- Transportation & Logistics

- Bicycle Brake Components Market

Bicycle Brake Components Market Size, Share, and Growth Forecast 2026 - 2033

Bicycle Brake Components Market Disc Type (Rim Brake (Caliper, Brake Lever, Brake Cable), Disc Brake (Rotor, Caliper, Brake Lever, Brake Cable Hose)), Bike Type (Mountain, Hybrid, Road, Comfort, Youth, Cruiser, Electric), Sales Channel (OEM, Aftermarket), and Regional Analysis, 2026 - 2033

Bicycle Brake Components Market Size and Trend Analysis

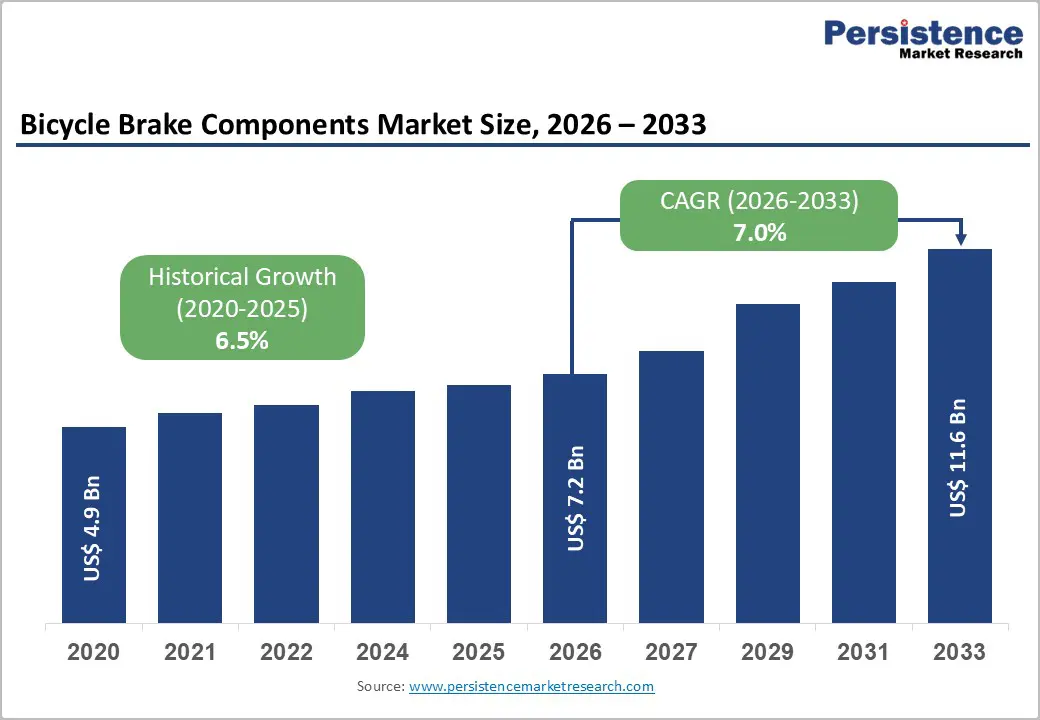

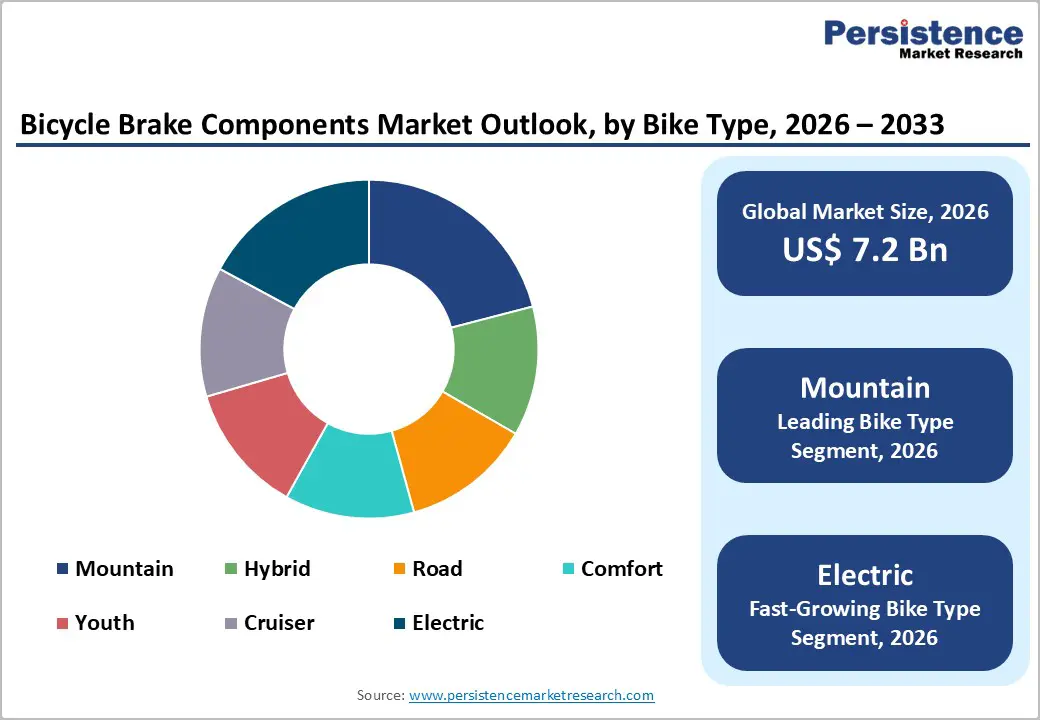

The global bicycle brake components market size is expected to be valued at US$ 7.2 billion in 2026 and projected to reach US$ 11.6 billion by 2033, growing at a CAGR of 7.0% between 2026 and 2033.

