- Automotive Components & Materials

- Bicycle Bearings Market

Bicycle Bearings Market Size, Share, and Growth Forecast, 2026 - 2033

Bicycle Bearings Market by Bearing Type (Ball Bearing, Roller Bearing, Plain Bearing), by Bicycle Type (Road Bicycle Bearings, Electric Bicycle Bearings, Mountain Bike Bearings, Hybrid Bike Bearings, Comfort Bicycle Bearings, Cruiser Bicycle Bearings, and Youth Bicycle Bearings), by Sales Channel (OEM, and Aftermarket), Application, and Regional Analysis for 2026 - 2033

Bicycle Bearings Market Size and Trends Analysis

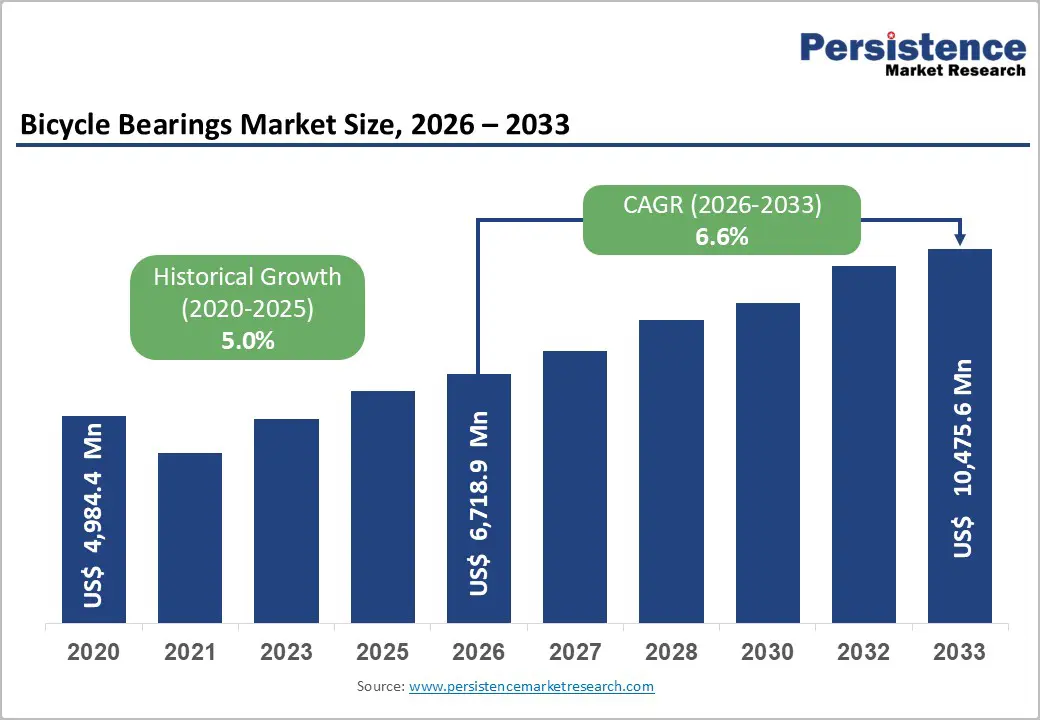

The global bicycle bearings market is likely to be valued at US$ 6.72 billion in 2026 and is projected to reach US$ 10.48 billion by 2033, expanding at a CAGR of 6.6% between 2026 and 2033.

The market has grown from approximately US$ 4.98 Bn in 2020, reflecting a historical CAGR of around 5.0%, primarily driven by strong bicycle and e-bike demand during and after the pandemic. This growth is closely aligned with the expansion of the global bicycle market, which is expected to reach US$ 123.9 Bn by 2025 and further grow at US$ 171.5 billio by 2032. Increasing urbanization, environmental awareness, and government initiatives promoting sustainable mobility continue to boost bicycle adoption worldwide. The integration of cycling infrastructure in smart cities, the expansion of bike-sharing systems, rising health consciousness, and the growing use of cargo bikes for last-mile delivery are further strengthening overall industry momentum.

Global bicycle and e-bike production reached nearly 193 million units in 2021, with China accounting for about 63%, creating a large installed base that continuously drives replacement and OEM demand for wheel hub, bottom bracket, headset, suspension, and drivetrain bearings. Moreover, the rapidly growing e-bike market, valued at US$ 79.5 billion in 2025 and projected to reach US$ 129.3 billion by 2032. This sustained growth is significantly driving demand for advanced, high-performance bearings designed to withstand heavier loads, higher torque levels, and enhanced durability requirements associated with electric drivetrains.

