- Non-food Packaging

- Pharmaceutical Packaging Market

Pharmaceutical Packaging Market Size, Share, and Growth Forecast, 2025 - 2032

Pharmaceutical Packaging Market by Material (Plastics [HDPE, LDPE, and LLDPE, PET, Other], Glass [Type I Borosilicate, Type II Treated Soda-lime, Type III Soda-lime], Metal, Paper and Paperboard, Biopolymers and Other Materials), Packaging (Primary Secondary, Tertiary) Delivery, and Regional Analysis for 2025 - 2032

Pharmaceutical Packaging Market Size and Trend Analysis

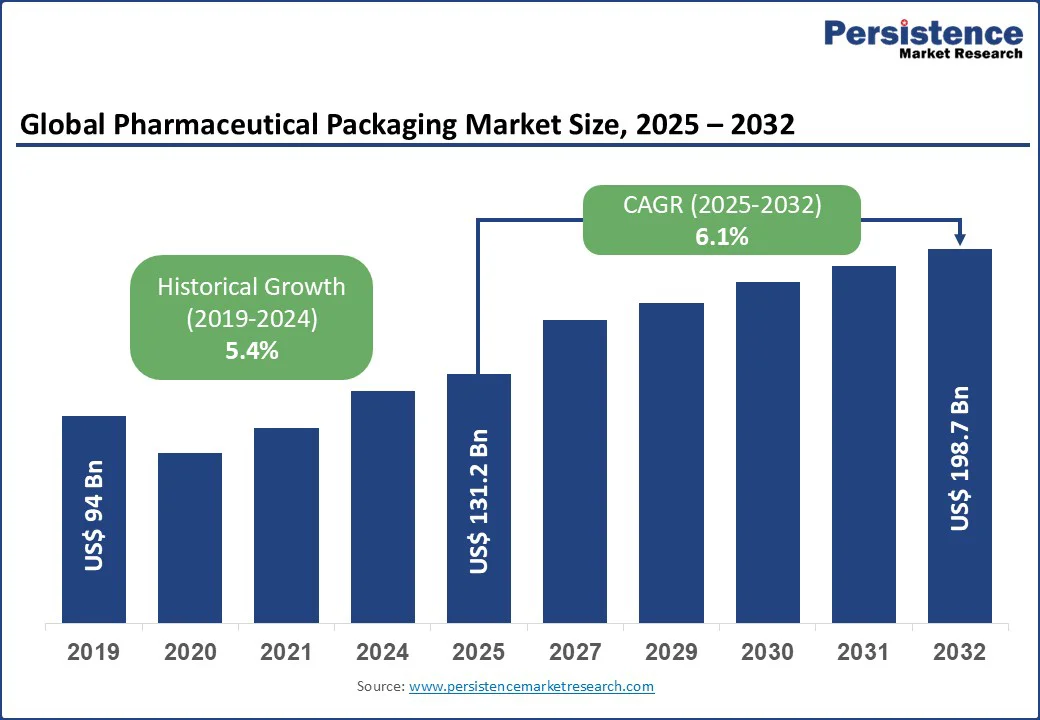

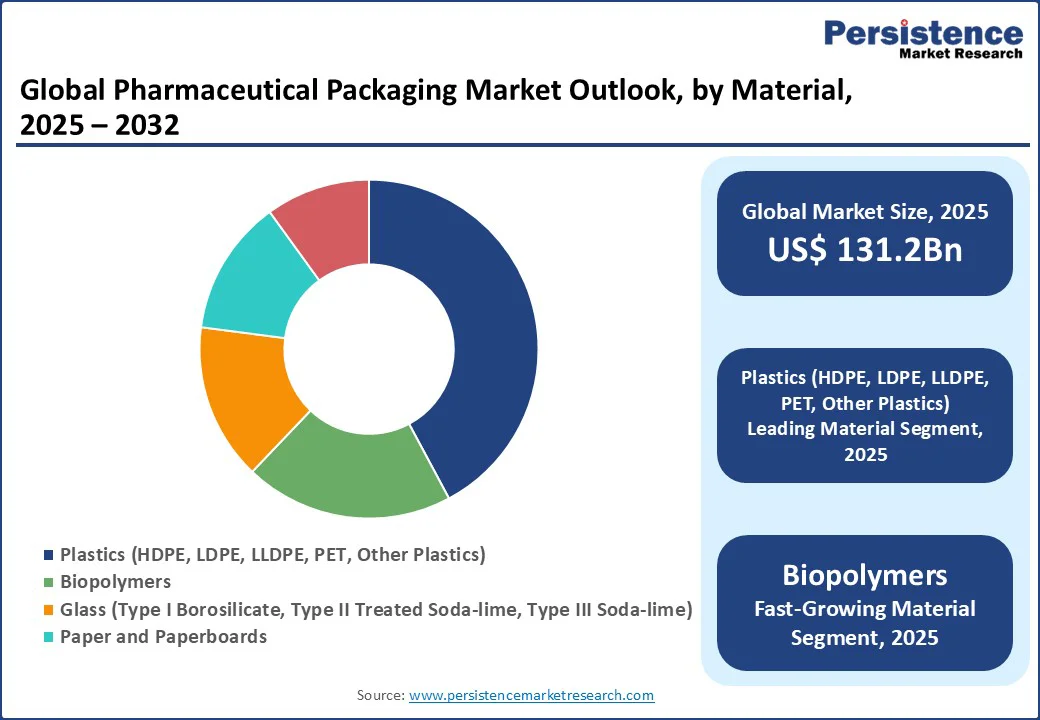

The global pharmaceutical packaging market size is likely to be valued at US$131.2 Bn in 2025 and reach US$198.7 Bn by 2032, growing at a CAGR of 6.1% during the forecast period from 2025 to 2032.

The pharmaceutical packaging industry is experiencing robust growth, driven by increasing demand for safe, efficient, and sustainable packaging solutions in the pharmaceutical industry. Pharmaceutical packaging, critical for ensuring drug safety, stability, and compliance, is witnessing heightened demand due to rising global healthcare needs, aging populations, and advancements in drug delivery systems. The surge in biopharmaceuticals and personalized medicine further supports market expansion, with innovations in tamper-evident and eco-friendly packaging gaining traction.

