.

- Giant Manufacturing Co. Ltd

- Trek Bicycle Corporation

- Merida Industry Co., Ltd.

- Scott Sports SA

- Canyon Bicycles GmbH

- Specialized Bicycle Components, Inc.

- F.I.V.E. Bianchi S.p.A.

- Cicli Pinarello S.p.A.

- Colnago Ernesto & C. S.r.l.

- Factor Bikes

- BMC Switzerland AG

- Hero Cycles Limited

- Accell Group N.V.

- Cube Bikes (Radsportvertrieb Nessetal GmbH)

- Riese & Müller GmbH

- Brompton Bicycle Ltd.

- Cannondale (Dorel Sports)

- Atlas Cycles Ltd.

- Derby Cycle Holding GmbH

- SRAM Corporation

- Rad Power Bikes

- Cannondale

- Cervelo Bicycles

- Decathlon

- Liv Cycling

- Haro Cycles

- Aoki Mobility

- Polygon Bikes

Frequently Asked Questions

The global Bicycle Market is valued at US$ 137.1 billion in 2026 and is projected to grow at a CAGR of 4.4% through 2033.

Demand is driven by government-backed sustainable mobility initiatives and increasing health-conscious and recreational cycling adoption.

Asia Pacific leads with around 59% share due to strong manufacturing in China, rising e-bike adoption in India, and expanding cycling infrastructure across the region.

Key opportunities include growth in e-bikes, expansion of direct-to-consumer channels, and rising demand from bicycle sharing and micro-mobility platforms.

The global Bicycle Market is led by prominent companies including Shimano Inc., Giant Manufacturing Co. Ltd, Trek Bicycle Corporation, Specialized Bicycle Components, Inc., Pon Holding B.V., Merida Industry Co., Ltd., Canyon Bicycles GmbH, Scott Sports SA, BMC Switzerland AG, etc.