Key Industry-Highlights:

- Market size and growth: The bicycle bearings market is expected to grow from about US$ 6.72 Bn in 2026 to US$ 10.48 Bn by 2033, at a CAGR of 6.6%, up from a historical growth rate of 5.0%.

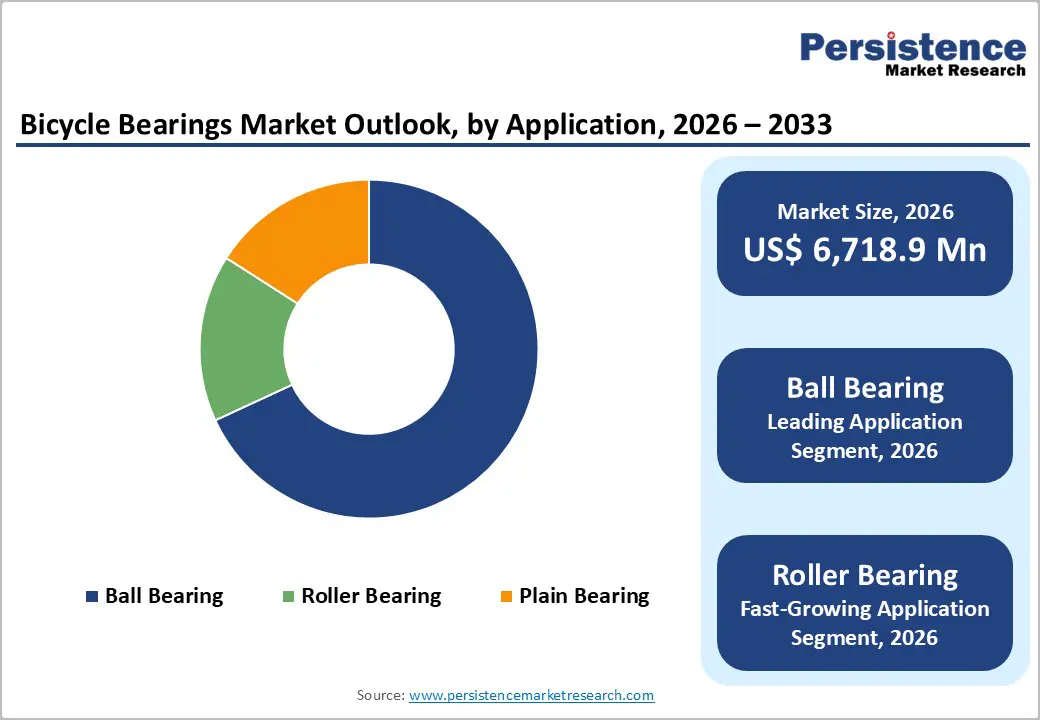

- Bearing Type Analysis: Ball bearings hold above 65% share, while roller bearings are the fastest-growing type with around 7.1% CAGR, reflecting higher-load e-MTB and cargo applications.

- Bicycle types of Analysis: Road bicycle bearings account for over 32% of revenue, while e-bike bearings are expanding at roughly 7.0% CAGR, supported by a global e-bike market CAGR of 13.4%.

- Sales channels Analysis: OEM sales exceed 65% of revenue, but the aftermarket channel is growing faster at about 7.3% CAGR, driven by premium upgrades and performance-oriented consumers.

- Applications Analysis: Wheel hub bearings contribute more than 40% of revenue, while bottom bracket bearings show the highest growth, at around 7.5% CAGR, driven by a focus on drivetrain efficiency and standard fragmentation.

