- Transportation & Logistics

- Bicycle and Components Market

Bicycle and Components Market Size, Share, and Growth Forecast, 2026 - 2033

Bicycle and Components Market by Product Type [Component Type (Drivetrain Systems, Electronic & Smart Components, Braking Systems, Motor, Wheelsets & Tires, Suspension & Forks, Frames & Handlebars, Pedals, Saddles & Seatposts), Bicycle Type (Commuting/Leisure (City/Urban), Performance/Race, Mountain Bike (MTB)/Trekking Gravel & Touring, and Others (Cargo bikes)], Sales Channel (Online and Offline), and Regional Analysis for 2026 - 2033

Bicycle and Components Market Size and Trends Analysis

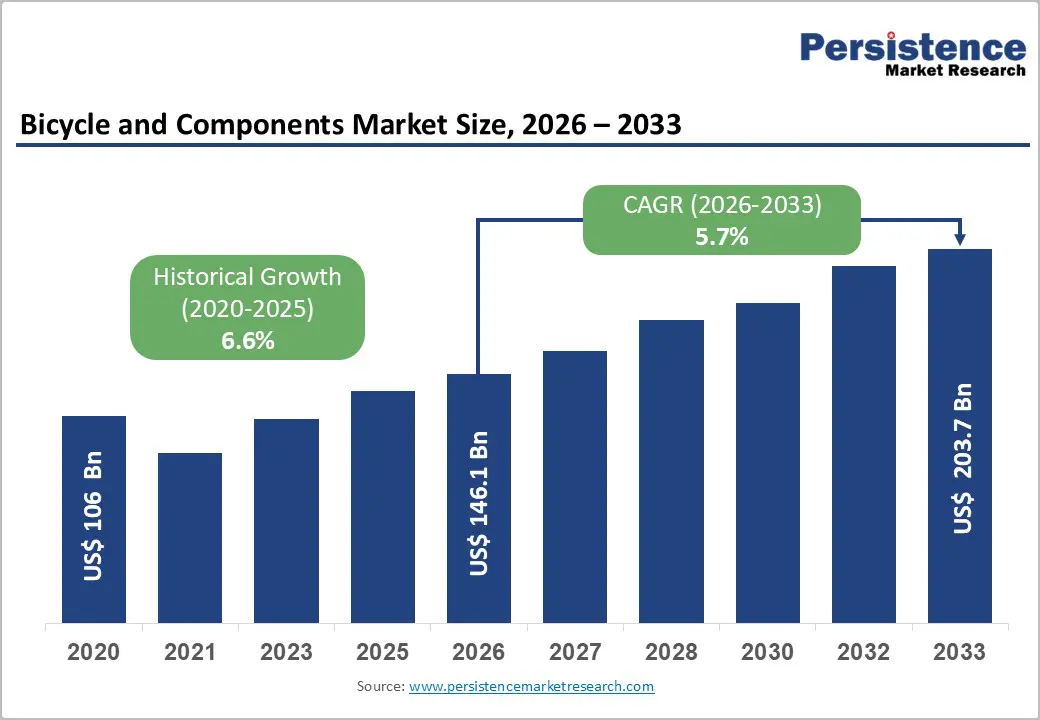

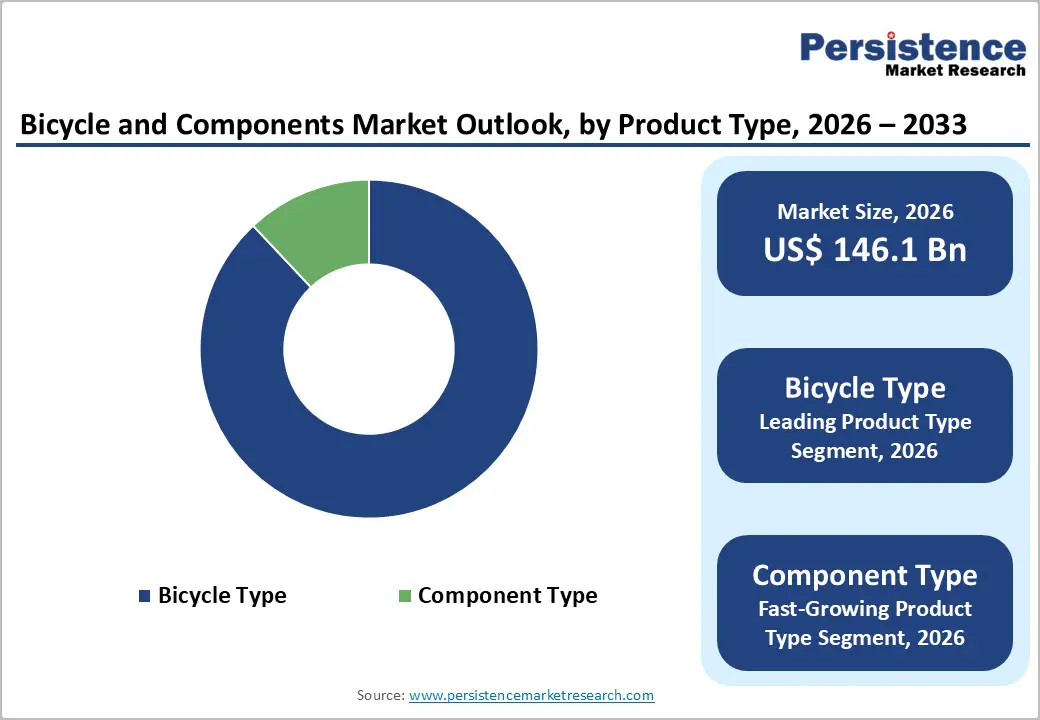

The global bicycle and components market size is likely to be valued at US$ 146.1 billion in 2026 and is projected to reach US$ 203.7 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033. The market benefits from rising health consciousness, the shift to low-carbon urban mobility, and continued preference for cycling as a form of exercise, trends also reflected in independent estimates that place the standalone global bicycle market on a high single-digit growth trajectory through 2033.

