- Industrial Goods & Service

- Test and Measurement Equipment Market

Test and Measurement Equipment Market Size, Share, and Growth Forecast, 2025 - 2032

Test and Measurement Equipment Market by Product (General Purpose Test Equipment, Mechanical Test Equipment), Service Type (Calibration Services, Repair/After-Sales Services, Others), Vertical, and Regional Analysis for 2025 - 2032

Test and Measurement Equipment Market Size and Trends

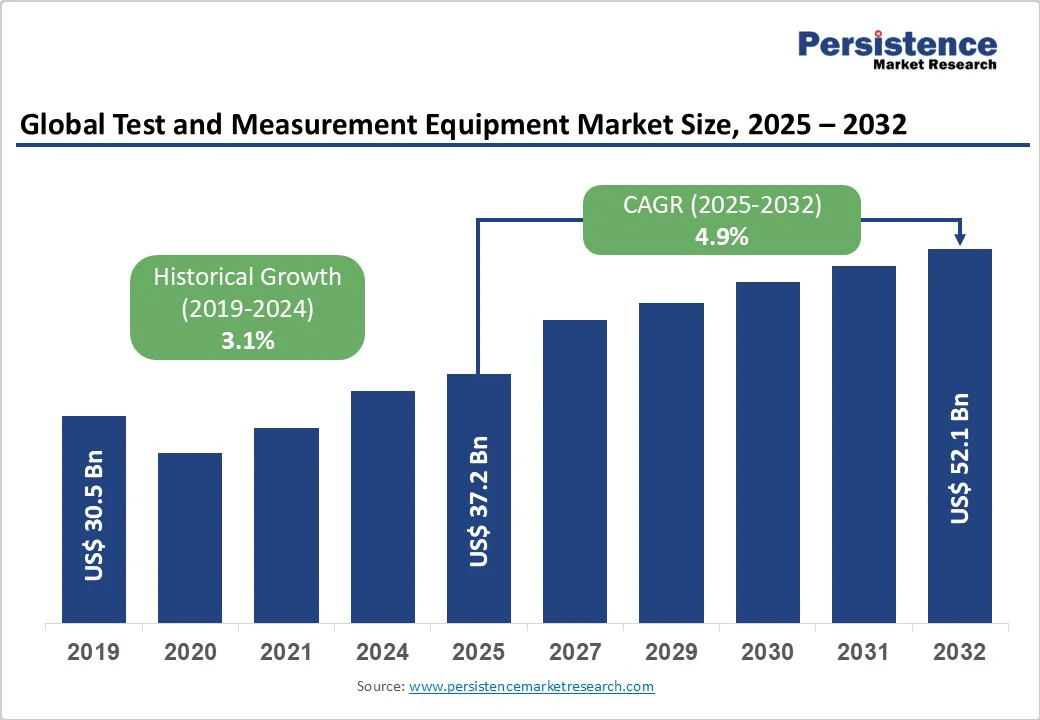

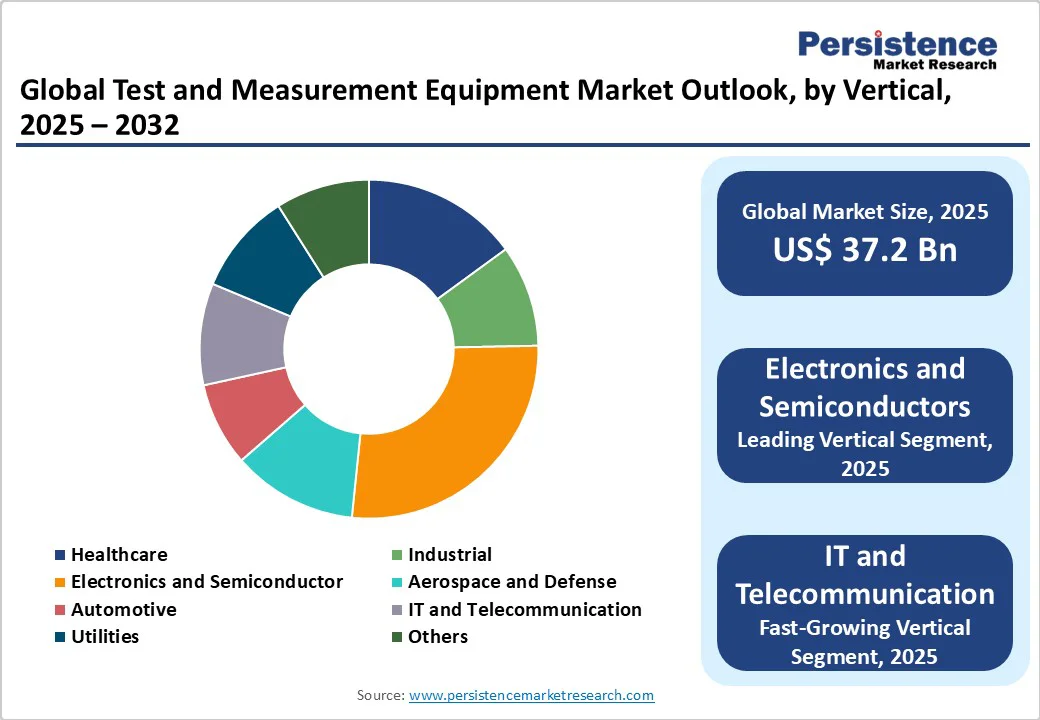

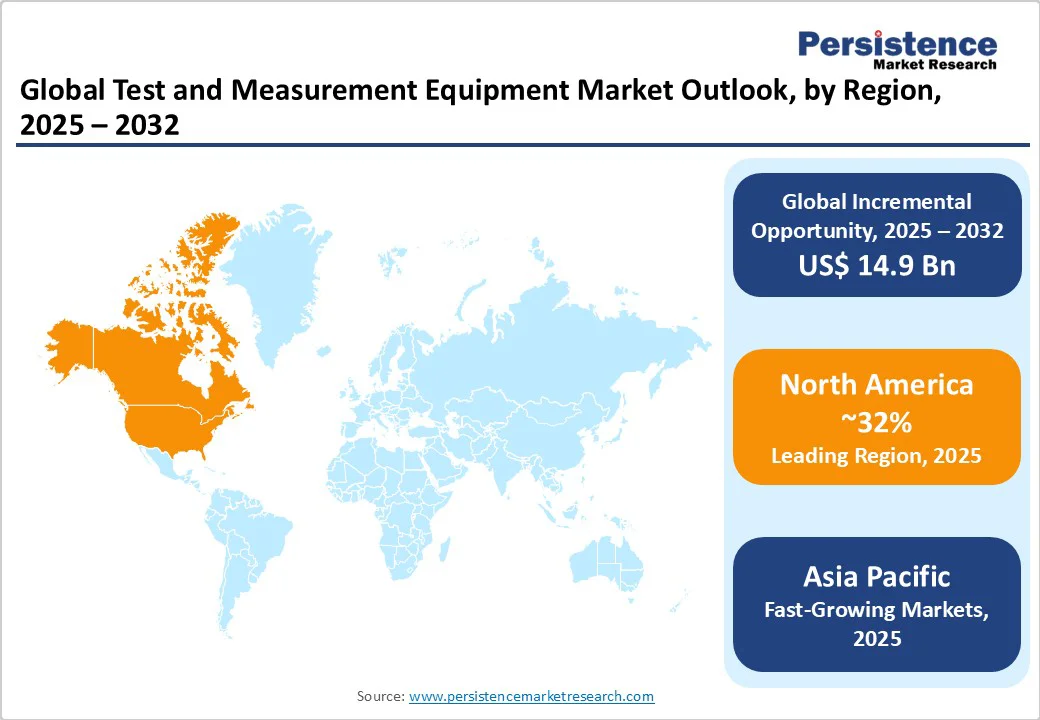

The global test and measurement equipment market size is likely to value US$37.2 Bn in 2025 to US$52.1 Bn by 2032, growing at a CAGR of 4.9% during the forecast period from 2025 to 2032.