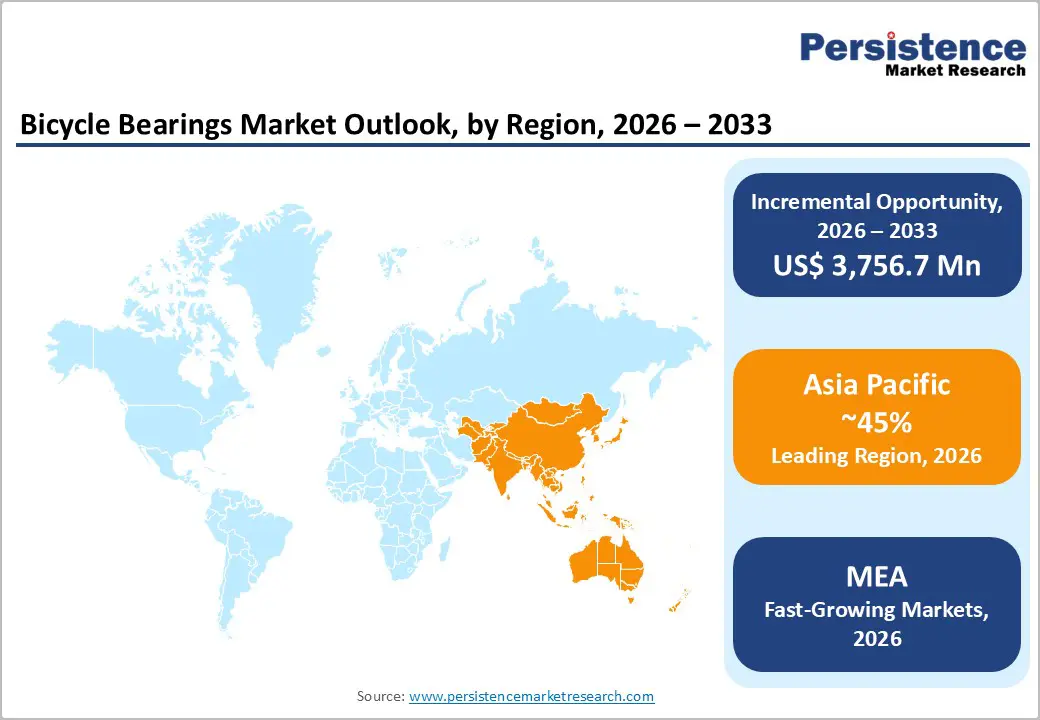

- Regional leadership: Asia Pacific commands above 45% of global revenue, anchored by China and India’s production and demand, whereas the Middle East and Africa region is projected to be the fastest-growing with about 7.3% CAGR.

- Strategic developments: Recent moves by Enduro Bearings and CeramicSpeed to deepen global reach and expand high-performance product portfolios, coupled with €3.21–4.5 Bn of EU cycling infrastructure funding through 2027, are reshaping long-term demand patterns and reinforcing the premiumization and regional diversification of the bicycle bearings market.

| Key Insights | Details |

|---|---|

|

Bicycle Bearings Market Size (2026E) |

US$ 6,718.9 Mn |

|

Market Value Forecast (2033F) |

US$ 10,475.6 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

6.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.0% |

Market Dynamics

Key Growth Drivers

Rising bicycle and e-bike adoption as sustainable mobility

Global sales of bicycles and e-bikes reached roughly 136 million units in 2021, with total annual production around 193 million units, indicating structural growth in cycling as a transport and leisure mode. Independent compilations of industry data suggest more than 256 million bicycles were sold worldwide in 2021, reflecting both commuter and recreational demand across major regions. At the same time, the global e-bike market is expanding rapidly from about US$ 39.7 Bn in 2022 to a projected US$ 108.6 Bn by 2030, at 13.4% CAGR multiplying bearing content per unit because of additional motor, drivetrain and pivot points. This combination of high unit volumes and increasing bearing intensity per vehicle directly supports sustained growth in OEM and aftermarket bicycle bearings, particularly for wheel hubs, bottom brackets and suspension systems.

Urban cycling infrastructure and pro-cycling policy support

Cycling is benefiting from targeted public investment in active mobility infrastructure, which increases usage intensity and replacement cycles for bicycle components and bearings. In the European Union, structural and cohesion funds earmarked about €3.21 Bn for cycling projects in the 2021–2027 period, a 30% increase over the prior funding cycle and expected to support roughly 12,000 km of cycling infrastructure. The European Commission’s dedicated progress report on its cycling declaration indicates that €4.5 Bn will be directed toward cycling between 2021 and 2027, including €3.2 Bn from EU funds and an estimated €1.3 Bn from national recovery plans. Similar active-mobility investments are visible in large cities worldwide, where protected bikeways and urban trail networks are expanding to support modal shift and public health objectives. These policy-driven shifts increase real-world mileage per bike, tighten maintenance cycles and push OEMs and aftermarket suppliers toward higher-quality, better-sealed bearings to withstand year-round commuting conditions.

