- Healthcare Services

- Sexually Transmitted Disease Testing Market

Sexually Transmitted Disease Testing Market Size, Share, and Growth Forecast, 2025 - 2032

Sexually Transmitted Disease Testing Market By Product Type (Analyzers/Instruments, Others), Disease Type (Chlamydia, Gonorrhea, Syphilis, Others), Technology (Laboratory Testing, Point of Care (POC)Testing), and Regional Analysis for 2025 - 2032

Sexually Transmitted Disease Testing Market Share and Trends Analysis

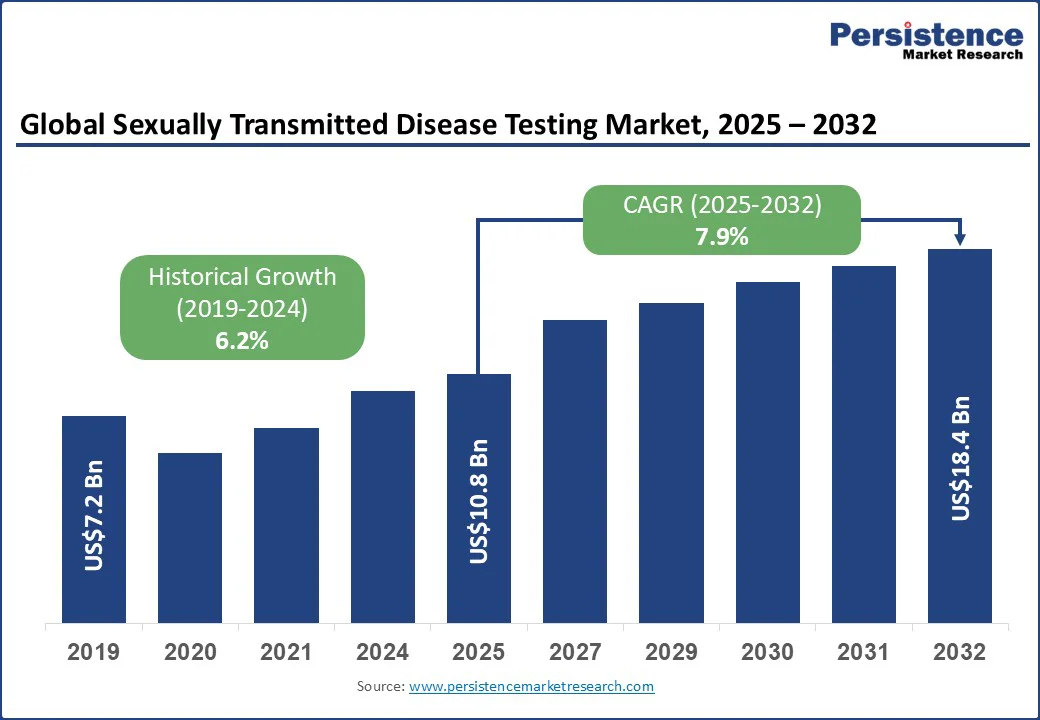

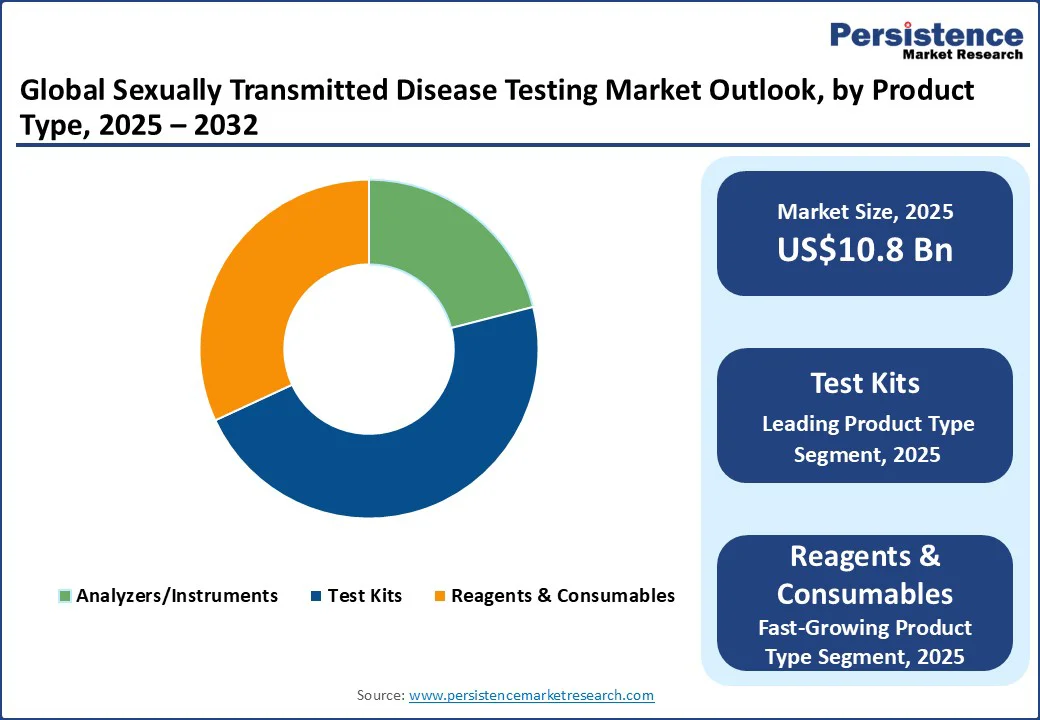

The global sexually transmitted disease testing market size is expected to be valued at US$10.8 Bn in 2025 and is expected to reach US$18.4 Bn by 2032, growing at a CAGR of 7.9% during the forecast period from 2025 to 2032.

The sexually transmitted disease (STD) testing market is witnessing consistent growth, driven by rising awareness of sexual health, increasing prevalence of STDs, and expanding government screening programs. The demand is