- Automotive Components & Materials

- EV Charging Infrastructure Market

EV Charging Infrastructure Market Size, Share, and Growth Forecast 2026 - 2033

EV Charging Infrastructure Market by Charger Type (Slow Charger, Fast Charger, Hybrid), Application (Commercial: Destination Charging Stations, Highway Charging Stations, Bus Charging Stations, Fleet Charging Stations, Other Charging Stations; Residential: Private Houses, Apartments/Societies), Connector Type (CHAdeMO, CCS, Others), Level of Charging (Level 1, Level 2, Level 3), Operation Outlook (Mode 1, Mode 2, Mode 3, Mode 4), and Regional Analysis for 2026 - 2033

EV Charging Infrastructure Market Size and Trend Analysis

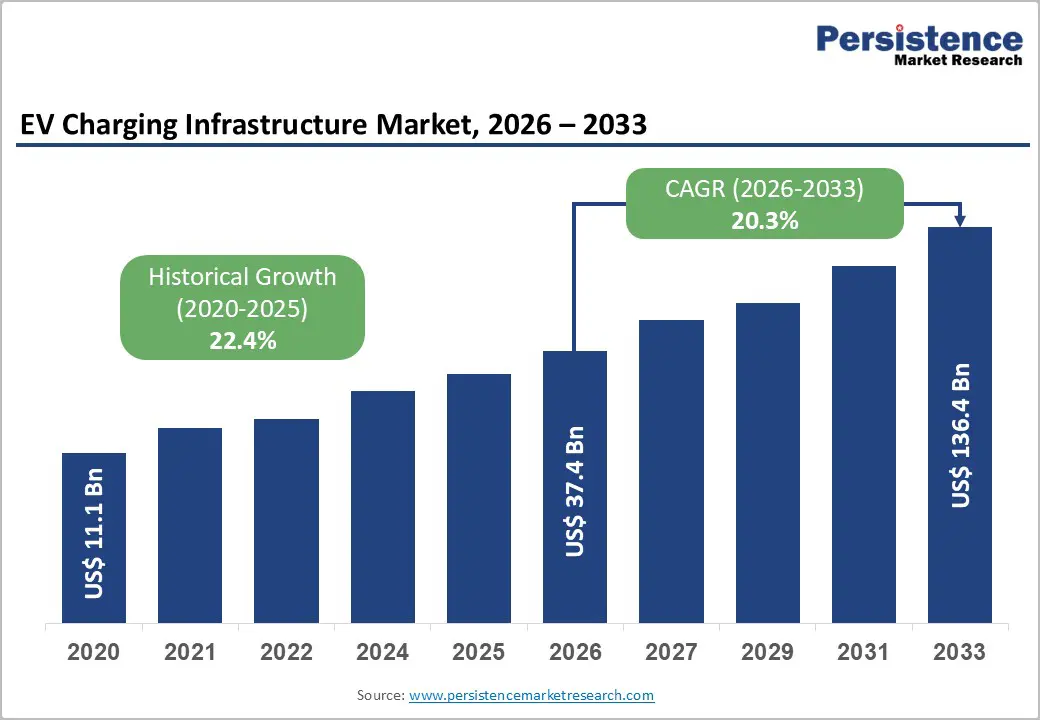

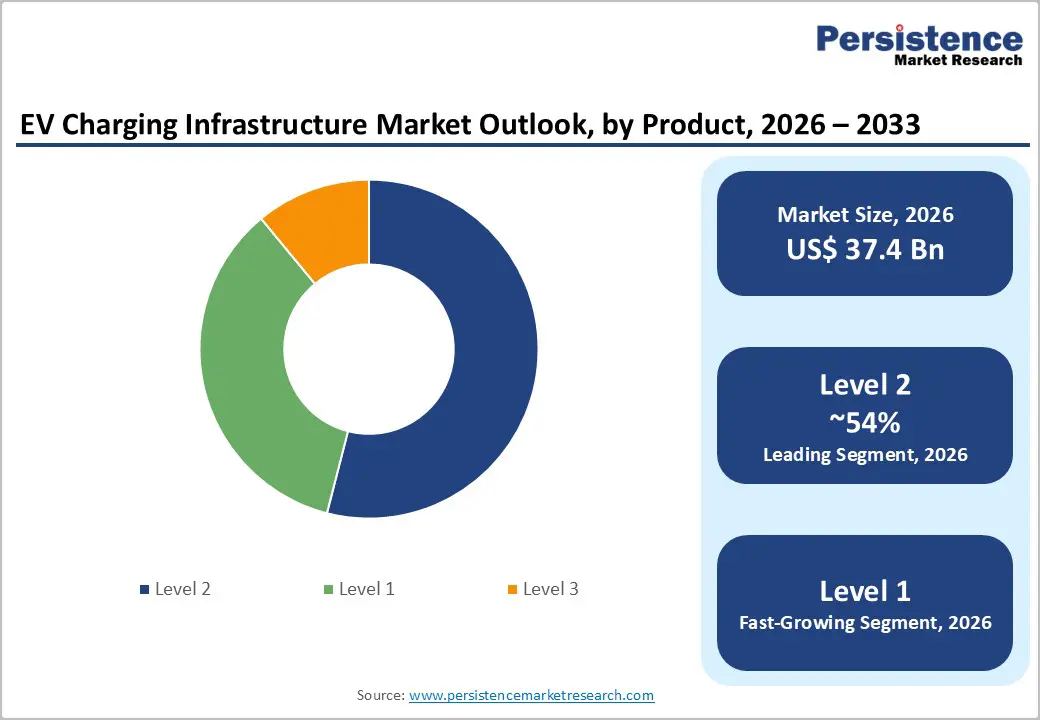

The global EV charging infrastructure market size is expected to be valued at US$ 37.4 billion in 2026 and is projected to reach US$ 136.4 billion by 2033, growing at a CAGR of 20.3% between 2026 and 2033. This robust expansion is primarily driven by accelerating global electric vehicle adoption, stringent government decarbonisation mandates, and surging investments in public and private charging networks.

Regulatory frameworks such as the U.S. Bipartisan Infrastructure Law, which allocated US$ 7.5 Bn for EV charging and the European Union's Alternative Fuels Infrastructure Regulation (AFIR), which mandates charging points every 60 km on the Trans-European Transport Network, are structurally reshaping deployment timelines and instilling long-term investor confidence across all major regions.

Key Industry Highlights:

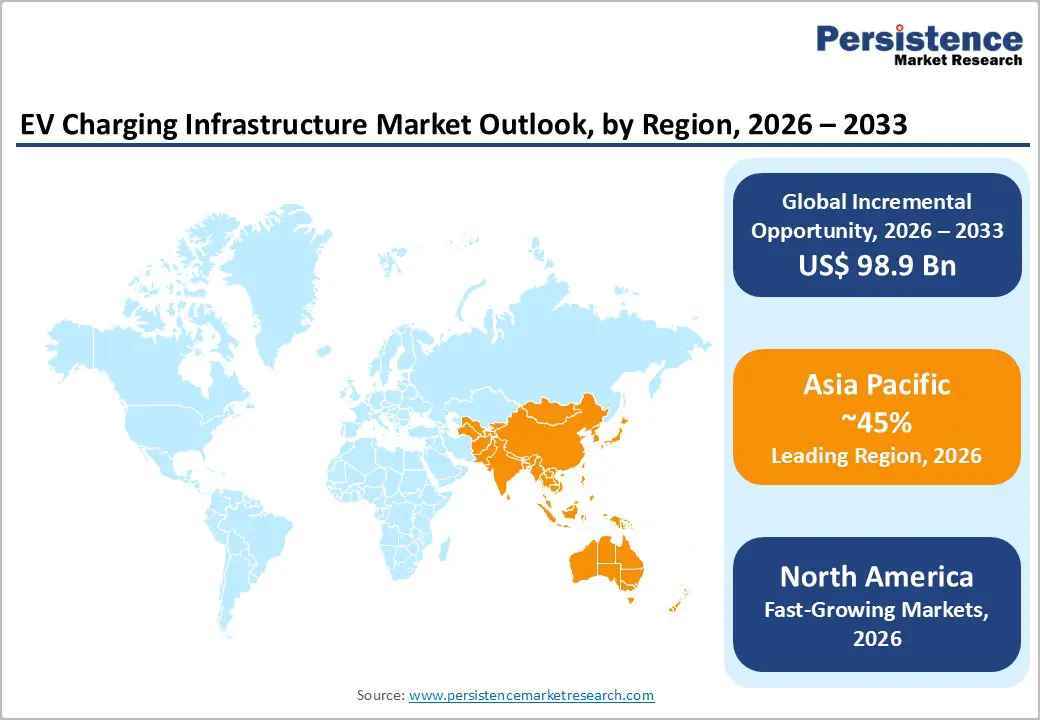

- Leading Region: Asia Pacific dominates the global EV charging infrastructure market with over 45% revenue share in 2025, led by China's unprecedented deployment of over 9.2 million public and private charging points and strong state-backed investment programs.

- Fastest Growing Region: South Asia, particularly India, is the fastest growing regional market with a projected CAGR exceeding 28% through 2033, driven by FAME-II incentives, two- and three-wheeler electrification, and expanding urban charging mandates.

- Dominant Segment: Fast Chargers lead the Charger Type category with approximately 52% market share in 2025, favoured for public and highway charging networks due to their ability to deliver a significant range within 20-40 minutes.

- Fastest Growing Segment: Fleet Charging Stations within the Commercial Application segment represent the fastest growing sub-segment, propelled by logistics giants committing to large-scale electric fleet transitions under tightening EU and U.S. emissions regulations.

- Key Opportunity: Vehicle-to-Grid (V2G) smart charging technology offers transformative revenue potential, enabling EV operators to earn up to €1,500 annually per vehicle through grid services, while creating new business models for utilities and charge point operators.

DRO Analysis

Drivers - Rapid Surge in Electric Vehicle Sales Globally

The single most powerful catalyst propelling the EV charging infrastructure market is the historic surge in global electric vehicle sales. According to the International Energy Agency (IEA), global electric car stock surpassed 40 million units in 2023, with annual sales exceeding 14 million vehicles, representing nearly 18% of all new car sales. The IEA's Net Zero Emissions scenario projects over 300 million EVs on roads by 2030.

This exponential vehicle base expansion creates an inescapable demand multiplier for charging infrastructure: every additional EV on the road necessitates accessible charging points, directly translating into sustained capital deployment across Level 2 and DC fast-charger installations by utilities, automakers, and independent charge point operators.

Government Policy Support and Infrastructure Funding Programs

Governments across major economies are deploying unprecedented fiscal and regulatory tools to accelerate charging network build-out. The U.S. National Electric Vehicle Infrastructure (NEVI) Formula Program commits US$ 5 Bn over five years to create a national network of EV chargers, requiring stations every 50 miles along designated Alternative Fuel Corridors.

Similarly, the European Commission's Green Deal Industrial Plan and individual member-state incentives have spurred over €3.2 Bn in public EV infrastructure commitments through 2025. China's Ministry of Industry and Information Technology (MIIT) mandates one charging pile per EV in new residential buildings.

Restraints - Grid Capacity Constraints and High Infrastructure Installation Costs

A critical barrier limiting broader EV charging infrastructure rollout is the inadequacy of existing electricity grid infrastructure. DC fast chargers can draw between 50 kW to 350 kW per unit, placing severe strain on local distribution networks. According to the U.S. Department of Energy (DOE), grid upgrade costs can represent up to 50% of total charging station installation expenses in underserved areas.

High capital expenditure ranging from US$ 10,000 to US$ 140,000 per DC fast-charger port deters smaller operators from entering the market and slows deployment in rural and semi-urban regions, creating geographic charging deserts that undermine consumer EV adoption confidence.

Lack of Standardisation and Interoperability Challenges

Fragmented technical standards across charging connector types including CHAdeMO, CCS (Combined Charging System), GB/T, and proprietary systems create significant interoperability barriers that impede seamless consumer experiences and complicate network operator planning.

The coexistence of multiple protocols increases hardware procurement costs and driver range anxiety. Although the Society of Automotive Engineers (SAE) is advancing SAE J3400 (NACS) as a unified North American standard, global harmonisation remains years away. These interoperability gaps discourage cross-network roaming, fragment utilisation rates, and reduce the return on investment for independent charge point operators.