Market Restraining Factors

Industry Cyclicality and Premium Bearing Adoption Constraints

The bicycle bearings market faces restraints stemming from industry cyclicality and limitations on premium products. Following the pandemic-driven surge, the bicycle industry has entered a correction phase marked by significant inventory overhang. In 2021, global bicycle and e-bike production reached 193 million units, exceeding sales of 136 million units and creating a surplus of over 57 million units, nearly 30% of annual output. This imbalance has led to discounting, cautious OEM procurement, and slower component restocking cycles, directly affecting short-term demand and pricing stability.

Additionally, high-end ceramic and ceramic-hybrid bearings, though favored in performance cycling for their low friction, remain constrained by high costs and durability concerns. Their premium pricing, potential brittleness, and shorter service life compared to steel alternatives limit mass-market adoption. As a result, most OEMs continue to prioritize cost-effective steel and stainless-steel bearings, thereby restricting the widespread adoption of advanced ceramic solutions.

Bicycle Bearings Market Trends and Opportunities

Premiumization in performance, e-MTB, gravel and commuting segments

There is a clear opportunity to capture higher margins through a premium bicycle-specific bearing systems that combine low friction with long life and robust sealing. Enduro, for example, has developed XD15 ceramic-hybrid bearings using a nitrogen-infused stainless alloy that offers exceptional corrosion resistance and is sold with lifetime guarantees for bottom brackets, wheel hubs and headsets. CeramicSpeed similarly focuses on high-precision ceramic bearings and optimized drivetrain components aimed at racing and performance cyclists, distributing to more than 50 countries from its Danish base. As the broader cycling industry is projected to roughly double in value by the late 2020s, these high-end segments can support a disproportionate share of bearing revenue and profit pools for suppliers that can demonstrate measurable watt savings and significantly extended maintenance intervals.

Bicycle Bearings Market Insights and Trends

Bearing Type Insights

Ball Bearings Lead Revenue While Roller Segment Gains Momentum

Ball bearings dominate the bicycle bearings market, accounting for above 65% of revenue in 2026, driven by their widespread use in wheel hubs, bottom brackets, headsets, pedals and gear mechanisms across all bicycle categories. Their balance of low friction, cost-effectiveness and mature manufacturing base among global suppliers such as SKF, NTN, NSK and others sustains their leadership and underpins predictable OEM sourcing models.

The roller bearing segment is the fastest-growing, projected to expand at a CAGR of around 7.1%, driven by high-load applications, especially in e-MTB, cargo bikes and suspension pivots demand higher radial load capacity and stiffness. Suppliers are increasingly engineering roller and full-complement designs tailored to the uneven loads and contamination typical of mountain and gravel riding, building on innovations such as Enduro’s MAX full-complement bearings. Over the forecast period, this segment will gain share in premium and utility applications where durability and load handling outweigh minimal friction gains.

Bicycle Type Insights

Road Segment Leads While Electric Bicycle Bearings Accelerate Growth

Road bicycle bearings hold a dominant share exceeding 32%, reflecting the long-standing prevalence of road bikes in global sales and their continued importance in enthusiast and performance segments. High-end road bikes often use multiple cartridge bearings in hubs, bottom brackets, headsets and jockey wheels, and their owners show a higher propensity to upgrade to premium ceramic or stainless options, supporting healthy aftermarket demand.

The electric bicycle bearings segment is the fastest-growing, with an estimated CAGR of about 7.0%, underpinned by the broader e-bike market’s 13.4% CAGR between 2022 and 2030. E-bikes require more and higher-spec bearings in motors, mid-drive units, rear hubs and suspension linkages, while heavier system weights accelerate wear, shortening replacement cycles relative to conventional bikes. As e-bikes gain share in Europe, Asia and North America, specialized sealing, thermal performance and load-optimized bearings will increasingly differentiate suppliers in this segment.

Sales Channel Insights

OEM Channel Leads Revenue While Aftermarket Shows Strongest Growth

OEM sales account for more than 65% of bicycle bearing revenue, as large-volume contracts with bicycle and e-bike manufacturers secure recurring demand across model years. Global industrial bearing majors such as SKF and other multinational brands leverage their manufacturing scale, quality systems and global distribution networks to serve OEM platforms, particularly in Asia and Europe, where most bicycle assembly is concentrated.