The growing complexity of modern electronics, high-speed communications, and advanced sensors has increased the need for precise testing solutions. The expansion of electric vehicles, 5G networks, and renewable energy systems drives demand for high-voltage and power-related testing.

At the same time, the widespread adoption of automation, IoT, and smart devices requires continuous monitoring and calibration.

Key Industry Highlights:

- Leading Product: Oscilloscopes are expected to account for over 21% share in 2025, driven by demand for real-time, high-bandwidth testing in EVs, 5G infrastructure, and IoT devices. Bit error rate testers (BERT) are growing fastest, fueled by rising complexity in digital communication networks and the need for low-error, high-throughput connectivity.

- Leading Service Type: Calibration services hold over 55% share in 2025, as precision, compliance, and safety requirements drive continuous instrument calibration. Repair and after-sales services are growing rapidly due to the need for uninterrupted operations, predictive maintenance, and extended equipment lifespan.

- Leading Vertical: Electronics and semiconductors are likely to account for over 27% share in 2025, owing to high-precision testing needs in miniaturized and integrated devices. IT and telecommunications will grow fastest, supported by 5G rollout, 6G trials, IoT proliferation, and demand for network reliability.

- Leading Region: North America holds more than 32% share in 2025, supported by EV adoption, autonomous driving validation, and cloud/data center expansion. Asia Pacific will be the fastest-growing region, driven by booming electronics manufacturing in China, South Korea’s semiconductor leadership, and India’s production-linked incentives for electronics and semiconductors to ensure product quality and reliability.

| Key Insights | Details |

|---|---|

| Test and Measurement Equipment Market Size (2025E) | US$37.2 Bn |

| Market Value Forecast (2032F) | US$52.1 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.1% |

Market Dynamics

Driver - Growing Need for Advanced Solutions Amid Electrification & Miniaturization

With the integration of miniaturized electronics, embedded systems, high-frequency communications, and complex sensor networks, manufacturers face rising pressure to ensure performance, safety, and reliability. This has accelerated the adoption of sophisticated test and measurement tools that replicate real-world conditions through rigorous stress testing under strict industry standards. Sector-specific needs such as high-voltage testing for EVs, optical and RF testers for semiconductors, and in-process metrology for additive manufacturing are further driving demand for advanced solutions.

The rapid electrification of transport has further intensified this, with global EV sales reaching nearly 17 million units in 2024, marking a 25% increase from 2023. This expansion has multiplied the need for battery test systems, high-voltage sensors, EV charging interoperability testing, EMC/EMI testing, and high-power test benches across OEMs and suppliers.

Semiconductor fabrication plants demand optical, RF, and parametric testers, while additive manufacturing requires materials characterization to ensure repeatability. These advancements are fueling strong demand in both R&D and production environments.

Advancing Test and Measurement Needs Amid 5G Rollout and Digital Transformation

The rapid adoption of digital transformation initiatives, combined with the rapid global expansion of 5G networks, is fueling demand for advanced test and measurement equipment. As enterprises upgrade infrastructure to support high-speed data transmission and low-latency communication, the need for precise testing of devices, systems, and network components becomes critical.

With 5G technologies operating across complex architectures and multiple frequency bands, advanced equipment ensures signal integrity, compliance, and network reliability for next-generation communication systems. The complexity of 5G technology requires advanced spectrum analyzers capable of handling millimeter-wave frequencies, with devices above 4 GHz bandwidth projected to grow significantly.

By the end of 2024, 5G networks were deployed in 37 of 38 OECD countries, reaching 84% of the population, highlighting the reliance on robust testing solutions. In these countries, the average 5G download speeds reached 223 Mbps in urban areas compared to 174 Mbps in rural regions, underlining the importance of consistent performance validation.

The integration of IoT, AI, and edge computing into digital ecosystems creates further demand for continuous monitoring and measurement solutions. This makes test and measurement equipment essential for optimizing performance, ensuring compliance with global standards, and supporting the seamless deployment of digital infrastructure.