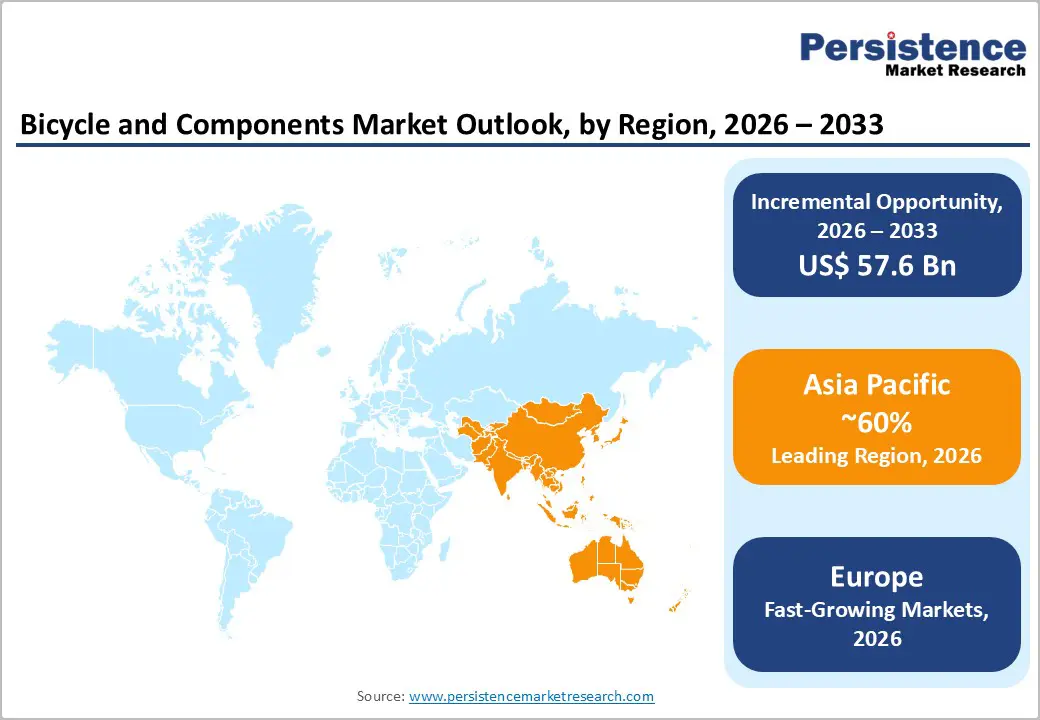

Rapid adoption of e-bikes and advanced components, including electronic drivetrains, motors, and smart connectivity, supports higher value per unit and underpins above-market growth of the components segment. Government incentives for cycling and e-bikes, plus investments in bike lanes and urban cycling infrastructure across Europe, North America, and Asia, are structurally expanding the addressable commuter and leisure base. Asia Pacific accounts for well over half of global bicycle demand and more than 59% of market revenue, while Europe is emerging as the fastest-growing region on the back of strong policy support and premiumization.

Key Industry Highlights:

- Market Scenario: The global Bicycle and Components market is projected to grow from US$ 146.1 billion in 2026 to US$ 203.7 billion by 2033, at a 5.7% CAGR, supported by health, sustainability, and micromobility trends.

- Key Opportunity: Flexible monthly rentals appeal to urban riders, offering affordable, hassle-free mobility and aligning with expanding bike-sharing systems worldwide.

- Trend: Across independent sources, the underlying bicycle and components ecosystem is expected to expand at approximately 4-8% CAGR through the early 2030s, with e-bikes and premium components growing above the market average.

- Leading Product Bicycle type (complete bikes) accounts for over 88% of market revenue, while component type is the fastest-growing product category, with external estimates placing the standalone components market at 6.4-7.2% CAGR to 2030 - 2032.

- Leading Component: Within components, drivetrain systems hold above 45% value share, and electronic/smart components (e-bike systems, electronic drivetrains, connectivity) are the fastest-growing sub-segment.

- Regional Analysis: Asia Pacific commands more than 60% of global revenues, anchored by China, India, and ASEAN manufacturing and demand, while Europe is the fastest-growing region, underpinned by strong e-bike incentives and cycling infrastructure investment.

- Government incentives such as EU e-bike subsidies, national climate programs, and North American provincial rebates-are materially boosting e-bike affordability, particularly for commuting and cargo use cases.