The aftermarket channel is the fastest-growing, with an indicative CAGR of about 7.3%, as riders increasingly upgrade to premium bearings for performance, durability or noise reduction. Boutique brands like Enduro and CeramicSpeed have built strong positions in hubs, bottom brackets, headsets and pulley wheels, targeting enthusiasts and competitive cyclists through specialized retailers and online channels. This channel also benefits from rising awareness of bearing performance and the proliferation of service shops offering bearing refresh packages, especially in urban and high-income markets

Application Insights

Wheel Hubs Dominate Applications While Bottom Brackets Drive Growth

Wheel hub bearings represent the largest application, with above 40% revenue share, because every bicycle uses at least two hub assemblies and many higher-end wheels integrate multiple cartridge bearings for stiffness and low drag. The critical safety role of wheel hubs, combined with direct ride-feel implications, encourages OEMs and riders to prioritize reliable, corrosion-resistant bearings in this location, supporting steady replacement demand.

Bottom bracket bearings are the fastest-growing application, with an estimated CAGR of roughly 7.5%, as riders increasingly perceive drivetrain efficiency as a differentiator and as OEM bottom bracket standards fragment (e.g., various press-fit and threaded systems). Enduro’s Torqtite threaded press-fit solutions and Maxhit bottom brackets, as well as CeramicSpeed’s premium bottom bracket offerings, illustrate the shift toward purpose-designed, high-precision units that improve alignment and reduce noise and friction. This trend is especially pronounced in road, gravel and e-MTB categories, where torque loads and rider expectations are highest.

Propulsion Type Insights

Electric Propulsion Dominates Revenue While Hybrids Drive Growth

Battery-Electric propulsion systems command a revenue share above 55%, reflecting technological maturity, regulatory acceptance, and alignment with sustainability objectives across aviation authorities. Battery-electric platforms demonstrate superior energy efficiency (85-92% drivetrain efficiency) and dramatically lower operational noise compared to conventional aircraft. Manufacturing simplicity of electric propulsion systems enables cost reduction and rapid production scaling.

Hybrid-Electric propulsion is the fastest-growing category, with a 32% CAGR, addressing extended-range requirements and operational flexibility for longer-duration missions. Hybrid systems combine battery-electric and conventional-fuel power, enabling 4-8 hour mission durations compared to 1-2 hour battery-only mission durations. This segment captures applications requiring intermediate range and extended endurance, including regional medical services and search-and-rescue operations.

Regional Insights and Trends

Asia Pacific Leads Market Driven by Manufacturing Scale and E-Bike Demand

Asia Pacific is the dominant region, accounting for above 45% of global bicycle bearings revenue, driven by its role as the manufacturing center of the global bicycle industry and by large domestic markets in China, India and Southeast Asia. China produced about 122 million bicycles and e-bikes in 2021, accounting for 63% of global production, while India purchased over 39 million bicycles in 2022.

Many global bearings majors and regional specialists operate manufacturing or assembly plants across China, Taiwan and Southeast Asia, supplying global bicycle OEMs and wheel manufacturers. Asia Pacific also leads the global e-bike market by volume, particularly in China, where more than 41 million e-bikes were purchased in 2021, intensifying demand for higher-load bearings in motors and drivetrains. The region’s regulatory environment supports electric mobility and micromobility while also driving stronger product safety and quality standards, especially for export-oriented OEMs. Competition includes global groups (SKF, NTN, NSK) alongside Chinese and Taiwanese specialists such as FHD Bearings, which positions itself as a leading Chinese producer of high-performance bicycle bearings serving OEM and aftermarket customers worldwide.

Europe Strengthens Position Through Policy Support and E-Bike Expansion

Europe is a core region for bicycle and e-bike demand, with countries like Germany, the Netherlands and France posting some of the highest per-capita cycling rates and strong market values (e.g., Germany’s bicycle market reached €6.56 Bn in 2021). The Czech Republic, Portugal, Italy and others are important manufacturing hubs, supplying both EU and export markets. Policy support is robust: EU structural funds are expected to deliver about €3.21 Bn of cycling investments between 2021 and 2027, while the European Commission’s cycling declaration progress report highlights €4.5 Bn in cycling-related spending and over 12,000 km of new or upgraded cycle paths. This regulatory and funding backdrop enhances the business case for durable, sealed bearings that can withstand year-round urban use. Competitive dynamics feature a strong presence of European industrial bearing groups, such as SKF (Sweden) and Schaeffler’s FAG/INA brands (Germany), alongside performance specialists like CeramicSpeed, headquartered in Holstebro, Denmark, which assembles bearings by hand and distributes them to more than 50 countries. Investment opportunities include supplying e-bike-specific bearings to leading European OEMs, partnering with local wheel and drivetrain brands, and leveraging EU sustainability programs to qualify for green mobility procurement