Restraint- Downtime, Delays, and Compliance Risks from Recurring Calibration Cycles

Precision instruments require regular calibration against international standards to ensure accuracy, increasing total ownership costs due to investment in equipment, ongoing calibration, and downtime management. Strict regulatory mandates demand traceable certificates, with lapses risking compliance, safety, or product rejection, making advanced instruments less viable for SMEs and research institutions. High-frequency, high-precision calibration needs specialized expertise, software, and controlled conditions, often forcing reliance on external providers, adding costs, delays, and productivity challenges.

For example, South Africa’s National Regulator for Compulsory Specifications (NRCS) reported that SANAS-accredited labs calibrated 11,677 mass verification standards, 722 volumetric verification standards, and 207 balances used by verification officers in 2023/24.

Inspections of 12,583 measuring instruments revealed 1,279 (10.2%) with lapsed verification status and 1,604 (12.7%) non-compliances, triggering embargoes and rejections, demonstrating how recurring calibration workloads and lapses create compliance risks, slow innovation, and restrain market growth.

Opportunity - Innovation in Software-Defined and AI-Enhanced Test Platforms

Software-defined architectures allow real-time reconfiguration, automation, and remote operation, reducing reliance on costly fixed-function instruments while enabling scalability across various industries. With the rollout of 5G and upcoming 6G trials, operators and equipment makers increasingly need flexible T&M systems that can simulate complex scenarios and adapt to evolving standards. According to the European Union, 13.5% of enterprises (41% of large enterprises) in the EU utilized AI in 2024, driving demand for programmable, over-the-air updatable instruments and AI-assisted test orchestration.

In January 2025, the U.S. Department of Commerce announced a CHIPS for America flagship R&D facility at Arizona State University, designed to bridge lab-to-fab with 300 mm flows and shared access to advanced tools directly requiring software-defined instrumentation and high-fidelity analytics.

The European Commission committed up to €1.67 billion (via Digital Europe + Horizon Europe) for semiconductor pilot lines and testing facilities, funding infrastructures that depend on scalable, reconfigurable test benches and AI-driven analytics to shorten time-to-yield. These initiatives open strong growth avenues for vendors of programmable RF, power, and reliability test systems with ML-based outlier detection.

Need for Remote-Capable Systems to Support Smart Grids

Rapid deployment of variable renewables is increasing test complexity as operators must validate performance across diverse conditions such as varying irradiance, wind speeds, and partial loads. The U.S. EIA reported that solar generation grew by ~25% in 2024 compared to 2023, while wind and solar’s share of U.S. generation also rose significantly.

These necessitate more acceptance testing, performance verification, and long-term monitoring of inverters, trackers, and balance-of-system components. In early 2025, the UK’s rising renewable share in quarterly generation highlighted the growing importance of frequency response testing, power-hardware-in-the-loop (PHIL), and EMC validation to ensure system reliability.

As renewables expand and grids evolve into smart grids, testing requirements extend to sensors, communication devices, and automation technologies to ensure interoperability and cybersecurity. Remote-enabled testing, once driven by pandemic disruptions, has now become a long-term standard for quality assurance and compliance verification.

Industries demand remote-capable solutions that maintain secure communication channels and traceability, ensuring compliance with tightening safety and performance regulations. This shift toward renewable integration, digital operations, and secure, remote testing underscores the increasing complexity and importance of T&M solutions across sectors.

Category-wise Analysis

By Product, Oscilloscopes Driving with Real-Time, High-Bandwidth Testing Capabilities

Among general-purpose test equipment, oscilloscopes are expected to account for more than 21% share in 2025 due to their role in debugging, design validation, and signal integrity analysis across industries. The growing adoption of EVs, 5G infrastructure, and IoT devices requires precise real-time waveform analysis to ensure performance, safety, and compliance. Engineers and researchers increasingly rely on advanced digital and mixed-signal oscilloscopes to validate high-speed designs and troubleshoot system behavior, driving strong demand.

Bit error rate testers (BERT) are expected to grow at a significant rate due to the rising complexity of digital communication systems and high-speed data networks. As enterprises and service providers demand reliable, high-throughput connections, BERT devices ensure signal integrity, low error rates, and compliance with standards. Advancements in high-speed memory and storage further drive the need for precise error monitoring to maintain performance and data integrity.