Key Industry Highlights

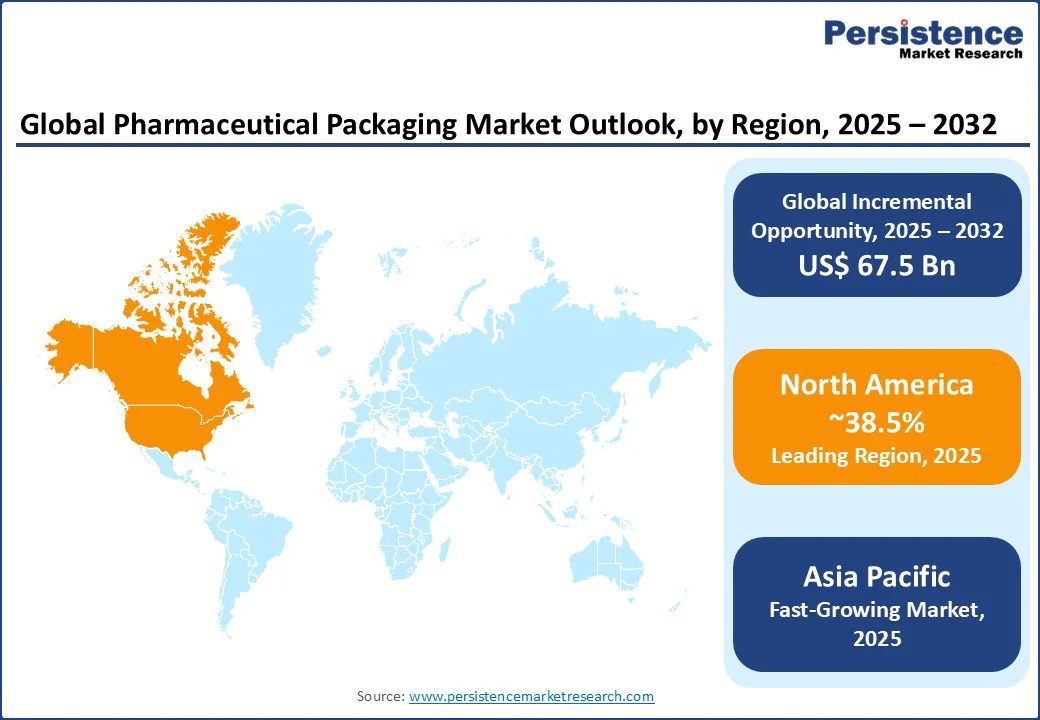

- Leading Region: North America holds a 38.5% market share in 2025 of the pharmaceutical packaging market, driven by advanced healthcare infrastructure and stringent regulatory standards in the U.S. and Canada.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, propelled by increasing pharmaceutical production and healthcare investments in China and India.

- Investment Plans: India’s Production Linked Incentive (PLI) scheme, announced in 2021, aims to boost domestic pharmaceutical manufacturing, increasing demand for advanced packaging solutions by 2030.

- Dominant Material Type: Plastics account for approximately 42.3% of the pharmaceutical packaging market share, owing to their versatility, cost-effectiveness, and suitability for various drug formats.

- Leading Application: Primary packaging contributes over 60.1% of market revenue, driven by the need for secure and compliant packaging for pharmaceuticals.

| Report Attribute | Details |

|---|---|

|

Pharmaceutical Packaging Market Size (2025E) |

US$ 131.2Bn |

|

Market Value Forecast (2032F) |

US$ 198.7Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.4% |

Market Dynamics

Driver - Rising Global Healthcare Needs and Biopharmaceutical Growth Fuel Market Expansion

The pharmaceutical packaging market is witnessing robust growth, fueled by the rising demand for biologics, vaccines, and advanced drug delivery systems that require specialized packaging solutions. Biopharmaceuticals such as monoclonal antibodies and mRNA vaccines demand high-barrier, sterile packaging, such as Type I borosilicate glass vials and prefillable syringes to ensure stability and safety. Companies such as Gerresheimer AG reported 8.0% organic revenue growth in 2024 in their Plastics & Devices division, largely attributed to increasing demand for such advanced delivery systems.

In emerging markets such as India, government initiatives such as Ayushman Bharat and the expansion of Health & Wellness Centres are significantly boosting pharmaceutical access and infrastructure. The Indian government’s allocation of Rs. 5,268.72 crore to the Department of Pharmaceuticals for FY 2025–26, a 28.8% increase from the previous year, underscores this commitment. These healthcare expansions and regulatory standards are intensifying the need for innovative, safe, and compliant pharmaceutical packaging, pushing manufacturers to adopt next-generation materials and technologies.

Restraint - High Costs of Sustainable Packaging and Regulatory Compliance

The pharmaceutical packaging market faces notable challenges, particularly related to cost pressures and complex regulatory compliance. The push toward sustainability has driven demand for eco-friendly materials, such as biopolymers and recyclable plastics; however, these alternatives often require extensive R&D investments and costlier production processes. This significantly impacts manufacturers’ profit margins, especially in emerging markets where price sensitivity is high. Moreover, stringent regulatory frameworks such as the U.S. FDA’s Current Good Manufacturing Practices (CGMP) and the EU’s Falsified Medicines Directive (FMD) demand rigorous validation, serialization, and quality assurance, adding further costs. For smaller manufacturers, meeting these regulatory standards presents a major barrier to entry, limiting innovation and competitiveness.

Additionally, the growing popularity of alternative, low-cost packaging formats, such as flexible pouches in over-the-counter (OTC) segments, creates competitive pressure on traditional pharmaceutical packaging providers. These challenges collectively constrain market growth, making it harder for companies to balance innovation, compliance, and cost-efficiency in an increasingly complex regulatory and environmental landscape.