Middle East and Africa Emerges as Fastest-Growing Market

The Middle East and Africa (MEA) is projected to be the fastest-growing regional market for bicycle bearings, expanding at an estimated CAGR of 7.3% during 2026–2033. Growth is driven by rapid urbanization, rising congestion, and government initiatives promoting active mobility and micromobility solutions. Programs such as Saudi Arabia’s Vision 2030, including Riyadh’s 135 km Sports Boulevard cycling corridor, are strengthening long-term demand for durable wheel hub, bottom bracket, and steering bearings as fleet sizes increase.

MEA is also witnessing expansion in shared micromobility and e-mobility ecosystems. The regional bike-sharing market, valued at approximately US$ 273 million in 2022, continues to grow steadily, while broader smart-mobility revenues are expected to more than double by 2033. In Africa, increasing adoption of electric bicycles for commuting and delivery services further supports demand for high-performance, load-bearing components.

Bicycle Bearings Market Competitive Landscape

The bicycle bearings market is moderately fragmented, combining global industrial bearing majors with specialized cycling-focused brands. General-purpose bearing manufacturers such as SKF, NTN, FAG/INA (Schaeffler), NSK, Timken, Koyo and Nachi are identified as leading global brands and supply a significant share of OEM bicycle and e-bike platforms worldwide. Alongside these players, boutique cycling specialists such as Enduro Bearings and CeramicSpeed focus on high-performance applications, premium materials and customized solutions for hubs, bottom brackets, headsets and suspension pivots. Market concentration is higher in premium aftermarket niches than in mass-market OEM supply, where numerous regional manufacturers in China and Southeast Asia compete on cost.

Key Industry Developments

- In 2024, Enduro Bearings, operating as a DBA of ABI Industries, continues to consolidate its position as a cycling-focused bearing specialist, with operations based in California and Singapore and a portfolio spanning over 1,000 cycling-specific bearings and components.

- In 2024, CeramicSpeed, headquartered in Holstebro, Denmark, has continued to expand its international footprint, with offices across Europe, Asia and the Americas and distribution into more than 50 countries for both sports and industrial applications. Building

- In Nov 2022, Schaeffler and the CERATIZIT Group had a deal in place for the purchase of CERASPIN. CERASPIN has more than 25 years of experience in the design and production of premium ceramic materials, the majority of which are transformed into rolling components for different bearing applications.

- In Feb 2022, Schaeffler develops bearings for electromobility and expands its bearings business. Compared to normal bearings with two ball-bearing rows, the Schaeffler TriFinity triple-row bearing is more robust and has a longer service life. The face spline design paves the possibility for large bearing diameter reductions.

Companies Covered in Bicycle Bearings Market

- SKF Group

- NSK Ltd.

- NTN Corporation

- The Timken Company

- Schaeffler Group

- JTEKT Corporation

- MinebeaMitsumi Inc.

- RBC Bearings

- C&U Group

- ZWZ Group

- Nachi-Fujikoshi Corp.

- CeramicSpeed

- Enduro Bearings

- Kogel Bearings

- FHD Bearings

- Other Market Players

Frequently Asked Questions

The Bicycle Bearings market is estimated to be valued at US$ 6,718.9 Mn in 2026.

The key demand driver for the Bicycle Bearings market is the rising global production and adoption of bicycles and e-bikes, particularly the rapid expansion of the electric bicycle segment.

In 2026, the Asia Pacific region will dominate the market with an exceeding 45% revenue share in the global Bicycle Bearings market.

Among bearing types, ball bearing has the highest preference, capturing beyond 65% of the market revenue share in 2026, surpassing other bearing types.

SKF Group, NSK Ltd., NTN Corporation, The Timken Company, Schaeffler Group, JTEKT Corporation, Minebea Mitsumi Inc., RBC Bearings are a few leading players in the Bicycle Bearings market.