further supported by advancements in diagnostic technologies such as rapid point-of-care tests and nucleic acid amplification tests (NAATs), which offer faster and more accurate detection.

Key Highlights of the Market:

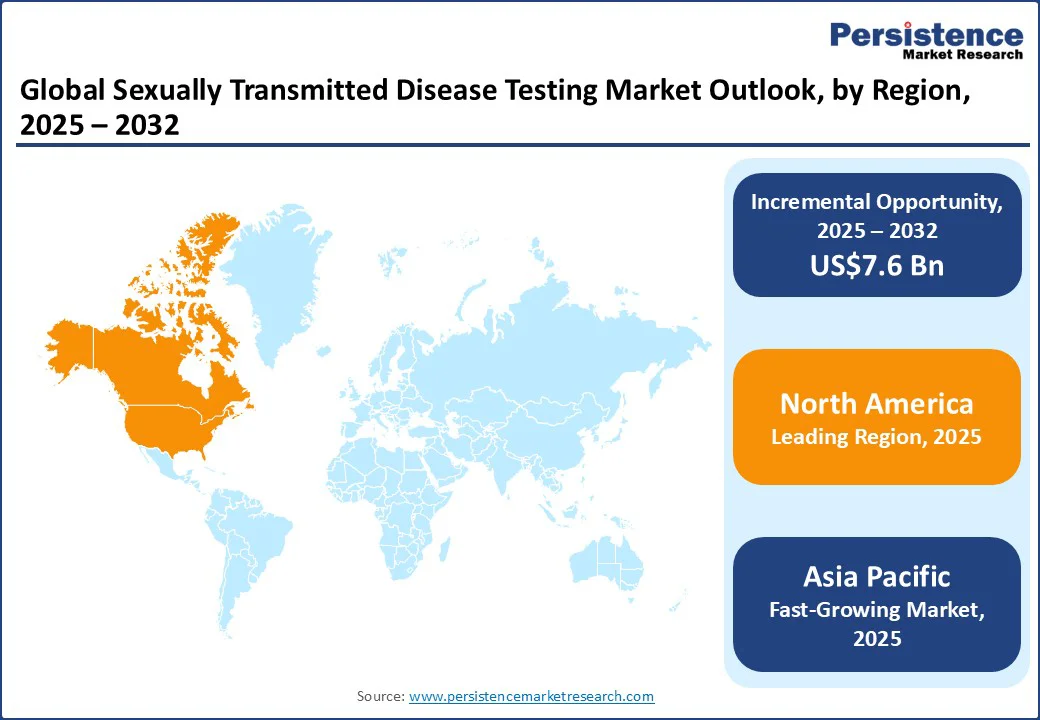

- Key Leading Region: North America, 38.4% market share in 2025, supported by advanced healthcare infrastructure, high awareness, and well-established diagnostic networks.

- Fastest-growing Region: Asia Pacific, driven by rising STD prevalence, growing population, increasing awareness programs, and expanding healthcare access across India, China, and Southeast Asia.

- Investment Plans: Europe, emphasizing advanced diagnostic technologies, public health campaigns, and government support for early STD detection, including funding for molecular diagnostics and point-of-care solutions.

- Dominant Product Type: Test kits, holding over 47.1% market share, fueled by growing demand for reagents, test kits, and approved diagnostic solutions.