- Leading players including Shimano, SRAM, Bosch eBike Systems, Trek, Giant, Merida, Accell, and others are investing heavily in e-bike systems, electronic drivetrains, and digital services, while optimizing supply chains and product portfolios to capture structurally higher growth in premium and electric segments

| Key Insights | Details |

|---|---|

| Bicycle and Components Market Size (2026E) | US$ 146.1 Bn |

| Market Value Forecast (2033F) | US$ 203.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.6% |

Market Dynamics

Drivers - Active Mobility and Government Incentives Driving Bicycle Market Growth

Rising emphasis on active mobility, preventive healthcare, and sustainable urban transport is significantly accelerating growth in the global bicycle and components market. Increasing awareness of cycling’s health benefits such as reducing obesity, cardiovascular disease, and other lifestyle-related conditions has transformed bicycles from purely recreational products into essential mobility solutions for commuting and daily fitness. Industry assessments consistently project annual market growth of approximately 4-8% through the early 2030s, supported by new rider adoption and steady replacement cycles. For component manufacturers, this trend generates recurring revenue streams from wear-and-tear parts including drivetrains, brakes, and tires, alongside upgrade-driven demand in premium and performance segments.

Simultaneously, government decarbonization policies and urban air-quality initiatives are strengthening bicycle and e-bike adoption worldwide. The European Declaration on Cycling (2023) underscores cycling as a strategic transport mode, promoting infrastructure expansion, multimodal integration, and secure charging facilities. Financial incentives across Germany, France, Italy, the Netherlands, Austria, and other EU nations ranging from €200 to over €1,200 significantly reduce consumer payback periods. Similar rebate programs in North America and low-emission urban policies further expand the addressable market, particularly for electric, cargo, and smart bicycle segments, enhancing long-term industry profitability and supply chain resilience.