Opportunity - Growing Demand for Smart and Sustainable Packaging Solutions

The growing emphasis on smart and sustainable packaging is unlocking substantial opportunities in the pharmaceutical packaging market. Smart packaging technologies such as RFID tags, QR codes, and temperature indicators are revolutionizing supply chain transparency, enhancing drug traceability, and promoting better patient adherence by enabling real-time monitoring and authentication. Simultaneously, rising environmental concerns and regulatory pressure are accelerating the shift toward eco-friendly materials, such as biopolymers, recyclable plastics, and biodegradable solutions. Industry leaders such as Amcor plc are at the forefront, developing recyclable PET bottles and compostable pouches to align with global initiatives, such as the EU’s Circular Economy Action Plan.

Additionally, governments in Europe and Asia are offering incentives and tax breaks for companies investing in sustainable packaging solutions, further stimulating R&D and market innovation. These trends are pushing pharmaceutical packaging beyond traditional functionality, creating room for patient-centric, sustainable, and technology-integrated solutions that meet both regulatory expectations and consumer demands through 2032.

Category-wise Insights

By Material

- Plastics, including HDPE, LDPE, LLDPE, and PET, hold the largest market share at 42.3% in 2025 of the pharmaceutical packaging market, due to their versatility, lightweight nature, and cost-effectiveness. Widely used in primary packaging, such as bottles and blister packs, plastics ensure drug protection and ease of handling. Companies such as Berry Global, Inc. and Amcor plc dominate with extensive plastic packaging portfolios, catering to demand in North America and the Asia Pacific oral and injectable drugs.

- Biopolymers are the fastest-growing material segment, driven by rising demand for sustainable and eco-friendly packaging. Used in pouches and secondary packaging, biopolymers offer biodegradability and compliance with environmental regulations. Firms such as WestRock Company are expanding biopolymer offerings in Europe and North America, supported by consumer preference for green packaging and government incentives for sustainability.

By Packaging

- Primary packaging, including plastic bottles, blister packs, and parenteral containers, accounts for over 60.1% of market revenue in 2025. Its dominance is driven by the need for direct drug protection and compliance with stringent safety standards. Major players, such as Schott AG and Gerresheimer AG, supply high-quality vials and syringes for vaccines and biologics, particularly in North America and Europe.

- Secondary packaging, such as prescription containers and accessories, is the fastest-growing segment, propelled by rising demand for patient-centric and tamper-evident solutions. Companies such as West Pharmaceutical Services, Inc. are innovating with child-resistant and senior-friendly containers, driven by increasing retail pharmacy sales in the Asia Pacific and North America.

By Drug Delivery

- Oral drug delivery, including tablets and capsules, holds the largest market share in 2025, driven by the high prevalence of oral medications globally. Packaging like blister packs and plastic bottles ensures stability and ease of use. Companies such as AptarGroup, Inc. and CCL Industries, Inc. lead with innovative oral packaging solutions, catering to demand in North America and the Asia Pacific.

- Injectable drug delivery, including prefillable syringes and vials, is the fastest-growing segment, fueled by the rise in biologics and vaccines. The demand for Type I borosilicate glass and advanced plastics for parenteral containers is increasing, with firms such as Becton, Dickinson, and Company expanding offerings in Europe and the Asia Pacific to support biopharmaceutical growth.

Regional Insights

North America Pharmaceutical Packaging Market Trends

North America dominates the pharmaceutical packaging market in 2025, commanding a substantial 38.5% market share, driven by its advanced healthcare infrastructure and stringent regulatory standards, particularly in the U.S. and Canada. The U.S., as one of the largest pharmaceutical markets globally, heavily depends on primary packaging solutions for biologics and vaccines, ensuring drug safety and efficacy. Canada’s expanding biopharmaceutical sector further fuels demand for specialized parenteral containers, as highlighted by Health Canada’s increasing focus on quality and compliance. Leading companies such as West Pharmaceutical Services, Inc. and Berry Global, Inc. dominate the region, leveraging extensive distribution networks and innovative packaging technologies to meet rigorous industry standards.

Additionally, rising consumer demand for sustainable and smart packaging including features such as RFID and tamper-evident seals aligns with regulatory mandates from the FDA, enhancing traceability and patient safety. These factors collectively strengthen North America’s pharmaceutical packaging market, positioning it for sustained growth and innovation through 2032.