Opportunities - Fleet Electrification and Commercial Charging Infrastructure Buildout

The electrification of commercial vehicle fleets represents one of the most transformative near-term opportunities within the EV charging infrastructure market. The European Commission's CO2 Standards for Heavy-Duty Vehicles mandates a 90% reduction in new truck emissions by 2040, while in the U.S., the EPA's Phase 3 greenhouse gas standards target fleet electrification aggressively.

Major logistics companies, including Amazon, UPS, and DHL, have committed to electrifying significant portions of their delivery fleets by 2030. These commitments necessitate purpose-built fleet charging depots featuring high-power Level 3 infrastructure, representing multi-billion-dollar investment opportunities for charge point operators, utilities, and infrastructure developers.

Vehicle-to-Grid (V2G) Technology and Smart Charging Ecosystems

The emergence of Vehicle-to-Grid (V2G) bidirectional charging technology is unlocking a paradigm-shifting revenue stream for market participants. V2G enables EVs to discharge stored energy back to the grid during peak demand, creating a distributed energy resource network. According to the Rocky Mountain Institute (RMI), a V2G-enabled EV fleet could provide up to 200 GW of flexible power capacity in the U.S. by 2030.

Pilot programs by Nissan and Enel X in Europe have demonstrated annual earnings of up to €1,500 per vehicle through grid services. Smart charging software that integrates demand response, dynamic tariff optimisation, and renewable energy scheduling further enhances operator margins, positioning technology-forward charge point operators for superior long-term competitive positioning.

Category-wise Analysis

Charger Type Insights

Among all charger types, the fast charger segment commands the dominant market share, accounting for approximately 52% of the total EV charging infrastructure market in 2025. Fast chargers encompassing DC fast chargers (DCFC) operating at power outputs between 50 kW and 350 kW are rapidly becoming the de facto choice for public charging networks, highway corridors, and commercial fleets due to their ability to deliver significant driving range within 20-40 minutes. Data from the U.S.

Alternative Fuels Data Centre (AFDC) confirms that DC fast-charger installations in the U.S. alone grew by over 40% year-over-year in 2023. The segment's leadership is further reinforced by falling DCFC hardware costs, consumer demand for convenience, and automaker investments in proprietary ultra-fast charging networks.

Application Insights

The commercial segment leads the application category, representing an estimated 65% of total market revenue in 2025. Within commercial applications, Highway Charging Stations and Fleet Charging Stations are the fastest expanding sub-segments. Highway charging is structurally underpinned by regulatory mandates such as the NEVI program in the U.S. and AFIR in Europe, both of which prioritise corridor coverage as a prerequisite for mass EV adoption.

Fleet charging captures premium revenue from logistics and public transit operators who require guaranteed uptime and high-throughput depot infrastructure. According to Bloomberg NEF, commercial charging stations generate on average 3-5× higher utilisation rates compared to residential installations, underpinning their superior revenue-generating capability and dominant market share.

Connector Type Insights

The CCS (Combined Charging System) connector type leads the global market with a dominant share of approximately 58% in 2025, underpinned by broad OEM adoption across European and North American markets. CCS supports both AC and DC charging through a single inlet, offering unmatched versatility and scalability for high-power applications.

Crucially, the CharIN (Charging Interface Initiative) consortium, backed by over 200 industry members including BMW, Volkswagen, Ford, and General Motors, has standardised CCS as the preferred global protocol. Further cementing its lead, major North American automakers have committed to transitioning to NACS (SAE J3400), which retains CCS compatibility. Meanwhile, CHAdeMO's market presence is declining as Japanese automakers pivot toward emerging standards, further entrenching CCS's structural dominance.

Level of Charging Insights

Level 2 charging holds the leading position within the Level of Charging category, representing nearly 54% of installed charging points globally in 2025. Operating at 208-240V AC with power outputs of 3.3 kW to 22 kW, Level 2 chargers strike the optimal balance between cost-effectiveness and utility, making them the standard for workplace charging, destination charging at retail and hospitality venues, and urban residential installations.