Growth is driven by rising demand for high-performance bicycles, particularly in the e-bike and mountain bike segments. Increasing urbanization, greater health awareness, and recreational cycling are driving demand for reliable braking systems. Compliance with International Organization for Standardization (ISO) safety standards and insights from Union Cycliste Internationale (UCI), showing over 15% annual growth in bicycle registrations, further propel the market. Advanced, durable brake components are now a priority for manufacturers.

Key Industry Highlights:

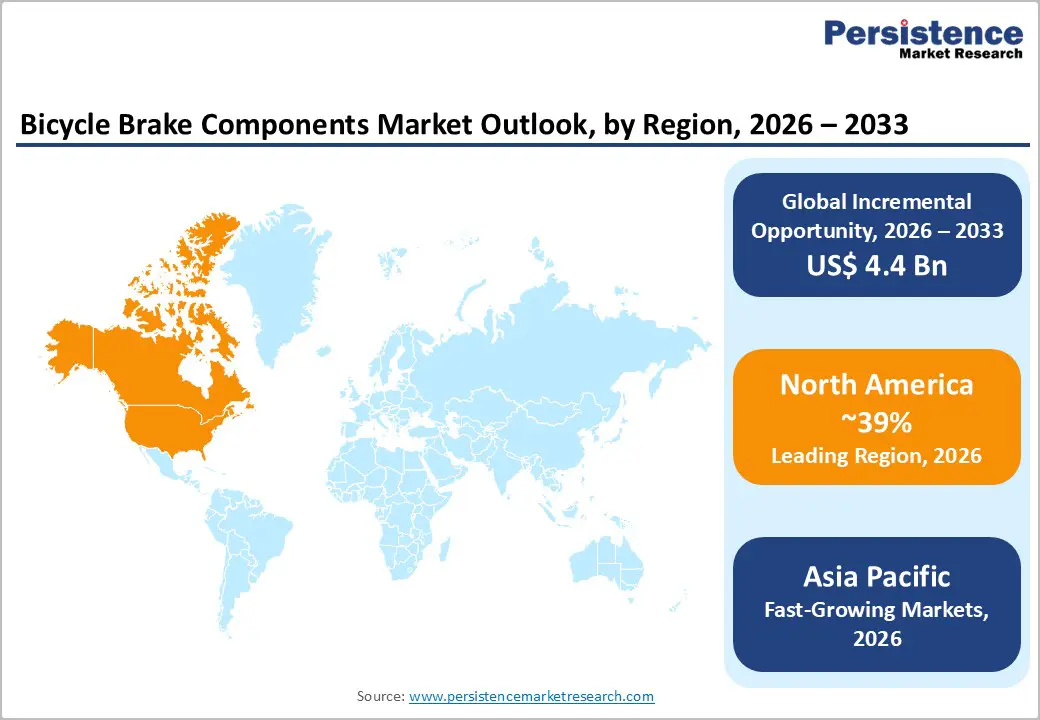

- Leading Region: North America dominates the Bicycle Brake Components Market with a 39% share in 2025, driven by U.S. regulations, innovation hubs, and growing e-bike adoption.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with a 32% share in 2025 and strong expansion supported by China’s manufacturing base and India’s subsidy programs.