- Leading Disease Type: Chlamydia testing, contributing the largest revenue share, due to its high global prevalence and strong public health screening recommendations.

|

Global Market Attribute |

Key Insights |

|

Sexually Transmitted Disease Testing Market Size (2025E) |

US$10.8 Bn |

|

Market Value Forecast (2032F) |

US$18.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.2% |

Market Dynamics

Driver - Rise in Global Prevalence of STDs

The rising global prevalence of sexually transmitted diseases (STDs) is a primary growth driver in the sexually transmitted disease testing market. According to the World Health Organization (WHO), more than one million sexually transmitted infections (STIs) are acquired every day, with around 374 million new cases annually from four curable STDs, including chlamydia, gonorrhea, syphilis, and trichomoniasis.

In the U.S., the Centers for Disease Control and Prevention (CDC) reported over 2.5 million cases of chlamydia, gonorrhea, and syphilis in 2022 alone. Alarming increases in congenital syphilis and antimicrobial-resistant gonorrhea highlight the urgent need for early diagnosis and intervention.

Low- and middle-income countries are also witnessing growing STD burdens, often worsened by poor access to diagnostic services, social stigma, and low awareness. As untreated STDs can lead to severe complications such as infertility, ectopic pregnancy, neonatal death, and increased HIV risks, public health agencies are pushing for broader screening programs and sexual health education.

This rising clinical and public health urgency is directly fueling the demand for reliable, rapid, and cost-effective STD testing technologies, especially point-of-care diagnostics and molecular tests, to enable timely identification and treatment across diverse healthcare settings.

Restraint - Social Stigma and Privacy Concerns

Social stigma and privacy concerns are significant restraints in the growth of the sexually transmitted disease testing market, as they discourage individuals from seeking timely and routine testing. Many people avoid testing due to fear of being judged, discriminated against, or exposed in their communities, especially in conservative or rural settings.

According to the Centers for Disease Control and Prevention (CDC), stigma is one of the leading barriers to STD prevention and care in the U.S., particularly among adolescents, LGBTQ+ individuals, and certain ethnic minorities. The CDC notes that social stigma contributes to delayed testing, resulting in untreated infections and continued transmission.

In India, a study published in the Indian Journal of Sexually Transmitted Diseases and AIDS found that over 40% of participants cited embarrassment and fear of social exposure as primary reasons for avoiding STI clinics. Similarly, the World Health Organization (WHO) highlights stigma as the key reason for underutilization of testing services globally, particularly in low- and middle-income countries. These concerns are compounded by inadequate privacy measures in public clinics and a lack of anonymous testing options, further suppressing market demand despite rising infection rates.

Opportunity - Expansion of At-Home and Self-Testing Kits

The expansion of at-home and self-testing kits represents a major opportunity in the sexually transmitted disease testing market, particularly by addressing stigma, enhancing privacy, and improving access. Home-based sample collection has shown impressive performance; the I Want The Kit (IWTK) program in the U.S. reports 4-7% positivity rates for chlamydia and gonorrhea in mailed-in specimens, with users citing ease, anonymity, and reduced barriers to testing.

In the U.S., the FDA recently cleared the first over-the-counter at-home kit that detects chlamydia, gonorrhea, and trichomoniasis (Visby Medical Women’s Sexual Health Test), demonstrating test accuracy exceeding 97% for all three infections, and delivering results in under 30 minutes. In Australia, the TGA-approved self-test for chlamydia and gonorrhea boasts over 99% sensitivity, meeting stringent regulatory standards.

These kits empower asymptomatic individuals and high-risk groups to test earlier and more discreetly, increasing diagnosis rates without clinic visits. As digital health platforms and telemedicine grow, this channel is poised to reduce stigma-related barriers while improving sexual health outcomes globally.

Category-wise Analysis

Product Type Insights

Test kits are anticipated to be the leading segment with 47.1% share in 2025, due to their accessibility, affordability, and rapid results. According to the CDC, the TakeMeHome program distributed 440,000 HIV self-test kits in one year, more than twice the original goal and higher than all other CDC-supported nonclinical testing combined. Such initiatives show how test kits reach far more people than clinic-based testing.

Moreover, over 10% of self-test users sought additional STI testing, highlighting their role in encouraging broader sexual health care. With more than 2.4 million syphilis, gonorrhea, and chlamydia cases reported in 2023 in the U.S., increasing test coverage is critical. Experts suggest that if self-tests become as routine as pregnancy kits, testing could potentially double or triple nationwide, positioning test kits as the dominant product driving growth in STD testing worldwide.

Disease Type Insights

Chlamydia testing is projected to be the leading segment with a 38.6% share in 2025, due to its high global prevalence and strong public health screening recommendations. According to the World Health Organization (WHO), an estimated 129 million new chlamydia infections occur annually worldwide, making it the most common bacterial sexually transmitted infection. In comparison, the WHO estimates for gonorrhea and syphilis stand at 82 million and 7.1 million cases per year, respectively.