Electrification, smart components and micromobility expansion

Electrification is structurally upgrading the value of each bicycle sold by adding motors, batteries, controllers, sensors, and electronic drivetrains. European e-bike sales reached about 5.1 million units in 2024, up 23% year-on-year, illustrating how policy support and consumer acceptance are accelerating this segment. Dedicated e-bike component markets covering motors, batteries, and electronic control systems are identified as among the fastest-growing sub-segments within the broader components industry. Suppliers such as Shimano, SRAM, Bosch eBike Systems, and others are expanding portfolios of electronic shifting, integrated drive units, and digital services, which command premium pricing and lock in long-term upgrade paths. As cities encourage micromobility for last-mile delivery and commuting, e-bikes and cargo bikes further increase ASPs (average selling prices) and components content per vehicle.

Restraint - Cost pressures, supply chain complexity, and affordability gaps

The transition to sophisticated drivetrains, hydraulic braking, and motorized systems increases bill-of-materials costs and exposes OEMs to volatility in metals, electronics, and battery materials. Dedicated bicycle components markets are forecast to grow at around 6.4-7.2% CAGR to 2030-2032, partly reflecting higher unit values for advanced parts like drivetrains, wheels, and suspension systems. However, this premiumization risks pricing out more price-sensitive consumers in emerging markets and lower-income segments, especially where subsidies are absent. During and after the pandemic, inventory imbalances and shipping disruptions created overstock situations for some OEMs and retailers, forcing discounts and complicating capital allocation for innovation.

Opportunities - E-Bike and Urban Cargo Platforms Driving Bicycle Market Growth

The global bicycle industry is entering a structurally attractive growth phase, led by the rapid expansion of e-bikes and smart component ecosystems alongside accelerating adoption in urban commuting and last-mile logistics. E-bikes remain the fastest-growing segment, with global revenues projected to reach tens of billions of dollars by 2030. In Europe alone, the market is expected to approach €37 billion by 2032, supported by modal shift targets, sustainability mandates, and subsidy programs. This momentum is creating significant opportunities for suppliers of motors, batteries, power electronics, electronic drivetrains, smart displays, and integrated software platforms for diagnostics and navigation. As the broader bicycle components market grows at mid- to high-single-digit CAGRs, e-bike-focused platforms are positioned to outperform the industry average by an estimated 150-250 basis points over the next decade.

Simultaneously, urban mobility transformation is unlocking high-value commercial applications. Investments in cycling infrastructure across Europe, combined with low-emission regulations and cargo e-bike incentives, are accelerating the shift from delivery vans to e-cargo bikes in dense city centers. These use cases demand durable frames, high-capacity battery systems, cargo-specific components, and telematics integration driving higher revenue per unit and recurring aftermarket service opportunities for OEMs and component manufacturers.

Bicycle and Components Market Insights and Trends

Product Type Insights - Complete Bicycles Dominate Revenue; Components Fastest Growing Segment

The complete bicycle segment continues to dominate overall product-type revenues, accounting for more than 88% of total market value. This dominance is largely attributed to strong OEM channel dynamics, where most components are integrated and sold as part of fully assembled bicycles rather than as standalone products. Independent industry assessments estimate the global standalone bicycle market to be valued between US$60-80 billion in the mid-2020s, expanding at a mid-single- to high-single-digit CAGR. This reflects sustained demand across commuter, performance, and electric bicycle categories, reinforcing the structural strength of complete-bike sales within the industry ecosystem.

In contrast, the component segment represents the fastest-growing product category. While smaller in total value, it is projected to expand at approximately 7.9% CAGR, supported by increasing consumer preference for customization, performance upgrades, and replacement cycles. External market estimates value the dedicated bicycle components market at roughly US$10.5-15.3 billion in 2024-2025, expected to reach US$15.8-25.3 billion by 2030-2032, growing at 6.4-7.2% CAGR. Growth is primarily driven by high-value drivetrains, braking systems, wheels, suspension technologies, and advanced e-bike components, alongside rising aftermarket demand from performance-oriented and enthusiast riders seeking enhanced functionality and durability.