- Leading Disc Type: The Disc Brake segment leads with a 55% share in 2025, offering superior safety and performance for mountain and electric bikes.

- Leading Bike Type: Mountain bikes dominate with a 35% share in 2025, fueled by trail expansions and rising global MTB participation.

- Key Opportunity: Innovations in hydraulic disc brakes for e-bikes present a significant revenue opportunity in premium and performance segments.

| Key Insights | Details |

|---|---|

| Bicycle Brake Components Size (2026E) | US$ 7.2 billion |

| Market Value Forecast (2033F) | US$ 11.6 billion |

| Projected Growth CAGR (2026 - 2033) | 7.0% |

| Historical Market Growth (2020 - 2025) | 6.5% |

Market Dynamics

Drivers - Rising Popularity of E-Bikes and Performance Cycling Boosts Demand for Advanced Brake Components

The growing adoption of electric bicycles (e-bikes) and high-performance cycling is a major factor driving the global bicycle brake components market. E-bikes, which are heavier and faster than traditional bicycles, require more robust braking systems to ensure rider safety. Hydraulic disc brakes with superior modulation are increasingly preferred, aligning with ISO 4210-4 safety standards.

Manufacturers are responding with innovative brake technologies to serve both OEM and aftermarket customers. European Cyclists' Federation data shows e-bike sales in Europe exceeded 4 million units in 2024, reflecting a 25% growth from previous years. This trend is driving component upgrades and replacements, creating sustained demand for high-performance brake calipers, rotors, levers, and cables across all cycling categories.

Urban Mobility Expansion and Global Cycling Infrastructure Investments Driving Growth

The expansion of urban cycling infrastructure worldwide is accelerating demand for reliable bicycle brake components. Cities are adding extensive bike lanes, with the United Nations Environment Programme (UNEP) reporting over 1,000 km of new lanes annually in major metropolitan areas. Improved infrastructure encourages commuter cycling, necessitating dependable rim and disc-brake systems to ensure safety in dense traffic.

Additionally, post-pandemic cycling adoption has surged, with World Health Organization (WHO) data indicating a 20% increase in bicycle commuting. This trend pressures manufacturers to deliver durable, high-quality brake components suitable for daily use. Growing investments in city cycling networks and retrofitting of existing bicycles further contribute to the market’s steady growth trajectory, benefiting both OEM suppliers and aftermarket providers.

Restraints - High Raw Material Costs and Supply Chain Disruptions Pose Challenges to Bicycle Brake Component Manufacturers

Rising and fluctuating prices of essential materials, including aluminum and steel, present significant challenges for bicycle brake component manufacturers. According to the International Aluminium Institute, aluminum prices surged by 30% in 2024 due to energy constraints and supply disruptions in China and Europe. This escalation increases production costs for critical components such as calipers, rotors, and brake levers, squeezing profit margins and leading to higher prices for end users.

Smaller manufacturers face difficulties securing reliable material supplies, limiting their ability to innovate or expand market presence. Prolonged procurement delays can slow product development cycles and reduce responsiveness to market demand, restraining overall market growth and making it challenging for new entrants to compete effectively against established players.

Stringent Regulatory Compliance Burdens Restrict Growth and Increase Operational Costs for Manufacturers

Evolving safety regulations and mandatory compliance requirements present another restraint for the bicycle brake components market. Regulatory frameworks, such as EN 15194 for e-bikes, require advanced braking systems, including hydraulic brakes on high-power models, to ensure rider safety. Manufacturers must invest significantly in compliance testing and certification, which increases operational expenses, particularly for small- and medium-sized enterprises (SMEs).

Insights from Bike Europe indicate that R&D budgets for SMEs can rise by 15-20% to meet evolving standards, while delays in certification processes can push back product launches. These regulatory hurdles restrict growth in highly regulated markets such as the European Union and the United States, slowing market expansion and making it challenging for manufacturers to introduce innovative or updated braking solutions promptly.

Opportunity - Advancements in Lightweight Hydraulic Disc Brakes Present Lucrative Opportunities for Premium Bicycle Segments

The evolution of lightweight hydraulic disc brakes is creating significant growth opportunities in the premium bicycle market. Leading manufacturers like Shimano have introduced calipers that are 20% lighter, made with carbon composites, targeting high-performance mountain and road bikes. According to the Cycling Industry Association, global bike sales grew 12% in 2024, reflecting strong demand for advanced braking solutions.