Data from the U.S. Centers for Disease Control and Prevention (CDC) further supports this trend. In 2021, there were over 1.6 million reported chlamydia cases in the U.S. alone, compared with 710,000 gonorrhea and 176,000 syphilis cases.

Since chlamydia is often asymptomatic, especially in women, routine screening is widely recommended for sexually active individuals under 25, driving consistent demand for testing. This combination of high prevalence, silent progression, and public health emphasis positions chlamydia testing as the dominant driver within the STD testing market.

Regional Insights

North America Sexually Transmitted Disease Testing Market Trends

North America is anticipated to be the leading region, holding a market share of 38.4% of the market share in 2025, owing to the high infection burden and the region’s strong public health infrastructure. In the U.S., the CDC reported more than 2.4 million cases of chlamydia, gonorrhea, and syphilis in 2023, making STDs one of the most common infectious disease groups.

Chlamydia remains the most frequently reported notifiable disease, with 1.6 million cases in 2021, followed by gonorrhea (710,000) and syphilis (176,000). Testing demand is reinforced by serious complications, such as 3,882 congenital syphilis cases in 2022, the highest in three decades.

Canada also records significant STD incidence, with rising chlamydia and gonorrhea rates, further boosting testing needs. Together, these trends establish North America’s leadership in the STD testing market through both the scale of cases and advanced testing initiatives.

Europe Sexually Transmitted Disease Testing Market Trends

Europe's STD testing landscape is undergoing a significant transformation. Public health surveillance data show persistent increases in infections such as gonorrhea, syphilis, and chlamydia, driving increased testing demand and urgency for robust diagnostics. In response, innovative testing models, including self-collection kits distributed via pharmacies and at-home channels, are gaining traction, offering privacy, accessibility, and streamlined care through telehealth tie-ins.

Multiplex testing using NAAT is increasingly preferred in laboratories, enabling fast detection of multiple infections from a single sample and improving clinical efficiency. Emerging resistance patterns, particularly antimicrobial resistance in gonorrhea, have prompted the adoption of “test-of-cure” protocols and enhanced surveillance systems to support appropriate treatment strategies across the region. Additionally, national programs in the U.K. have expanded remote testing, offering, such as Preventx’s self-sampling kits, allowing widespread access to routine STD testing in the community.

Competitive Landscape

The global sexually transmitted disease testing market is highly competitive, led by global diagnostic giants such as Abbott, Roche, Hologic, bioMérieux, and BD, which dominate with laboratory-based multiplex NAAT assays and high-throughput platforms.

At the same time, innovators are reshaping the field with consumer-centric solutions. Sherlock Bio is developing a CRISPR-based rapid STI test for 2025, while FDA-approved at-home kits such as LetsGetChecked’s Simple 2 and NOWDiagnostics’ syphilis test expand access. The U.K.-based Preventx further drives growth through large-scale remote self-sampling STI testing programs.

Key Industry Developments:

- In January 2025, Roche announced that it received FDA clearance along with a CLIA waiver for its cobas® liat molecular tests, enabling the rapid diagnosis of sexually transmitted infections (STIs) at the point of care.

- In August 2024, Seegene announced the development of new PCR test assays for detecting mpox shortly after the World Health Organization (WHO) declared the virus a global health emergency. The company stated that the assays were designed to provide accurate and rapid detection, supporting global efforts to contain the outbreak.

- In January 2024, QIAGEN announced that it had received FDA clearance for its NeuMoDx CT/NG Assay, designed for the detection of Chlamydia trachomatis (CT) and Neisseria gonorrhea (NG).

Companies Covered in Sexually Transmitted Disease Testing Market

- BD

- F. Hoffmann-La Roche Ltd

- Hologic Inc.

- Abbott

- Cepheid (Danaher)

- Qiagen

- OraSure Technologies, Inc.

- Bio-Rad Laboratories, Inc.

- bioMérieux SA

- Thermo Fisher Scientific, Inc.

- Seegene Inc.

- DiaSorin S.P.A

- Chembio Diagnostics, Inc.

- Trinity Biotech Plc

- Meridian Bioscience, Inc.

- Binx Health, Inc.

- QuidelOrtho Corporation

Frequently Asked Questions

The sexually transmitted disease testing market is projected to be valued at US$10.8 Bn in 2025.

Rising STD prevalence, early detection demand, technological advances, and government screening initiatives drive global testing.

The sexually transmitted disease testing market is poised to witness a CAGR of 7.9% between 2025 and 2032.

Key opportunities include at-home testing kits, digital health integration, emerging markets, and multiplex molecular diagnostics.

Key players include BD, F. Hoffmann-La Roche Ltd, Hologic Inc., Abbott, Cepheid (Danaher), and Qiagen.