The Electric Power Research Institute (EPRI) reports that Level 2 chargers represent over 80% of all non-residential charger installations in the U.S. market. Their relatively modest installation costs of US$ 2,500-US$ 7,500 per port, broad vehicle compatibility, and compatibility with standard commercial electrical services make Level 2 the workhorse of the global charging ecosystem.

Operation Outlook Insights

Mode 3 charging, defined under IEC 61851 as AC charging with a dedicated EV supply equipment connection to the AC grid with control pilot functions, commands the leading share in the Operation Outlook category, accounting for approximately 49% of the addressable market in 2025. Mode 3 is the foundation for all public and semi-public smart charging infrastructure, enabling real-time communication between the vehicle, charging station, and energy management systems.

The protocol's inherent support for smart grid integration, dynamic load management, and OCPP (Open Charge Point Protocol) compatibility makes it indispensable for fleet and commercial operators. IEC 61851-1:2017 and the evolving ISO 15118 standard for Plug & Charge communication are further institutionalising Mode 3 as the preferred operational paradigm for next-generation charging networks.

Regional Analysis

North America EV Charging Infrastructure Market Trends & Analysis

North America represents the second-largest regional market for EV charging infrastructure globally, with the market projected to grow at a CAGR of approximately 19.8% during 2026 - 2033. The region's growth is anchored by the landmark Bipartisan Infrastructure Law (BIL) of 2021, which allocated US$ 7.5 Bn to create a national charging network under the NEVI program. As of mid-2024, the U.S. Federal Highway Administration (FHWA) has approved infrastructure plans for all 50 states, with deployments accelerating across interstate corridors.

U.S. EV Charging Infrastructure Market Size

The U.S. market is projected to account for approximately US$ 18.5 Bn in 2026 and reach US$ 78.0 Bn by 2033, driven by NEVI-funded deployments, utility-led infrastructure programs, and surging fleet electrification commitments from major logistics and rideshare operators.

Europe EV Charging Infrastructure Market Trends, Drivers, & Insights

Europe is the most regulated and policy-driven EV charging market globally. The EU's Alternative Fuels Infrastructure Regulation (AFIR) mandates that every 60 km along the Trans-European Transport Network (TEN-T) must have public fast-charging pools with a combined output of at least 300 kW per pool by 2025, scaling to 1,200 kW by 2027. As of 2024, the European Automobile Manufacturers' Association (ACEA) reports that Europe houses over 630,000 public charging points but estimates a requirement of over 3.4 million by 2030.

Germany EV Charging Infrastructure Market Size

Germany's market is valued at approximately US$ 3.2 Bn in 2026, underpinned by the Federal Network Agency's Ladesäulenregister registering over 100,000 public charge points as of late 2023, with aggressive expansion targets set by the coalition government to reach 1 million public chargers by 2030.

U.K. EV Charging Infrastructure Market Size

The U.K. market is projected at US$ 2.4 Bn in 2026, supported by the Zero Emission Vehicle (ZEV) Mandate, which requires 80% of new car sales to be zero-emission by 2030, and government funding under the Electric Vehicle Infrastructure Strategy targeting 300,000 public chargers by 2030.

France EV Charging Infrastructure Market Size

France's market stands at approximately US$ 1.9 Bn in 2026. The government's France 2030 investment plan and obligations under the Loi orientation des Mobilities (LOM) are accelerating deployments, with France targeting over 400,000 public charge points by 2030 across motorway and urban networks.

Asia Pacific EV Charging Infrastructure Market Drivers & Analysis

Asia Pacific dominates the global EV charging infrastructure market, commanding over 45% of global market revenue in 2025, fuelled overwhelmingly by China's extraordinary deployment velocity and supportive state policies. According to the China Electricity Council (CEC), China surpassed 9.2 million public and private charging points by the end of 2023, adding over 3.5 million in 2023 alone.

China EV Charging Infrastructure Market Size

China's market is estimated at approximately US$ 8.5 Bn in 2026, forecast to reach US$ 37.2 Bn by 2033. The National Development and Reform Commission (NDRC)'s charging infrastructure guidelines and State Grid Corporation investments continue to underpin China's global leadership.

India EV Charging Infrastructure Market Size

India is one of the fastest-growing EV charging markets, valued at US$ 600 Mn in 2026 and forecast to grow at a leading CAGR driven by FAME-II and PM e-DRIVE scheme incentives, Bureau of Energy Efficiency (BEE) charging standards, and aggressive two- and three-wheeler electrification.