Government policies, such as the EU Green Deal, further incentivize the adoption of energy-efficient and lightweight components. These innovations not only enhance rider performance and safety but also drive higher-margin sales in both OEM and aftermarket channels. The trend positions hydraulic disc brakes as a key revenue driver, particularly in markets favoring high-end and performance-oriented bicycles.

Expansion in Emerging E-Bike Markets Drives Demand for Advanced Brake Components Across the Asia Pacific

Emerging e-bike markets in the Asia Pacific present vast opportunities for bicycle brake component manufacturers. China’s Ministry of Industry and Information Technology projects e-bike sales reaching 50 million units by 2030, creating strong demand for advanced disc rotors, calipers, and levers. Local manufacturing hubs help reduce costs, supporting affordable aftermarket sales and encouraging adoption across mass-market segments.

In India, initiatives like the FAME-II scheme are driving annual growth of around 30%, enabling firms to profitably target youth, cruiser, and commuter bicycles. This rapid market expansion allows OEMs and aftermarket suppliers to capitalize on increasing e-bike penetration, while also encouraging innovation in durable and efficient braking systems suited for high-speed and high-load applications.

Category-wise Analysis

Disc Type Insights

Disc brakes lead with a 55% share in 2025, driven by superior wet-weather stopping power and precise modulation. Consumer Product Safety Commission (CPSC) data shows that bikes equipped with disc brakes reduce crash risks by 40% during off-road riding. Mountain and electric bikes particularly benefit, with Union Cycliste Internationale (UCI) trials confirming 25% better performance over rim systems. OEM integrations by major assemblers further consolidate this segment’s market dominance.

While disc brakes dominate, rim brake systems are witnessing renewed interest in cost-sensitive and youth segments. These mechanical setups remain popular for entry-level road bikes and cruisers due to their simplicity, lightweight design, and ease of maintenance. Increasing urban cycling and retrofitting trends encourage incremental adoption, creating opportunities for manufacturers to innovate rim brake materials and cable systems while serving value-conscious consumers.

Bike Type Insights

Mountain bikes command a 35% share in 2025, fueled by the need for reliable braking on rugged terrains. The International Mountain Bicycling Association (IMBA) reports that over 18 million MTB riders worldwide are driving the adoption of hydraulic disc brakes. Expansion of trails, adding approximately 10,000 km annually, reinforces the requirement for robust calipers, rotors, and levers, outpacing adoption in road or hybrid bicycles.

E-bikes represent the fastest-growing category, driven by urban mobility needs and rising disposable incomes. Their higher speeds and weight necessitate advanced braking systems for safety, encouraging both OEM and aftermarket upgrades. Adoption is expanding rapidly in the Asia Pacific and Europe, where government incentives and infrastructure development support commuter and recreational e-bike usage. This segment offers manufacturers opportunities to introduce innovative, high-performance brake components tailored to emerging mobility trends.

Sales Channel Insights

OEM channels hold 65% share in 2025 as bicycle manufacturers prioritize integrated braking systems to meet warranty and quality standards. The Japan Bicycle Association notes that 80% of new bikes feature OEM-installed brakes compliant with JIS D 9417 standards. Volume efficiencies, brand synergy, and the ability to standardize components make OEM the preferred choice, especially for electric and performance-oriented bicycles.

The aftermarket is emerging as the fastest-growing channel, fueled by rising consumer interest in performance upgrades and the replacement of worn components. Enthusiasts and urban cyclists increasingly invest in premium rotors, calipers, and hydraulic levers to enhance safety and performance. Growth is strongest in mature markets, where riders seek customization and enhanced braking reliability, providing lucrative opportunities for component manufacturers.

Regional Insights

North America Bicycle Brake Components Market Trends

North America leads the global bicycle brake components market with a 39% share in 2025, anchored by innovation hubs in the U.S. Intertek certifications and rigorous safety standards have driven widespread adoption of disc brakes, with the National Highway Traffic Safety Administration (NHTSA) reporting 15% fewer bicycle accidents following 2023 regulations. E-bike subsidies under the Bipartisan Infrastructure Law further boost demand, with PeopleForBikes reporting 2 million e-bike units sold in 2024.

In addition to performance bicycles, urban commuter trends and recreational cycling stimulate replacement and upgrade sales. The aftermarket for advanced calipers, rotors, and hydraulic levers is expanding, creating opportunities for manufacturers to cater to safety-conscious consumers and e-bike enthusiasts. OEM partnerships with local assemblers ensure integration of high-quality braking systems, reinforcing North America’s leadership in both production and adoption.