Asia Pacific Pharmaceutical Packaging Market Trends

The Asia Pacific region is the fastest-growing pharmaceutical packaging market, fueled by rapid pharmaceutical production and significant healthcare investments, especially in China and India. China, recognized as the world’s second-largest pharmaceutical market, plays a pivotal role due to its extensive manufacturing capabilities and supportive policies highlighted by the China National Health Commission. Meanwhile, India’s pharmaceutical industry benefits from government initiatives such as the Production-Linked Incentive (PLI) scheme, which bolsters domestic manufacturing and drives demand for essential packaging formats such as vials, ampoules, and blister packs.

The region’s expanding middle class, coupled with a rising prevalence of chronic diseases, intensifies demand for both oral and injectable drug packaging. Key players, such as SGD Pharma and Gerresheimer AG, are strategically expanding operations in the Asia Pacific, capitalizing on lower production costs and favorable regulations. Growing biopharmaceutical exports and evolving regulatory frameworks further cement the region’s leadership in pharmaceutical packaging through 2032.

Europe Pharmaceutical Packaging Market Trends

Europe is the second fastest-growing pharmaceutical packaging market, fueled by stringent safety regulations, rising biopharmaceutical demand, and healthcare advancements, particularly in Germany and France. The robust European pharmaceutical market drives strong demand for both primary and secondary packaging solutions that ensure drug safety and compliance. Germany’s leadership in biologics significantly boosts the need for high-quality Type I borosilicate glass, with industry leaders such as Schott AG and Gerresheimer AG spearheading innovations in specialized packaging materials.

Additionally, the EU’s Green Deal actively promotes sustainability, encouraging pharmaceutical companies to adopt eco-friendly materials such as biopolymers and recyclable plastics. Europe’s rigorous focus on anti-counterfeiting measures, including serialization and tamper-evident packaging, along with adherence to high-quality standards, further propels market growth. As a result, pharmaceutical packaging firms are continuously innovating to meet evolving regulatory requirements and consumer expectations, securing Europe’s strong market position through 2032.

Competitive Landscape

The global pharmaceutical packaging market is highly competitive, characterized by a fragmented landscape with numerous global and regional players. Leading companies, such as Amcor plc, Gerresheimer AG, and Schott AG, dominate through extensive product portfolios and global distribution networks. Regional players, such as SGD Pharma in the Asia Pacific, focus on localized offerings. Firms are investing in smart packaging technologies, sustainable materials, and advanced manufacturing to enhance market share, driven by demand for high-quality, compliant packaging in biopharmaceuticals and retail pharmacies.

Key Industry Developments

- January 2025: Gerresheimer introduced the Gx Cap connected tablet container at Pharmapack 2025. The Gx Cap is a digitally connected tablet container closure designed to monitor medication adherence. It uses cellular signals to report to a cloud-based software platform when the prescription vial is opened, allowing pharmacies and clinical partners to track medication intake in real time.

- October 2024: Bormioli Pharma announced a partnership with Chiesi, an international, research-focused biopharmaceutical company, to supply Carbon Capture PET bottles for pharmaceutical use. This collaboration marks the first time Carbon Capture PET bottles will be utilized in the pharmaceutical industry. The bottles will package a medication indicated for the prophylaxis and treatment of seasonal and perennial allergic rhinitis, as well as vasomotor rhinitis.

Companies Covered in Pharmaceutical Packaging Market

- Amcor plc

- Becton, Dickinson, and Company

- AptarGroup, Inc.

- Drug Plastics Group

- Gerresheimer AG

- Schott AG

- Owens-Illinois, Inc.

- West Pharmaceutical Services, Inc.

- Berry Global, Inc.

- WestRock Company

- SGD Pharma

- International Paper

- Comar, LLC

- CCL Industries, Inc.

- Vetter Pharma International

- Others

Frequently Asked Questions

Increasing healthcare expenditures globally is a key factor driving market growth.

A few of the leading industry players in the market are Baxter International Incorporated, Amcor Limited, and Centor and Lilly (Eli) Company.

Development of intelligent packaging technologies is a key opportunity in the market.

Asia pacific to hold the notable growth rate in the market.

Plastics & polymers to capture notable share in the market.