By Service Type, Calibration Services Driving Demand Through Precision, Compliance, and Technological Advancements

Calibration services are expected to account for over 55% share in 2025 due to the growing need for precise and accurate measurements to ensure product quality, safety, and compliance with standards. The increasing complexity of processes and the adoption of advanced technologies drive continuous demand for calibrated instruments. Frequent equipment upgrades and strict regulatory requirements make regular calibration essential.

Repair/after-sales services are expected to grow at a significant rate due to organizations increasingly relying on precise and uninterrupted measurements for critical operations. Regular maintenance and quick repair reduce downtime and enhance equipment lifespan.

The rising complexity of modern test and measurement instruments drives demand for specialized service support, including calibration, troubleshooting, and software updates. Customers prioritize reliability and performance, making after-sales services an essential part of their procurement strategy.

By Verticals, Electronics & Semiconductor Drives High-Precision Testing Demand

Electronics and semiconductors are expected to account for more than 27% share in 2025 due to the growing complexity of devices and rising miniaturization. Manufacturers require high-precision instruments to ensure reliability, performance, and quality.

The push for higher yield and lower defects further fuels equipment adoption. Continuous innovation in electronics amplifies testing requirements across all stages of design, production, and validation. As devices become faster and more integrated, the demand for accurate, high-frequency, and automated testing solutions grows.

The IT and telecommunications segment is expected to grow at the highest rate due to the rapid rollout of 5G networks and preparation for 6G trials. Network operators and equipment manufacturers need advanced solutions to validate high-speed data transmission, low-latency performance, and complex network configurations. The increasing adoption of cloud computing and IoT devices further drives the demand for precise testing of communication infrastructure.

Regional Insights

North America Test and Measurement Equipment Market Trends

North America is expected to account for a share of more than 32% in 2025, driven by the automotive sector’s shift toward electric vehicles (EVs) and autonomous driving technologies. EVs require extensive testing of batteries, electric motors, and charging systems, while autonomous vehicles need validation of sensors and communication systems.

According to the IEA, electric car sales in the U.S. are projected to rise by 20% in 2024 compared to 2023, adding nearly half a million units. The growing demand for cloud services and data storage has spurred T&M equipment usage, with the U.S. Department of Energy's LIFTOFF initiative highlighting the role of reliable testing in data center development.

Telecom operators in the U.S. and Canada are testing 5G networks, using spectrum analyzers, signal generators, and network analyzers to ensure signal integrity and optimize performance. Regulatory requirements from the FDA and FCC also drive adoption for electronic devices, medical equipment, and communication systems.

Manufacturers in the U.S. are deploying automated quality control systems, while Canada’s industries modernize processes for efficiency and defect detection. AI, machine learning, and predictive analytics are increasingly applied in testing, supported by U.S. government initiatives that enhance intelligent T&M system deployment and process optimization.

Asia Pacific Test and Measurement Equipment Market Trends

Asia Pacific is expected to grow at the highest rate, due to the region’s booming electronics manufacturing. China remains a dominant force, producing 1.67 billion mobile phones in 2024, a 7.8% increase from 2023, and achieving a 22.2% growth in integrated circuit production, reaching 4,514 billion units, according to the Ministry of Industry and Information Technology.

Shanghai's integrated circuit industry alone exceeded 390 billion yuan in 2024, emphasizing the city’s leadership in the semiconductor supply chain, which heightens the need for precise T&M equipment to ensure product quality and reliability.

South Korea continues to lead in semiconductor production, with Samsung and SK Hynix dominating the memory chip market, supported by the government’s KRW 2.4 trillion investment in 2025 for sectors like secondary cells and displays. SMEs exported US$28.47 billion in Q3 2024, demonstrating strong global competitiveness and reinforcing the demand for advanced equipment.

India’s electronics production surged from INR 1.9 lakh crore in 2014-15 to INR 11.3 lakh crore in 2024-25, driven by initiatives such as the PLI scheme and the India Semiconductor Mission with approved projects worth INR.1.60 lakh crore in six states. The region’s automotive shift toward electric vehicles and the trend of renting and leasing T&M equipment, especially among SMEs, further expand the market.