Europe Bicycle Brake Components Market Trends

Europe is a mature market for bicycle brake components, with Germany, the U.K., France, and Spain leading adoption. German VDZ data indicates that over 12 million bikes with disc brakes will be in use by 2025, supported by harmonization under the EU Machinery Directive 2006/42/EC. Urban mobility programs in France and Spain contribute to 20% growth in cycling participation, while premium performance bike sales continue to drive disc brake integration. The region is expected to grow at a CAGR of 7.2% between 2025 and 2032, reflecting steady demand for high-quality and safety-compliant braking systems.

Emerging trends in e-bike commuting and retrofitting existing bikes present growth avenues for both OEM and aftermarket suppliers. Hydraulic disc brakes and lightweight components are increasingly preferred in urban and recreational segments, while standard rim brakes maintain relevance in budget and entry-level bicycles. Manufacturers leveraging performance, safety compliance, and local distribution networks can capitalize on Europe’s stable, high-value market.

Asia Pacific Bicycle Brake Components Market Trends

Asia Pacific holds a 32% share in 2025 and is the fastest-growing region, driven by China, India, and Japan. The China Bicycle Association reports over 400 million bicycles in circulation, with cost-effective rim brakes dominating commuter segments. Japan focuses on high-end disc brakes, while ASEAN manufacturing hubs reduce production costs by approximately 25%, supporting the rapid growth of e-bikes and urban cycling adoption.

Government incentives, urban infrastructure development, and rising health consciousness boost demand for both OEM-installed and aftermarket brake components. The region’s electric bicycle segment is particularly strong, encouraging adoption of durable hydraulic discs and advanced rotors. Asia Pacific’s growth trajectory underscores opportunities for manufacturers to scale production, introduce affordable components, and cater to expanding e-bike and performance bike markets across urban and semi-urban centers.

Competitive Landscape

The global bicycle brake components market is moderately consolidated, with leading players leveraging R&D and extensive supply chains to maintain a competitive edge. Industry leaders focus on developing lightweight and high-performance materials, such as advanced composites, while integrating hydraulic and disc technologies to meet the demands of performance and e-bike segments. Strategic collaborations with OEMs enable seamless integration of braking systems in new bicycles, enhancing brand visibility and customer trust.

Emerging competitors are differentiating through direct-to-consumer channels and subscription-based maintenance services, targeting urban and commuter cyclists. Customization options, aftermarket upgrades, and innovative service models allow new entrants to capture niche demand, intensifying competition while driving product innovation and market expansion globally.

Key Developments:

- In January 2025, SRAM launched Eagle AXS wireless disc brakes, offering advanced MTB performance with precise modulation, reduced weight, and seamless app integration for ride data and customization, enhancing rider control and safety on challenging off-road terrains.

- In June 2024, Shimano introduced the Deore series featuring hydraulic disc brakes with 30% improved heat dissipation, designed for endurance racing and long-distance rides, ensuring consistent braking performance, reduced fade, and superior reliability in demanding road and mountain conditions.

- In October 2023, Magura expanded its range of hydraulic calipers for e-bikes, fully compliant with updated ISO safety standards, providing higher stopping power, enhanced durability, and better modulation to meet growing performance and regulatory requirements in the electric bike segment.

Companies Covered in Bicycle Brake Components Market

- Ashima Ltd.

- BBB Cycling

- Campagnolo S.r.l.

- DIA-COMPE TAIWAN Co., Ltd.

- Full Speed Ahead S.r.l

- Hayes Bicycles Group Inc.

- Clarks Cycle Systems Ltd.

- Industrias Galfer S.A.

- Shimano Inc.

- SRAM LLC

- Tektro Technology Corporation

- Hope Technology (IPCO) Ltd

- Rex Articoli Tecnici SA

Frequently Asked Questions

The global Bicycle Brake Components Market is expected to reach US$ 7.2 billion in 2026, growing to US$ 11.6 billion by 2033 at 7.0% CAGR.

Rising e-bike adoption and urban cycling infrastructure, including UNEP’s 1,000 km annual bike lane expansions, are driving demand for reliable and safety-focused brake components.

North America leads with a 39% share in 2025, supported by U.S. NHTSA regulations, innovation hubs, and e-bike subsidies.

Advancements in lightweight hydraulic disc brakes for e-bikes present premium revenue growth, particularly in the Asia Pacific.

Leading firms include Ashima Ltd., BBB Cycling, Campagnolo S.r.l., DIA-COMPE TAIWAN Co., Ltd., and Full Speed Ahead S.r.l.