Bicycle and Component Segments Driving Market Expansion Globally

The global bicycle industry continues to evolve through strong momentum in both complete bicycles and high-value component systems, reflecting a balanced growth structure across product categories. Within bicycle types, commuting and leisure (city/urban) bicycles remain the dominant segment by value, supported by expanding cycling infrastructure, employer-backed mobility initiatives, and government policies promoting low-emission urban transport. Large installed bases across Asia Pacific and Europe further reinforce stable demand, while the increasing electrification of city bikes is attracting older riders and long-distance commuters. At the same time, performance and race bicycles represent the fastest-growing segment, driven by rising participation in road, gravel, MTB, and endurance sports. Consumers are increasingly upgrading to carbon frames, aerodynamic designs, and electronic shifting systems, resulting in higher average selling prices and shorter replacement cycles.

On the component side, drivetrain systems account for over 45% of total component value, reflecting their central role in performance, efficiency, and durability. Continuous innovation in materials, gear optimization, and wireless electronic shifting platforms sustains revenue leadership. Meanwhile, electronic and smart components are the fastest-growing category, integrating connectivity modules, sensor-based systems, and app-controlled customization particularly in e-MTB, gravel, and premium road segments thereby reshaping the competitive landscape.

Sales Channel Insights

Offline Dominates While Online Sales Accelerate Bicycle Market Growth

Offline distribution channels continue to dominate the global bicycle market, contributing more than 70% of total revenues as of 2026. Independent bike dealers, specialty retail chains, and brand-owned stores remain critical for the sale of technically complex products such as e-bikes and high-performance bicycles. These outlets provide essential advisory services, including professional bike fitting, component selection guidance, and after-sales maintenance support. Their role is particularly significant in mature cycling markets across Europe and Asia, where consumers value personalized service and technical expertise before making high-value purchases.

In contrast, online channels are emerging as the fastest-growing sales avenue, projected to expand at approximately 8.1% CAGR between 2026 and 2033. Growth is driven by the expansion of direct-to-consumer (D2C) strategies, digital bike configuration tools, and click-and-collect models that blend online convenience with offline support. E-commerce marketplaces and specialist platforms are also broadening access to components, accessories, and mid-range bicycles. For component manufacturers, online sales offer a strategic advantage in targeting informed enthusiasts seeking drivetrain upgrades, smart systems, and performance-enhancing accessories directly.

Regional Insights and Trends

Asia Pacific Leads Global Bicycle Market Growth Momentum

Asia Pacific remains the dominant region in the global bicycle market, accounting for approximately 60% of total market value. This leadership is primarily driven by large commuting and utility bicycle segments across China, India, and Southeast Asia, where cycling plays a structurally embedded role in daily mobility. According to research by the World Bank, non-motorized vehicles (NMVs) including bicycles, cycle-rickshaws, and carts represent between 25% and 80% of vehicle trips in many Asian cities, the highest proportion globally. In several Chinese cities, bicycles account for 50-80% of urban vehicle trips, highlighting a vast installed base that consistently drives replacement demand for components and accessories.

Policy frameworks across the region further reinforce cycling’s importance. Studies emphasize that NMVs contribute significantly to poverty reduction, congestion management, and air quality improvement. In Indian cities, bicycles account for 10-30% of total person trips and up to 50% of traffic on primary urban corridors. Meanwhile, countries such as Sri Lanka are targeting an increase in non-motorized transport share to 20% by 2030 and 30% by 2035. Despite challenges from rising motorization and infrastructure gaps, Asia Pacific is expected to remain the largest revenue and volume hub, supported by electrification, urban cycling networks, and multimodal transit integration.

Europe Leads Fastest Bicycle and E-Bike Market Growth

Europe has emerged as the fastest-growing major regional market for bicycles and components, supported by strong cycling adoption, rapid e-bike penetration, and structured policy backing. According to the European Cyclists’ Federation (ECF), more than 20 million bicycles were sold across Europe in 2023, with e-bikes accounting for approximately 30% of total sales highlighting the accelerating electrification of the fleet. ECF’s 2024 assessment of national cycling strategies indicates that at least nine EU member states, including Austria, Germany, Italy, Luxembourg, and Spain, have implemented formal cycling plans aligned with infrastructure investments such as the EuroVelo network, reinforcing long-term institutional commitment.