Europe Test and Measurement Equipment Market Trends

Germany’s focus on industrial automation and precision engineering, coupled with its commitment to Industry 4.0 and digitalization, is driving demand for advanced equipment. Initiatives supported by the Federal Ministry for Economic Affairs and Climate Action promote the adoption of digital technologies in manufacturing, increasing the need for precise measurement tools.

The European Green Deal’s push for zero-emission transport is boosting EV production, requiring T&M equipment to test battery performance, charging infrastructure, and vehicle electronics. According to IEA, Europe saw year-on-year EV sales growth of over 5% in Q1 2024, slightly above overall car sales, stabilizing the EV share, with 40% of battery electric car sales in Europe for small and medium models, compared to 25% in the U.S. and 50% in China.

Italy’s growing clean tech sector, particularly solar PV manufacturing, drives demand, with 6.8 GW of solar PV installed in 2024, necessitating testing of photovoltaic cells and modules for performance and quality assurance. In 2025, Italy’s focus on affordable healthcare is likely to increase T&M use in diagnostics and medical equipment certification.

WindEurope notes that Germany, the UK (1.9 GW), and France (1.7 GW) built the newest wind capacity, requiring T&M for grid stability and turbine performance. The U.K.’s "Invest 2035" strategy and 5G network expansion are boosting demand for network analyzers, high-frequency testing, and research tools.

Competitive Landscape

The global test and measurement equipment market is moderately fragmented, with a mix of large multinational leaders and numerous regional or niche players serving specialized segments. They are competing through innovation-led differentiation, with a focus on high-precision measurement, multi-function instruments, and IoT/AI-enabled analytics.

Many are pursuing vertical-specific solutions, e.g., for automotive EV testing, 5G, aerospace, etc., to capture high-growth niches. Emerging models such as equipment-as-a-service (EaaS) subscriptions are gaining traction, offering flexible, cost-effective access to advanced testing solutions

Key Industry Developments:

- In September 2025, VeEX Inc. launched the MTX642 2x400GE Multi-Service Handheld Test Set, the industry’s most compact dual 400GE portable solution. Designed for next-generation optical networks, it supports QSFP-DD, SFP-DD, and 400GE links with full PAM4 hardware, enabling fast, precise testing, troubleshooting, and commissioning in the field.

- In August 2025, Axiometrix Solutions launched the imc CANSASflex HISO-T-8-2L, a high-isolation CAN-Bus measurement module for high-voltage EV battery testing. Featuring 8 thermocouple channels, 1400?Vdc isolation, and a cable-free click-in design, it enables precise, safe temperature monitoring in advanced e-mobility applications.

- In May 2025, Yokogawa Test & Measurement Corporation launched the SL2000 high-speed data acquisition unit, a modular ScopeCorder series device that combines mixed-signal oscilloscope and data recorder functions. Designed for R&D, validation, and troubleshooting, it enables precise multi-channel measurement of fast signal transients and long-term trends, advancing mechatronics and electric power applications.

Companies Covered in Test and Measurement Equipment Market

- Keysight Technologies

- Rohde & Schwarz GmbH & Co. KG

- Yokogawa Electric Corporation

- Fluke Corporation

- Megger Group Limited

- TDK-Lambda

- Teledyne Technologies

- Gossen Metrawatt

- BENNING Elektrotechnik und Elektronik GmbH & Co. KG

- HIOKI E.E. CORPORATION

- Anritsu Corporation

- AMETEK.Inc.

- VIAVI Solutions Inc.

Frequently Asked Questions

The global test and measurement equipment market is likely to value at US$37.2 Bn in 2025.

The growing need for precise, reliable, and high-speed testing of increasingly complex electronics, EV systems, and 5G networks is a key driver of the market.

The test and measurement equipment market is poised to witness a CAGR of 4.9% from 2025 to 2032.

The increasing adoption of next-generation wireless networks and automation in manufacturing is creating strong growth opportunities.

Keysight Technologies, Rohde & Schwarz GmbH & Co. KG, Yokogawa Electric Corporation, Fluke Corporation, Megger Group Limited, and TDK-Lambda are among the leading key players.