Japan EV Charging Infrastructure Market Size

Japan's market is projected at approximately US$ 1.1 Bn in 2026. The Japanese government's target of 150,000 public fast chargers and 300,000 normal chargers by 2030 under the Green Growth Strategy is redirecting infrastructure investment, even as the market navigates a transition from CHAdeMO toward emerging global standards.

Competitive Landscape

The global EV charging infrastructure market exhibits a moderately fragmented competitive structure, with a blend of large utility conglomerates, specialised charge point operators, and automotive OEM-backed networks competing for market share. Leading players such as ABB Ltd., ChargePoint Holdings, Inc., BP Pulse, and IONITY GmbH are pursuing aggressive network expansion through utility partnerships, motorway concession agreements, and software platform integrations.

Market leaders are differentiating through proprietary smart charging software, open-protocol interoperability, and energy management services. Consolidation is accelerating, with strategic M&A activity evident across the value chain.

Key Market Developments

- In December 2025, V-GREEN signed a strategic agreement with Hindustan Petroleum Corporation Limited, a state-owned oil firm with 24,400+ retail outlets and 5,300+ HP e-Charge stations, to deploy EV charging stations (EVCS) at select HPCL fuel outlets nationwide.

- In January 2025, Tata Power Renewable Energy Limited, an arm of Tata Power's expansive EZ Charge network, partnered with Tivolt Electric Vehicles, Murugappa Group's EV venture under TI Clean Mobility, to deploy EV charging infrastructure for small commercial vehicles at Tivolt dealerships, customer sites, and high-traffic public areas nationwide.

EV Charging Infrastructure Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 11.1 Bn |

| Current Market Value (2026) | US$ 37.4 Bn |

| Projected Market Value (2033) | US$ 136.4 Bn |

| CAGR (2026 - 2033) | 20.3% |

| Leading Region | Asia Pacific, 45% share |

| Dominant Application | Level 2, 54% share |

| Top-ranking Product | Commercial segment, 65% |

| Incremental Opportunity | US$ 98.9 Bn |

Companies Covered in EV Charging Infrastructure Market

- UFI Filters

- ABB Ltd.

- ChargePoint Holdings, Inc.

- BP Pulse

- IONITY GmbH

- Blink Charging Co.

- EVgo Services LLC

- Schneider Electric SE

- Siemens AG

- Eaton Corporation plc

- Webasto Group

- Wallbox N.V.

- BTC Power

- Kempower Oyj

- Tritium DCFC Limited

- ENGIE SA

- Shell Recharge Solutions

- Electrify America LLC

- Allego B.V.

- Zaptec AS

Frequently Asked Questions

The global EV Charging Infrastructure market is expected to be valued at US$ 37.4 Bn in 2026 and is projected to reach US$ 136.4 Bn by 2033, growing at a CAGR of 20.3% during the forecast period.

The market is primarily driven by the exponential growth in global electric vehicle sales exceeding 14 million units in 2023 per IEA data combined with landmark government funding programs such as the U.S. NEVI Formula Program (US$ 5 Bn) and the EU's AFIR mandates.

The Fast Charger segment is the dominant charger type, accounting for approximately 52% of the global EV charging infrastructure market in 2025. Fast chargers, particularly DC fast chargers operating between 50 kW and 350 kW, are the preferred choice for public networks and highway corridors due to their ability to deliver substantial driving range within 20-40 minutes.

Asia Pacific is the leading region in the EV Charging Infrastructure market, holding over 45% of global market revenue in 2025. China is the primary contributor, having surpassed 9.2 million public and private charging points by end-2023, supported by extensive government investment through the National Development and Reform Commission (NDRC) and the China Electricity Council frameworks.

The key companies operating in the EV Charging Infrastructure market include ABB Ltd., ChargePoint Holdings Inc., BP Pulse, IONITY GmbH, Blink Charging Co., EVgo Services LLC, Schneider Electric SE, Siemens AG, Wallbox N.V., Tritium DCFC Limited, Shell Recharge Solutions, and Electrify America LLC, among others.