Data from Eurostat shows that over 60% of Europe’s urban population prioritizes eco-friendly transportation, while cities expanding dedicated bike lanes have experienced usage growth of nearly 40%, demonstrating infrastructure-led demand acceleration. Germany now leads Europe in overall e-bike volumes, with electric models surpassing traditional bicycles in 2024, while the Netherlands maintains the highest per-capita e-bike penetration. Substantial public investments in France, Luxembourg, and Belgium further stimulate premium bicycle sales and advanced component demand, solidifying Europe’s leadership in e-bikes, cargo bicycles, and smart mobility systems.

Competitive Landscape

The global bicycle and components market remains moderately fragmented at the OEM level but highly concentrated within core component categories such as drivetrains, braking systems, and e-bike powertrains. Leading suppliers including Shimano, SRAM, Bosch eBike Systems, and Campagnolo collectively command dominant shares in premium drivetrain and electric systems across several regions. In contrast, bicycle manufacturing is more fragmented, with global brands such as Trek and Giant operating alongside numerous regional players, creating a partnership-driven ecosystem where component platforms often become industry standards.

Post-2023 strategies emphasize innovation and operational efficiency. Bosch is expanding lightweight smart drive systems, Shimano is strengthening electronic and mid-range drivetrain portfolios, and Trek is increasing U.S. manufacturing capacity while streamlining SKUs. Across the industry, leaders are prioritizing digital integration, supply-chain resilience, regional production, and omnichannel expansion, alongside service-based and fleet-oriented business models to capture long-term value.

Key Developments:

- In 2026, Hero Electric Cycle is poised to disrupt India’s e-mobility segment with a claimed 120 km range and 65 km/h top speed at an ultra-affordable INR 4,000 price point, significantly accelerating mass adoption of electric bicycles and clean transportation solutions.

- In 2026, KTM is expected to expand its electric portfolio with the KTM Electric Cycle, blending its motorsport legacy with advanced e-mobility technology, targeting urban commuters, fitness enthusiasts, and adventure riders seeking high-performance electric cycling solutions.

- In January 2026, British bicycle brand Muddyfox announced its entry into India through an exclusive distribution partnership with Surat-based Ananta Ventures, strengthening premium bicycle availability and intensifying competition in India’s fast-growing cycling market.

- BC Bike Fest, scheduled for May 29-31, 2026, on Vancouver Island, will feature multi-format competitive races across XC, Enduro, Downhill, Adaptive XC, and eMTB, fostering community engagement and promoting mountain biking culture globally.

Companies Covered in Bicycle and Components Market

- Shimano Inc.

- Pon Holding B.V.

- Giant Manufacturing Co. Ltd

- Trek Bicycle Corporation

- Merida Industry Co., Ltd.

- Scott Sports SA

- Canyon Bicycles GmbH

- Specialized Bicycle Components, Inc.

- F.I.V.E. Bianchi S.p.A.

- Cicli Pinarello S.p.A.

- Colnago Ernesto & C. S.r.l.

- Factor Bikes

- BMC Switzerland AG

- Hero Cycles Limited

- Giant Bicycles Inc.

- Atlas Cycles Ltd.

- Derby Cycle Holding GmbH

- SRAM Corporation

- Rad Power Bikes

- Cannondale

- Cervelo Bicycles

- Decathlon

- Polygon Bikes

- Other Market Players

Frequently Asked Questions

The Bicycle and Components market is estimated to be valued at US$ 146.1 Bn in 2026.

The key demand driver for the Bicycle and Components Market is the rapid shift toward sustainable and eco-friendly mobility solutions.

In 2026, the Asia Pacific region will dominate the market with an approximate 60% revenue share in the global Bicycle and Components market.

Among product types, the bicycle type has the highest preference, capturing beyond 88% of the market revenue share in 2026, surpassing the component type.

Shimano Inc., Pon Holding B.V., Giant Manufacturing Co., Ltd., Trek Bicycle Corporation, Merida Industry Co., Ltd., Scott Sports SA, and Canyon Bicycles GmbH are a few leading players in the Bicycle and Components market.